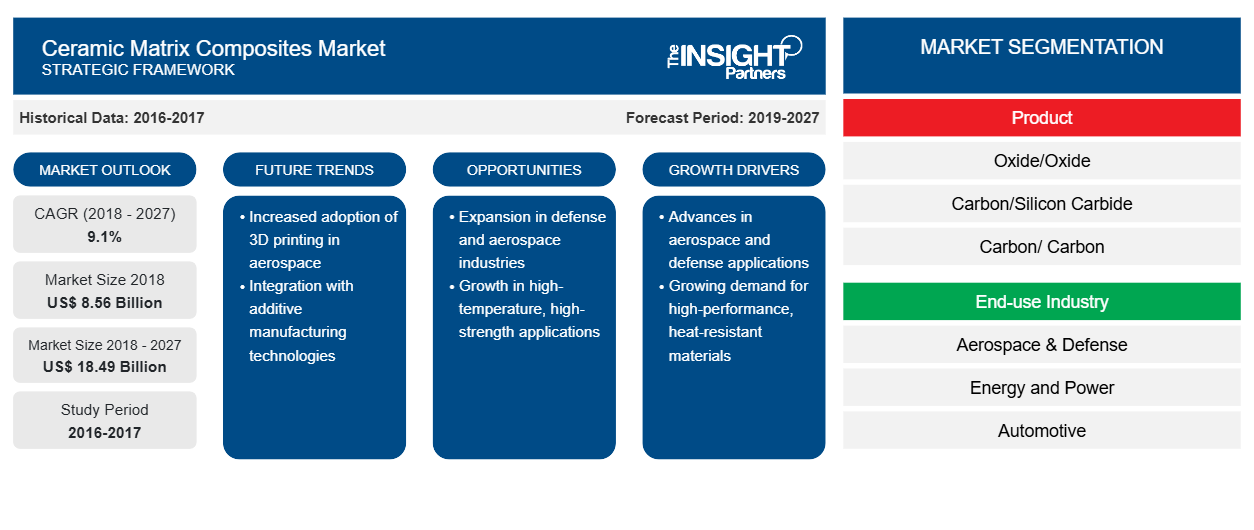

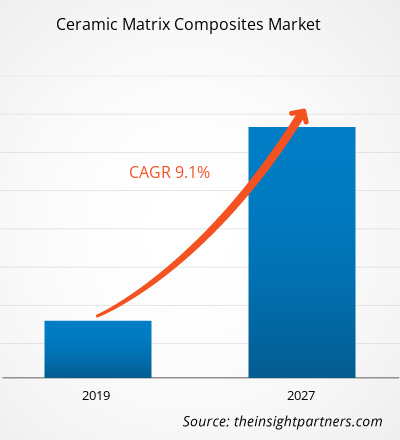

[تقرير بحثي] بلغت قيمة سوق مركبات المصفوفة الخزفية 8,560.0 مليون دولار أمريكي في عام 2018 ومن المتوقع أن تنمو بمعدل نمو سنوي مركب قدره 9.1٪ خلال الفترة المتوقعة 2019-2027، لتصل إلى 18,485.0 مليون دولار أمريكي بحلول عام 2027.

تحليل السوق

تشير المركبات ذات المصفوفة الخزفية (CMCs) إلى فئة من المواد المتقدمة التي تجمع بين الألياف أو الجسيمات الخزفية مع مصفوفة خزفية لإنشاء مادة مركبة عالية الأداء. تم تصميم هذه المركبات للاستفادة من الخصائص المرغوبة لكل من الألياف/الجسيمات المقوية والمصفوفة الخزفية لتحقيق قوة ميكانيكية محسنة واستقرار حراري وخصائص محسنة أخرى مقارنة بالمواد الخزفية التقليدية. تجعل الخصائص الميكانيكية للمركبات ذات المصفوفة الخزفية مثل مقاومة الحرارة العالية وقوة الشد جزءًا مهمًا من قطاعات السيارات والدفاع والفضاء الجوي. ومن المتوقع أن يوفر ارتفاع قاعدة التطبيق في مختلف الصناعات النهائية الفرصة لنمو سوق المركبات ذات المصفوفة الخزفية.

محركات النمو والتحديات

ينبع الطلب المتزايد على مركبات المصفوفة الخزفية (CMCs) في الصناعات الناشئة من خصائصها الفريدة التي تتوافق مع متطلبات هذه القطاعات. في مجال الطاقة المتجددة ، تجد مركبات المصفوفة الخزفية تطبيقات في توربينات الرياح وأنظمة الطاقة الشمسية، حيث تساعد طبيعتها خفيفة الوزن على تحسين كفاءة الطاقة وخفض التكاليف. بالإضافة إلى ذلك، فإن أداء مركبات المصفوفة الخزفية في درجات الحرارة العالية يجعلها مناسبة للاستخدام في محطات الطاقة الشمسية المركزة وأنظمة الطاقة الحرارية الأرضية. في صناعة المركبات الكهربائية، تقدم مركبات المصفوفة الخزفية حلولاً خفيفة الوزن وعالية القوة لمكونات مثل أغلفة البطاريات وأغلفة المحرك وأنظمة الفرامل، مما يساهم في تطوير مركبات كهربائية أكثر كفاءة واستدامة. إن تعدد استخدامات مركبات المصفوفة الخزفية يجعلها خيارًا واعدًا للمواد في هذه الصناعات الناشئة، مما يدفع نمو سوق مركبات المصفوفة الخزفية .

ومع ذلك، فإن التكلفة العالية للمواد المركبة ذات المصفوفة الخزفية تعمل كقيد كبير على نمو سوق المواد المركبة ذات المصفوفة الخزفية. تساهم عمليات التصنيع المعقدة والمتخصصة المشاركة في إنتاج المواد المركبة ذات المصفوفة الخزفية، بما في ذلك إنتاج الألياف، وإعداد المصفوفة، وتصنيع المركبات، في ارتفاع تكاليف الإنتاج مقارنة بالمواد التقليدية. وتحد هذه التكلفة الإضافية من التبني الواسع النطاق للمواد المركبة ذات المصفوفة الخزفية، وخاصة في الصناعات التي تعطي الأولوية للفعالية من حيث التكلفة. كما تفرض التكلفة العالية تحديات على الشركات المصنعة الأصغر حجمًا أو الشركات ذات الموارد المحدودة، حيث قد تجد صعوبة في الاستثمار في المعدات والخبرة اللازمة لإنتاج المواد المركبة ذات المصفوفة الخزفية. وعلاوة على ذلك، فإن قابلية التوسع المحدودة لعمليات إنتاج المواد المركبة ذات المصفوفة الخزفية تحد بشكل أكبر من توفرها بكميات كبيرة، مما يجعلها أقل سهولة في الوصول إليها وبأسعار معقولة للمستخدمين المحتملين. ونتيجة لذلك، تعمل التكلفة العالية للمواد المركبة ذات المصفوفة الخزفية كحاجز أمام نمو سوق المواد المركبة ذات المصفوفة الخزفية.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق مركبات المصفوفة السيراميكية:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه

"تحليل سوق مركبات المصفوفة الخزفية العالمية حتى عام 2027" هو دراسة متخصصة ومتعمقة مع التركيز الرئيسي على اتجاهات سوق مركبات المصفوفة الخزفية العالمية وفرص النمو. يهدف التقرير إلى تقديم نظرة عامة على سوق مركبات المصفوفة الخزفية العالمية مع تقسيم السوق التفصيلي حسب المنتج وصناعة الاستخدام النهائي والجغرافيا. شهد سوق مركبات المصفوفة الخزفية العالمية نموًا مرتفعًا خلال الماضي القريب ومن المتوقع أن يستمر هذا الاتجاه خلال فترة التنبؤ. يقدم التقرير إحصائيات رئيسية عن استهلاك مركبات المصفوفة الخزفية في جميع أنحاء العالم جنبًا إلى جنب مع الطلب عليها في المناطق والبلدان الرئيسية. بالإضافة إلى ذلك، يقدم التقرير تقييمًا نوعيًا للعوامل المختلفة التي تؤثر على أداء سوق مركبات المصفوفة الخزفية في المناطق والبلدان الرئيسية. يتضمن التقرير أيضًا تحليلًا شاملاً للاعبين الرائدين في سوق مركبات المصفوفة الخزفية وتطوراتهم الاستراتيجية الرئيسية. يتم أيضًا تضمين العديد من التحليلات حول ديناميكيات السوق للمساعدة في تحديد العوامل الدافعة الرئيسية واتجاهات السوق وفرص سوق مركبات المصفوفة الخزفية المربحة والتي من شأنها بدورها أن تساعد في تحديد جيوب الإيرادات الرئيسية.

علاوة على ذلك، يوفر تحليل النظام البيئي وتحليل القوى الخمس لبورتر رؤية بزاوية 360 درجة لسوق مركبات المصفوفة السيراميكية العالمية، مما يساعد على فهم سلسلة التوريد بأكملها والعوامل المختلفة التي تؤثر على نمو السوق.

التحليل القطاعي

يتم تقسيم سوق مركبات المصفوفة الخزفية العالمية على أساس المنتج وصناعة الاستخدام النهائي. بناءً على المنتج، يتم تقسيم سوق مركبات المصفوفة الخزفية إلى أكاسيد/أكسيد، وكربيد السيليكون/كربيد السيليكون، وكربون/كربيد السيليكون، وكربون/كربون. بناءً على صناعة الاستخدام النهائي، يتم تصنيف سوق مركبات المصفوفة الخزفية على أنها، الفضاء والدفاع، والطاقة والكهرباء، والسيارات، والصناعة، وغيرها.

استنادًا إلى المنتج، استحوذ قطاع الأكاسيد/الأكسيد على حصة سوقية كبيرة من مركبات المصفوفة الخزفية في عام 2022. تلعب مركبات المصفوفة الخزفية المكونة من أكاسيد/أكسيد دورًا مهمًا في دفع نمو السوق. توفر هذه المركبات مزايا فريدة مثل الاستقرار الحراري الممتاز ومقاومة درجات الحرارة العالية والخصائص الميكانيكية المحسنة. تعمل الأكاسيد، مثل أكسيد الألومنيوم (Al2O3) وأكسيد الزركونيوم (ZrO2)، كمصفوفة خزفية في هذه المركبات، بينما تعمل الألياف القائمة على الأكسيد، مثل ألياف الألومينا، على تعزيز البنية. تجد مركبات المصفوفة الخزفية المكونة من أكاسيد/أكسيد تطبيقات واسعة النطاق في صناعات مثل الفضاء والدفاع والطاقة، حيث تكون خصائصها الحرارية الاستثنائية ومتانتها أمرًا بالغ الأهمية. يتم استخدامها في الأقسام الساخنة لمحركات التوربينات الغازية وطلاءات الحاجز الحراري والمكونات عالية الحرارة في الطائرات واستكشاف الفضاء. إن الطلب المتزايد على المواد عالية الأداء القادرة على تحمل درجات الحرارة القصوى والبيئات القاسية يدفع إلى اعتماد مركبات CMC المكونة من أكسيد/أكسيد، مما يؤدي إلى توسيع سوق المركبات ذات المصفوفة السيراميكية وفرص النمو.

التحليل الإقليمي

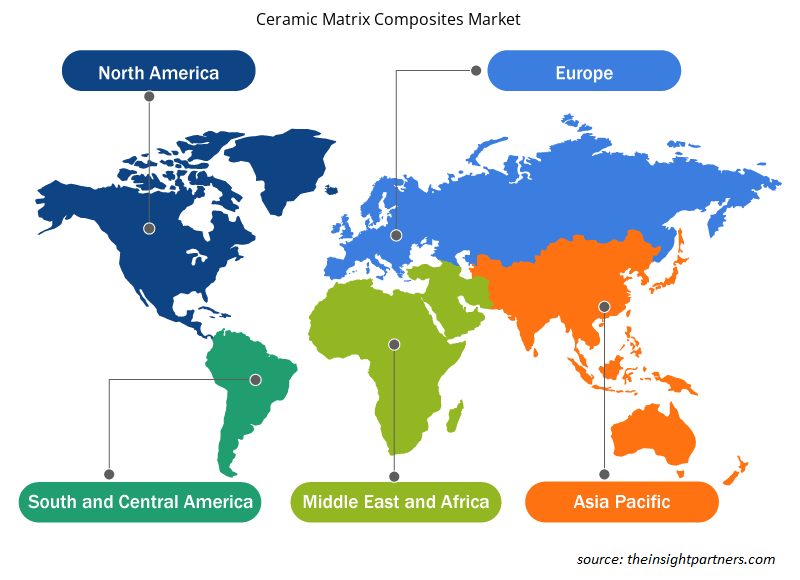

يقدم التقرير نظرة عامة مفصلة على سوق مركبات المصفوفة الخزفية العالمية فيما يتعلق بخمس مناطق رئيسية، وهي؛ أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ (APAC) والشرق الأوسط وأفريقيا (MEA) وأمريكا الجنوبية والوسطى. سيطرت منطقة أمريكا الشمالية على سوق مركبات المصفوفة الخزفية، حيث حققت إيرادات تزيد عن 4500 مليون دولار أمريكي في عام 2022. تتمتع أمريكا الشمالية بحضور قوي للصناعات الرئيسية التي تستخدم على نطاق واسع مركبات المصفوفة الخزفية، مثل الفضاء والدفاع والطاقة. تتمتع هذه الصناعات بطلب كبير على المواد المتقدمة ذات الخصائص الفائقة، بما في ذلك الوزن الخفيف والقوة العالية والاستقرار الحراري، والتي يمكن أن توفرها مركبات المصفوفة الخزفية. من المتوقع أن تصل إيرادات سوق مركبات المصفوفة الخزفية في أوروبا إلى أكثر من 7300 مليون دولار أمريكي في عام 2028. اكتسبت صناعة مركبات المصفوفة الخزفية مكانة مهمة في الاقتصاد الأوروبي، مما عزز النمو والابتكار والتوظيف. ترتبط مركبات المصفوفة الخزفية ارتباطًا وثيقًا بمختلف القطاعات الصناعية مثل صناعات الدفاع والفضاء والطاقة والكهرباء والإلكترونيات. من المتوقع أن ينمو سوق مركبات المصفوفة الخزفية في منطقة آسيا والمحيط الهادئ بمعدل نمو سنوي مركب كبير يزيد عن 10٪. وتشهد بلدان المنطقة ارتفاعًا في عدد السكان بالإضافة إلى النمو في التحضر، مما يوفر فرصًا واسعة للاعبين الرئيسيين في سوق CMC.

تطورات الصناعة والفرص المستقبلية

وُجِد أن الشراكة والاستحواذات وإطلاق المنتجات الجديدة هي الاستراتيجيات الرئيسية التي يتبناها اللاعبون العاملون في سوق مركبات المصفوفة الخزفية العالمية.

- في عام 2019، مددت شركة SGL Carbon عقدها مع شركة Elbe Flugzeugwerke لتوريد منسوجات ألياف الكربون المشبعة لاستخدامها في ألواح أرضيات مقصورة طائرة إيرباص A350 حتى نهاية عام 2020.

- في أبريل 2023، أعلنت شركة SGL Carbon عن شراكة جديدة مع شركة Lancer Systems لتطوير مركبات المصفوفة الخزفية لاستخدامها في أنظمة الحماية الحرارية.

- في يناير 2023، وقعت شركة رولز رويس مذكرة تفاهم مع جامعة شيفيلد في المملكة المتحدة للتعاون في تطوير مواد مركبة جديدة من مصفوفة السيراميك.

رؤى إقليمية حول سوق مركبات المصفوفة الخزفية

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق مركبات المصفوفة الخزفية طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق مركبات المصفوفة الخزفية والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق مركبات المصفوفة الخزفية

نطاق تقرير سوق مركبات المصفوفة السيراميكية

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2018 | 8.56 مليار دولار أمريكي |

| حجم السوق بحلول عام 2027 | 18.49 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2018 - 2027) | 9.1% |

| البيانات التاريخية | 2016-2017 |

| فترة التنبؤ | 2019-2027 |

| القطاعات المغطاة | حسب المنتج

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

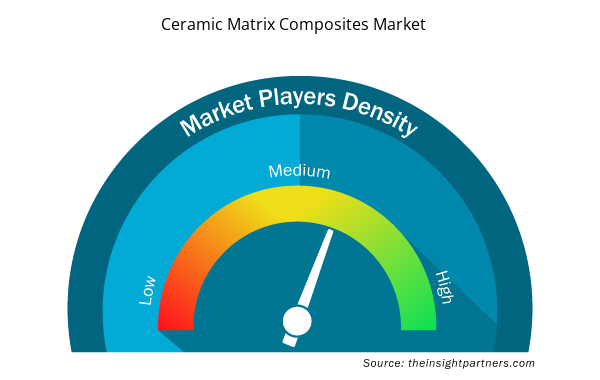

كثافة اللاعبين في سوق مركبات المصفوفة الخزفية: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق مركبات المصفوفة الخزفية نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق مركبات المصفوفة السيراميكية هي:

- شركة سي أو آي للسيراميك

- شركة جنرال الكتريك

- أنظمة لانسر

- اس جي ال كاربون

- شركة رولز رويس المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق مركبات المصفوفة الخزفية

تأثير كوفيد

كان لوباء كوفيد-19 تأثيرًا كبيرًا على سوق مركبات المصفوفة الخزفية (CMCs)، مما تسبب في حدوث اضطرابات وإعاقة نمو السوق. أدى الوباء إلى انتشار حالة من عدم اليقين الاقتصادي على نطاق واسع، وانقطاعات في سلسلة التوريد، وتقليص الأنشطة الصناعية في مختلف القطاعات. واجهت العديد من صناعات المستخدم النهائي لمركبات المصفوفة الخزفية، مثل صناعة الطيران والسيارات والطاقة، انتكاسات كبيرة، بما في ذلك توقف الإنتاج وتأخير المشاريع وانخفاض الاستثمارات. كما أثرت القيود المفروضة على السفر والتجارة على الطلب على مركبات المصفوفة الخزفية في الأسواق العالمية. وعلاوة على ذلك، أدت القيود المالية التي تواجهها الشركات والتركيز على تدابير خفض التكاليف إلى انخفاض الإنفاق الرأسمالي والنهج الحذر تجاه تبني المواد المتقدمة مثل مركبات المصفوفة الخزفية. وعلى الرغم من أنه من المتوقع أن يتعافى السوق تدريجيًا مع إعادة فتح الاقتصادات واستئناف الأنشطة الصناعية، إلا أن جائحة كوفيد-19 أعاقت بالتأكيد مسار نمو سوق مركبات المصفوفة الخزفية في الأمد القريب.

المشهد التنافسي والشركات الرئيسية

تشمل بعض اللاعبين الرئيسيين العاملين في سوق مركبات المصفوفة الخزفية شركة COI Ceramics، Inc.؛ وGeneral Electric Company؛ وLancer Systems؛ وSGL Carbon؛ وRolls-Royce Plc؛ وCoorsTek، Inc.؛ وApplied Thin Films Inc.؛ وUltramet؛ وCFCCARBON CO، LTD؛ وMatech وغيرها.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

Global ceramic matrix composites market in oxides product is expected to grow at a CAGR of 8.7% during the forecast period 2019 – 2027.

The oxides ceramic matrix composites are gaining increasing importance as a mainstream material alternative for the high-temperature components, mainly in the industrial, advanced energy and aerospace sectors. These materials are known to compete with other alternatives such as titanium in terms of cost-reductions. The oxide ceramic matrix composites have significant potential in the oxidation sensitive component applications. The demand for oxide ceramic matrix composites has been growing considerably in the aerospace sector for turbine engines and other high-temperature components. The oxide ceramic matrix composites have excellent thermal and mechanical properties coupled with damage-tolerant quasi ductile fracture behavior, which has been a significant factor for its application in the high temperature processes. Another supporting factor that has led to increasing demand for the oxide-ceramic matrix composites is its low weight and prolonged service lifetime. The oxide-ceramic matrix composites components such as changing racks, lift gates, or flame tubes have represented their potential in varied industrial high-temperature applications. The O-ceramic matrix composites components for gas turbines are currently being tested and developed. The oxide-ceramic matrix composites are light in weight due to their reduced density and mass. The increase in thermal efficiency and reduced maintenance cost have been a contributing factor to favor the oxide-ceramic matrix composites market all over the globe.

Ceramic Matrix Composites (CMC) are the materials consisting of a ceramic matrix combined with ceramic oxides or carbides. Ceramic materials are inorganic and nonmetallic solids, which are crystalline. They exhibit improved crack resistance and do not rupture easily under heavy loads as compared to conventional technical ceramics. Ceramic matrix composites reinforced by either continuous long fibers or discontinuous short fibers. High mechanical strength, high stiffness, high thermal and shock resistance, high thermal stability, high corrosion resistance, and lightweight making them suitable for the number of applications in aerospace & defense, automotive, energy, and power industries.

These favorable characteristics of the ceramic matrix composites is helping the product to grow and is being considered in a wide range of end user industry.

The North American region led the ceramic matrix composites market in 2018. North America comprises developed and developing countries such as the US, Canada, and Mexico. North America will account for a remarkable share in the ceramic matrix composites market owing to the rigorous growth of aerospace and defense spending in the region. Over the forecast period, the commercial aerospace sector is also expected to gain significant movement. Rigorous research and development activities by the United States Environmental Protection Agency (USEPA) for developing renewable energy sources are expected to create lucrative opportunities for ceramic matrix composites market in the region. Further, North America region has the existence of several ceramic matrix composite manufacturers such as COI Ceramics, INC. and Applied Thin Films, Inc., which are mainly focused on the adoption of various business strategies for increasing their production capacity.

The List of 10 Companies - Ceramic Matrix Composites Market

- COI Ceramics, Inc.

- General Electric Company

- Lancer Systems

- SGL Carbon

- Rolls-Royce Plc

- Coorstek, Inc.

- Applied Thin Films Inc.

- Ultramet

- CFC Carbon Co,. Ltd

- Matech

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير