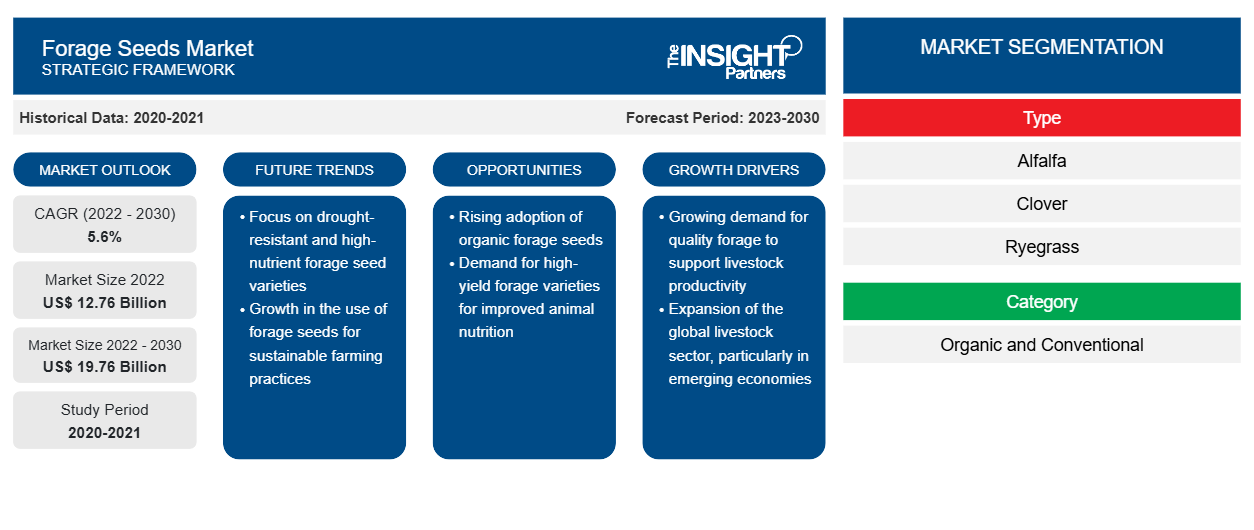

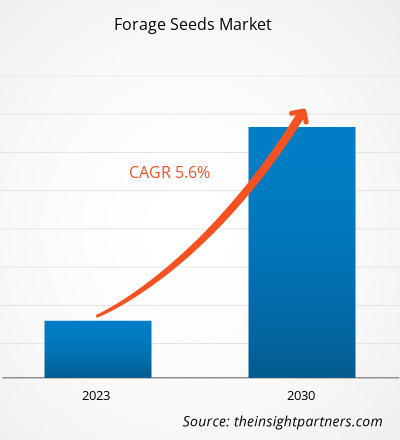

[تقرير بحثي] من المتوقع أن ينمو السوق من 12،757.00 مليون دولار أمريكي في عام 2022 إلى 19،755.46 مليون دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 5.6٪ من عام 2022 إلى عام 2030.

رؤى السوق ووجهة نظر المحلل:

غالبًا ما تحتوي الأعلاف التقليدية على كميات عالية من المواد الكيميائية التي تعوق جودة اللحوم عند استهلاكها من قبل الحيوانات. على المدى الطويل، يؤدي استهلاك مثل هذه اللحوم إلى اضطرابات صحية مختلفة. للتغلب على هذه المشكلة، يعمل المصنعون على تطوير أعلاف عضوية لا تحتوي على إضافات كيميائية. تقدم الحيوانات التي تتغذى على مثل هذه الأعلاف لحومًا ذات قيمة غذائية عالية. وبالتالي، غالبًا ما يجد المستهلكون المنتجات العضوية والطبيعية بدائل أكثر صحة للمنتجات التقليدية. يميل المستهلكون بشكل أساسي إلى المنتجات العضوية، مما شجع المصنعين على الاستثمار بكثافة في المنتجات المنتجة بمكونات عضوية. علاوة على ذلك، أدى الوصول الأكثر سهولة إلى المعلومات اللانهائية بمساعدة الإنترنت إلى زيادة وعي المستهلكين باحتياجاتهم الصحية، مما أدى إلى زيادة الطلب على الأعلاف العضوية. وبالتالي، من المتوقع أن يصبح التفضيل المتزايد للأعلاف العضوية اتجاهًا مهمًا في سوق بذور العلف خلال فترة التنبؤ.

محركات النمو والتحديات:

تقدم التحسينات التكنولوجية في علم الوراثة للبذور فرصة لنمو سوق بذور الأعلاف العالمية. طور مصنعو البذور أصنافًا أو سمات مختلفة من البذور، مثل البذور الهجينة، والبذور المعدلة وراثيًا، وغير المعدلة وراثيًا، والبذور العضوية، مع التطورات التكنولوجية. يتزايد تفضيل المزارعين لهذه الأصناف المعدلة وراثيًا ببطء في مناطق زراعة الأعلاف المختلفة لتقليل خسائر المحاصيل بسبب الأعشاب الضارة والأمراض وتحسين جودة البذور. يتم تطوير البذور الهجينة من خلال التلقيح المتبادل الخاص والمتحكم فيه بعناية لنباتين مختلفين من نفس النوع لإنتاج سمات جديدة لا يمكن إنشاؤها عن طريق التزاوج الداخلي لنباتين من نفس النوع. عادة، يتم التلقيح المتبادل للبذور الهجينة يدويًا.

يتم إنتاج البذور المعدلة وراثيًا عن طريق الهندسة الوراثية، وتغيير المادة الوراثية للكائن الحي. تتم زراعة البذور المعدلة وراثيًا في المختبر باستخدام تقنيات التكنولوجيا الحيوية الحديثة. من ناحية أخرى، تتم زراعة البذور غير المعدلة وراثيًا عن طريق التلقيح. تعتبر البذور العضوية بذورًا غير معدلة وراثيًا. يتم إنتاج البذور العضوية بشكل طبيعي دون مساعدة المبيدات الحشرية أو الأسمدة أو أي مادة كيميائية أخرى. تتمتع هذه البذور بقدرة أكبر على مقاومة الأمراض وتنمو في ظروف معاكسة.

وتسمح تقنيات التربية هذه بتطوير أصناف جديدة من البذور ذات السمات المرغوبة من خلال تعديل الحمض النووي للبذور وخلايا النباتات. وتساعد هذه التحسينات التكنولوجية في معالجة التحديات التي يواجهها المزارعون أثناء زراعة بذور العلف. وبالتالي، من المتوقع أن تخلق التحسينات التكنولوجية المستمرة فرصًا مربحة في سوق بذور العلف في السنوات القادمة.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق بذور الأعلاف:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

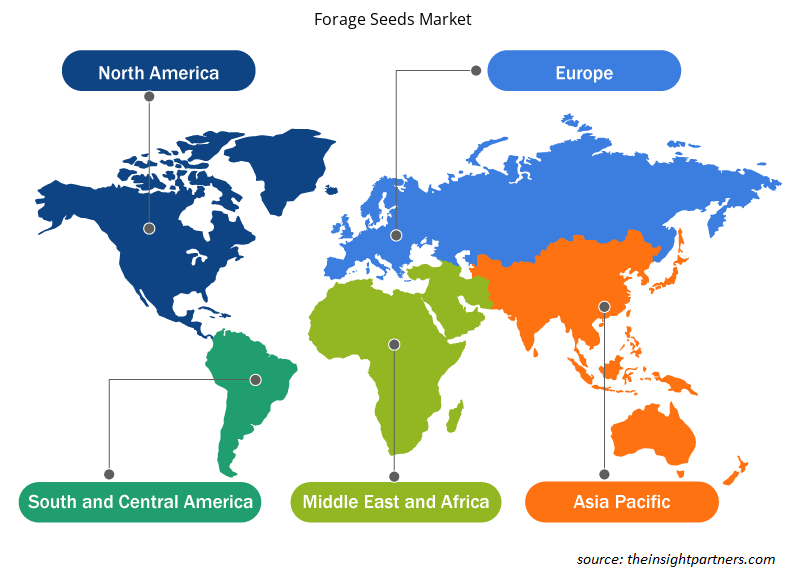

"سوق بذور الأعلاف العالمية" مقسمة على أساس النوع والفئة والثروة الحيوانية والجغرافيا. بناءً على النوع، يتم تقسيم سوق بذور الأعلاف إلى [البرسيم، والبرسيم (الأبيض، والأحمر، والهجين، وغيرها)، وعشبة الجاودار (عشبة الجاودار السنوية، وعشبة الجاودار الدائمة، وعشبة الجاودار الإيطالية، وعشبة الجاودار الهجينة)، والتيموثي، والذرة الرفيعة، والبروم، والبرسيم البري، واللوبيا، والفيسكو المرج، وغيرها]. بناءً على الفئة، يتم تقسيم السوق إلى عضوي وتقليدي. بناءً على الثروة الحيوانية، يتم تقسيم سوق بذور الأعلاف إلى المجترات والدواجن والخنازير وغيرها. يتم تقسيم سوق بذور العلف، على أساس الجغرافيا، إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك)، وأوروبا (ألمانيا وفرنسا وإيطاليا والمملكة المتحدة وروسيا وبقية أوروبا)، وآسيا والمحيط الهادئ (أستراليا والصين واليابان والهند وكوريا الجنوبية وبقية آسيا والمحيط الهادئ)، والشرق الأوسط وأفريقيا (جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وبقية الشرق الأوسط وأفريقيا)، وأمريكا الجنوبية والوسطى (البرازيل وتشيلي وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

بناءً على الثروة الحيوانية، يتم تقسيم سوق بذور الأعلاف إلى المجترات والدواجن والخنازير وغيرها. احتل قطاع المجترات أكبر حصة في سوق بذور الأعلاف في عام 2022 ومن المتوقع أن يسجل معدل نمو كبير خلال فترة التنبؤ. تشمل المجترات الأبقار والأغنام والماعز والجاموس. العلف هو المصدر الأساسي للبروتين والألياف والطاقة للمجترات. توفر الأعلاف البقولية مثل البرسيم والبرسيم 75٪ من البروتين الخام للمجترات. توفر أعشاب العلف كميات كبيرة من الألياف للمجترات. كما يقلل العلف أيضًا من التكلفة الإجمالية لتغذية الكرش. لذلك، يستخدم مربي الماشية عادةً العلف جنبًا إلى جنب مع الأعلاف الحيوانية . إن الوعي المتزايد بالتغذية المحددة للمجترات، وخاصة الأبقار الحلوب والماعز والأغنام والماشية، يدفع الطلب على العلف، وبالتالي دفع نمو سوق بذور العلف.

التحليل الإقليمي:

بناءً على الجغرافيا، يتم تقسيم سوق بذور العلف إلى خمس مناطق رئيسية - أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا. هيمنت أمريكا الشمالية على سوق بذور العلف العالمية وقُدِّرت بنحو 5000 مليون دولار أمريكي في عام 2022. تعد أمريكا الشمالية واحدة من الأسواق المهمة لبذور العلف بسبب الطلب المتزايد على العلف كعلف واستهلاك اللحوم وظروف الطقس، فضلاً عن ارتفاع استهلاك منتجات الثروة الحيوانية على الرغم من ارتفاع الأسعار والأعلاف الحيوانية الراسخة والصناعة الزراعية. يساهم عدد متزايد من الأفراد الذين يختارون المنتجات الغنية بالبروتين والأكثر صحة، والدخل المتاح المتزايد، وتغييرات نمط الحياة، وأنماط الأكل في زيادة الطلب على اللحوم الغنية بالبروتين في الولايات المتحدة وكندا والمكسيك. وبالتالي، مع ارتفاع استهلاك منتجات اللحوم، يزداد الطلب على الأعلاف الحيوانية ويدفع سوق بذور العلف إلى الأمام. تمثل المنطقة واحدة من أكبر منتجي الأعلاف الحيوانية في جميع أنحاء المنطقة. وفقًا لتقرير Alltech Global، أنتجت المنطقة في عام 2020 أكثر من 254 مليون طن متري من منتجات الأعلاف الحيوانية. أدى الإنتاج الضخم للأعلاف الحيوانية في أمريكا الشمالية والمخاوف المتزايدة بشأن سلامة الأغذية، وخاصة فيما يتعلق باللحوم ومنتجات الألبان، إلى زيادة استهلاك الأعلاف الحيوانية المغذية مثل الأعلاف في المنطقة.

ومن المتوقع أيضًا أن يؤدي الارتفاع الكبير في تربية الماشية في أمريكا الشمالية إلى دفع الطلب على الأعلاف الحيوانية، مثل الأعلاف، خلال الفترة المتوقعة. على سبيل المثال، وفقًا لجمعية Foothills Forage & Grazing Association، بلغت مخزونات الماشية الكندية 12.29 مليون رأس في 1 يوليو 2021، بزيادة 0.2٪ عن 1 يوليو 2020. ويعزى هذا الارتفاع إلى الطلب المتزايد على منتجات اللحوم الطازجة، مما أدى إلى زيادة استيراد الماشية. وعلاوة على ذلك، وفقًا لتقرير وزارة الزراعة الأمريكية (UDSA)، في عام 2021، سجلت أمريكا الشمالية أكثر من 114 مليون رأس من الماشية وأكثر من 109 مليون رأس من الخنازير في المنطقة. وبالتالي، فإن زيادة مخزون الماشية والطلب المتزايد على الأعلاف الحيوانية الصحية يدفعان الطلب على بذور العلف في جميع أنحاء المنطقة.

تطورات الصناعة والفرص المستقبلية:

فيما يلي قائمة بالمبادرات المختلفة التي اتخذها اللاعبون الرئيسيون العاملون في سوق بذور العلف:

- في نوفمبر 2022، أعلنت شركة UPL Ltd.، وهي شركة عالمية تقدم حلولاً زراعية مستدامة، أن شركتها Advanta Seeds UK وشركة Bunge قد وقعتا اتفاقية لشراء حصة 20% لكل منهما في SEEDCORP|HO. هذا الاستثمار المقصود هو جزء من هدف مجموعة UPL OpenAg لدفع التعاون لتقديم حزمة كاملة من الحلول للمزارعين.

- في أكتوبر 2022، أعلنت شركة KKR، وهي شركة استثمار عالمية، وشركة UPL Limited، وهي شركة عالمية تقدم حلول الزراعة، عن توقيع اتفاقيات نهائية بموجبها ستستثمر KKR 300 مليون دولار أمريكي مقابل حصة 13.33٪ في Advanta Enterprises Limited، وهي شركة تابعة لشركة UPL Limited.

تأثير كوفيد-19:

أثرت جائحة كوفيد-19 على الاقتصادات والصناعات في مختلف البلدان. أثر حظر السفر والإغلاق وإغلاق الأعمال في الدول الرائدة في أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا سلبًا على نمو مختلف الصناعات، بما في ذلك صناعة الزراعة والأعلاف الحيوانية. أدى إغلاق وحدات التصنيع إلى اضطراب سلاسل التوريد العالمية وجداول التسليم وأنشطة التصنيع ومبيعات مختلف المنتجات الأساسية وغير الأساسية. أعلنت شركات مختلفة عن تأخيرات محتملة في تسليم المنتجات وانخفاض في مبيعات منتجاتها المستقبلية في عام 2020. بالإضافة إلى ذلك، أجبر الحظر الذي فرضته حكومات مختلفة في أوروبا وآسيا وأمريكا الشمالية على السفر الدولي الشركات على تعليق خطط التعاون والشراكة مؤقتًا. كل هذه العوامل أعاقت صناعة الأعلاف الحيوانية في عام 2020 وأوائل عام 2021، وبالتالي كبح جماح نمو سوق بذور العلف.

رؤى إقليمية حول سوق بذور الأعلاف

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق بذور الأعلاف طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق بذور الأعلاف والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق بذور الأعلاف

نطاق تقرير سوق بذور العلف

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 12.76 مليار دولار أمريكي |

| حجم السوق بحلول عام 2030 | 19.76 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 5.6% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2030 |

| القطاعات المغطاة | حسب النوع

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق بذور الأعلاف نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق بذور الأعلاف هي:

- شركة يو بي إل المحدودة

- بذور DLF AS

- شركة كورتيفا

- شركة ليماجرين المملكة المتحدة المحدودة

- شركة S&W للبذور

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق بذور الأعلاف

المنافسة والشركات الرئيسية:

تعد UPL Ltd وDLF Seeds AS وCorteva Inc وLimagrain UK Ltd وS&W Seed Co وDeutsche Saatveredelung AG وCerience وAllied Seed LLC وMAS Seeds SA وSyngenta AG من بين أبرز اللاعبين العاملين في سوق بذور العلف العالمية. تقدم شركات تصنيع بذور العلف هذه حلول بذور متطورة بميزات مبتكرة لتقديم تجربة متفوقة للمزارعين ومواشيهم.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- Artificial Turf Market

- Fish Protein Hydrolysate Market

- Smart Locks Market

- Digital Pathology Market

- Energy Recovery Ventilator Market

- Europe Industrial Chillers Market

- Aerosol Paints Market

- Nitrogenous Fertilizer Market

- Biopharmaceutical Tubing Market

- Artificial Intelligence in Healthcare Diagnosis Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The forage seeds manufacturers across the globe are investing significantly in strategic development initiatives such as product innovation, mergers and acquisitions, and expansion of their businesses to attract many consumers and enhance their market position. To maintain their strategic position in the market, key players are investing significantly in quality enhancement of forage seeds. For instance, DLF Seeds, the world's leading grass seed breeder, invested US$ 4.6 million in new state-of-the-art mixing and distribution facilities in 2021. The company has invested in transforming its current production facilities of Offshore Patrol Vessels (OPVs) and the hybrid seed of forage and bringing much-needed additional capacity and efficiency to cope with the increasing market demands by consumers and environmental stewardship in the forage seed market. Such strategic development initiatives by key players help to create a strong foothold in the market.

Based on the livestock, ruminants segment is projected to grow at the fastest CAGR over the forecast period. Ruminants include cattle, sheep, goats, and buffalo. Forage is the primary source of protein, fiber, and energy for ruminants. Leguminous forages such as alfalfa and clover provide 75% of the crude protein to ruminants. Forage grasses provide high amounts of fiber to the ruminants.

North America accounted for the largest share of the global forage seeds market. The growth in region is attributed to the increased demand for forage as feed, meat consumption, and weather conditions, as well as rising consumption of livestock products despite the rising prices, well-established animal feed, and agriculture industry. An increasing number of individuals opting for protein-rich and healthier products, growing disposable income, lifestyle changes, and eating patterns contribute to a surge in demand for protein-rich meat in the US, Canada, and Mexico. Thus, with the rising consumption of meat products, the demand for animal feed increases and further drives the market for forage seeds. The region accounts for one of the largest animal feed producers across the region. As per the report of Alltech Global, in 2020, the region produced more than 254 million metric tons of animal feed products. The mass production of animal feed in North America and the rising food safety concerns, especially about meat and dairy products, have led to the increased consumption of nutritional animal feed such as forages in the region.

Based on category, conventional segment mainly has the largest revenue share. Conventional forage seeds are grown using chemical fertilizers, genetically modified organisms (GMOs), and chemical pesticides. Conventional forage seeds provide higher yields than organic ones due to the use of GMOs and chemical fertilizers. Moreover, conventional forage seeds are highly affordable and readily available.

The major players operating in the global forage seeds market are UPL Ltd, DLF Seeds AS, Corteva Inc, Limagrain UK Ltd, S&W Seed Co, Deutsche Saatveredelung AG, Cerience, Allied Seed LLC, MAS Seeds SA, and Syngenta AG.

The seed manufacturers have developed different varieties or traits of seeds, such as hybrid, GMO, non-GMO, and organic seeds, with technological developments. The farmer's preference for these transgenic varieties is slowly rising in various forage-growing regions to minimize crop losses by weeds and diseases and enhance the quality of seeds. The hybrid seeds are developed by the special, carefully controlled cross-pollination of two different parent plants of the same species to produce new traits that cannot be created by the inbreeding of two of the same plants. Usually, the hybrid seeds are cross-pollinated by hand.

The List of Companies - Forage Seeds Market

- UPL Ltd

- DLF Seeds AS

- Corteva Inc

- Limagrain UK Ltd

- S&W Seed Co

- Deutsche Saatveredelung AG

- Cerience

- Allied Seed LLC

- MAS Seeds SA

- Syngenta AG

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير