تقرير سوق الإلكترونيات المقواة بالإشعاع 2031 حسب القطاعات والجغرافيا والديناميكيات والتطورات الأخيرة والرؤى الإستراتيجية

البيانات التاريخية : 2021-2022 | سنة الأساس : 2023 | فترة التنبؤ : 2024-2031حجم سوق الإلكترونيات المُقوّاة بالإشعاع وتوقعاته (2021-2031)، والحصة العالمية والإقليمية، والاتجاهات، وتحليل فرص النمو. يغطي التقرير: حسب المكونات (مكونات إدارة الطاقة، وأجهزة الإشارات المختلطة التناظرية والرقمية، والذاكرة، ووحدات التحكم والمعالجات)، وتقنية التصنيع [التصلب الإشعاعي بالتصميم (RHBD) والتصلب الإشعاعي بالمعالجة (RHBP)]، والتطبيق (الفضاء والدفاع، ومحطات الطاقة النووية، والفضاء، وغيرها)، والجغرافيا.

- تاريخ التقرير : Mar 2026

- رمز التقرير : TIPRE00011821

- الفئة : الإلكترونيات وأشباه الموصلات

- الحالة : البيانات الصادرة

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 150

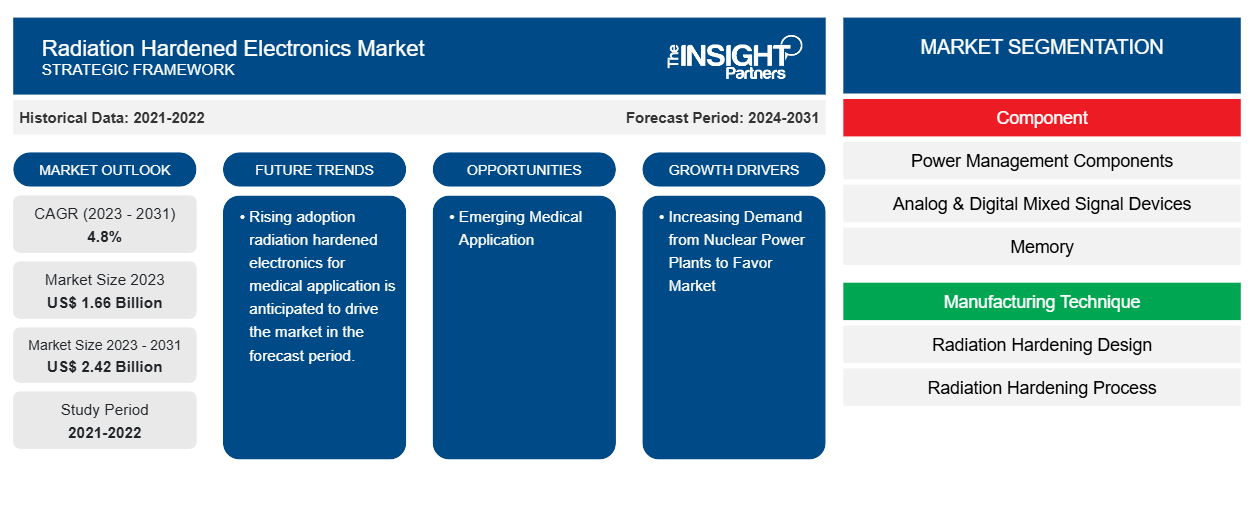

من المتوقع أن يصل حجم سوق الإلكترونيات المقاومة للإشعاع إلى 2.42 مليار دولار أمريكي بحلول عام 2031 من 1.66 مليار دولار أمريكي في عام 2023. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 4.8٪ خلال الفترة 2023-2031. ومن المرجح أن يظل التبني المتزايد للإلكترونيات المقاومة للإشعاع وزيادة الاستثمار في برامج الفضاء من الاتجاهات والدوافع الرئيسية في السوق.

تحليل سوق الإلكترونيات المقاومة للإشعاع

من المتوقع أن يؤدي الطلب المتزايد على أجهزة استشعار ردود الفعل المعززة بالإشعاع بين مصنعي المعدات والأنظمة الحيوية في جميع أنحاء العالم إلى تعزيز سوق أجهزة استشعار ردود الفعل المعززة بالإشعاع خلال فترة التنبؤ. يتم دمج أجهزة استشعار ردود الفعل المعززة بالإشعاع على نطاق واسع في أنظمة الطيران والدفاع والمركبات الفضائية والأقمار الصناعية والمسبارات الفضائية والمعدات الطبية وغيرها. تعمل التطورات التكنولوجية وتصغير أجهزة استشعار ردود الفعل المعززة بالإشعاع والطلب المتزايد على الطاقة المتجددة وزيادة أنشطة البحث والتطوير على دفع سوق أجهزة استشعار ردود الفعل المعززة بالإشعاع.

نظرة عامة على سوق الإلكترونيات المقاومة للإشعاع

أجهزة استشعار ردود الفعل المعززة للإشعاع هي أجهزة مصممة لتحمل مستويات عالية من الإشعاع، والتي توجد عادة في البيئات النووية والفضائية. تستخدم هذه المستشعرات آلية ردود الفعل لمراقبة أدائها بشكل مستمر وتعديلها وفقًا لذلك من خلال ضمان عمليات موثوقة ودقيقة في الإشعاعات الصلبة. تستخدم المستشعرات حلقات ردود الفعل للكشف عن أي انحرافات عن سلوكها المتوقع بسبب الضرر الناجم عن الإشعاع.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الإلكترونيات المقاومة للإشعاع: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق الإلكترونيات المقاومة للإشعاع

تزايد الطلب على محطات الطاقة النووية لصالح السوق

تشارك محطات الطاقة النووية في توليد الكهرباء من خلال عملية الانشطار النووي. في هذه العملية، يتم إنتاج كمية كبيرة من الطاقة، مما يولد كمية كبيرة من الإشعاع. هذا الإشعاع ضار بالبشر ويمكن أن يتلف المعدات الإلكترونية، مما يزيد من الطلب على أجهزة استشعار ردود الفعل المعززة للإشعاع. يتم وضع أجهزة استشعار ردود الفعل المعززة للإشعاع بشكل استراتيجي في جميع أنحاء المحطة لمراقبة التغيرات في درجات الحرارة في المناطق الحرجة، مثل أنظمة التبريد، ونواة المفاعل، والمكونات المختلفة. توفر هذه المستشعرات ردود فعل مستمرة لأنظمة التحكم، مما يمكن مشغلي المحطة من اتخاذ الإجراءات اللازمة للحفاظ على نطاق درجة الحرارة المطلوب واتخاذ قرارات مستنيرة لتحسين أداء النظام. تقوم العديد من الشركات باستثمارات كبيرة في تطوير محطات الطاقة. على سبيل المثال، وفقًا لبيانات وزارة الطاقة الأمريكية المنشورة في يناير 2024، استثمرت وزارة الطاقة حوالي 12 مليار دولار أمريكي في Plant Vogtle لتوفير أكثر من 1100 ميغاواط من الطاقة النظيفة للشبكة بمجرد التشغيل.

التطبيقات الطبية الناشئة.

تلعب أجهزة استشعار ردود الفعل المقواة بالإشعاع دورًا حاسمًا في ضمان سلامة ودقة وموثوقية المعدات الطبية المستخدمة في صناعة الرعاية الصحية. يتم دمج هذه المستشعرات في مجموعة متنوعة من المعدات الطبية، بما في ذلك أشعة جاما والأشعة السينية وحزم الإلكترونات، من خلال جعلها تتحمل مستويات عالية من الإشعاع. يتم دمج أجهزة استشعار ردود الفعل المقواة بالإشعاع في المقام الأول في معدات العلاج الإشعاعي لدعم الأطباء في علاج مرضى السرطان. العلاج الإشعاعي ، المعروف أيضًا باسم العلاج الإشعاعي، هو أكثر طرق العلاج شيوعًا لمرضى السرطان، حيث تُستخدم حزم الإشعاع عالية الطاقة لاستهداف الخلايا السرطانية وتدميرها، والتي تتطلب أجهزة استشعار ردود الفعل المقواة بالإشعاع لمراقبة معلمات مختلفة، بما في ذلك توصيل الجرعة وكثافة الشعاع وموضع الشعاع. يستخدم المتخصصون في الرعاية الصحية أجهزة استشعار ردود الفعل المقواة بالإشعاع لضمان توصيل علاج دقيق ومحدد من خلال تقليل الضرر الذي يلحق بالأنسجة السليمة. على سبيل المثال، في أبريل 2022، قدمت مجموعة ماكسون أجهزة ترميز ENX GAMA المصممة للاستخدام في محيط المسرعات الخطية الطبية على معدات مثل أجهزة التجميع متعددة الأوراق. تعتبر أجهزة ترميز ENX GAMA أجهزة ترميز مقاومة للإشعاع مدمجة بمحركات التيار المستمر وهي مناسبة للغاية لأجهزة العلاج الإشعاعي.

تقرير تحليل تجزئة سوق الإلكترونيات المقواة بالإشعاع

إن القطاعات الرئيسية التي ساهمت في اشتقاق تحليل سوق الإلكترونيات المقواة بالإشعاع هي المكونات وتقنيات التصنيع والتطبيقات.

- بناءً على المكونات، يتم تقسيم سوق الإلكترونيات المقاومة للإشعاع إلى مكونات إدارة الطاقة، وأجهزة الإشارات المختلطة التناظرية والرقمية، والذاكرة، ووحدات التحكم والمعالجات. ومن المتوقع أن يستحوذ قطاع مكونات إدارة الطاقة على حصة سوقية كبيرة خلال فترة التوقعات.

- بناءً على تقنية التصنيع، يتم تقسيم سوق الإلكترونيات المقواة بالإشعاع إلى التصلب الإشعاعي حسب التصميم (RHBD) والتصلب الإشعاعي حسب العملية (RHBP). ومن المتوقع أن يحظى قطاع التصلب الإشعاعي حسب التصميم (RHBD) بحصة سوقية كبيرة في فترة التوقعات.

- من حيث التطبيقات، يتم تقسيم السوق إلى الفضاء والدفاع، ومحطة الطاقة النووية، والفضاء، وغيرها. ومن المتوقع أن يستحوذ الفضاء والدفاع على حصة سوقية كبيرة في الفترة المتوقعة.

تحليل حصة سوق الإلكترونيات المقاومة للإشعاع حسب المنطقة الجغرافية

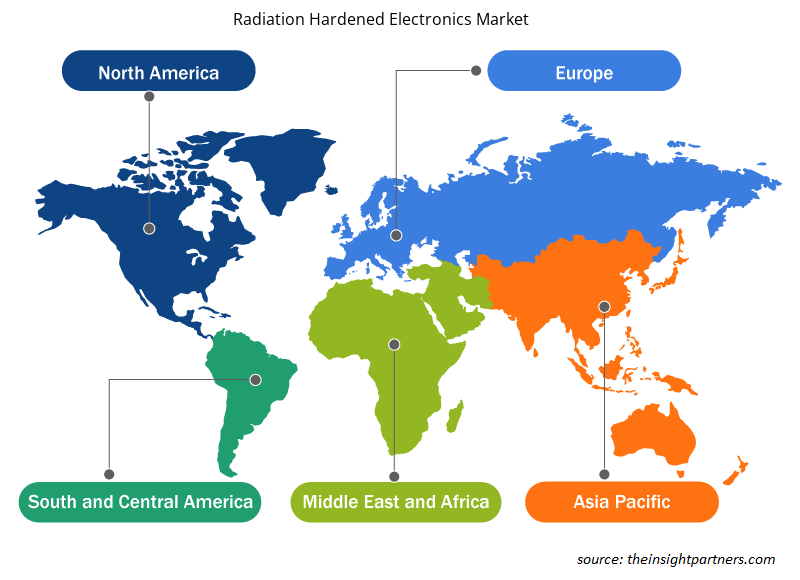

ينقسم النطاق الجغرافي لتقرير سوق الإلكترونيات المقواة بالإشعاع بشكل أساسي إلى خمس مناطق: أمريكا الشمالية، ومنطقة آسيا والمحيط الهادئ، وأوروبا، والشرق الأوسط وأفريقيا، وأمريكا الجنوبية والوسطى.

سيطرت أمريكا الشمالية على سوق الإلكترونيات المقواة بالإشعاع. تعمل صناعة الفضاء المتوسعة على تعزيز سوق أجهزة استشعار ردود الفعل المقواة بالإشعاع في أمريكا الشمالية. كانت الولايات المتحدة في طليعة رحلات الفضاء لأكثر من 60 عامًا. ولديها أكبر برنامج فضائي حكومي في العالم. شكلت الأقمار الصناعية المسجلة في الولايات المتحدة أكثر من نصف جميع الأقمار الصناعية العاملة في عام 2022. تعد الولايات المتحدة حاليًا الدولة الوحيدة التي لديها حساب موضوعي للأنشطة الفضائية. علاوة على ذلك، فإن التركيز القوي على البحث والتطوير في الاقتصادات المتقدمة في الولايات المتحدة وكندا يجبر اللاعبين في أمريكا الشمالية على جلب حلول متقدمة تقنيًا إلى السوق. بالإضافة إلى ذلك، تمتلك الولايات المتحدة عددًا كبيرًا من اللاعبين في سوق الإلكترونيات المقواة بالإشعاع والذين يركزون بشكل متزايد على تطوير حلول مبتكرة. تساهم كل هذه العوامل في نمو سوق الإلكترونيات المقواة بالإشعاع في المنطقة.

رؤى إقليمية حول سوق الإلكترونيات المقاومة للإشعاع

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الإلكترونيات المقواة بالإشعاع طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الإلكترونيات المقواة بالإشعاع والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الإلكترونيات المقاومة للإشعاع

نطاق تقرير سوق الإلكترونيات المقواة بالإشعاع

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2023 | 1.66 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 2.42 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2023 - 2031) | 4.8% |

| البيانات التاريخية | 2021-2022 |

| فترة التنبؤ | 2024-2031 |

| القطاعات المغطاة |

حسب المكون

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

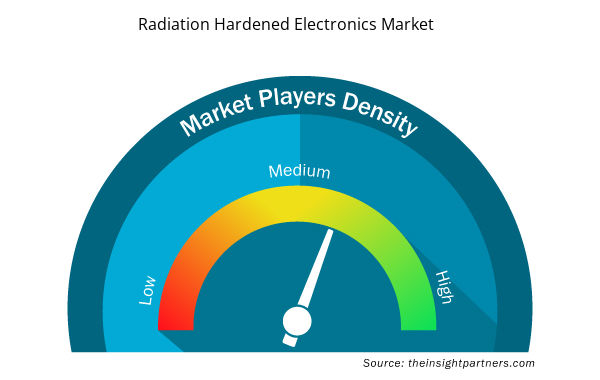

كثافة اللاعبين في سوق الإلكترونيات المقاومة للإشعاع: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الإلكترونيات المقاومة للإشعاع نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الإلكترونيات المقاومة للإشعاع هي:

- بي ايه اي سيستمز

- شركة داتا ديفايس

- شركة هونيويل الدولية

- شركة إنفينيون للتكنولوجيا

- شركة رينيساس للإلكترونيات

- شركة تكساس إنسترومنتس

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الإلكترونيات المقاومة للإشعاع

أخبار سوق الإلكترونيات المقاومة للإشعاع والتطورات الأخيرة

يتم تقييم سوق الإلكترونيات المقواة بالإشعاع من خلال جمع البيانات النوعية والكمية بعد البحث الأولي والثانوي، والتي تتضمن منشورات الشركات المهمة وبيانات الجمعيات وقواعد البيانات. فيما يلي بعض التطورات في سوق الإلكترونيات المقواة بالإشعاع:

- قدمت شركة EPC Space رقاقة EPC7009L16SH، وهي رقاقة IC لمحرك بوابة من نتريد الجاليوم المقوى بالإشعاع. باستخدام تقنية eGaN IC الحصرية من EPC، تعمل رقاقة GaN المبتكرة هذه على تمكين مهندسي التصميم من الاستفادة الكاملة من قدرات تقنية eGaN FET. (المصدر: EPC Space، موقع الشركة على الويب، أبريل 2024)

- أطلقت شركة Renesas Electronics Corporation، وهي شركة توريد حلول أشباه الموصلات المتقدمة، خطًا جديدًا من الأجهزة المعبأة في بلاستيك والمُعززة بالإشعاع (rad-hard) لأنظمة إدارة طاقة الأقمار الصناعية. تتضمن الأجهزة الأربعة الجديدة منظم الحمل (POL) ISL71001SLHM/SEHM، وعوازل رقمية ISL71610SLHM وISL71710SLHM، و100V GaN FET ISL73033SLHM ومشغل مدمج منخفض الجانب. (المصدر: شركة Renesas Electronics Corporation، موقع الشركة، يوليو 2021)

تقرير سوق الإلكترونيات المقاومة للإشعاعات والتغطية والنتائج المتوقعة

يوفر تقرير "حجم سوق الإلكترونيات المقواة بالإشعاع والتوقعات (2021-2031)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم سوق الإلكترونيات المقواة بالإشعاع وتوقعاته على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية المشمولة بالنطاق.

- اتجاهات سوق الإلكترونيات المقاومة للإشعاع بالإضافة إلى ديناميكيات السوق مثل المحركات والقيود والفرص الرئيسية.

- تحليل مفصل لقوى PEST/Porter الخمس و SWOT.

- تحليل سوق الإلكترونيات المقاومة للإشعاع يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي واللاعبين الرئيسيين واللوائح والتطورات الأخيرة في السوق.

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة في سوق الإلكترونيات المقاومة للإشعاع.

- ملفات تعريفية مفصلة للشركة.

نافين خبيرٌ متمرسٌ في أبحاث السوق والاستشارات، يتمتع بخبرةٍ تزيد عن 9 سنوات في مشاريع مُخصصة ومُشتركة واستشارية. يشغل حاليًا منصب نائب الرئيس المساعد، وقد نجح في إدارة أصحاب المصلحة عبر سلسلة قيمة المشاريع، وألّف أكثر من 100 تقرير بحثي وأكثر من 30 مهمة استشارية. يمتد نطاق عمله ليشمل مشاريع صناعية وحكومية، مساهمًا بشكل كبير في نجاح العملاء واتخاذ القرارات القائمة على البيانات.

نافين حاصلٌ على شهادة في هندسة الإلكترونيات والاتصالات من جامعة فرجينيا التقنية، كارناتاكا، وشهادة ماجستير في إدارة الأعمال في التسويق والعمليات من جامعة مانيبال. وهو عضوٌ نشطٌ في معهد مهندسي الكهرباء والإلكترونيات (IEEE) لمدة 9 سنوات، حيث شارك في مؤتمراتٍ وندواتٍ تقنية، وتطوّع على مستوى الأقسام والمناطق. قبل منصبه الحالي، عمل مستشارًا استراتيجيًا مساعدًا في IndustryARC، ومستشارًا للخوادم الصناعية في شركة هيوليت باكارد (HP Global).

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق الإلكترونيات المقاومة للإشعاع

احصل على عينة مجانية ل - سوق الإلكترونيات المقاومة للإشعاع