Marktübersicht für Satellitenkonnektivität im Gesundheitswesen, Wachstum, Trends, Analyse, Forschungsbericht (2021–2028)

Marktprognose für Satellitenkonnektivität im Gesundheitswesen bis 2028 – Auswirkungen von COVID-19 und globale Analyse nach Komponenten (System und Software, medizinische Geräte und Dienste), Anwendungen (E-Health und andere), Konnektivität (mobile Satellitendienste und feste Satellitendienste) und Endbenutzern (klinische Forschungsorganisationen, Krankenhäuser und Kliniken, Forschungs- und Diagnoselabore und andere) und Geografie

- Status : Veröffentlicht

- Berichtscode : TIPHC00002288

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 274

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 13, 2024

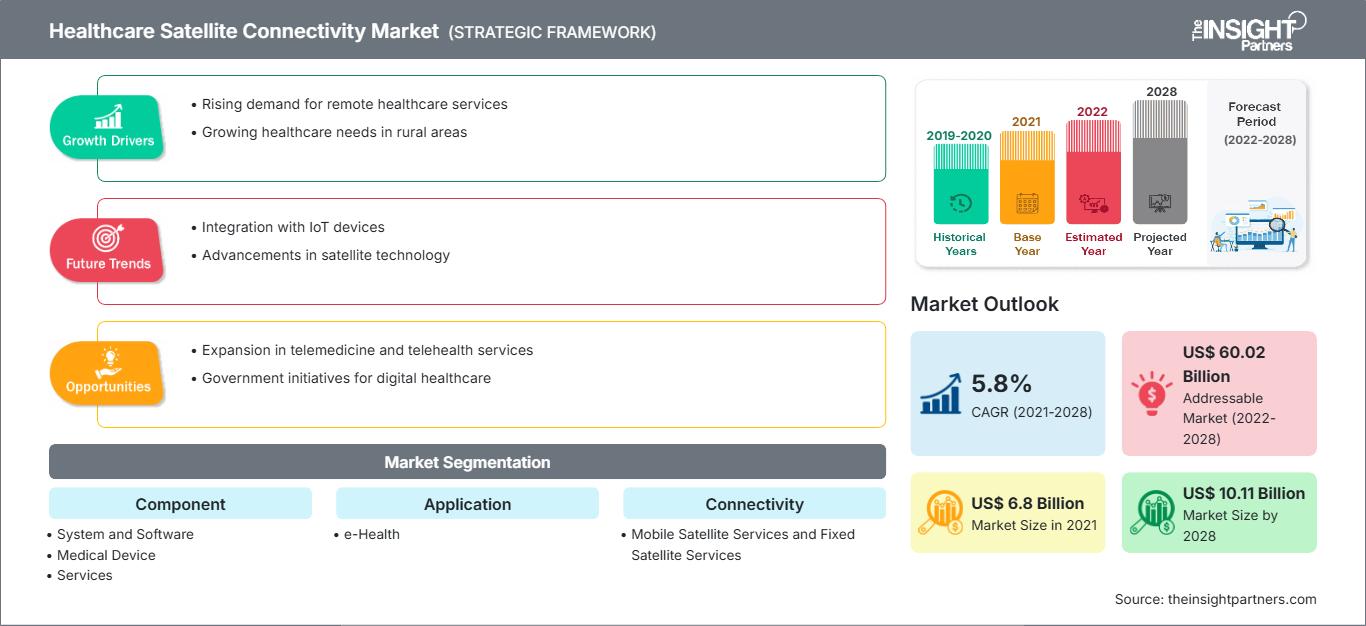

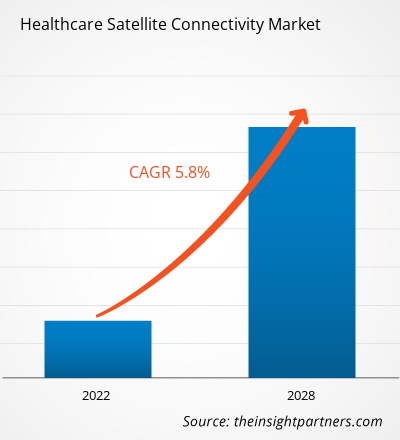

Der Markt für Satellitenkommunikation im Gesundheitswesen soll von 6.797,22 Millionen US-Dollar im Jahr 2021 auf 10.105,21 Millionen US-Dollar im Jahr 2028 wachsen; die durchschnittliche jährliche Wachstumsrate (CAGR) von 5,8 % wird von 2021 bis 2028 geschätzt.

Satellitenkommunikation im Gesundheitswesen ermöglicht medizinische Ferndiagnosen und -versorgung bequem von zu Hause aus. Sie ermöglicht digitale Bildgebung, Patientenüberwachung aus der Ferne, E-Learning und -Beratung sowie den Zugang zu Live-Sitzungen, um das Wissen von medizinischem Fachpersonal an entfernten Standorten zu erweitern.

Das Wachstum des Marktes für Satellitenkommunikation im Gesundheitswesen ist auf Faktoren wie staatliche Initiativen zur Förderung und Entwicklung satellitenbasierter Lösungen im Gesundheitswesen und die zunehmende Nutzung von E-Health zurückzuführen. Bedenken hinsichtlich des Datenschutzes hemmen jedoch das Marktwachstum.

Markteinblicke: Wachsende Gesundheits-IT-Branche in Schwellenländern

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Satellitenkonnektivität im Gesundheitswesen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Gesundheitssysteme erleben weltweit ein wachsendes Engagement der Verbraucher. In Entwicklungsländern werden die Systeme technologiefreundlicher. Diese erleben eine Internationalisierung der Versorgung, da etablierte Marken – wie die US-amerikanische Cleveland Clinic – ihre Geschäfte in den VAE ausweiteten und Start-ups – wie das englische Babylon, eine auf maschinellem Lernen und KI basierende Diagnose-App für die Primärversorgung – in die Märkte Chinas und Ruandas eintraten. Darüber hinaus bieten IT-Start-ups mit zunehmenden Investitionen in den Gesundheitssektor im asiatisch-pazifischen Raum lukrative Möglichkeiten für dessen Wachstum. So sammelte beispielsweise DXY (ein chinesisches Gesundheitsportalunternehmen) im Dezember 2020 in einer von Trustbridge Partners angeführten Finanzierungsrunde der Serie E 500 Millionen US-Dollar ein. Alodokter, eine indonesische Gesundheitstechnologieplattform, erhielt 33 Millionen US-Dollar in der Serie C. Die wachsende Gesundheits-IT-Branche im asiatisch-pazifischen Raum dürfte den Akteuren lukrative Möglichkeiten bieten, ihre Kapazitäten in der gesamten Region auszubauen. Zudem hat die COVID-19-Pandemie den Einsatz digitaler Gesundheitstechnologien weltweit beschleunigt. Die Pandemie hat Fernüberwachungslösungen priorisiert. Die Regierungen in der Region fördern den Einsatz von Telemedizin. So veröffentlichte die indische Regierung im März 2020 die Telemedizin-Praxisrichtlinien, um es niedergelassenen Ärzten zu ermöglichen, Gesundheitsdienstleistungen mithilfe von Telekommunikation und digitalen Technologien anzubieten. Solche Initiativen würden in den kommenden Jahren lukrative Möglichkeiten für das Wachstum des Patientenportalmarktes bieten.

Komponentenbasierte Erkenntnisse

Der Markt für Satellitenkonnektivität im Gesundheitswesen ist nach Komponenten segmentiert in medizinische Geräte, Systeme und Software sowie Dienstleistungen. Im Jahr 2021 hatte das Segment Systeme und Software den größten Marktanteil. Es wird erwartet, dass dasselbe Segment zwischen 2021 und 2028 die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnet.

Anwendungsbasierte Erkenntnisse

Nach Anwendungen ist der Markt für Satellitenkonnektivität im Gesundheitswesen in E-Health und Sonstiges unterteilt. Im Jahr 2021 hatte das Segment E-Health den größeren Marktanteil. Für das sonstige Segment wird jedoch in den kommenden Jahren eine höhere CAGR erwartet.

Konnektivitätsbasierte Erkenntnisse

Basierend auf der Konnektivität ist der Markt für Satellitenkonnektivität im Gesundheitswesen in mobile Satellitendienste und feste Satellitendienste unterteilt. Im Jahr 2021 hatte das Segment der festen Satellitendienste einen größeren Marktanteil. Auf der anderen Seite wird für das Segment der mobilen Satellitendienste im Prognosezeitraum eine höhere CAGR erwartet.

Endnutzerbasierte Erkenntnisse

Basierend auf dem Endnutzer ist der Markt für Satellitenkonnektivität im Gesundheitswesen in klinische Forschungsorganisationen, Krankenhäuser und Kliniken, Forschungs- und Diagnoselabore und Sonstige segmentiert. Im Jahr 2021 hatte das Segment Krankenhäuser und Kliniken den größten Marktanteil. Für das Segment der klinischen Forschungsorganisationen wird jedoch in den kommenden Jahren die höchste CAGR erwartet.

Produkteinführungen und -zulassungen sind gängige Strategien von Unternehmen, um ihre globale Präsenz und ihr Produktportfolio zu erweitern. Darüber hinaus konzentrieren sich die Akteure auf dem Markt für Satellitenkonnektivität im Gesundheitswesen auf die Partnerschaftsstrategie, um ihren Kundenstamm zu erweitern, was ihnen wiederum ermöglicht, ihren Markennamen weltweit zu behaupten.

Satellitenkonnektivität im Gesundheitswesen

Regionale Einblicke in den Markt für Satellitenkonnektivität im GesundheitswesenDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Satellitenkonnektivität im Gesundheitswesen im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts zur Satellitenkonnektivität im Gesundheitswesen

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2021 | US$ 6.8 Billion |

| Marktgröße nach 2028 | US$ 10.11 Billion |

| Globale CAGR (2021 - 2028) | 5.8% |

| Historische Daten | 2019-2020 |

| Prognosezeitraum | 2022-2028 |

| Abgedeckte Segmente |

By Komponente

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Satellitenkonnektivität im Gesundheitswesen: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Satellitenkonnektivität im Gesundheitswesen wächst rasant. Dies wird durch die steigende Nachfrage der Endnutzer aufgrund veränderter Verbraucherpräferenzen, technologischer Fortschritte und eines stärkeren Bewusstseins für die Produktvorteile vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Satellitenkonnektivität im Gesundheitswesen Übersicht der wichtigsten Akteure

- System und Software

- Ferngeräteverwaltung

- Netzwerkbandbreitenverwaltung

- Datenanalyse

- Anwendungssicherheit

- Netzwerksicherheit

- Medizinisches Gerät

- Tragbares externes Gerät

- Implantiertes medizinisches Gerät

- Stationäres medizinisches Gerät

- Dienste

- Systemintegrationsdienste

- Beratung

- Schulung und Ausbildung

- Support- und Wartungsdienste

Markt für Satellitenkonnektivität im Gesundheitswesen – nach Anwendung

- E-Health

- Telemedizin

- Klinischer Betrieb

- Sonstige

Markt für Satellitenkonnektivität im Gesundheitswesen – nach Konnektivität

- Mobile Satellitendienste

- Feste Satellitendienste

Markt für Satellitenkonnektivität im Gesundheitswesen – nach Endbenutzer

- Klinische Forschungseinrichtungen

- Krankenhäuser und Kliniken

- Forschungs- und Diagnoselabore

- Sonstige

Markt für Satellitenkonnektivität im Gesundheitswesen – nach Geografie

- Nordamerika

- USA

- Kanada

- Mexiko

- Europa

- Großbritannien

- Deutschland

- Frankreich

- Italien

- Spanien

- Restliches Europa

- Asien-Pazifikraum

- China

- Japan

- Indien

- Australien

- Südkorea

- Restlicher Asien-Pazifikraum

- Naher Osten und Afrika

- VAE

- Saudi-Arabien

- Südafrika

- Restlicher Naher Osten und Afrika

- Süd- und Mittelamerika

- Brasilien

- Argentinien

- Restlicher Süd- und Amerika

Unternehmensprofile

- Inmarsat Global Limited

- Hughes Network Systems

- SES SA

- X2nSat

- Expedition Communications

- Globalstar

- EUTELSAT COMMUNICATIONS SA

- AT&T Intellectual Property

- DISH Network LLC

- Ligado Networks

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends