Marktstrategien für Hartschaumstoffe, Top-Player, Wachstumschancen, Analyse und Prognose bis 2027

Markt für Hartschaumstoffe bis 2027 – Globale Analyse und Prognosen nach Typ (Polyurethanschaum, Polystyrolschaum, Polypropylenschaum, Polyethylenschaum, Polyvinylchloridschaum und andere), Endverbrauchsindustrie (Bauwesen und Konstruktion, Haushaltsgeräte, Verpackung, Automobilindustrie und andere)

- Status : Veröffentlicht

- Berichtscode : TIPRE00005351

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 144

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 17, 2024

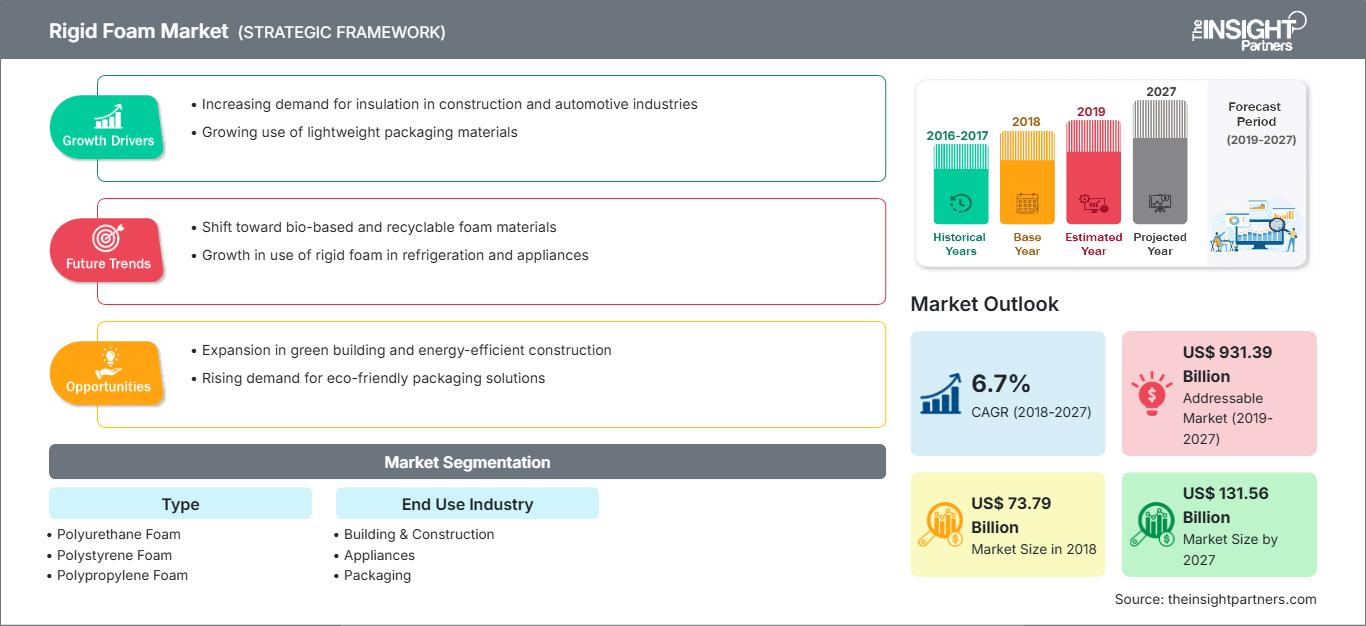

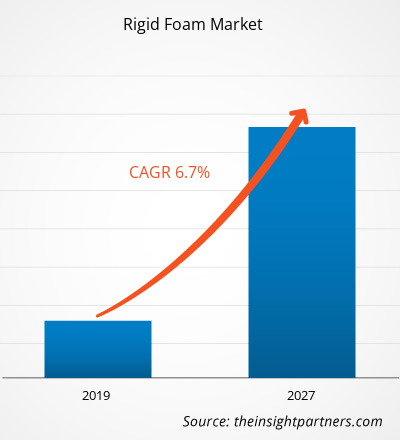

[Forschungsbericht]Der Markt für Hartschaumstoffe belief sich im Jahr 2018 auf 73.786,7 Mio. US-Dollar und soll im Prognosezeitraum 2019–2027 mit einer durchschnittlichen jährlichen Wachstumsrate von 6,7 % wachsen und bis 2027 131.558,9 Mio. US-Dollar erreichen.

Hartschäume besitzen nachweislich verschiedene Eigenschaften wie Wasserdichtigkeit, Antistatik, Vibrationshemmung und Rutschfestigkeit, was sie zu einem idealen Material für den Einsatz in vielen Industriezweigen sowie im Baugewerbe macht. Hartschaumstoffe schützen die Betonoberflächen, auf die sie aufgetragen werden, und verlängern die Lebensdauer der darunter liegenden Betonböden. Sie sind unempfindlich gegenüber Ölen, Wasch- und Reinigungsmitteln, Getriebeflüssigkeiten, Wasser, Hagel, Schnee und ätzenden Chemikalien. Hartschaumstoffe werden auch verwendet, um die Ästhetik von Böden zu verbessern. Sie sind in verschiedenen Farben, Schattierungen und Texturen erhältlich. Metallische Pigmente und Vinylfarbflocken werden den Hartschaumsystemen zugesetzt, um Oberflächen mit schillernden Farben zu erzeugen. Die Ästhetik von buntem Hartschaum dürfte den Markt für Hartschaum ankurbeln und er wird zunehmend in Neubauprojekten und bei der Renovierung alter Häuser eingesetzt.

Im Jahr 2018 hatte die Region Asien-Pazifik den größten Anteil am globalen Hartschaummarkt. Dieses Marktwachstum in der Region ist hauptsächlich auf die Präsenz großer Hartschaumhersteller in der Region zurückzuführen. Auch die steigende Produktion von Hartschaum dürfte das Marktwachstum zwischen 2019 und 2027 ankurbeln. Im asiatisch-pazifischen Raum machte China gemessen am Umsatz den größten Anteil an Hartschaum aus.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Hartschaum: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

In den letzten Jahren wurden rasante Fortschritte im Polymerbereich mit einer steigenden Produktion von Kunststoffen und Polymeren beobachtet. Der Aufwärtstrend in der Polymerindustrie dürfte zu einer hohen Produktion von Polymerabfällen führen. Darüber hinaus wurden im Zuge des Umweltschutzes neue Regeln und Vorschriften erlassen, die Wissenschaftler und Unternehmer dazu bewegen, nach alternativen Lösungen für die Handhabung und Behandlung von Kunststoffabfällen zu suchen oder biologisch abbaubare Kunststoffe einzusetzen, die sich in der Natur zersetzen. Unter den verschiedenen weltweit produzierten biologisch abbaubaren Kunststoffen gilt Polylactid (PLA) als eine der bevorzugten Biokunststoffe. Die Abfälle dieser Kunststoffe lassen sich problemlos zu vollwertigen Produkten wie Polyurethan-Polyisocyanurat-Hartschäumen (RPU/PIR) verarbeiten. Solche Schäume aus biologisch abbaubarem Polylactid gelten als nachhaltige Lösungen. Einer von Europe PMC vorgelegten Studie zufolge kann Polylactid petrochemisches Polyol bei der Formulierung von Polyisocyanurat teilweise ersetzen. Die erhaltenen PIR-Schäume weisen zudem verschiedene Eigenschaften auf, wie beispielsweise eine minimale Rohdichte, Sprödigkeit und Wasseraufnahmefähigkeit. Daher kann die Verwendung von aus Kunststoffabfällen hergestelltem PLA-Polyol eine hervorragende Alternative zu petrochemischen Polyolen sein. Solche Entwicklungen helfen, die knappen Ressourcen zu verwalten und Abfälle effektiv zu nutzen. Zudem gelten die aus solchen Biomaterialien hergestellten Produkte als umweltfreundliche Lösungen.

Typ-Einblicke

Basierend auf dem Typ ist der Markt für Hartschaumstoffe in Polyurethanschaum, Polystyrolschaum, Polypropylenschaum, Polyethylenschaum, Polyvinylchloridschaum und andere unterteilt. Das Segment Polyurethanschaum dominiert den globalen Markt für Hartschaumstoffe. Harter Polyurethanschaum wird aufgrund seiner hervorragenden Isoliereigenschaften und guten Dimensionsstabilität häufig in der Kühl-, Bau- und Verpackungsindustrie verwendet.

Einblicke in die Endverbraucherbranche

Der Markt für Hartschaumstoffe ist nach Endverbraucherbranchen in Bauwesen, Haushaltsgeräte, Verpackung, Automobilindustrie und andere unterteilt. Der Bausektor machte den größten Anteil am globalen Markt für Hartschaumstoffe aus. Ihr Einsatz beim Bau von Häusern und Gebäuden reduziert den Energiebedarf zum Heizen und Kühlen von Innenräumen von Gebäuden, Geschäften und Büros. Der steigende Verbrauch von Hartschaumstoffen im Bausektor dürfte das Wachstum des globalen Marktes für Hartschaumstoffe im Prognosezeitraum unterstützen.

Unternehmen verfolgen häufig verschiedene Strategien, um ihre weltweite Präsenz auszubauen. Huntsman Corporation, Covestro und BASF SE gehören zu den Hauptakteuren auf dem globalen Markt für Hartschaumstoffe, die diese Strategien umsetzen, um ihren Kundenstamm zu erweitern und bedeutende Marktanteile zu gewinnen, was ihnen wiederum ermöglicht, ihren Markennamen weltweit zu behaupten.

Hartschaum

Regionale Einblicke in den HartschaummarktDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Hartschaummarkt im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts über Hartschaum

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2018 | US$ 73.79 Billion |

| Marktgröße nach 2027 | US$ 131.56 Billion |

| Globale CAGR (2018 - 2027) | 6.7% |

| Historische Daten | 2016-2017 |

| Prognosezeitraum | 2019-2027 |

| Abgedeckte Segmente |

By Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Hartschaum: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Hartschaumstoffe wächst rasant. Die steigende Nachfrage der Endverbraucher ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Hartschaum Übersicht der wichtigsten Akteure

- Fortschreitende Branchentrends im Hartschaummarkt helfen den Akteuren bei der Entwicklung effektiver langfristiger Strategien

- Geschäftswachstumsstrategien entwickelter und sich entwickelnder Märkte

- Quantitative Analyse des Hartschaummarktes von 2017 bis 2027

- Schätzung der Nachfrage nach Hartschaum in verschiedenen Branchen

- PEST-Analyse zur Veranschaulichung der Wirksamkeit von in der Branche tätigen Käufern und Lieferanten bei der Vorhersage des Marktwachstums

- Jüngste Entwicklungen zum Verständnis des Wettbewerbsmarktszenarios und der Nachfrage nach Hartschaum

- Markttrends und -aussichten in Verbindung mit Faktoren, die das Wachstum des Hartschaummarktes vorantreiben und hemmen

- Verständnis der Strategien, die das kommerzielle Interesse im Hinblick auf das Wachstum des Hartschaummarktes untermauern, was den Entscheidungsprozess für die Größe des Hartschaummarktes der Beteiligten an verschiedenen Marktknotenpunkten erleichtert

- Detaillierter Überblick und Segmentierung des Hartschaummarktes sowie seiner Dynamik in der Branche

Globaler Hartschaummarkt – nach Typ

- Polyurethanschaum

- Polystyrolschaum

- Polypropylenschaum

- Polyethylenschaum

- Polyvinylchloridschaum

- Sonstige

Globaler Markt für Hartschaum – nach Endverbrauchsbranche

- Bau & Bauwesen

- Haushaltsgeräte

- Verpackung

- Automobil

- Sonstige

Unternehmensprofile

- Saint-Gobain

- Dow Chemical Corporation

- BASF SE

- Borealis AG

- Sekisui Chemical Co.,Ltd

- Covestro AG

- Armacell International SA

- Huntsman International LLC

- JSP

- Zotefoams Plc

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends