Rapporto sul mercato della schiuma rigida 2027 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Mercato della schiuma rigida fino al 2027 - Analisi e previsioni globali per tipologia (schiuma di poliuretano, schiuma di polistirene, schiuma di polipropilene, schiuma di polietilene, schiuma di cloruro di polivinile e altri), settore di utilizzo finale (edilizia e costruzioni, elettrodomestici, imballaggi, automotive e altri)

- Stato : Edito

- Codice del report : TIPRE00005351

- Categoria : Prodotti chimici e materiali

- Numero di pagine : 144

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 17, 2024

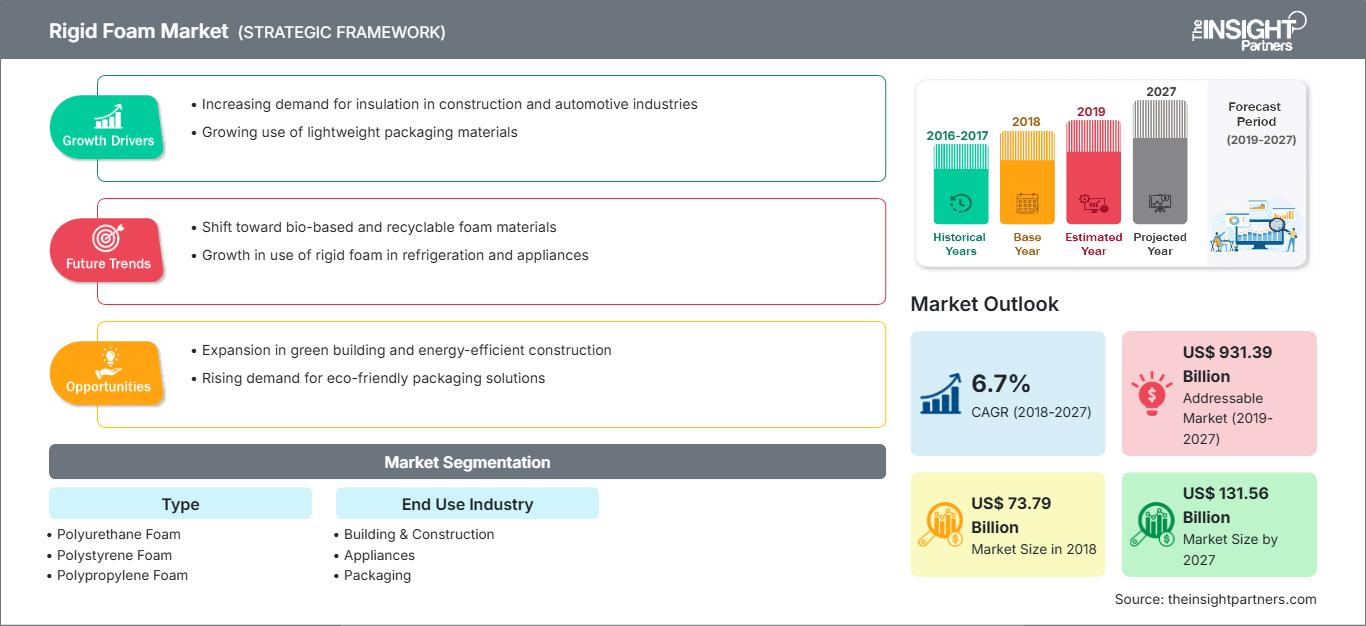

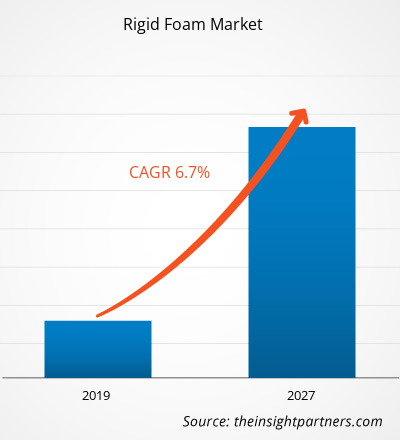

[Rapporto di ricerca]Il mercato della schiuma rigida ha rappresentato 73.786,7 milioni di dollari nel 2018 e si prevede che crescerà a un CAGR del 6,7% nel periodo di previsione 2019-2027, fino a raggiungere i 131.558,9 milioni di dollari entro il 2027.

Le schiume rigide sono note per possedere diverse proprietà, come impermeabilità, antistatiche, antivibrazioni e antiscivolo, che le rendono un materiale ideale per l'utilizzo in molti settori industriali e edili. La schiuma rigida protegge le superfici in calcestruzzo su cui viene applicata e prolunga la durata dei pavimenti in calcestruzzo sottostanti. È inerte a oli, detergenti e detergenti, fluidi di trasmissione, acqua, grandine, neve e sostanze chimiche corrosive. La schiuma rigida viene utilizzata anche per migliorare l'aspetto estetico del pavimento. È disponibile in diversi colori, tonalità e texture. Pigmenti metallici e scaglie di colore vinilico vengono aggiunti ai sistemi di schiuma rigida per produrre superfici dai colori iridescenti. Si prevede che l'appeal estetico della schiuma rigida colorata guiderà il mercato della schiuma rigida e il suo utilizzo è sempre più diffuso nei nuovi progetti edilizi e nelle ristrutturazioni di vecchie case.

Nel 2018, l'area Asia-Pacifico deteneva la quota maggiore del mercato globale delle schiume rigide. Questa crescita del mercato nell'area Asia-Pacifico è principalmente attribuibile alla presenza di importanti produttori di schiuma rigida nella regione. Inoltre, si prevede che l'aumento delle attività produttive di schiuma rigida alimenterà la crescita del mercato tra il 2019 e il 2027. Nell'area Asia-Pacifico, la Cina ha rappresentato la quota maggiore di schiume rigide in termini di fatturato generato.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato della schiuma rigida: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Negli ultimi anni si sono registrati rapidi progressi nel campo dei polimeri, con un aumento della produzione di materie plastiche e polimeri. Si prevede che una tendenza al rialzo nell'industria dei polimeri genererà un'elevata percentuale di scarti di polimeri. Inoltre, sono state emanate nuove norme e regolamenti sulla scia della tutela ambientale, che stanno spingendo scienziati e imprenditori a cercare soluzioni alternative per la gestione e il trattamento dei rifiuti plastici o l'adozione di plastiche biodegradabili che potrebbero decomporsi nell'ambiente naturale. Tra i diversi tipi di plastiche biodegradabili prodotte in tutto il mondo, il polilattide (PLA) è considerato una delle forme preferite di bioplastiche. I rifiuti generati da queste plastiche possono essere facilmente trasformati in un prodotto di valore aggiunto come le schiume rigide di poliuretano-poliisocianurato (RPU/PIR). Tali schiume prodotte da polilattide biodegradabile sono considerate soluzioni sostenibili. Secondo uno studio presentato da Europe PMC, il polilattide può sostituire parzialmente il poliolo petrolchimico nella formulazione del poliisocianurato. Inoltre, le schiume PIR ottenute possiedono diverse caratteristiche, come densità apparente minima, fragilità e capacità di assorbimento d'acqua. Pertanto, l'uso di poliolo PLA composto da rifiuti plastici può rappresentare un'ottima alternativa ai polioli petrolchimici. Tali sviluppi contribuiscono alla gestione delle risorse limitate e all'utilizzo efficace dei rifiuti. Inoltre, i prodotti realizzati con tale biomateriale sono considerati soluzioni ecocompatibili.

Approfondimenti sulle tipologie

In base alla tipologia, il mercato delle schiume rigide si divide in schiuma di poliuretano, schiuma di polistirene, schiuma di polipropilene, schiuma di polietilene, schiuma di polivinilcloruro e altre. Il segmento della schiuma di poliuretano ha dominato il mercato globale delle schiume rigide. La schiuma di poliuretano rigida è ampiamente utilizzata nei settori della refrigerazione, dell'edilizia e dell'imballaggio grazie alle sue eccellenti proprietà isolanti e alla buona stabilità dimensionale.

Approfondimenti sul settore di utilizzo finale

Il mercato della schiuma rigida è suddiviso in base al settore di utilizzo finale: edilizia, elettrodomestici, imballaggi, automotive e altri. Il segmento dell'edilizia rappresenta la quota maggiore del mercato globale della schiuma rigida. Il suo utilizzo nella costruzione di case ed edifici riduce l'energia necessaria per il riscaldamento e il raffreddamento degli spazi interni di edifici, negozi e uffici. Si prevede che il crescente consumo di schiume rigide da parte del settore dell'edilizia sosterrà la crescita del mercato globale della schiuma rigida durante il periodo di previsione.

Diverse strategie vengono comunemente adottate dalle aziende per espandere la propria presenza a livello mondiale. Huntsman Corporation, Covestro e BASF SE sono tra i principali attori del mercato globale della schiuma rigida che implementano queste strategie per ampliare la base clienti e acquisire una quota significativa, il che, a sua volta, consente loro di mantenere il proprio marchio a livello globale.

Approfondimenti regionali sul mercato della schiuma rigida

Le tendenze regionali e i fattori che influenzano il mercato della schiuma rigida durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato della schiuma rigida in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America meridionale e centrale.

Ambito del rapporto sul mercato della schiuma rigida

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2018 | US$ 73.79 Billion |

| Dimensioni del mercato per 2027 | US$ 131.56 Billion |

| CAGR globale (2018 - 2027) | 6.7% |

| Dati storici | 2016-2017 |

| Periodo di previsione | 2019-2027 |

| Segmenti coperti |

By Tipo

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato della schiuma rigida: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della schiuma rigida è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato della schiuma rigida Panoramica dei principali attori chiave

- Le tendenze progressive del settore nel mercato della schiuma rigida aiutano gli operatori a sviluppare strategie efficaci a lungo termine

- Strategie di crescita aziendale adottate dai mercati sviluppati e in via di sviluppo

- Analisi quantitativa del mercato della schiuma rigida dal 2017 al 2027

- Stima della domanda di schiuma rigida in vari settori

- Analisi PEST per illustrare l'efficacia di acquirenti e fornitori che operano nel settore nel prevedere la crescita del mercato

- Sviluppi recenti per comprendere lo scenario competitivo del mercato e la domanda di schiuma rigida

- Tendenze e prospettive di mercato insieme ai fattori che guidano e frenano la crescita del mercato della schiuma rigida

- Comprensione delle strategie che sostengono l'interesse commerciale per quanto riguarda la crescita del mercato della schiuma rigida, che facilita il processo decisionale per le dimensioni del mercato della schiuma rigida degli stakeholder in vari nodi del mercato

- Panoramica dettagliata e segmentazione del mercato della schiuma rigida, nonché le sue dinamiche nel industria

Mercato globale della schiuma rigida - per tipo

- Schiuma di poliuretano

- Schiuma di polistirene

- Schiuma di polipropilene

- Schiuma di polietilene

- Schiuma di cloruro di polivinile

- Altri

Mercato globale della schiuma rigida - per settore di utilizzo finale

- Edilizia e Edilizia

- Elettrodomestici

- Imballaggi

- Automotive

- Altro

Profili aziendali

- Saint-Gobain

- Dow Chemical Corporation

- BASF SE

- Borealis AG

- Sekisui Chemical Co.,Ltd

- Covestro AG

- Armacell International SA

- Huntsman International LLC

- JSP

- Zotefoams Plc

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative