Marktübersicht, Wachstum, Trends, Analyse, Forschungsbericht für Spiritusglasverpackungen (2022-2028)

Marktprognose für Spirituosenglasverpackungen bis 2028 – Globale Analyse nach Kapazität (bis 200 ml, 200 ml bis 750 ml und über 750 ml), Glasfarbe (unbehandeltes Glas und farbiges Glas) und Anwendung (Whisky, Wodka, Rum, Wein, Bier und andere)

- Status : Veröffentlicht

- Berichtscode : TIPRE00005316

- Kategorie : Chemikalien und Materialien

- Anzahl der Seiten : 160

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 17, 2024

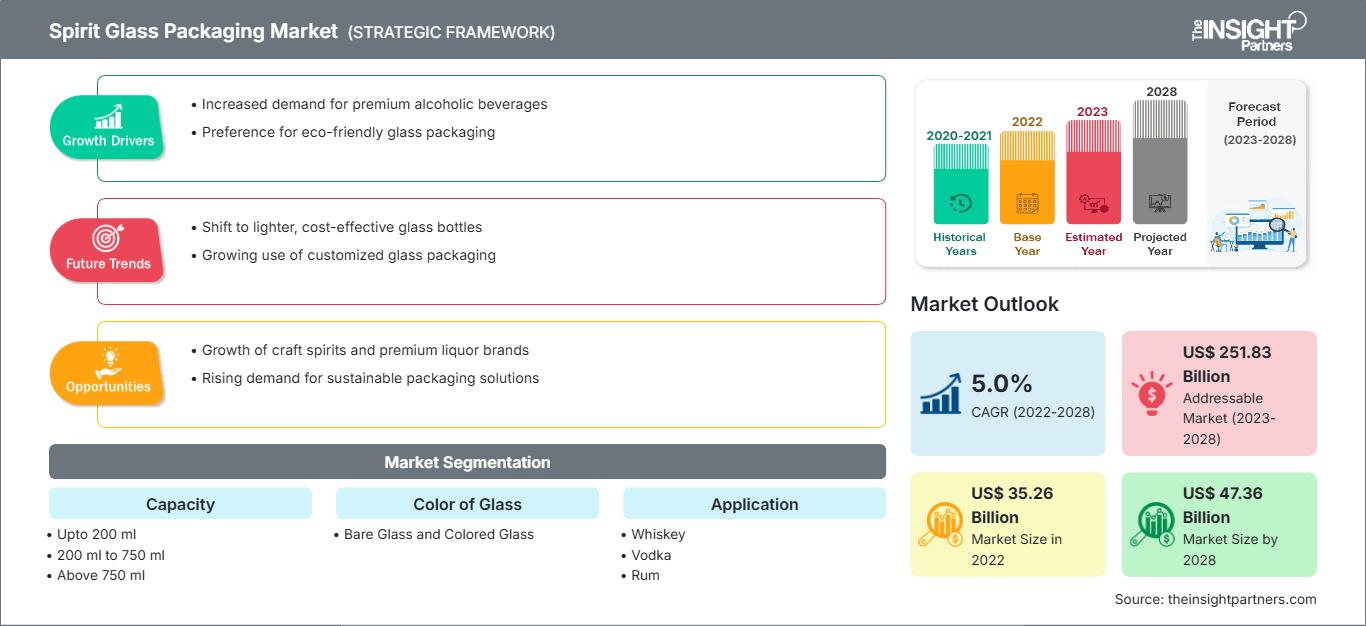

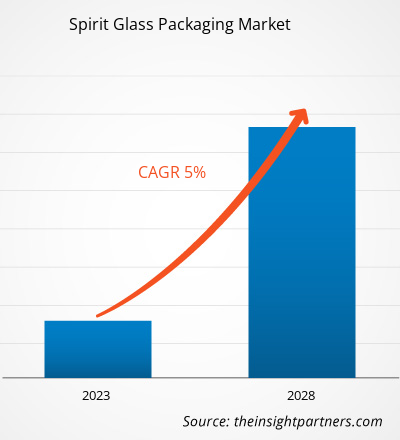

[Forschungsbericht]Der Markt für Spirituosenglasverpackungen wurde im Jahr 2022 auf 35.258,06 Millionen US-Dollar geschätzt und soll bis 2028 47.357,29 Millionen US-Dollar erreichen; von 2022 bis 2028 wird eine durchschnittliche jährliche Wachstumsrate von 5,0 % erwartet.

Spirituosenglasverpackungen werden in der Spirituosenindustrie häufig zur Verpackung von Spirituosenprodukten wie Wein, Bier, Rum, Whisky und Wodka verwendet. Die Produktinnovation verschiedener Spirituosen, wie z. B. aromatisierter Liköre, und die Entwicklung von Spirituosenmischungen in Flaschen schaffen eine Nachfrage nach Spirituosenglasverpackungen. Die individuell gestalteten und abwechslungsreichen farbigen Glasverpackungen verbessern das gesamte Sinneserlebnis und beeinflussen die Kaufentscheidung der Verbraucher. Design und Art der Glasverpackung wirken sich positiv auf das Markenimage, die Produktdifferenzierung sowie die Produktakzeptanz und -präferenz aus. Die steigende Vorliebe der Verbraucher für Glasverpackungen hat Spirituosenhersteller dazu veranlasst, sich durch Verpackungsdesign und innovative Produkte für Spirituosen zu differenzieren. Dies ist auf die Verfügbarkeit von Glasflaschen mit dickem Boden, Prägungen und Dekorationen sowie auf das Etikettendesign zurückzuführen; all diese Merkmale sorgen für ein harmonisches, hochwertiges Markenimage und transportieren die Marken- oder Produktgeschichte.

Im Jahr 2022 hatte der asiatisch-pazifische Raum den größten globalen Marktanteil bei Glasverpackungen für Spirituosen. Das Marktwachstum in Japan, Indien, China, Australien, Südkorea, Singapur, Taiwan und Indonesien wird auf den steigenden Alkoholkonsum der Bevölkerung, die Verschiebung der Vorlieben von Standard- zu Premium-Bieren, Whisky, Wodka, Wein und anderen Spirituosen, eine zunehmende Anzahl von Feiern mit alkoholischen Getränken und ungewöhnliche Produktinnovationen der Spirituosenhersteller in der gesamten Region zurückgeführt. So stellte beispielsweise die Scrapegrace Distillery, eine Brennerei mit Sitz in Neuseeland, im September 2020 den weltweit ersten natürlich schwarzen Gin (Naturally Black Brew) her, der aus einer Mischung ungewöhnlicher Pflanzenstoffe hergestellt wird. Dieser Premium-Gin verfärbt sich beim Mischen mit Tonic rot und violett. Die Brennerei verkaufte innerhalb von 24 Stunden einen Dreimonatsvorrat. Mit steigenden Produktverkäufen stieg auch die Nachfrage nach Glasverpackungen deutlich. All diese Faktoren tragen zum Wachstum des regionalen Marktes für Spirituosenglasverpackungen bei.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Spirituosenglasverpackungen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Auswirkungen der COVID-19-Pandemie auf den Markt für Spirituosenglasverpackungen

Die COVID-19-Pandemie hatte erhebliche Auswirkungen auf den Markt für Spirituosenglasverpackungen. Die weltweiten Lockdowns und Beschränkungen für Reisen und gesellschaftliche Zusammenkünfte haben zu einem Rückgang des Konsums alkoholischer Getränke und damit zu einer geringeren Nachfrage nach Spirituosenglasverpackungen geführt. Viele Bars, Restaurants und Hotels, wichtige Kunden des HORECA-Sektors, mussten vorübergehend schließen oder mit reduzierter Kapazität arbeiten, was zu einer geringeren Nachfrage nach kleineren Glasflaschen führte. Darüber hinaus haben Unterbrechungen der Lieferkette aufgrund von Transport- und Fertigungsbeschränkungen die Kosten für Produktion und Vertrieb von Spirituosenglasverpackungen erhöht.

Im Jahr 2021 begann sich der globale Markt von den Verlusten des Jahres 2020 zu erholen, da Regierungen verschiedener Länder Lockerungen der sozialen Beschränkungen ankündigten. Den Herstellern wurde erlaubt, mit voller Kapazität zu arbeiten, was ihnen half, die Lücke zwischen Angebot und Nachfrage zu schließen. Darüber hinaus trugen steigende Impfraten zu einer Verbesserung der Gesamtbedingungen in verschiedenen Ländern bei, was zu günstigen Bedingungen für industriellen und kommerziellen Fortschritt führte. Die zunehmenden Spirituosenproduktionskapazitäten im asiatisch-pazifischen Raum und in Europa haben die Nachfrage nach Spirituosenglasverpackungen im Jahr 2021 weiter erhöht.

Markteinblicke

Wachstum des HORECA-Sektors

Der HORECA-Sektor ist einer der wichtigsten Endverbraucher von Spirituosenglasverpackungen. HORECA steht für Hotel/Restaurant/Catering und ist ein Teil des Food-Service-Segments, zu dem unter anderem Bars, Pubs, Biercafés, Clubs und Hotels gehören. Der Einfluss von HORECA auf Spirituosenglasverpackungen ist aufgrund der großen Menge an Produkten, die der Sektor konsumiert, erheblich. Die Neigung der Weltbevölkerung zu Speisen und Getränken zum Mitnehmen und ein Anstieg des verfügbaren Einkommens kurbeln die HORECA-Branche weltweit an. Laut der National Restaurant Association (USA) ist die Lebensmittel- und Die Getränkeumsätze im Full-Service-Segment (darunter Familienrestaurants, Casual-Dining-Restaurants und Fine-Dining-Full-Service-Restaurants) stiegen von 199 Milliarden US-Dollar im Jahr 2020 auf 289 Milliarden US-Dollar im Jahr 2022. Im Gegensatz dazu stiegen die US-Umsätze im Limited-Service-Segment (darunter Schnellrestaurants, Fast-Casual-Restaurants und Cafeterias) von 297 Milliarden US-Dollar im Jahr 2020 auf 355 Milliarden US-Dollar im Jahr 2022. Der Bericht ergab, dass die Umsätze mit Lebensmitteln und Getränken Der Umsatz mit Getränken in den USA aus Bars, Tavernen, Nachtclubs oder an Orten, an denen alkoholische Getränke zubereitet und serviert werden, stieg von 13 Milliarden US-Dollar im Jahr 2020 auf 21 Milliarden US-Dollar im Jahr 2022.

Kapazitätseinblicke

Basierend auf der Kapazität ist der globale Markt für Spirituosenglasverpackungen in bis zu 200 ml, 200 ml bis 750 ml und über 750 ml segmentiert. Das Segment 200 ml bis 750 ml hatte im Jahr 2022 den größten Marktanteil bei Spirituosenglasverpackungen weltweit. Diese Kategorie umfasst Glasflaschen mit Kapazitäten wie 375 ml, 500 ml, 650 ml, 700 ml und 750 ml. Diese Arten von Glasflaschen sind in verschiedenen Formen und Designs erhältlich. Diese Glasflaschen sind in verschiedenen Farben erhältlich, beispielsweise Bernsteinbraun, Feuersteinweiß, Smaragdgrün, Saphirblau, Sonnengelb, Barrenschwarz und Gun Metallic. Sie werden hauptsächlich für die Verpackung von Brandy, Gin, Rum, Tequila, Wodka, Whisky, Wein, Bier usw. verwendet. 375-ml- und 650-ml-Flaschen werden hauptsächlich für Bier verwendet, während 750-ml-Flaschen hauptsächlich für Spirituosen wie Whisky, Gin, Rum, Tequila und Liköre verwendet werden. Darüber hinaus konzentrieren sich Hersteller von Spirituosengläsern auf die Herstellung attraktiver Glasflaschen mit unterschiedlichen Fassungsvermögen, die sich auf die Produktpreise und das Kaufverhalten der Verbraucher auswirken.

Zu den wichtigsten Akteuren auf dem globalen Markt für Spirituosenglasverpackungen gehören OI Glass Inc, Toyo Glass Co Ltd, Ardagh Group SA, Verallia SA, Vidrala SA, Gerresheimer AG, Nihon Yamamura Glass Co Ltd, Vitro SAB de CV, BA Glass BV und HEINZ-GLAS GmbH & Co KGaA. Akteure auf dem globalen Markt für Spirituosenglasverpackungen konzentrieren sich auf die Bereitstellung qualitativ hochwertiger Produkte, um die Kundennachfrage zu erfüllen. Sie konzentrieren sich auch auf Strategien wie Investitionen in Forschungs- und Entwicklungsaktivitäten und die Einführung neuer Produkte.

Berichts-Spotlights

- Fortschreitende Branchentrends auf dem Markt für Spirituosenglasverpackungen, um den Akteuren bei der Entwicklung effektiver langfristiger Strategien zu helfen

- Geschäftswachstumsstrategien in entwickelten und sich entwickelnden Märkten

- Quantitative Analyse des Marktes für Spirituosenglasverpackungen von 2020 bis 2028

- Schätzung der weltweiten Nachfrage nach Spirituosenglasverpackungen

- Porters Fünf-Kräfte-Analyse zur Veranschaulichung der Wirksamkeit von Käufern und Lieferanten in der Branche

- Jüngste Entwicklungen zum Verständnis des Wettbewerbsmarktszenarios

- Markttrends und -aussichten sowie Faktoren, die das Wachstum des Marktes für Spirituosenglasverpackungen vorantreiben und hemmen

- Unterstützung im Entscheidungsprozess durch Hervorhebung von Marktstrategien, die das kommerzielle Interesse untermauern und zum Marktwachstum führen

- Die Größe des Marktes für Spirituosenglasverpackungen an verschiedenen Knotenpunkten

- Detaillierte Übersicht und Segmentierung des Markt sowie die Dynamik der Spirituosenglasverpackungsindustrie

- Die Größe des Spirituosenglasverpackungsmarktes in verschiedenen Regionen mit vielversprechenden Wachstumschancen

Spirituosenglasverpackung

Regionale Einblicke in den Markt für SpirituosenglasverpackungenDie Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Spirituosenglasverpackungen im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.

Umfang des Marktberichts für Spirituosenglasverpackungen

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2022 | US$ 35.26 Billion |

| Marktgröße nach 2028 | US$ 47.36 Billion |

| Globale CAGR (2022 - 2028) | 5.0% |

| Historische Daten | 2020-2021 |

| Prognosezeitraum | 2023-2028 |

| Abgedeckte Segmente |

By Fassungsvermögen

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Spirituosenglasverpackungen: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Spirituosenglasverpackungen wächst rasant. Die steigende Nachfrage der Endverbraucher ist auf Faktoren wie veränderte Verbraucherpräferenzen, technologische Fortschritte und ein stärkeres Bewusstsein für die Produktvorteile zurückzuführen. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Spirituosenglasverpackungen Übersicht der wichtigsten Akteure

Globaler Markt für Spirituosenglasverpackungen

Basierend auf der Kapazität ist der globale Markt für Spirituosenglasverpackungen in bis zu 200 ml, 200 ml bis 750 ml und über 750 ml unterteilt. Basierend auf der Glasfarbe ist der Markt für Spirituosenglasverpackungen in unbehandeltes Glas und farbiges Glas unterteilt. Basierend auf der Anwendung ist der Markt für Spirituosenglasverpackungen in Whisky, Wodka, Rum, Wein, Bier und andere unterteilt.

Firmenprofile

- OI Glass Inc

- Toyo Glass Co Ltd

- Ardagh Group SA

- Verallia SA

- Vidrala SA

- Gerresheimer AG

- Nihon Yamamura Glass Co Ltd

- Vitro SAB de CV

- BA Glass BV

- HEINZ-GLAS GmbH & Co KGaA.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends