Panoramica del mercato degli imballaggi in vetro per liquori, crescita, tendenze, analisi, rapporto di ricerca (2022-2028)

Previsioni del mercato degli imballaggi in vetro per alcolici fino al 2028 - Analisi globale per capacità (fino a 200 ml, da 200 ml a 750 ml e oltre 750 ml), colore del vetro (vetro nudo e vetro colorato) e applicazione (whisky, vodka, rum, vino, birra e altri)

- Stato : Edito

- Codice del report : TIPRE00005316

- Categoria : Prodotti chimici e materiali

- Numero di pagine : 160

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 17, 2024

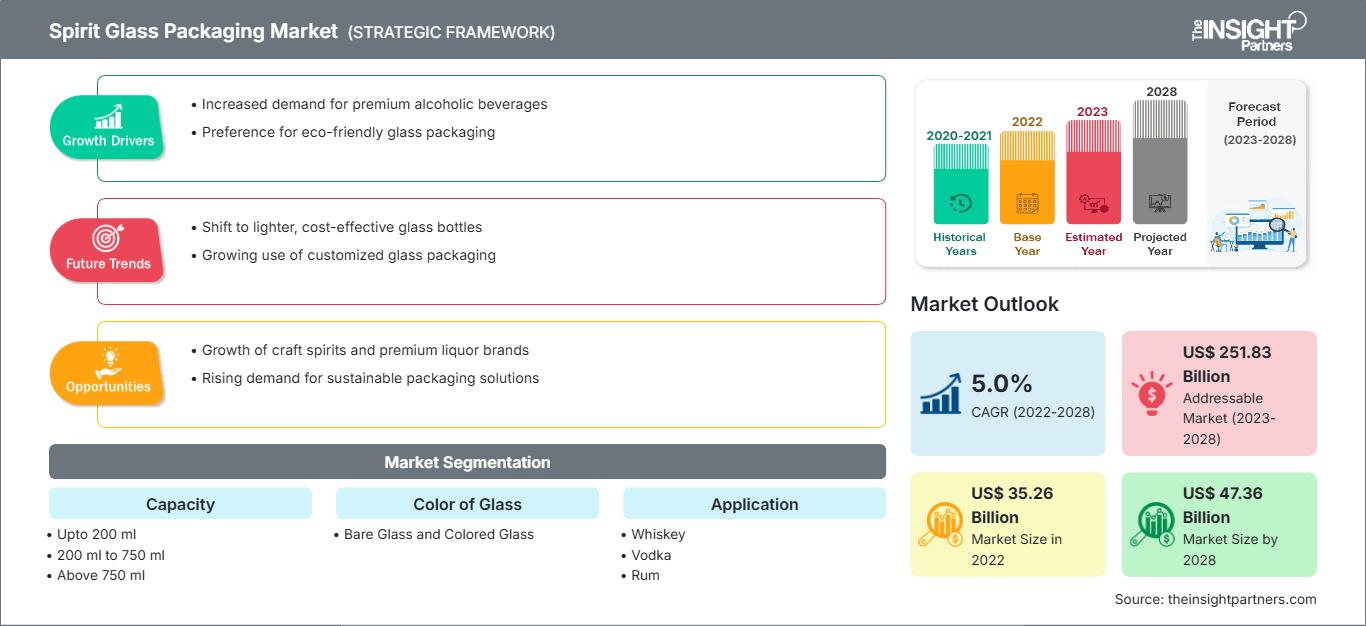

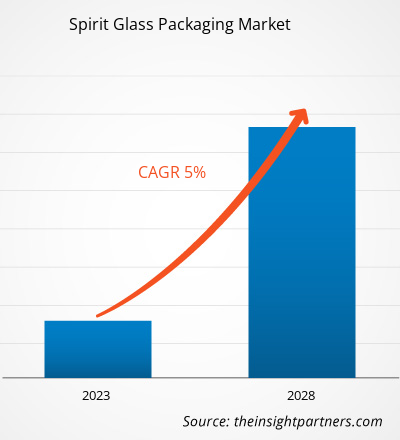

[Rapporto di ricerca]Il mercato degli imballaggi in vetro per alcolici è stato valutato a 35.258,06 milioni di dollari nel 2022 e si prevede che raggiungerà i 47.357,29 milioni di dollari entro il 2028; si stima che registrerà un CAGR del 5,0% dal 2022 al 2028.

Gli imballaggi in vetro per alcolici sono ampiamente utilizzati nel settore degli alcolici per contenere prodotti alcolici come vino, birra, rum, whisky e vodka, tra gli altri. L'innovazione di prodotto di diversi alcolici, come i liquori aromatizzati e lo sviluppo di miscele di alcolici in bottiglia, creano una domanda di imballaggi in vetro per alcolici. Gli imballaggi in vetro dal design distintivo e dai colori variegati migliorano l'esperienza sensoriale complessiva e influenzano la decisione di acquisto dei consumatori. Il design e la tipologia degli imballaggi in vetro influenzano positivamente l'immagine del marchio, la differenziazione del prodotto, l'accettabilità e la preferenza del prodotto. La crescente preferenza dei consumatori per gli imballaggi in vetro ha spinto i produttori di alcolici a offrire una differenziazione dei prodotti attraverso il design del packaging e prodotti innovativi. Ciò è dovuto alla disponibilità di bottiglie in vetro con fondo spesso, goffrature e decorazioni, abbinate al design dell'etichetta; tutte queste caratteristiche forniscono un'immagine di marca armoniosa e di alta qualità e trasmettono la storia del marchio o del prodotto.

Nel 2022, l'Asia-Pacifico ha detenuto la maggiore quota di mercato globale degli imballaggi in vetro per alcolici. La crescita del mercato in Giappone, India, Cina, Australia, Corea del Sud, Singapore, Taiwan e Indonesia è attribuita al crescente consumo di alcol tra la popolazione; al cambiamento delle preferenze da birre standard a birre premium, whisky, vodka, vini e altri alcolici; a un numero crescente di celebrazioni con bevande alcoliche; e a innovazioni di prodotto insolite da parte dei produttori di alcolici in tutta la regione. Ad esempio, nel settembre 2020, la Scrapegrace Distillery, una distilleria con sede in Nuova Zelanda, ha prodotto il primo gin nero naturale al mondo (natural black brew), ottenuto da una miscela di botaniche insolite. Inoltre, questo gin premium assume tonalità rosse e viola se miscelato con acqua tonica. La distilleria ha venduto una fornitura di prodotto sufficiente per tre mesi in 24 ore. Con l'aumento delle vendite, anche la domanda di imballaggi in vetro è cresciuta in modo significativo. Tutti questi fattori contribuiscono alla crescita del mercato regionale degli imballaggi in vetro per alcolici.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato degli imballaggi in vetro per alcolici: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Impatto della pandemia di COVID-19 sul mercato del packaging in vetro per alcolici

La pandemia di COVID-19 ha avuto un impatto significativo sul mercato del packaging in vetro per alcolici. I lockdown globali e le restrizioni su viaggi e assembramenti sociali hanno portato a un calo del consumo di bevande alcoliche, con conseguente calo della domanda di packaging in vetro per alcolici. Molti bar, ristoranti e hotel, importanti clienti del settore HORECA, sono stati costretti a chiudere temporaneamente o a operare a capacità ridotta, con conseguente riduzione della domanda di bottiglie di vetro di piccole dimensioni. Inoltre, l'interruzione della catena di approvvigionamento dovuta alle restrizioni sui trasporti e sulle attività di produzione ha aumentato i costi di produzione e distribuzione del packaging in vetro per alcolici.

Nel 2021, il mercato globale ha iniziato a riprendersi dalle perdite subite nel 2020, con l'annuncio da parte dei governi di diversi paesi di un allentamento delle restrizioni sociali. Ai produttori è stato consentito di operare a piena capacità, il che li ha aiutati a colmare il divario tra domanda e offerta. Inoltre, l'aumento dei tassi di vaccinazione ha contribuito a migliorare le condizioni generali in diversi paesi, creando ambienti favorevoli al progresso industriale e commerciale. L'aumento della capacità produttiva di alcolici in Asia-Pacifico e in Europa ha ulteriormente aumentato la domanda di imballaggi in vetro per alcolici nel 2021.

Approfondimenti di mercato

Crescita del settore HORECA

Il settore HORECA è uno dei principali utilizzatori finali di imballaggi in vetro per alcolici. L'HORECA è chiamato Hotel/Restaurant/Catering, una parte del segmento della ristorazione che comprende bar, pub, birrerie, club e hotel, tra gli altri. L'impatto dell'HORECA sul packaging in vetro per alcolici è significativo a causa dell'elevato volume di prodotti consumati dal settore. La propensione della popolazione globale verso cibi e bevande da asporto e l'aumento del reddito disponibile stanno dando impulso al settore HORECA in tutto il mondo. Secondo la National Restaurant Association (USA), il settore alimentare e catering Le vendite di bevande del segmento full-service (che comprende ristoranti per famiglie, ristoranti informali e ristoranti raffinati) sono cresciute da 199 miliardi di dollari nel 2020 a 289 miliardi di dollari nel 2022. Al contrario, le vendite statunitensi del segmento a servizio limitato (che comprende ristoranti quick-service, ristoranti fast-casual e mense) sono aumentate da 297 miliardi di dollari nel 2020 a 355 miliardi di dollari nel 2022. Il rapporto ha rivelato che le vendite di cibo e bevande Le bevande negli Stati Uniti provenienti da bar, taverne, locali notturni o luoghi dedicati alla preparazione e alla somministrazione di bevande alcoliche sono cresciute da 13 miliardi di dollari nel 2020 a 21 miliardi di dollari nel 2022.

Informazioni sulla capacità

In base alla capacità, il mercato globale degli imballaggi in vetro per alcolici è segmentato in fino a 200 ml, da 200 ml a 750 ml e oltre 750 ml. Il segmento da 200 ml a 750 ml ha detenuto la quota di mercato globale più significativa degli imballaggi in vetro per alcolici nel 2022. Questa categoria include bottiglie di vetro con capacità come 375 ml, 500 ml, 650 ml, 700 ml e 750 ml. Questi tipi di bottiglie di vetro sono disponibili in varie forme e design. Inoltre, questi tipi di bottiglie di vetro sono disponibili in diversi colori, come marrone ambra, bianco flint, smeraldo, verde, blu zaffiro, giallo sole, nero lingotto e canna di fucile metallizzato. Queste bottiglie di vetro sono utilizzate principalmente per il confezionamento di brandy, gin, rum, tequila, vodka, whisky, vino, birra, ecc. Le bottiglie da 375 ml e 650 ml sono utilizzate principalmente per il confezionamento di birra, mentre quelle da 750 ml sono utilizzate principalmente per liquori come whisky, gin, rum, tequila e liquori. Inoltre, i produttori di vetro per alcolici si concentrano sulla realizzazione di bottiglie di vetro accattivanti di varie capacità, che influenzeranno i prezzi dei prodotti e il comportamento d'acquisto dei consumatori.

I principali attori che operano nel mercato globale del packaging in vetro per alcolici includono OI Glass Inc, Toyo Glass Co Ltd, Ardagh Group SA, Verallia SA, Vidrala SA, Gerresheimer AG, Nihon Yamamura Glass Co Ltd, Vitro SAB de CV, BA Glass BV e HEINZ-GLAS GmbH & Co KGaA. Gli operatori che operano nel mercato globale degli imballaggi in vetro per alcolici si concentrano sulla fornitura di prodotti di alta qualità per soddisfare la domanda dei clienti. Si concentrano inoltre su strategie quali investimenti in attività di ricerca e sviluppo e lanci di nuovi prodotti.

In evidenza nel rapporto

- Tendenze progressive del settore nel mercato degli imballaggi in vetro per alcolici per aiutare gli operatori a sviluppare strategie efficaci a lungo termine

- Strategie di crescita aziendale adottate dai mercati sviluppati e in via di sviluppo

- Analisi quantitativa del mercato degli imballaggi in vetro per alcolici dal 2020 al 2028

- Stima della domanda globale di imballaggi in vetro per alcolici

- Analisi delle cinque forze di Porter per illustrare l'efficacia di acquirenti e fornitori che operano nel settore

- Sviluppi recenti per comprendere lo scenario competitivo del mercato

- Tendenze e prospettive di mercato, nonché fattori che guidano e frenano la crescita del mercato degli imballaggi in vetro per alcolici

- Assistenza nel processo decisionale evidenziando le strategie di mercato che sostengono l'interesse commerciale, portando alla crescita del mercato

- Dimensioni del mercato degli imballaggi in vetro per alcolici a vari livelli nodi

- Panoramica dettagliata e segmentazione del mercato, nonché dinamiche del settore degli imballaggi in vetro per alcolici

- Dimensioni del mercato degli imballaggi in vetro per alcolici in varie regioni con promettenti opportunità di crescita

Approfondimenti regionali sul mercato degli imballaggi in vetro per alcolici

Le tendenze regionali e i fattori che influenzano il mercato degli imballaggi in vetro per alcolici durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato degli imballaggi in vetro per alcolici in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto sul mercato degli imballaggi in vetro per alcolici

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2022 | US$ 35.26 Billion |

| Dimensioni del mercato per 2028 | US$ 47.36 Billion |

| CAGR globale (2022 - 2028) | 5.0% |

| Dati storici | 2020-2021 |

| Periodo di previsione | 2023-2028 |

| Segmenti coperti |

By Capacità

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato degli imballaggi in vetro per alcolici: comprendere il suo impatto sulle dinamiche aziendali

Il mercato degli imballaggi in vetro per alcolici è in rapida crescita, trainato dalla crescente domanda da parte degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato degli imballaggi in vetro per alcolici Panoramica dei principali attori chiave

Mercato globale degli imballaggi in vetro per alcolici

In base alla capacità, il mercato globale degli imballaggi in vetro per alcolici è segmentato in fino a 200 ml, da 200 ml a 750 ml e oltre 750 ml. In base al colore del vetro, il mercato degli imballaggi in vetro per alcolici si divide in vetro nudo e vetro colorato. In base all'applicazione, il mercato degli imballaggi in vetro per alcolici è segmentato in whisky, vodka, rum, vino, birra e altri.

Profili aziendali

- OI Glass Inc

- Toyo Glass Co Ltd

- Ardagh Group SA

- Verallia SA

- Vidrala SA

- Gerresheimer AG

- Nihon Yamamura Glass Co Ltd

- Vitro SAB de CV

- BA Glass BV

- HEINZ-GLAS GmbH & Co KGaA.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative