Diagnóstico del cáncer colorrectal Estrategias de mercado, principales actores, oportunidades de crecimiento, análisis y pronóstico para 2028

Pronóstico del mercado de diagnóstico de cáncer colorrectal hasta 2028: análisis global por modalidad [pruebas de imagen (colonoscopia, colonografía por TC, sigmoidoscopia flexible, endoscopia con cápsula y otras) y pruebas de heces [prueba inmunoquímica fecal (FIT), prueba de sangre oculta en heces con guayaco (gFOBT) y prueba de ADN en heces]] y usuario final (hospitales, laboratorios de diagnóstico, institutos de investigación oncológica y otros).

- Estado : Publicada

- Código de informe : TIPRE00013454

- Categoría : Ciencias de la vida

- Número de páginas : 213

- Formatos de informe disponibles :

- Fecha de última actualización : June 19, 2024

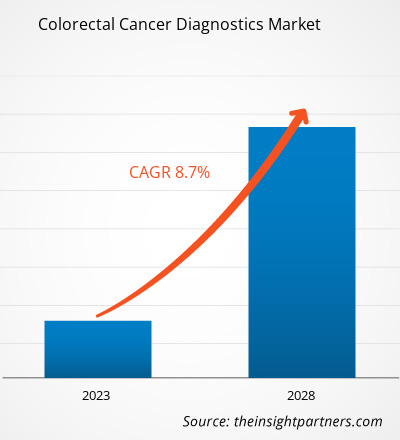

[Informe de investigación] Se espera que el tamaño del mercado de diagnóstico de cáncer colorrectal crezca de US$ 10.374,68 millones en 2022 a US$ 16.996,48 millones en 2028; se estima que registrará una CAGR del 8,7% entre 2023 y 2028.

El mercado de diagnóstico de cáncer colorrectal está segmentado en función de la modalidad, el usuario final y la geografía. El informe ofrece información y un análisis profundo del mercado, haciendo hincapié en parámetros como los impulsores, las tendencias, las oportunidades y el análisis del panorama competitivo de los principales actores del mercado en varias regiones. También incluye análisis del impacto de la pandemia de COVID-19 en las principales regiones.

Perspectivas del mercado

El lanzamiento de nuevos productos impulsa el tratamiento colorrectal

Los principales actores del mercado de diagnóstico del cáncer colorrectal fabrican una amplia gama de dispositivos que ayudan a reducir la carga del cáncer colorrectal y otras indicaciones asociadas, como pólipos de colon, enfermedad de Crohn, colitis y síndrome del intestino irritable. En julio de 2022, US Digestive Health (USDH), una red de consultorios gastrointestinales (GI) de primera categoría, anunció la comercialización de pruebas de detección mediante colonoscopia asistida por IA con la instalación más grande del país de módulos de endoscopia GI inteligentes Genious. Se espera que estos módulos ayuden a los médicos a identificar pólipos difíciles de detectar y potencialmente cancerosos en tiempo real. Con el lanzamiento de este dispositivo, los pacientes del sureste, suroeste y centro de Pensilvania ahora pueden acceder a la colonoscopia asistida por IA con capacidades mejoradas. En septiembre de 2020, Olympus Corporation anunció el lanzamiento de ENDO-AID, una plataforma de vanguardia impulsada por inteligencia artificial (IA). La plataforma incluye la aplicación (app) ENDO-AID CADe, un método endoscópico asistido por computadora para la detección de diferentes afecciones del colon. Esta nueva plataforma de IA permite la visualización en tiempo real de lesiones sospechosas detectadas automáticamente y funciona en combinación con su sistema EVIS X1. Por lo tanto, los desarrollos frecuentes y los lanzamientos de nuevos productos impulsan el crecimiento del mercado de diagnóstico del cáncer colorrectal.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de diagnóstico del cáncer colorrectal: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Perspectivas basadas en modalidades

Según la modalidad, el mercado de diagnóstico del cáncer colorrectal se bifurca en pruebas basadas en heces y pruebas de imagen. En 2022, el segmento de pruebas de imagen tuvo una mayor participación en el mercado de diagnóstico del cáncer colorrectal y se prevé que registre una CAGR más alta durante el período de pronóstico. El uso de pruebas de imagen en el diagnóstico del cáncer colorrectal ha evolucionado en los últimos años. Los resultados de las imágenes son fundamentales para la vigilancia, el diagnóstico, la estadificación, la selección del tratamiento y la programación del seguimiento. Las pruebas de imagen implican observar la estructura del colon y el recto para detectar la presencia de áreas anormales. Los exámenes de imagen utilizan endoscopios, instrumentos similares a tubos con una luz y una pequeña cámara de video en su extremo, que se insertan en el recto. Estas pruebas escanean el interior del colon y el recto en busca de áreas anormales que puedan ser cáncer o pólipos. Estas pruebas se utilizan con menos frecuencia que las pruebas basadas en heces y requieren más preparación previa y tienen algunos riesgos asociados, a diferencia de las pruebas basadas en heces. Las pruebas de imagen se clasifican además en colonoscopia, colonografía por TC, sigmoidoscopia flexible, endoscopia con cápsula y otras.

El segmento de colonoscopia tuvo la mayor participación del mercado en 2022. Sin embargo, se espera que la colonografía por TC crezca a un ritmo más rápido durante el período de pronóstico. La colonografía por TC ayuda en el análisis morfológico de las deformidades de la pared, proporcionando la información necesaria para la evaluación preoperatoria de la estadificación T en el cáncer colorrectal. Según las pautas de los Criterios de evaluación de respuesta en tumores sólidos (RECIST), la TC es la modalidad más utilizada para evaluar la respuesta al tratamiento en pacientes con tumores de colon y recto metastásicos. Las ventajas comunes de la colonografía por TC son las siguientes: es rápida y segura, ayuda a visualizar todo el colon y no se requiere sedación para realizar la prueba. Se recomienda realizar esta prueba cada cinco años en pacientes asintomáticos con riesgo medio.

Información basada en el usuario final

Según el usuario final, el mercado de diagnóstico del cáncer colorrectal se segmenta en hospitales, laboratorios de diagnóstico, institutos de investigación del cáncer y otros. El segmento de hospitales representó la mayor participación de mercado en 2022 y se prevé que registre la CAGR más alta durante el período de pronóstico.

Los actores del mercado de diagnóstico de cáncer colorrectal adoptan estrategias orgánicas, como el lanzamiento y la expansión de productos, para ampliar su presencia geográfica y sus carteras de productos y satisfacer las crecientes demandas. Las estrategias de crecimiento inorgánico adoptadas por los actores del mercado les permiten expandir sus negocios y mejorar su presencia geográfica. Además, estas estrategias de crecimiento ayudan a las empresas a fortalecer su clientela y ampliar sus carteras de productos.

- En diciembre de 2022, Epigenomics obtiene la licencia de tecnología de biomarcadores proteicos para pruebas de detección de cáncer colorrectal basadas en sangre. La empresa ha obtenido la licencia del MD Anderson Cancer Center de la Universidad de Texas sobre determinados derechos de patente y tecnología para biomarcadores asociados con la detección del cáncer colorrectal.

- En agosto de 2021, Illumina adquirió GRAIL para acelerar el acceso de los pacientes a una prueba de detección temprana de múltiples tipos de cáncer que les permite salvar vidas. La prueba de sangre Galleri de GRAIL detecta 50 tipos de cáncer diferentes antes de que presenten síntomas. La adquisición de GRAIL por parte de Illumina acelerará el acceso y la adopción de esta prueba que salva vidas en todo el mundo.

Perspectivas regionales del mercado de diagnóstico del cáncer colorrectal

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de diagnóstico de cáncer colorrectal durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de diagnóstico de cáncer colorrectal en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de diagnóstico de cáncer colorrectal

Alcance del informe de mercado sobre diagnóstico de cáncer colorrectal

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2022 | US$ 10.37 mil millones |

| Tamaño del mercado en 2028 | 17 mil millones de dólares estadounidenses |

| CAGR global (2022-2028) | 8,7% |

| Datos históricos | 2020-2021 |

| Período de pronóstico | 2023-2028 |

| Segmentos cubiertos |

Por modalidad

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de diagnóstico de cáncer colorrectal: comprensión de su impacto en la dinámica empresarial

El mercado de diagnóstico de cáncer colorrectal está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de diagnóstico de cáncer colorrectal son:

- Medtronic S.A.

- Illumina Inc

- Tecnologías de genómica clínica Pty Ltd

- Corporación EDP Biotech

- Epigenómica AG

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de diagnóstico de cáncer colorrectal

Perfiles de empresas

- Medtronic S.A.

- Illumina Inc

- Tecnologías de genómica clínica Pty Ltd

- Corporación EDP Biotech

- Epigenómica AG

- F. Hoffmann-La Roche Ltd

- Quest Diagnostics Inc

- Novigenix SA

- Siemens Healthineers AG

- Corporación Bruker

- Compañía química Eiken, Ltd.

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias