Análisis y pronóstico del mercado de aceites y grasas comestibles por tamaño, participación, crecimiento y tendencias para 2030

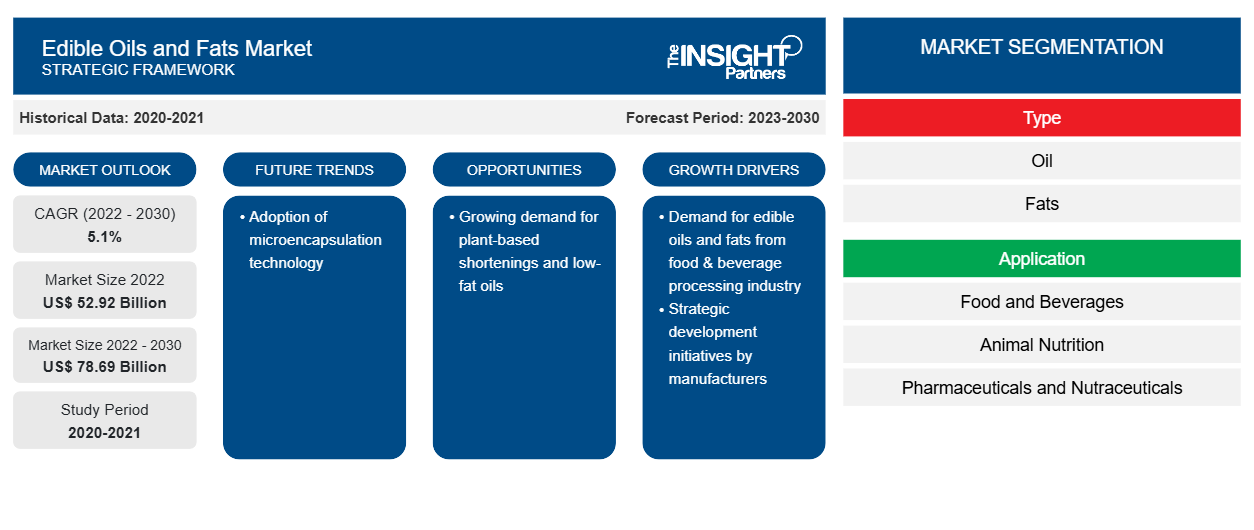

Datos históricos : 2020-2021 | Año base : 2022 | Período de pronóstico : 2023-2030Tamaño y pronósticos del mercado de aceites y grasas comestibles (2020-2030), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo [aceite (aceite de soja, aceite de girasol, aceite de palma, aceite de canola/colza y otros) y grasas (mantequilla, margarina, manteca vegetal a base de aceite de palma y otras)] y aplicación [alimentos y bebidas (panadería y confitería, lácteos y postres congelados, comidas listas para comer y listas para comer, refrigerios y otros), nutrición animal, y productos farmacéuticos y nutracéuticos].

- Estado : Publicada

- Código de informe : TIPRE00030249

- Categoría : Alimentos y bebidas

- Número de páginas : 150

- Formatos de informe disponibles :

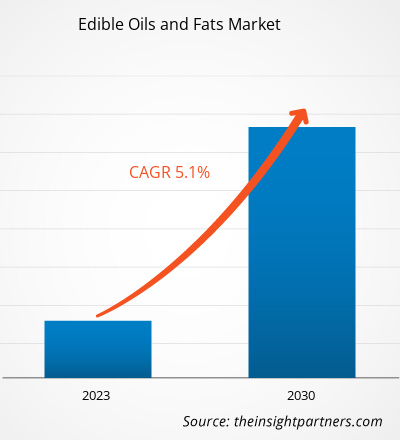

[Informe de investigación] Se espera que el mercado de aceites y grasas comestibles crezca de US$ 52.920,00 millones en 2022 a US$ 78.686,61 millones en 2030; se espera que registre una CAGR del 5,1% de 2023 a 2030.

Perspectivas del mercado y opinión de analistas:

Las grasas comestibles se obtienen a partir de materias primas de origen animal, como la manteca de cerdo y el sebo, o de origen vegetal. Los procesadores de carne son los proveedores de materias primas para los fabricantes de grasas comestibles de origen animal. Los fabricantes tienen acuerdos a largo plazo con las industrias de procesamiento de carne para un suministro ininterrumpido de materias primas. Los tejidos grasos de cerdo o de vacuno se cortan en trozos pequeños y se hierven en digestores de vapor, donde la grasa se libera en agua. La grasa flota sobre la superficie del agua y se recoge mediante desnatado. La materia membranosa de los tejidos animales se prensa en una prensa hidráulica donde se obtiene grasa adicional. La grasa se separa de la fase líquida en una centrífuga desfangadora.

Las grasas vegetales como la margarina se obtienen por hidrogenación de aceite de soja, aceite de maíz o aceite de cártamo. Primero se blanquea el aceite con tierra decolorante o carbón para eliminar el olor y el color indeseables. Luego se pasa por gas hidrógeno a alta presión, lo que solidifica el aceite para obtener la margarina. Existen varios procesos para fabricar aceites y grasas vegetales.

Los aceites y grasas comestibles refinados se envasan en contenedores y se envían a los usuarios finales, como las industrias de alimentos y bebidas, nutrición animal y productos farmacéuticos y nutracéuticos, a través de distribuidores y proveedores. Cargill Incorporated, Bunge Limited, ADM, Fuji Oil Co Ltd y Kao Corporation se encuentran entre los principales fabricantes de aceites y grasas comestibles en todo el mundo.

Factores impulsores del crecimiento y desafíos:

Según el Departamento de Agricultura de los Estados Unidos (USDA), el aceite de soja es el segundo aceite vegetal más consumido. Se utiliza ampliamente para freír, cocinar, manteca y margarina. Según la Organización para la Cooperación y el Desarrollo Económicos (OCDE), en 2022, el consumo de aceite vegetal alcanzó los 249 millones de toneladas métricas, y el sector alimentario representa la mayor parte. Además, la industria de la confitería utiliza significativamente la mantequilla como ingrediente principal, seguida de la margarina. Los aceites y grasas comestibles de alta calidad se utilizan en panadería y confitería, productos lácteos y postres helados, bocadillos, comidas listas para comer (RTE) y listas para cocinar (RTC) y otros alimentos y bebidas. Los aceites y grasas refinados son una rica fuente de lípidos. Por lo tanto, su uso está aumentando debido al aumento de su aplicación y al crecimiento de la población mundial.

La industria de alimentos y bebidas en varias regiones, como América del Norte y Asia Pacífico, está creciendo continuamente debido a una creciente inclinación hacia la sostenibilidad, la preferencia por los productos de conveniencia y listos para comer, y la creciente adopción de productos orgánicos y de origen vegetal. La industria está siendo testigo de un movimiento sustancial con la innovación en procesos, productos y servicios para satisfacer las preferencias de los consumidores que cambian rápidamente. Según la Oficina del Censo de los Estados Unidos, Estados Unidos tenía 39.646 plantas de fabricación de alimentos y bebidas en 2020. De las cuales California, Texas y Nueva York tenían 6.116, 2.625 y 2.600 respectivamente. De manera similar, la industria de alimentos y bebidas es uno de los contribuyentes importantes a la economía europea. Por lo tanto, la creciente industria de alimentos y bebidas en todo el mundo impulsa la demanda de aceites y grasas comestibles.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de aceites y grasas comestibles: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Segmentación y alcance del informe:

El " Mercado mundial de aceites y grasas comestibles " está segmentado en función del tipo, la aplicación y la geografía. Según el tipo, el mercado se divide en aceites y grasas. Según la aplicación, los aceites y grasas comestibles mundiales se dividen en alimentos y bebidas, nutrición animal y productos farmacéuticos y nutracéuticos. El segmento de aceites tenía una mayor participación en el mercado mundial.

Mercado de aceites y grasas comestibles

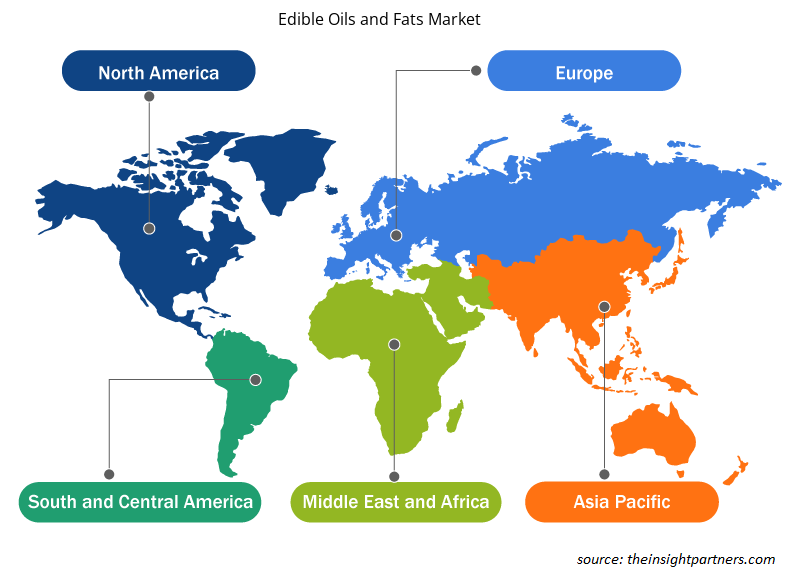

en 2022. Según la geografía, el mercado de aceites y grasas comestibles está segmentado en América del Norte (EE. UU., Canadá y México), Europa (Alemania, Francia, Italia, Reino Unido, Rusia y el resto de Europa), Asia Pacífico (Australia, China, Japón, India, Corea del Sur y el resto de Asia Pacífico), Medio Oriente y África (Sudáfrica, Arabia Saudita, Emiratos Árabes Unidos y el resto de Medio Oriente y África) y América del Sur y Central (Brasil, Chile y el resto de América del Sur y Central).

Análisis segmental:

Según el tipo, el mercado de aceites y grasas comestibles se bifurca en aceite y grasas. El segmento de aceite tuvo una mayor participación en el mercado de aceites y grasas comestibles en 2022 y se espera que registre una CAGR más alta durante el período de pronóstico. Los aceites vegetales pueden derivarse de semillas, cereales, nueces y frutas. Los aceites de oliva, girasol, palma, canola, coco, cártamo, maíz, maní, semilla de algodón, palmiste y soja se encuentran entre los aceites más consumidos. Generalmente, los aceites vegetales se utilizan en la preparación de alimentos y se agrega aceite crudo para darle sabor. El aceite vegetal también se utiliza en la producción de alimentos para animales. Los aceites de palma son fáciles de estabilizar y mantienen la calidad y la consistencia del sabor en los alimentos procesados. Por lo tanto, los fabricantes de alimentos los prefieren con frecuencia. Indonesia, Malasia, Tailandia y Nigeria se encuentran entre los mayores productores y exportadores de aceite de palma. La creciente conciencia relacionada con los problemas de salud asociados con las grasas trans en los aceites vegetales hidrogenados impulsa el uso de aceite de palma en la industria alimentaria. La industria agroalimentaria es un importante consumidor de aceite de palma, ya que se utiliza principalmente en productos de panadería industrial, productos de chocolate, confitería, helados e incluso sustitutos de comidas dietéticas. El aceite de palma es una fuente rica de tocoferoles y carotenoides, que le confieren estabilidad natural frente al deterioro oxidativo. Por tanto, los beneficios y las aplicaciones de los aceites de palma en diversas industrias de uso final impulsan su demanda en todo el mundo.

Análisis regional:

El mercado de aceites y grasas comestibles está segmentado en cinco regiones clave: América del Norte, Europa, Asia Pacífico, América del Sur y Central, y Oriente Medio y África. El mercado mundial de aceites y grasas comestibles estaba dominado por América del Sur y Central y se estimó que sería de unos 4.500 mil millones de dólares estadounidenses en 2022. El mercado de aceites y grasas comestibles en América del Sur y Central está segmentado en Brasil, Argentina y el resto de América del Sur y Central. El sector de los snacks en la región se está expandiendo debido a la creciente preferencia de los consumidores por diferentes opciones de snacks, como snacks congelados, snacks salados, snacks de frutas, snacks de confitería y snacks de panadería. Los aceites y grasas comestibles desempeñan un papel integral, ya que aportan sabores distintivos a los alimentos y proporcionan funciones únicas y deseables en la fabricación de snacks. Por ejemplo, los aceites son los medios de fritura para los alimentos fritos, y en los pasteles, se añaden mantecas a base de aceite vegetal para evitar que la harina y otros ingredientes se aglomeren. Por lo tanto, la creciente demanda de diferentes snacks y los beneficios asociados a los aceites y grasas comestibles impulsan la demanda de aceites y grasas comestibles en el sector de snacks en América del Sur y Central.

Además, la demanda de aceites y grasas comestibles en industrias de uso final como la nutrición animal ha experimentado un aumento en América del Sur y Central. Según Oil World, en 2022, China compró alrededor del 70% del aceite de soja brasileño, principalmente para el consumo de proteínas animales. Además, la expansión de las industrias de nutrición animal, farmacéutica y nutracéutica impulsa la demanda de aceites y grasas comestibles especializados. Estas industrias requieren tipos específicos de aceites para diversas aplicaciones, como en formulaciones de alimentos para animales y formulaciones farmacéuticas. A medida que estos sectores crecen y se diversifican, aumenta la demanda de sus requisitos únicos, lo que impulsa el crecimiento del mercado de aceites y grasas comestibles en América del Sur y Central.

Desarrollos industriales y oportunidades futuras:

A continuación se enumeran varias iniciativas adoptadas por los actores clave que operan en el mercado mundial de aceites y grasas comestibles:

- En octubre de 2021, ADM, uno de los principales fabricantes de aceites y grasas comestibles de EE. UU., anunció sus planes de construir la primera planta de trituración y refinería de soja dedicada en Dakota del Norte para atender la creciente demanda de aceite de soja de las industrias de alimentos y piensos.

- En diciembre de 2021, ITOCHU Corporation, con sede en Japón, anunció su acuerdo a través de ITOCHU International Inc., con sede en Nueva York, EE. UU., para el establecimiento de Fuji Oil International Inc. en EE. UU. Con este acuerdo, la firma planea fortalecer el negocio de aceites y grasas en América del Norte.

Perspectivas regionales del mercado de aceites y grasas comestibles

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de aceites y grasas comestibles durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de aceites y grasas comestibles en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de aceites y grasas comestibles

Alcance del informe de mercado de aceites y grasas comestibles

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2022 | US$ 52,92 mil millones |

| Tamaño del mercado en 2030 | US$ 78,69 mil millones |

| CAGR global (2022-2030) | 5,1% |

| Datos históricos | 2020-2021 |

| Período de pronóstico | 2023-2030 |

| Segmentos cubiertos |

Por tipo

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado: comprensión de su impacto en la dinámica empresarial

El mercado de aceites y grasas comestibles está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de aceites y grasas comestibles son:

- Bunge Ltd

- Condado Archer-Daniels-Midland

- Compañía petrolera Fuji Ltd.

- Corporación Kao

- AAK AB

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de aceites y grasas comestibles

Impacto de la pandemia de COVID-19:

La pandemia de COVID-19 afectó a las economías e industrias de varios países. Los confinamientos, las prohibiciones de viajes y los cierres de empresas en los principales países de América del Norte, Europa, Asia Pacífico (APAC), América del Sur y Central, y Oriente Medio y África (MEA) afectaron negativamente al crecimiento de varias industrias, incluida la industria de alimentos y bebidas. El cierre de las unidades de fabricación perturbó las cadenas de suministro globales, las actividades de fabricación, los cronogramas de entrega y las ventas de varios productos esenciales y no esenciales. Varias empresas anunciaron posibles retrasos en las entregas de productos y una caída en las ventas futuras de sus productos en 2020. Además, las prohibiciones impuestas por varios gobiernos en Europa, Asia y América del Norte a los viajes internacionales obligaron a las empresas a suspender temporalmente sus planes de colaboración y asociación. Todos estos factores obstaculizaron la industria de alimentos y bebidas en 2020 y principios de 2021, lo que restringió el crecimiento del mercado de aceites y grasas comestibles.

Panorama competitivo y empresas clave:

Bunge Ltd, Archer-Daniels-Midland Co., Fuji Oil Co Ltd, Kao Corp, AAK AB, J-Oil Mills Inc, Cargill Inc, Olam Group Ltd, ConnOils LLC y Louis Dreyfus Co BV. se encuentran entre los actores destacados que operan en el mercado global de aceites y grasas comestibles. Estos fabricantes de aceites y grasas comestibles ofrecen soluciones de extractos de vanguardia con características innovadoras para brindar una experiencia superior a los consumidores.

- Análisis histórico (2 años), año base, pronóstico (7 años) con CAGR

- Análisis PEST y FODA

- Tamaño del mercado, valor/volumen: global, regional y nacional

- Industria y panorama competitivo

- Conjunto de datos de Excel

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias

Desbloquea descuentos exclusivos en informes

Consultar ahora

Obtenga una muestra gratuita para - Mercado de aceites y grasas comestibles

Obtenga una muestra gratuita para - Mercado de aceites y grasas comestibles