Informe de mercado de Tratamiento de hematuria 2031 por segmentos, geografía, dinámica, desarrollos recientes e ideas estratégicas

Tamaño y pronóstico del mercado de tratamiento de la hematuria (2021-2031), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tratamiento (fármacos, terapias, otros); indicación (infecciones del tracto urinario, cálculos renales, uretritis, cáncer de sangre, cálculos vesicales, cáncer de próstata, cistitis, traumatismo, ejercicio vigoroso, enfermedad renal poliquística, endometriosis, menstruación); tipo (hematuria macroscópica, hematuria microscópica, hematuria idiopática, hematuria del corredor), usuario final (hospitales, clínicas, centros de cirugía ambulatoria, otros) y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00004601

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : February 15, 2025

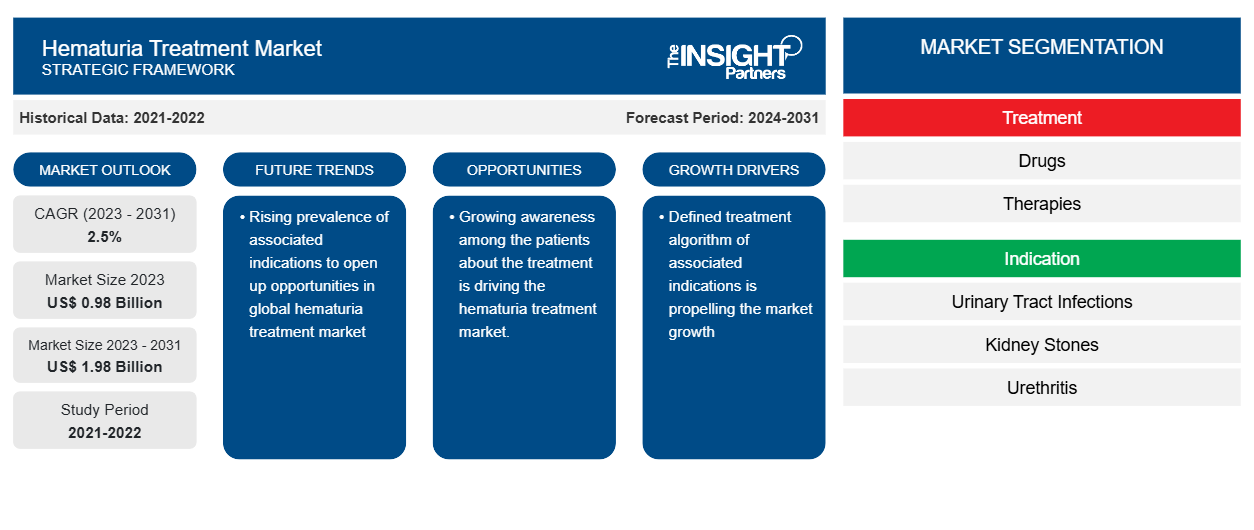

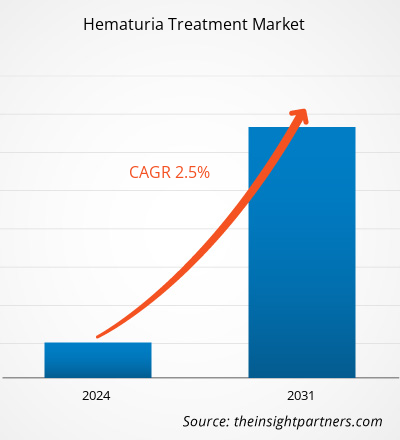

Se prevé que el tamaño del mercado de tratamiento de la hematuria alcance los 1.980 millones de dólares estadounidenses en 2031, frente a los 980 millones de dólares estadounidenses en 2023. Se espera que el mercado registre una CAGR del 2,5 % durante el período 2023-2031. Es probable que el aumento de la preferencia por terapias avanzadas siga siendo una tendencia clave en el mercado.hematuria treatment market size is projected to reach US$ 1.98 billion by 2031 from US$ 0.98 billion in 2023. The market is expected to register a CAGR of 2.5% during 2023–2031. A rise in preference for advanced therapies will likely remain a key trend in the market.

Análisis del mercado de tratamiento de la hematuria Treatment Market Analysis

Los factores clave que impulsan el crecimiento del mercado son la alta prevalencia de las indicaciones asociadas a la hematuria, la creciente conciencia sobre las opciones de tratamiento y la mejora del gasto sanitario, que son factores que impulsan el mercado del tratamiento de la hematuria. Además, los avances tecnológicos en dispositivos médicos y procedimientos de diagnóstico han dado lugar a diversas opciones para el tratamiento de las indicaciones asociadas a la hematuria, como los cálculos renales, los cálculos en la vejiga y las infecciones del tracto urinario, que probablemente ofrecerán oportunidades al mercado del tratamiento de la hematuria en los próximos años.hematuria-associated indications, increasing awareness about treatment options, and improving healthcare expenditure, which are factors propelling the hematuria treatment market. Furthermore, technological developments in medical devices and diagnostic procedures have led to various options for managing hematuria-associated indications, such as kidney stones, bladder stones, and urinary tract infections, which will likely offer opportunities to the hematuria treatment market in the coming years.

Descripción general del mercado de tratamiento de la hematuria Treatment Market Overview

La enfermedad renal crónica (ERC) es una afección común y potencialmente mortal que afecta a una mayor población en todo el mundo. Existen varios tipos de ERC, como cálculos renales, glomerulonefritis, enfermedad renal poliquística e infecciones del tracto urinario. La ERC es una de las causas fundamentales detrás de la prevalencia de la hematuria. Por ejemplo, según un estudio publicado en el Centro Nacional de Información Biotecnológica en mayo de 2019, las infecciones del tracto urinario (ITU) generalmente se observan como infecciones ambulatorias en los EE. UU., y ocurren principalmente entre mujeres del grupo de edad entre 14 y 24 años. Además, la prevalencia de ITU entre mujeres mayores de 65 años es de aproximadamente el 20% en comparación con la población general, que es de aproximadamente el 11%. Actualmente, el mercado mundial de tratamiento de la hematuria se está beneficiando significativamente de la creciente prevalencia de indicaciones asociadas.CKD) is a common and life-threatening condition that affects a larger population worldwide. There are various types of CKDs, such as kidney stones, glomerulonephritis, polycystic kidney disease, and urinary tract infections. CKD is one of the fundamental causes behind the prevalence of hematuria. For instance, according to a study published in the National Center for Biotechnology Information in May 2019, urinary tract infections (UTIs) are generally observed as UTI among women over 65 years of age is about 20% compared to the overall population, which is about 11%. Currently, the global hematuria treatment market is gaining significantly from the increasing prevalence of associated indications.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de tratamiento de la hematuria: Treatment Market: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado del tratamiento de la hematuria Treatment Market Drivers and Opportunities

Aumentar la conciencia sobre las opciones de tratamiento y mejorar el gasto en atención sanitaria

El gasto en atención sanitaria ha aumentado considerablemente debido a la creciente prevalencia de enfermedades crónicas. Los gobiernos de varias economías están invirtiendo sustancialmente en mejorar la infraestructura sanitaria. Por ejemplo, según los datos publicados en diciembre de 2020 por los Centros de Servicios de Medicare y Medicaid (CMS) de Estados Unidos, el Gasto Nacional de Salud (NHE) aumentó alrededor de un 4,6%, 11.582 dólares por persona, y representó alrededor del 17,7% del producto interno bruto (PIB). Además, los CMS proyectaron que se espera que el gasto en atención sanitaria en Estados Unidos alcance unos 6,19 billones de dólares en abril de 2020.CMS), the National Health Expenditure (NHE) increased by about 4.6%, US$ 11,582 per person, and accounted for about 17.7% of gross domestic product (GDP). In addition, CMS projected that the health care spending in the US is expected to reach about US$ 6.19 trillion in April 2020.

Además, los pacientes de las economías desarrolladas están tomando conciencia de los posibles tratamientos y de la disponibilidad de reembolso para el tratamiento de la hematuria. La hematuria es uno de los indicios iniciales de enfermedades crónicas como el cáncer de sangre, el cáncer de vejiga y el cáncer de riñón. Estas enfermedades están cubiertas por diversas pólizas de seguro médico que ayudan a facilitar el tratamiento de los pacientes y a reducir la carga financiera de la atención médica. Por lo tanto, la mejora del gasto sanitario y la concienciación entre los pacientes sobre el tratamiento están impulsando el mercado del tratamiento de la hematuria.hematuria treatment. Hematuria is among the initial indications of chronic diseases such as blood cancer, bladder cancer, and kidney cancer. These diseases are covered under various health insurance policies that help ease the treatment of the patients and reduce the financial burden of healthcare. Thus, improving healthcare expenditure and awareness among patients about the treatment is driving the hematuria treatment market.

Aumentar las oportunidades para tratamientos relacionados

El envejecimiento de la población, que tiene más probabilidades de contraer la enfermedad de hematuria debido al aumento de los cálculos renales y las infecciones del tracto urinario, es uno de los principales impulsores de la expansión del mercado. Se espera que el uso de tecnologías de tratamiento avanzadas mejore la atención al paciente. Por ejemplo, la implementación de la robótica en cirugías para tratar la urolitiasis ha ganado popularidad en los últimos años. Actualmente, el sistema quirúrgico Vinci, de Intuitive Surgical Inc., se utiliza ampliamente para realizar cirugías para tratar la urolitiasis . De manera similar, la adopción de intervenciones endourológicas para los cálculos renales ha aumentado significativamente en varios países de América del Norte, Europa y Asia. También se espera que los avances en las indicaciones asociadas respalden el mercado mundial de tratamiento de la hematuria durante el período de pronóstico.hematuria disease due to an increase in kidney stones and urinary tract infections, is one of the main drivers propelling the market's expansion. The use of advanced treatment technologies is expected to enhance patient care. For instance, the implementation of robotics in surgeries for treating urolithiasis has gained popularity in recent years. Currently, Vinci Surgical System, by Intuitive Surgical Inc., is widely used in performing surgeries to treat endourological interventions for kidney stones has increased significantly across various North American, European, and Asian countries. It is also expected that advancements in associated indications will support the global hematuria treatment market during the forecast period.

Análisis de segmentación del informe de mercado de tratamiento de la hematuria Treatment Market Report Segmentation Analysis

Los segmentos clave que contribuyeron a la derivación del análisis del mercado de tratamiento de la hematuria son el tipo de producto, el tipo de indicación y el usuario final.hematuria treatment market analysis are product type, indication type, and end user.

- Según el tratamiento, el mercado de tratamiento de la hematuria se segmenta en medicamentos, terapias y otros. El segmento de medicamentos tuvo la participación de mercado más importante en 2023.hematuria treatment market is segmented into drugs, therapies, and others. The drugs segment held the most significant market share in 2023.

- Según las indicaciones, el mercado de tratamiento de la hematuria se segmenta por infecciones del tracto urinario, cálculos renales, uretritis, cáncer de sangre, cálculos de vejiga, cáncer de próstata, cistitis, traumatismos, ejercicio vigoroso, enfermedad renal poliquística, endometriosis y menstruación. El segmento de infecciones del tracto urinario tuvo la mayor participación de mercado en 2023.hematuria treatment market is segmented by urinary tract infections, kidney stones, urethritis, blood cancer, bladder stones, prostate cancer, cystitis, trauma, vigorous exercise, polycystic kidney disease, endometriosis, menstruation. The urinary tract infections segment held the largest market share in 2023.

- Según el usuario final, el mercado de tratamiento de la hematuria está segmentado por hospitales, clínicas y centros de cirugía ambulatoria, entre otros. El segmento de hospitales tuvo la mayor participación de mercado en 2023.hematuria treatment market is segmented by hospitals, clinics, and ASCs, among others. The hospital's segment held the largest market share in 2023.

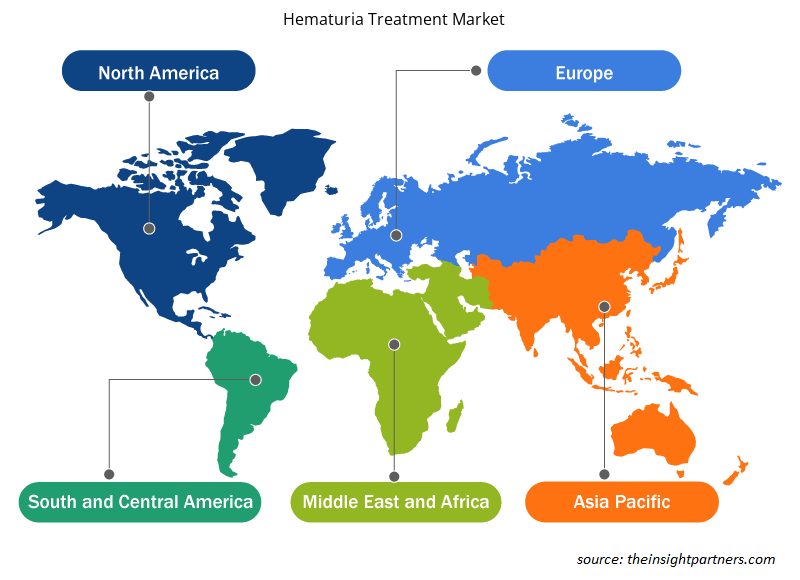

Análisis de la cuota de mercado del tratamiento de la hematuria por geografía Treatment Market Share Analysis by Geography

El alcance geográfico del informe del mercado de tratamiento de la hematuria se divide principalmente en cinco regiones: América del Norte, Asia Pacífico, Europa, Medio Oriente y África, y América del Sur y Central.

En América del Norte, Estados Unidos es el mayor mercado de tratamiento de la hematuria. El crecimiento de este mercado se debe principalmente a la creciente prevalencia de los trastornos renales crónicos (ERC) y al creciente número de lanzamientos de productos por parte de actores clave. Por ejemplo, en 2016, los Centros para el Control y la Prevención de Enfermedades (CDC) afirmaron que se estima que 0,7 millones de personas recibieron tratamiento por enfermedad renal en etapa terminal (ESRD) en los EE. UU. La prevalencia de ESRD se duplicó con creces entre 1990 y 2016. Además, también se espera que el aumento de la incidencia de la hematuria entre los adultos, el aumento de la concienciación y las amplias actividades de investigación y desarrollo impulsen la prevalencia de los tratamientos de la hematuria, lo que eventualmente ofrecerá una oportunidad lucrativa para el crecimiento del mercado.

Perspectivas regionales del mercado de tratamiento de la hematuria

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de tratamiento de la hematuria durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de tratamiento de la hematuria en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de tratamiento de la hematuria

Alcance del informe de mercado sobre el tratamiento de la hematuria

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2023 | 0,98 mil millones de dólares estadounidenses |

| Tamaño del mercado en 2031 | 1.980 millones de dólares estadounidenses |

| CAGR global (2023 - 2031) | 2,5% |

| Datos históricos | 2021-2022 |

| Período de pronóstico | 2024-2031 |

| Segmentos cubiertos |

Por tratamiento

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de tratamiento de la hematuria: comprensión de su impacto en la dinámica empresarial

El mercado de tratamiento de la hematuria está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado del tratamiento de la hematuria son:

- AstraZeneca

- Compañía farmacéutica Merck & Co., Inc.

- Compañía Bristol-Myers Squibb

- Compañía farmacéutica Merck & Co., Inc.

- F. HOFFMANN-LA ROCHE LTD.

- Compañía: GlaxoSmithKline plc.

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de tratamiento de la hematuria

Noticias y desarrollos recientes del mercado de tratamiento de la hematuria

El mercado de tratamiento de la hematuria se evalúa mediante la recopilación de datos cualitativos y cuantitativos posteriores a la investigación primaria y secundaria, que incluye publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se enumeran algunos de los avances en el mercado de tratamiento de la hematuria:

- Farxiga (dapagliflozina) de AstraZeneca ha sido aprobado en los EE. UU. para reducir el riesgo de muerte cardiovascular (CV), hospitalización por insuficiencia cardíaca (ICC) y visitas urgentes por insuficiencia cardíaca (IC) en adultos con IC. La aprobación por parte de la Administración de Alimentos y Medicamentos (FDA) se basó en los resultados positivos del ensayo de fase III DELIVER.1 Farxiga fue aprobado previamente en los EE. UU. para adultos con IC con fracción de eyección reducida (ICFEr). (Fuente: sitio web de la empresa AstraZeneca, mayo de 2023)

Informe sobre el mercado de tratamiento de la hematuria: cobertura y resultados

El informe “Tamaño y pronóstico del mercado de tratamiento de la hematuria (2021-2031)” proporciona un análisis detallado del mercado que cubre las siguientes áreas:

- Tamaño del mercado de tratamiento de la hematuria y pronóstico a nivel mundial, regional y nacional para todos los segmentos clave del mercado cubiertos bajo el alcance

- Tendencias del mercado de tratamiento de la hematuria, así como dinámica del mercado, como impulsores, restricciones y oportunidades clave

- Análisis detallado de las cinco fuerzas de Porter y PEST y FODA

- Análisis del mercado de tratamiento de la hematuria que cubre las tendencias clave del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia que abarca la concentración del mercado, el análisis de mapas de calor, los actores destacados y los desarrollos recientes en el mercado del tratamiento de la hematuria

- Perfiles detallados de empresas

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias