Rapporto sul mercato Trattamento dell’ematuria 2031 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Rapporto di analisi sulle dimensioni e le previsioni del mercato del trattamento dell'ematuria (2021-2031), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per trattamento (farmaci, terapie, altri); indicazione (infezioni del tratto urinario, calcoli renali, uretrite, tumore del sangue, calcoli alla vescica, tumore alla prostata, cistite, trauma, esercizio fisico intenso, malattia renale policistica, endometriosi, mestruazioni); tipo (ematuria macroscopica, ematuria microscopica, ematuria idiopatica, ematuria del jogger), utente finale (ospedali, cliniche e ASC, altri) e area geografica.

- Stato : Dati rilasciati

- Codice del report : TIPRE00004601

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : February 15, 2025

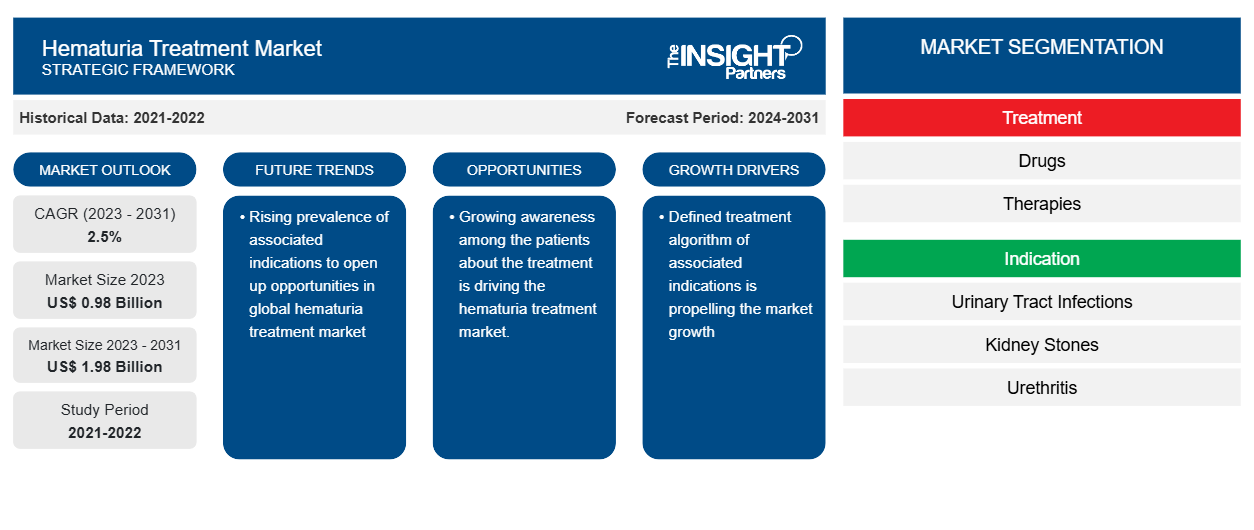

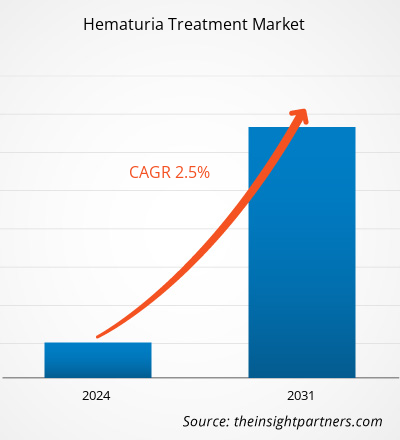

Si prevede che la dimensione del mercato del trattamento dell'ematuria raggiungerà 1,98 miliardi di dollari entro il 2031 da 0,98 miliardi di dollari nel 2023. Si prevede che il mercato registrerà un CAGR del 2,5% nel periodo 2023-2031. Un aumento della preferenza per le terapie avanzate rimarrà probabilmente una tendenza chiave nel mercato.hematuria treatment market size is projected to reach US$ 1.98 billion by 2031 from US$ 0.98 billion in 2023. The market is expected to register a CAGR of 2.5% during 2023–2031. A rise in preference for advanced therapies will likely remain a key trend in the market.

Analisi di mercato del trattamento dell'ematuria Treatment Market Analysis

I fattori chiave che stanno guidando la crescita del mercato sono l'elevata prevalenza di indicazioni associate all'ematuria, la crescente consapevolezza sulle opzioni di trattamento e il miglioramento della spesa sanitaria, che sono fattori che spingono il mercato del trattamento dell'ematuria. Inoltre, gli sviluppi tecnologici nei dispositivi medici e nelle procedure diagnostiche hanno portato a varie opzioni per la gestione delle indicazioni associate all'ematuria, come calcoli renali, calcoli alla vescica e infezioni del tratto urinario, che probabilmente offriranno opportunità al mercato del trattamento dell'ematuria nei prossimi anni.hematuria-associated indications, increasing awareness about treatment options, and improving healthcare expenditure, which are factors propelling the hematuria treatment market. Furthermore, technological developments in medical devices and diagnostic procedures have led to various options for managing hematuria-associated indications, such as kidney stones, bladder stones, and urinary tract infections, which will likely offer opportunities to the hematuria treatment market in the coming years.

Panoramica del mercato del trattamento dell'ematuria

La malattia renale cronica (CKD) è una condizione comune e pericolosa per la vita che colpisce una popolazione più ampia in tutto il mondo. Esistono vari tipi di CKD, come calcoli renali, glomerulonefrite, malattia renale policistica e infezioni del tratto urinario. La CKD è una delle cause fondamentali alla base della prevalenza dell'ematuria. Ad esempio, secondo uno studio pubblicato nel National Center for Biotechnology Information a maggio 2019, le infezioni del tratto urinario (UTI) sono generalmente osservate come infezioni ambulatoriali negli Stati Uniti, che si verificano principalmente tra le donne nella fascia di età compresa tra 14 e 24 anni. Inoltre, la prevalenza di UTI tra le donne di età superiore ai 65 anni è di circa il 20% rispetto alla popolazione complessiva, che è di circa l'11%. Attualmente, il mercato globale del trattamento dell'ematuria sta guadagnando significativamente dalla crescente prevalenza di indicazioni associate.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato del trattamento dell'ematuria: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato del trattamento dell'ematuria

Aumentare la consapevolezza sulle opzioni di trattamento e migliorare la spesa sanitaria

La spesa sanitaria è aumentata considerevolmente a causa della crescente prevalenza di indicazioni croniche. I governi di varie economie stanno investendo in modo sostanziale nel miglioramento dell'infrastruttura sanitaria. Ad esempio, secondo i dati pubblicati a dicembre 2020 dai Centers for Medicare & Medicaid Services (CMS) degli Stati Uniti, la spesa sanitaria nazionale (NHE) è aumentata di circa il 4,6%, 11.582 $ USA a persona, e ha rappresentato circa il 17,7% del prodotto interno lordo (PIL). Inoltre, i CMS hanno previsto che la spesa sanitaria negli Stati Uniti dovrebbe raggiungere circa 6,19 trilioni di $ USA ad aprile 2020.CMS), the National Health Expenditure (NHE) increased by about 4.6%, US$ 11,582 per person, and accounted for about 17.7% of gross domestic product (GDP). In addition, CMS projected that the health care spending in the US is expected to reach about US$ 6.19 trillion in April 2020.

Inoltre, i pazienti nelle economie sviluppate stanno diventando consapevoli dei possibili trattamenti e della disponibilità di rimborso per il trattamento dell'ematuria. L'ematuria è tra le prime indicazioni di malattie croniche come il cancro del sangue, il cancro della vescica e il cancro del rene. Queste malattie sono coperte da varie polizze assicurative sanitarie che aiutano ad alleviare il trattamento dei pazienti e a ridurre l'onere finanziario dell'assistenza sanitaria. Pertanto, il miglioramento della spesa sanitaria e la consapevolezza tra i pazienti sul trattamento stanno guidando il mercato del trattamento dell'ematuria.hematuria treatment. Hematuria is among the initial indications of chronic diseases such as blood cancer, bladder cancer, and kidney cancer. These diseases are covered under various health insurance policies that help ease the treatment of the patients and reduce the financial burden of healthcare. Thus, improving healthcare expenditure and awareness among patients about the treatment is driving the hematuria treatment market.

Aumentare le opportunità per trattamenti correlati

L'invecchiamento della popolazione, che ha maggiori probabilità di contrarre la malattia dell'ematuria a causa di un aumento di calcoli renali e infezioni del tratto urinario, è uno dei principali fattori trainanti che promuovono l'espansione del mercato. L'uso di tecnologie di trattamento avanzate dovrebbe migliorare l'assistenza ai pazienti. Ad esempio, l'implementazione della robotica negli interventi chirurgici per il trattamento dell'urolitiasi ha guadagnato popolarità negli ultimi anni. Attualmente, Vinci Surgical System, di Intuitive Surgical Inc., è ampiamente utilizzato nell'esecuzione di interventi chirurgici per il trattamento dell'urolitiasi . Allo stesso modo, l'adozione di interventi endourologici per i calcoli renali è aumentata in modo significativo in vari paesi del Nord America, Europa e Asia. Si prevede inoltre che i progressi nelle indicazioni associate supporteranno il mercato globale del trattamento dell'ematuria durante il periodo di previsione.hematuria disease due to an increase in kidney stones and urinary tract infections, is one of the main drivers propelling the market's expansion. The use of advanced treatment technologies is expected to enhance patient care. For instance, the implementation of robotics in surgeries for treating urolithiasis has gained popularity in recent years. Currently, Vinci Surgical System, by Intuitive Surgical Inc., is widely used in performing surgeries to treat endourological interventions for kidney stones has increased significantly across various North American, European, and Asian countries. It is also expected that advancements in associated indications will support the global hematuria treatment market during the forecast period.

Analisi della segmentazione del rapporto di mercato sul trattamento dell'ematuria Treatment Market Report Segmentation Analysis

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato del trattamento dell'ematuria sono il tipo di prodotto, il tipo di indicazione e l'utente finale.hematuria treatment market analysis are product type, indication type, and end user.

- In base al trattamento, il mercato del trattamento dell'ematuria è segmentato in farmaci, terapie e altri. Il segmento dei farmaci ha detenuto la quota di mercato più significativa nel 2023.hematuria treatment market is segmented into drugs, therapies, and others. The drugs segment held the most significant market share in 2023.

- In base all'indicazione, il mercato del trattamento dell'ematuria è segmentato in base a infezioni del tratto urinario, calcoli renali, uretrite, tumore del sangue, calcoli alla vescica, tumore alla prostata, cistite, traumi, esercizio fisico intenso, malattia renale policistica, endometriosi, mestruazioni. Il segmento delle infezioni del tratto urinario ha detenuto la quota di mercato maggiore nel 2023.hematuria treatment market is segmented by urinary tract infections, kidney stones, urethritis, blood cancer, bladder stones, prostate cancer, cystitis, trauma, vigorous exercise, polycystic kidney disease, endometriosis, menstruation. The urinary tract infections segment held the largest market share in 2023.

- In base all'utente finale, il mercato del trattamento dell'ematuria è segmentato da ospedali, cliniche e ASC, tra gli altri. Il segmento dell'ospedale ha detenuto la quota di mercato più grande nel 2023.hematuria treatment market is segmented by hospitals, clinics, and ASCs, among others. The hospital's segment held the largest market share in 2023.

Analisi della quota di mercato del trattamento dell'ematuria per area geografica Treatment Market Share Analysis by Geography

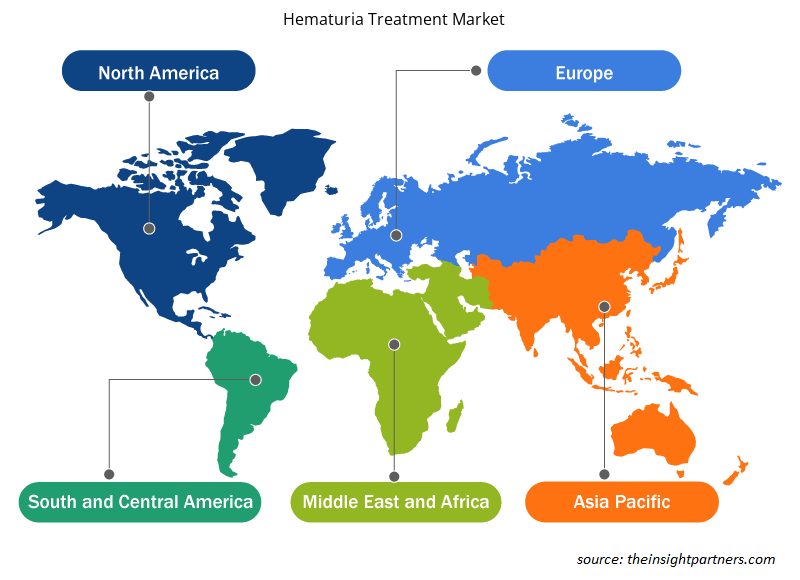

L'ambito geografico del rapporto di mercato sul trattamento dell'ematuria è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa, e Sud e Centro America.

In Nord America, gli Stati Uniti sono il più grande mercato per il trattamento dell'ematuria. La crescita di questo mercato è guidata principalmente dalla crescente prevalenza di malattie renali croniche (CKD) e dal crescente numero di lanci di prodotti da parte di attori chiave. Ad esempio, nel 2016, i Centers for Disease Control and Prevention (CDC) hanno dichiarato che circa 0,7 milioni di persone sono state curate per malattia renale allo stadio terminale (ESRD) negli Stati Uniti. La prevalenza di ESRD è più che raddoppiata tra il 1990 e il 2016. Inoltre, si prevede che anche l'aumento dell'incidenza di ematuria tra gli adulti, l'aumento della consapevolezza e le vaste attività di ricerca e sviluppo guideranno la prevalenza dei trattamenti per l'ematuria, che alla fine offriranno un'opportunità redditizia per la crescita del mercato.

Approfondimenti regionali sul mercato del trattamento dell'ematuria

Le tendenze regionali e i fattori che influenzano il mercato del trattamento dell'ematuria durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato del trattamento dell'ematuria in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato del trattamento dell'ematuria

Ambito del rapporto di mercato sul trattamento dell'ematuria

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 0,98 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 1,98 miliardi di dollari USA |

| CAGR globale (2023-2031) | 2,5% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per trattamento

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato del trattamento dell'ematuria: comprendere il suo impatto sulle dinamiche aziendali

Il mercato del trattamento dell'ematuria sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato del trattamento dell'ematuria sono:

- AstraZeneca

- Merck & Co., Inc.

- Società Bristol-Myers Squibb

- Merck & Co., Inc.

- F. HOFFMANN-LA ROCHE LTD.

- Società anonima GlaxoSmithKline.

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato del trattamento dell'ematuria

Notizie di mercato e sviluppi recenti sul trattamento dell'ematuria

Il mercato del trattamento dell'ematuria viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi nel mercato del trattamento dell'ematuria:

- Farxiga (dapagliflozin) di AstraZeneca è stato approvato negli Stati Uniti per ridurre il rischio di morte cardiovascolare (CV), ospedalizzazione per insufficienza cardiaca (CHF) e visite urgenti per insufficienza cardiaca (HF) negli adulti con HF. L'approvazione da parte della Food and Drug Administration (FDA) si è basata sui risultati positivi dello studio di fase III DELIVER.1 Farxiga era stato precedentemente approvato negli Stati Uniti per gli adulti con HF con frazione di eiezione ridotta (HFrEF). (Fonte: AstraZeneca, sito Web aziendale, maggio 2023)

Copertura e risultati del rapporto di mercato sul trattamento dell'ematuria

Il rapporto "Dimensioni e previsioni del mercato del trattamento dell'ematuria (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato del trattamento dell'ematuria a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato del trattamento dell'ematuria e dinamiche di mercato come fattori trainanti, limitazioni e opportunità chiave

- Analisi dettagliata delle cinque forze PEST/Porter e SWOT

- Analisi di mercato del trattamento dell'ematuria che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato.

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti nel mercato del trattamento dell'ematuria

- Profili aziendali dettagliati

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative