Batería secundaria Descripción general del mercado, crecimiento, tendencias, análisis, informe de investigación (2024-2031)

Tamaño y pronóstico del mercado de baterías secundarias (2021-2031), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tecnología (batería secundaria de plomo-ácido, batería secundaria de iones de litio, otras tecnologías); aplicación (automotriz, industrial, baterías portátiles, dispositivos médicos, montacargas, otras aplicaciones) y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00014996

- Categoría : Electrónica y semiconductores

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : February 15, 2025

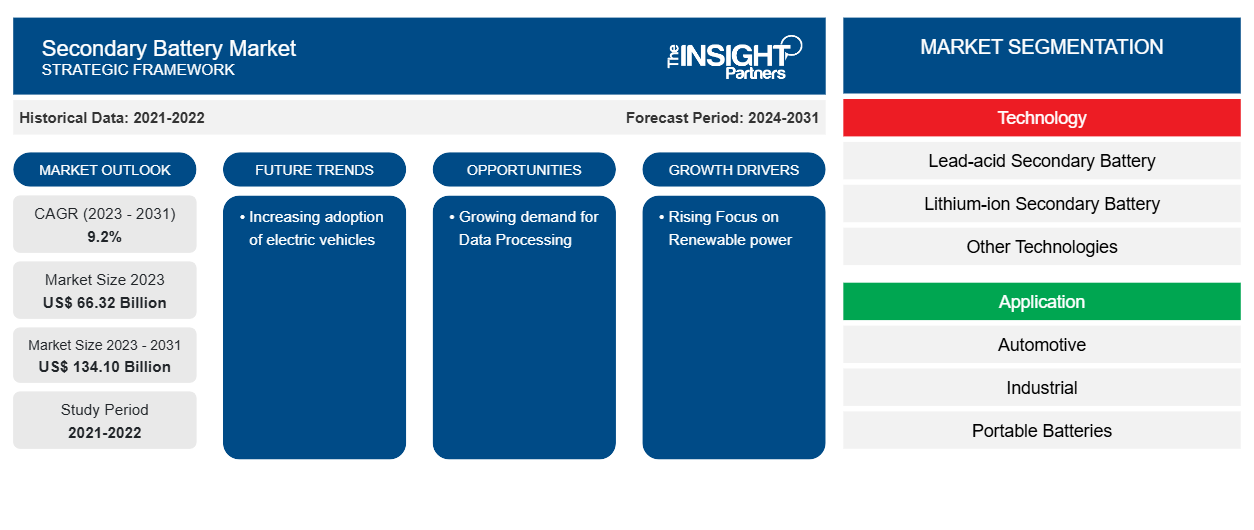

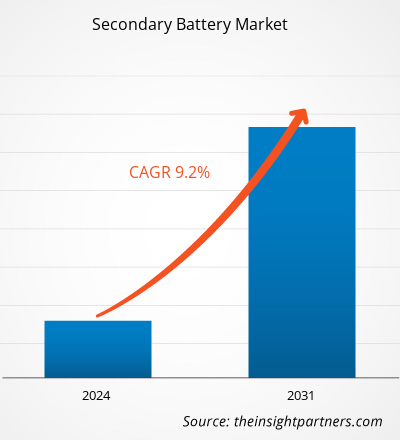

Se espera que el tamaño del mercado mundial de baterías secundarias crezca de 66.320 millones de dólares en 2023 a 134.100 millones de dólares en 2031; se anticipa que se expandirá a una CAGR del 9,2% entre 2024 y 2031. Es probable que la creciente adopción de vehículos eléctricos siga siendo una tendencia clave del mercado de baterías secundarias.

Análisis del mercado de baterías secundarias

El crecimiento del mercado global se puede atribuir a factores que incluyen los avances tecnológicos, un aumento en las industrias de usuarios finales y el apoyo a nivel de políticas gubernamentales para promover la infraestructura de almacenamiento de energía.

Descripción general del mercado de baterías secundarias

Una batería recargable, una batería de almacenamiento o una celda secundaria (oficialmente conocida como acumulador de energía) es un tipo de batería eléctrica que se puede cargar, descargar en una carga y recargar varias veces, a diferencia de una batería desechable o principal, que se entrega completamente cargada y se desecha después de su uso. Consiste en una o más celdas electroquímicas. El término "acumulador" se refiere a algo que reúne y almacena energía a través de un proceso electroquímico reversible. Las baterías recargables vienen en una variedad de formas y capacidades, desde pilas de botón hasta sistemas de megavatios utilizados para estabilizar una red de distribución eléctrica. Se utilizan varios materiales de electrodos y electrolitos, incluidos plomo-ácido, zinc-aire, níquel-cadmio (NiCd), níquel-hidruro metálico (NiMH), ion de litio (Li-ion), fosfato de hierro y litio (LiFePO4) y polímero de ion de litio.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de baterías secundarias: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de baterías secundarias

El creciente interés por las energías renovables favorece al mercado

La generación de energía renovable está ganando popularidad en todo el mundo, con Alemania y Francia a la cabeza en la implementación de tecnología de energía renovable. Sin embargo, estos países siguen dependiendo de las importaciones netas de electricidad. Las naciones emergentes, por otro lado, están adoptando energía renovable al mismo tiempo que se convierten en importadores netos de energía debido al aumento del consumo de energía y a la infraestructura de red insuficiente. Esta circunstancia resalta la necesidad vital de tecnologías de almacenamiento de energía, en particular baterías secundarias , para proporcionar un suministro constante de electricidad. Como consecuencia, se proyecta que el mercado mundial de baterías secundarias se expandirá significativamente en los próximos años.

Creciente demanda de procesamiento de datos

La creciente demanda de procesamiento de datos está impulsando la demanda del mercado de baterías secundarias. Esto se debe a varios factores, incluidos los avances tecnológicos, la creciente demanda de dispositivos electrónicos portátiles y el cambio hacia fuentes de energía renovables. La demanda de baterías secundarias está impulsada por los avances tecnológicos y la creciente demanda de dispositivos electrónicos portátiles como teléfonos inteligentes, tabletas y dispositivos portátiles. Estos dispositivos requieren fuentes de energía confiables y eficientes, y las baterías secundarias proporcionan el almacenamiento de energía necesario.fuelling the demand for the secondary battery market. This is due to several factors, including technological advancements, increasing demand for portable electronics, and the shift towards renewable energy sources. The demand for secondary batteries is driven by technological advancements and the increasing demand for portable electronics such as smartphones, tablets, and wearable devices. These devices require reliable and efficient power sources, and secondary batteries provide the necessary energy storage.

Análisis de segmentación del informe del mercado de baterías secundarias

Segmentos clave que contribuyeron a la derivación de la tecnología y aplicación del análisis del mercado de baterías secundarias.

- Según la tecnología, el mercado se divide en baterías secundarias de plomo-ácido, baterías secundarias de iones de litio y otras tecnologías. El segmento de baterías secundarias de plomo-ácido tuvo una mayor participación de mercado en 2023.

- Según la aplicación, el mercado se divide en aplicaciones automotrices, industriales, baterías portátiles , dispositivos médicos, carretillas elevadoras y otras. El segmento industrial tuvo una mayor participación de mercado en 2023.

Análisis de la cuota de mercado de baterías secundarias por geografía

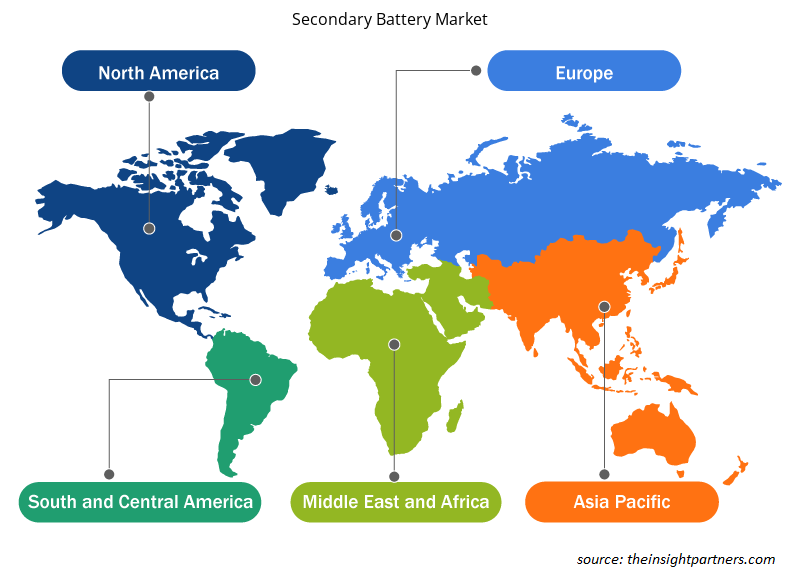

El alcance geográfico del informe del mercado de baterías secundarias se divide principalmente en cinco regiones: América del Norte, Asia Pacífico, Europa, Oriente Medio y África, y América del Sur/América del Sur y Central. América del Norte dominó el mercado de baterías secundarias en 2023. El mercado de baterías en la región de América del Norte, que incluye Estados Unidos, Canadá y México, está experimentando un crecimiento significativo debido a factores como un fuerte enfoque en el desarrollo sostenible y una mayor conciencia de los efectos negativos de los automóviles tradicionales. Los crecientes niveles de contaminación global y la disminución de la disponibilidad de combustibles fósiles han creado una demanda de soluciones de transporte respetuosas con el medio ambiente. En respuesta a estas preocupaciones, los fabricantes de automóviles están adoptando tecnologías avanzadas e incorporando baterías de iones de litio en vehículos híbridos y eléctricos (VE) para abordar la apremiante necesidad de preservación del medio ambiente.

Perspectivas regionales del mercado de baterías secundarias

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de baterías secundarias durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de baterías secundarias en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga los datos regionales específicos para el mercado de baterías secundarias

Alcance del informe sobre el mercado de baterías secundarias

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2023 | US$ 66.32 mil millones |

| Tamaño del mercado en 2031 | US$ 134,10 mil millones |

| CAGR global (2023 - 2031) | 9,2% |

| Datos históricos | 2021-2022 |

| Período de pronóstico | 2024-2031 |

| Segmentos cubiertos |

Por tecnología

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado: comprensión de su impacto en la dinámica empresarial

El mercado de baterías secundarias está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de baterías secundarias son:

- Tecnología Amperex Limitada

- Compañía BYD Ltd.

- Duracell Inc

- Sistemas energéticos

- Tecnología contemporánea Amperex Co. Limited

- Corporación Panasonic

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de baterías secundarias

Noticias y desarrollos recientes del mercado de baterías secundarias

El mercado de baterías secundarias se evalúa mediante la recopilación de datos cualitativos y cuantitativos posteriores a la investigación primaria y secundaria, que incluye publicaciones corporativas importantes, datos de asociaciones y bases de datos. A continuación, se incluye una lista de los avances del mercado:

- En abril de 2024, BYD, un fabricante de automóviles chino, tiene previsto presentar su paquete de baterías "blade" de segunda generación en agosto de 2024. Se espera que esta nueva tecnología de baterías tenga suficiente autonomía para conducir un coche eléctrico de Sídney a Melbourne con una sola carga. El paquete de baterías blade de segunda generación se basará en la tecnología de baterías de fosfato de iones de litio (LFP) patentada por BYD. Cabe señalar que esta tecnología superará la introducción de baterías de estado sólido con una autonomía similar declarada por Toyota, que actualmente está prevista para 2026 como muy pronto.

(Fuente: BYD, Nota de prensa, 2024)

Informe sobre el mercado de baterías secundarias: cobertura y resultados

El informe "Tamaño y pronóstico del mercado de baterías secundarias (2021-2031)" proporciona un análisis detallado del mercado que cubre las siguientes áreas:

- Tamaño del mercado y pronóstico a nivel global, regional y nacional para todos los segmentos clave del mercado cubiertos bajo el alcance

- Dinámica del mercado, como impulsores, restricciones y oportunidades clave

- Principales tendencias futuras

- Análisis detallado de las cinco fuerzas de Porter y PEST y FODA

- Análisis del mercado global y regional que cubre las tendencias clave del mercado, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia que abarca la concentración del mercado, el análisis de mapas de calor, los actores destacados y los desarrollos recientes

- Perfiles detallados de empresas

Naveen es un experimentado profesional en investigación de mercados y consultoría con más de 9 años de experiencia en proyectos personalizados, sindicados y de consultoría. Actualmente se desempeña como Vicepresidente Asociado, donde ha gestionado con éxito a las partes interesadas en toda la cadena de valor del proyecto y ha redactado más de 100 informes de investigación y más de 30 proyectos de consultoría. Su trabajo abarca proyectos industriales y gubernamentales, contribuyendo significativamente al éxito de los clientes y a la toma de decisiones basada en datos.

Naveen es licenciado en Ingeniería Electrónica y Comunicaciones por la VTU (Karnataka) y tiene un MBA en Marketing y Operaciones por la Universidad de Manipal. Ha sido miembro activo del IEEE durante 9 años, participando en conferencias, simposios técnicos y realizando voluntariado tanto a nivel de sección como regional. Antes de su puesto actual, trabajó como Consultor Estratégico Asociado en IndustryARC y como Consultor de Servidores Industriales en Hewlett Packard (HP Global).

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias