Stratégies de marché des infrastructures aéroportuaires, principaux acteurs, opportunités de croissance, analyse et prévisions d’ici 2030

Données historiques : 2020-2021 | Année de référence : 2022 | Période de prévision : 2022-2030Taille et prévisions du marché des infrastructures aéroportuaires (2020-2030), parts mondiales et régionales, tendances et opportunités de croissance. Rapport d'analyse : par type d'aéroport (aéroport commercial, aéroport militaire, aéroport d'aviation générale) ; type d'infrastructure (terminal, tour de contrôle, voie de circulation et piste, hangar, autres) ; et géographie

- Statut : Publié

- Code du rapport : TIPRE00023774

- Catégorie : Aérospatiale et défense

- Nombre de pages : 152

- Formats de rapport disponibles :

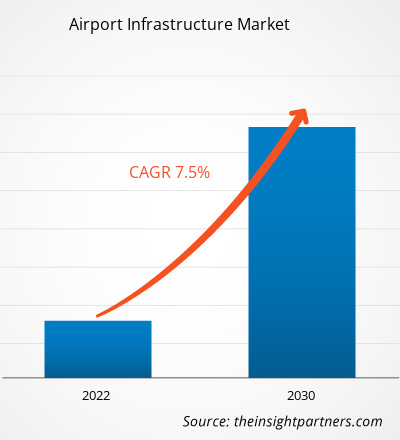

Français La taille du marché des infrastructures aéroportuaires devrait atteindre 139 144,01 millions USD d'ici 2030, contre 77 853,08 millions USD en 2022. Le marché devrait enregistrer un TCAC de 7,5 % en 2022-2030. Les gouvernements de différents pays ont pris des initiatives pour construire de nouveaux aéroports afin de répondre au nombre croissant de flottes d'avions et de passagers. Par exemple, en 2022, le gouvernement indien a annoncé son intention de construire 220 aéroports commerciaux d'ici fin 2025. De plus, en 2018, l'Administration de l'aviation civile de Chine (CAAC) a annoncé son intention de construire 216 nouveaux aéroports d'ici fin 2035, ce qui portera le nombre total d'aéroports à 450 d'ici 2035 (234 aéroports actuellement en 2023). De tels développements ont stimulé la croissance du marché des infrastructures aéroportuaires pour le segment des aéroports commerciaux dans le monde entier.

Analyse du marché des infrastructures aéroportuaires

La demande d’aéroports militaires et de nouvelles bases aériennes augmente en raison des tensions mondiales croissantes entre les pays de différentes régions. De nombreux pays ont accru leurs investissements militaires respectifs pour l’acquisition de technologies liées aux missions et la construction de nouvelles bases sur leurs sites cibles respectifs. De plus, l’extension des aéroports militaires existants pour répondre aux besoins d’un plus grand nombre d’avions militaires a stimulé la croissance du marché des infrastructures aéroportuaires pour le segment des aéroports militaires dans le monde entier. Par exemple, en septembre 2021, le gouvernement chinois a annoncé que 30 nouveaux aéroports avaient été construits dans les provinces du Tibet et du Xinjiang pour renforcer les infrastructures aéroportuaires civiles et militaires dans les régions. En outre, les plans annoncés précédemment par l’armée indienne pour la construction de 59 aéroports sont également en cours. À la fin novembre 2023, l’Inde comptait environ 39 aéroports militaires pour leurs opérations respectives. De tels développements ont stimulé la croissance du marché des infrastructures aéroportuaires pour le segment des aéroports militaires .

Aperçu du marché des infrastructures aéroportuaires

Français L'aéroport d'aviation générale accueille essentiellement des jets d'affaires, des avions à moteurs à pistons, des hélicoptères et des avions d'entraînement pour des opérations telles que le décollage, l'atterrissage, les services MRO, les contrôles opérationnels et les opérations d'affrètement privé. Plusieurs pays, comme les États-Unis, la Chine, la Russie et le Royaume-Uni, disposent déjà d'aéroports d'aviation générale en plus grand nombre, ce qui stimule la croissance du marché des infrastructures aéroportuaires pour le segment des aéroports d'aviation générale grâce à des projets d'expansion d'aéroports dans leurs régions respectives. Par exemple, en septembre 2023, l'un des principaux aéroports d'aviation générale (l'aéroport de San Carlos) dans la région de la baie de San Francisco, aux États-Unis, a annoncé des investissements pour la modernisation de l'aéroport avec 50 000 pieds carrés de nouvel espace de hangar et 22 000 pieds carrés supplémentaires d'espaces communs, de bureaux et de salles de réunion. De plus, en 2020, l'aéroport international Indira Gandhi de Delhi a également inauguré un nouveau terminal pour les opérations de jets d'affaires. De tels développements ont alimenté la croissance du marché des infrastructures aéroportuaires pour le segment des aéroports d'aviation générale.

Personnalisez ce rapport en fonction de vos besoins

Vous bénéficierez d'une personnalisation gratuite de n'importe quel rapport, y compris de certaines parties de ce rapport, d'une analyse au niveau des pays, d'un pack de données Excel, ainsi que de superbes offres et réductions pour les start-ups et les universités.

Marché des infrastructures aéroportuaires : perspectives stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Moteurs et opportunités du marché des infrastructures aéroportuaires

Construction croissante de nouveaux terminaux d'aéroport, pistes, voies de circulation et hangars

L'augmentation de la flotte mondiale d'avions commerciaux est l'un des principaux facteurs générant la demande de nouveaux vols, terminaux, pistes et hangars dans différents aéroports pour répondre au trafic croissant de passagers dans le monde entier. Cela stimule également les investissements des autorités aéroportuaires pour moderniser leurs locaux respectifs afin de répondre à un plus grand nombre d'avions, ce qui améliore également l'efficacité opérationnelle globale de l'aéroport. Cela est également soutenu par l'introduction de compagnies aériennes à bas prix qui ont soutenu le trafic aérien de passagers dans le monde entier. En mars 2023, le conseil municipal canadien de Kelowna a annoncé l'approbation d'un financement de 90 millions de dollars américains pour le projet d'agrandissement du terminal de l'aéroport de Kelowna. Plusieurs autorités gouvernementales de différents pays ont également prévu de construire de nouveaux aéroports dans leurs pays respectifs pour améliorer le flux du commerce international de fret et l'industrie du transport aérien. Par exemple, aux États-Unis, six nouveaux aéroports sont actuellement en construction. En 2022, le gouvernement indien a annoncé son intention de construire 220 aéroports d’ici fin 2025. De plus, en 2018, l’Administration de l’aviation civile de Chine (CAAC) a annoncé son intention de construire 216 nouveaux aéroports d’ici fin 2035 et devrait porter le nombre total d’aéroports à 450 d’ici 2035 (234 aéroports actuellement en 2023). Ainsi, la construction de nouveaux terminaux aéroportuaires, de pistes, de voies de circulation et de hangars contribue à la croissance du marché des infrastructures aéroportuaires à travers le monde.

Initiatives croissantes visant à moderniser les bases aériennes militaires pour l'utilisation de l'aviation commerciale

Les gouvernements de plusieurs pays ont pris des initiatives pour autoriser leurs aéroports militaires respectifs à accueillir des avions commerciaux et à effectuer des opérations d'atterrissage et de décollage, afin de faciliter la gestion du trafic croissant de passagers dans différentes régions jusqu'à ce que de nouveaux aéroports commerciaux soient opérationnels. Quelques autres initiatives incluent la transformation de certains aéroports militaires en aéroports hybrides. Par exemple, plusieurs aéroports militaires aux États-Unis, tels que AF Plant 42, Palmdale, CA ; Barter Island LRRS, Barter Island ; AK Charleston AFB, Charleston, SC ; Dover AFB, Dover, DE ; Eglin AFB, Valparaiso, FL ; Grissom AFB, Peru, IN ; et Kelly/Lackland AFB, TX, autorisent l'utilisation conjointe de ces aéroports militaires existants lorsqu'un sponsor civil souhaite utiliser l'aérodrome militaire pour ses opérations d'atterrissage ou de décollage. Ainsi, les initiatives croissantes visant à moderniser les bases aériennes militaires pour l'utilisation de l'aviation commerciale devraient alimenter la croissance du marché des infrastructures aéroportuaires au cours de la période de prévision.

Analyse de segmentation du rapport sur le marché des infrastructures aéroportuaires

Les segments clés qui ont contribué à l’élaboration de l’analyse du marché des infrastructures aéroportuaires sont le type d’aéroport, le type d’infrastructure et la géographie.

- En fonction du type d'aéroport, le marché des infrastructures aéroportuaires a été segmenté en aéroport commercial, aéroport militaire et aéroport d'aviation générale. Le segment des aéroports commerciaux détenait une part de marché plus importante en 2022.

- Par type d'infrastructure, le marché des infrastructures aéroportuaires a été segmenté en terminal, tour de contrôle, voie de circulation et piste, hangar et autres. Le segment des terminaux détenait la plus grande part du marché en 2022.

Analyse des parts de marché des infrastructures aéroportuaires par zone géographique

La portée géographique du rapport sur le marché des infrastructures aéroportuaires est principalement divisée en cinq régions : Amérique du Nord, Europe, Asie-Pacifique, Moyen-Orient et Afrique et Amérique du Sud.

L'Asie-Pacifique a dominé le marché des infrastructures aéroportuaires en 2022 et devrait conserver sa position dominante au cours de la période de prévision. En outre, la région Asie-Pacifique devrait enregistrer le TCAC le plus élevé sur le marché des infrastructures aéroportuaires au cours de la période 2022-2030. Cela est dû à une augmentation des investissements dans l'expansion et la modernisation des installations aéroportuaires de la région. En outre, l'Asie-Pacifique se présente comme une plaque tournante dynamique pour le développement des infrastructures aéroportuaires, tirée par la forte croissance économique de la région et l'essor du transport aérien. Des pays comme la Chine et l'Inde connaissent des investissements massifs dans la construction de nouveaux aéroports et des projets d'agrandissement. Ces initiatives visent à suivre le rythme de l'augmentation du nombre de passagers et à promouvoir la connectivité régionale.

Aperçu régional du marché des infrastructures aéroportuaires

Les tendances et facteurs régionaux influençant le marché des infrastructures aéroportuaires tout au long de la période de prévision ont été expliqués en détail par les analystes d'Insight Partners. Cette section traite également des segments et de la géographie du marché des infrastructures aéroportuaires en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et en Amérique centrale.

- Obtenez les données régionales spécifiques au marché des infrastructures aéroportuaires

Portée du rapport sur le marché des infrastructures aéroportuaires

| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2022 | 77 853,08 millions de dollars américains |

| Taille du marché d'ici 2030 | 139 144,01 millions USD |

| Taux de croissance annuel moyen mondial (TCAC) (2022-2030) | 7,5% |

| Données historiques | 2020-2021 |

| Période de prévision | 2022-2030 |

| Segments couverts |

Par type d'aéroport

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des infrastructures aéroportuaires : comprendre son impact sur la dynamique des entreprises

Le marché des infrastructures aéroportuaires connaît une croissance rapide, stimulée par la demande croissante des utilisateurs finaux en raison de facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une meilleure connaissance des avantages du produit. À mesure que la demande augmente, les entreprises élargissent leurs offres, innovent pour répondre aux besoins des consommateurs et capitalisent sur les tendances émergentes, ce qui alimente davantage la croissance du marché.

La densité des acteurs du marché fait référence à la répartition des entreprises ou des sociétés opérant sur un marché ou un secteur particulier. Elle indique le nombre de concurrents (acteurs du marché) présents sur un marché donné par rapport à sa taille ou à sa valeur marchande totale.

Les principales entreprises opérant sur le marché des infrastructures aéroportuaires sont :

- Hensel Phelps

- AECOM

- Entreprise de construction Turner

- Skanska

- Austin Industries

Avis de non-responsabilité : les sociétés répertoriées ci-dessus ne sont pas classées dans un ordre particulier.

- Obtenez un aperçu des principaux acteurs du marché des infrastructures aéroportuaires

Actualités et développements récents du marché des infrastructures aéroportuaires

Le marché des infrastructures aéroportuaires est évalué en collectant des données qualitatives et quantitatives issues de recherches primaires et secondaires, qui comprennent d'importantes publications d'entreprises, des données d'associations et des bases de données. Voici une liste des évolutions du marché des infrastructures aéroportuaires et des stratégies :

- En 2023, Hensel Phelps a été nommé gestionnaire de construction à risque (CMaR) pour le projet de nouveau terminal de l'aéroport international John Glenn Columbus par la Columbus Regional Airport Authority (CRAA). Pour le projet, les services de préconstruction et de construction seront fournis par l'équipe Hensel Phelps | Elford. Avec ce projet, Hensel Phelps entre sur le marché de l'Ohio et renforce son partenariat avec la CRAA et Elford. (Source : Hensel Phelps, communiqué de presse/site Web de l'entreprise/bulletin d'information)

- En 2022, AECOM a annoncé que sa coentreprise avec HJ Russell & Company, Airfield Management Partners, avait été sélectionnée pour fournir des services de gestion de programmes et de construction côté piste à l'aéroport international de Dallas Fort Worth. (Source : AECOM, communiqué de presse/site Web de l'entreprise/bulletin d'information)

Rapport sur le marché des infrastructures aéroportuaires : couverture et livrables

Le rapport « Taille et prévisions du marché des infrastructures aéroportuaires (2020-2030) » fournit une analyse détaillée du marché couvrant les domaines ci-dessous :

- Taille du marché et prévisions aux niveaux mondial, régional et national pour tous les segments de marché clés couverts par le périmètre

- Dynamique du marché, comme les facteurs moteurs, les contraintes et les opportunités clés

- Principales tendances futures

- Analyse détaillée des cinq forces de Porter

- Analyse du marché mondial et régional couvrant les principales tendances du marché, les principaux acteurs, les réglementations et les développements récents du marché

- Analyse du paysage industriel et de la concurrence couvrant la concentration du marché, l'analyse de la carte thermique, les principaux acteurs et les développements récents

- Profils d'entreprise détaillés avec analyse SWOT

Naveen est un professionnel expérimenté des études de marché et du conseil, fort de plus de 9 ans d'expertise dans des projets personnalisés, syndiqués et de conseil. Actuellement vice-président associé, il a géré avec succès les parties prenantes tout au long de la chaîne de valeur des projets et a rédigé plus de 100 rapports de recherche et plus de 30 missions de conseil. Son expertise couvre des projets industriels et gouvernementaux, contribuant significativement à la réussite de ses clients et à la prise de décision fondée sur les données.

Naveen est titulaire d'un diplôme d'ingénieur en électronique et communication de la VTU, Karnataka, et d'un MBA en marketing et opérations de l'Université de Manipal. Membre actif de l'IEEE depuis 9 ans, il a participé à des conférences et des colloques techniques et s'est porté volontaire au niveau des sections et des régions. Avant d'occuper ce poste, il a travaillé comme consultant stratégique associé chez IndustryARC et comme consultant en serveurs industriels chez Hewlett Packard (HP Global).

- Analyse historique (2 ans), année de base, prévision (7 ans) avec TCAC

- Analyse PEST et SWOT

- Taille du marché Valeur / Volume - Mondial, Régional, Pays

- Industrie et paysage concurrentiel

- Ensemble de données Excel

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires

Débloquez des remises exclusives sur les rapports

Demander maintenant

Obtenez un échantillon gratuit pour - Marché des infrastructures aéroportuaires

Obtenez un échantillon gratuit pour - Marché des infrastructures aéroportuaires