Aperçu du marché des dispositifs d’autotransfusion, croissance, tendances, analyse, rapport de recherche (2021-2028)

Prévisions du marché des dispositifs d'autotransfusion jusqu'en 2028 - Impact de la COVID-19 et analyse mondiale par type (produit et accessoires) ; application (chirurgie cardiaque, chirurgie orthopédique, transplantation d'organes, interventions traumatologiques et autres) ; utilisateur final (hôpitaux, cliniques spécialisées et centres de chirurgie ambulatoire)

- Statut : Publié

- Code du rapport : TIPRE00006521

- Catégorie : Sciences de la vie

- Nombre de pages : 178

- Formats de rapport disponibles :

- Date de dernière mise à jour : June 17, 2024

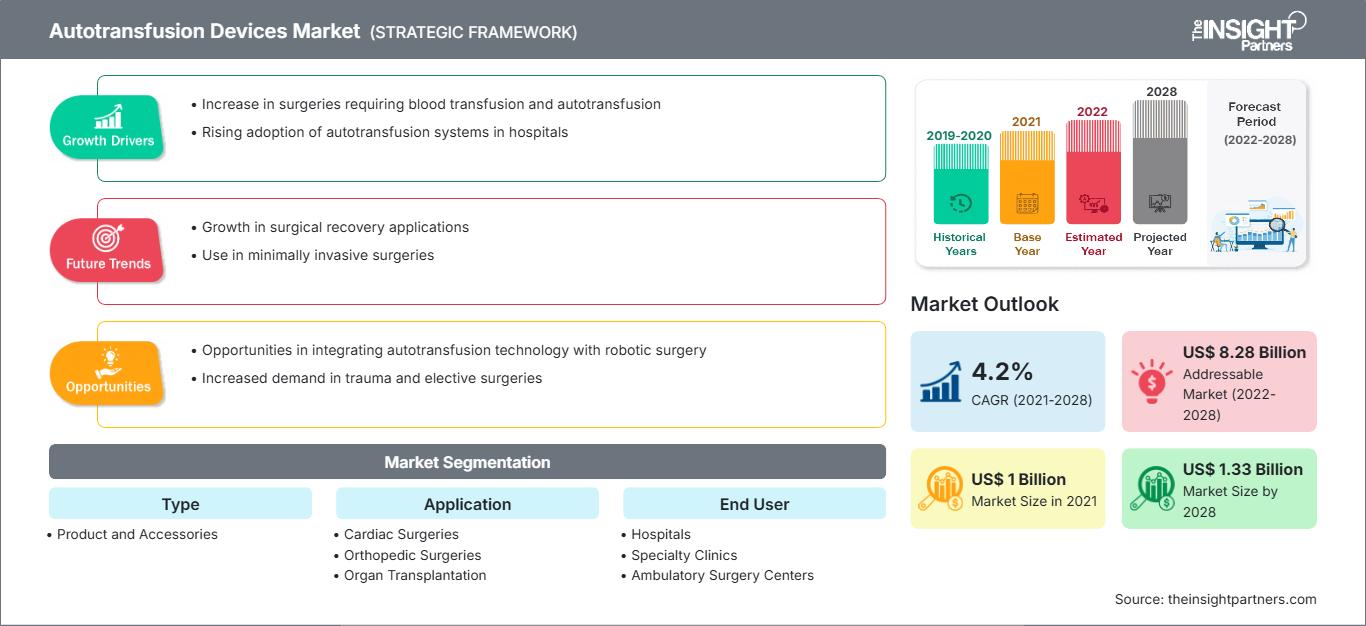

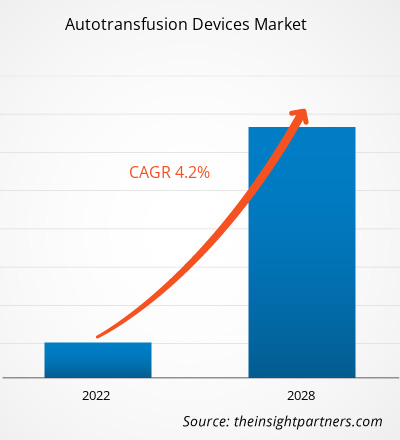

Le marché des dispositifs d'autotransfusion devrait passer de 1 000,26 millions de dollars américains en 2021 à 1 331,99 millions de dollars américains en 2028 ; sa croissance devrait atteindre un TCAC de 4,2 % entre 2021 et 2028.

La transplantation d'organes est une intervention chirurgicale pratiquée en cas de défaillance d'organes. Elle concerne généralement des organes tels que le cœur, le foie et les reins. Cependant, face à l'augmentation des maladies chroniques, d'autres organes tels que les poumons, le pancréas, la cornée et les tissus vasculaires doivent être transplantés. Ces interventions durent généralement plusieurs heures et entraînent d'importantes pertes sanguines. L'autotransfusion est donc l'une des méthodes les plus efficaces pour prévenir les pertes sanguines. Selon le Réseau uni pour le partage d'organes (UNOS), les transplantations d'organes réalisées aux États-Unis sont en constante augmentation, avec plus de 41 000 transplantations réalisées en 2021. De même, selon les données du Registre mondial des transplantations, l'Espagne représentait 20 % de tous les dons d'organes dans l'UE en 2019 et 6 % des dons mondiaux. Le taux de dons d'organes en Australie s'est amélioré ces dernières années, atteignant 21,8 donneurs par million d'habitants en 2019.

Vous bénéficierez d’une personnalisation sur n’importe quel rapport - gratuitement - y compris des parties de ce rapport, ou une analyse au niveau du pays, un pack de données Excel, ainsi que de profiter d’offres exceptionnelles et de réductions pour les start-ups et les universités

Marché des dispositifs d'autotransfusion: Perspectives stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

De même, le Canada compte 22,2 donneurs par million d'habitants et connaît une amélioration constante, en partie grâce au nombre de « médecins spécialistes des dons », c'est-à-dire les médecins de soins intensifs responsables des dons d'organes. Selon le Registre mondial des transplantations, la Chine comptait 5 818 donneurs en 2019, soit 4,1 par million d'habitants, et l'Inde 715 donneurs, soit 0,5 par million d'habitants. En revanche, la Russie affichait un taux légèrement supérieur de 5,1 donneurs par million d'habitants. Le partenariat public-privé, en collaboration avec les coordinateurs de transplantation, a contribué de manière significative à l'amélioration de la transplantation d'organes. Les pays en développement comme les pays développés ont constaté une augmentation des opérations de transplantation d'organes. Par exemple, des pays en développement comme l'Inde et Singapour émergent comme destinations de tourisme médical en Asie-Pacifique. Les pays progressent en termes de fourniture de traitements médicaux de meilleure qualité et plus avancés. Ainsi, le besoin croissant de transplantation d'organes est l'un des principaux facteurs à l'origine de la demande de diagnostics de transplantation tels que les dispositifs d'autotransfusion.

Le processus d'autotransfusion consiste à réinjecter le sang du patient. Le sang est prélevé dans la cavité péritonéale ou la région thoracique. Ce processus peut être réalisé avant, pendant et après l'intervention chirurgicale à l'aide du système d'autotransfusion. Les interventions médicales, telles que les arthroplasties, les chirurgies de la colonne vertébrale et les interventions cardiaques, entre autres, nécessitent l'autotransfusion. Elle contribue à réduire le risque d'infection et à éliminer les problèmes et complications liés à la conservation et à l'administration du sang de donneurs homologues. Elle contribue à prévenir la transmission de maladies transmissibles par le sang liées à la transfusion chez les patients.

Aperçu du marché : Développements technologiques dans les dispositifs d'autotransfusion

Les dispositifs d'autotransfusion sont généralement déployés lors d'interventions chirurgicales de longue durée, comme les transplantations rénales, et en cas d'urgence. Ces interventions chirurgicales sont associées à des risques de pertes sanguines excessives, ce qui rend difficile le rattrapage sanguin par du sang neuf, notamment en cas de groupes sanguins rares. Face à la forte demande, les principaux acteurs du marché des dispositifs d'autotransfusion proposent des dispositifs avancés et entièrement automatisés qui réduisent les interventions humaines. Par exemple, en avril 2021, le B-Capta de LivaNova PLC a été approuvé par la Food and Drug Administration (FDA) américaine. Lors des interventions chirurgicales complexes de pontage cardiopulmonaire chez l'enfant et l'adulte, ce dispositif permet une surveillance rapide et précise des paramètres veineux et des gaz du sang. De même, en avril 2019, BD a lancé son milieu de contrôle qualité BD BACTEC dans le monde entier pour faciliter l'identification des plaquettes contaminées lors des transfusions. De plus, de nombreuses entreprises ont mis en œuvre des stratégies telles que des acquisitions, des partenariats et autres pour conquérir le marché. Par exemple, Medtronics a acquis AV Medical Technologies en octobre 2019. En décembre 2019, Getinge a racheté Applikon Biotechnology, leader mondial du développement et de la fourniture de systèmes de bioréacteurs innovants, du laboratoire à l'échelle industrielle. Ainsi, ces avancées sont susceptibles d'apporter de nouvelles tendances sur le marché des dispositifs d'autotransfusion dans les années à venir.

Informations basées sur les applications

En fonction des applications, le marché des dispositifs d'autotransfusion est segmenté en chirurgies cardiaques, chirurgies orthopédiques, transplantation d'organes, interventions traumatologiques, etc. Le segment des chirurgies cardiaques détenait la plus grande part de marché en 2021, tandis que le segment de la transplantation d'organes devrait également enregistrer le TCAC le plus élevé du marché au cours de la période de prévision.

Les acteurs du marché des dispositifs d'autotransfusion adoptent des stratégies organiques telles que le lancement et l'expansion de produits pour étendre leur présence et leur portefeuille de produits à l'échelle mondiale et répondre à la demande croissante. Les développements des entreprises sur le marché des dispositifs d'autotransfusion se caractérisent par des développements organiques et inorganiques. Plusieurs entreprises privilégient des stratégies organiques, telles que le lancement et l'expansion de produits. Les stratégies de croissance inorganiques observées sur le marché des dispositifs d'autotransfusion reposent sur des partenariats et des collaborations. Ces stratégies ont permis aux acteurs du marché de développer leurs activités et d'améliorer leur présence géographique. De plus, des stratégies de croissance telles que les acquisitions et les partenariats ont permis de renforcer leur clientèle et d'élargir leur portefeuille de produits. Les entreprises ont maximisé leur croissance grâce à plusieurs stratégies inorganiques afin d'améliorer la valeur et le positionnement des dispositifs d'autotransfusion sur le marché. Les développements organiques représentent 66,67 % du total des développements stratégiques sur le marché des dispositifs d'autotransfusion, tandis que les stratégies inorganiques représentent 33,33 % de la croissance des entreprises.

Le marché des dispositifs d'autotransfusion est segmenté comme suit :

Le marché des dispositifs d'autotransfusion est segmenté en fonction du type, de l'application et de l'utilisateur final. Selon le type, le marché des dispositifs d'autotransfusion se divise en produits et accessoires. Selon l'application, le marché des dispositifs d'autotransfusion est segmenté en chirurgies cardiaques, chirurgies orthopédiques, transplantations d'organes, interventions traumatologiques, etc.

Le marché des dispositifs d'autotransfusion, selon l'utilisateur final, est divisé en hôpitaux, cliniques spécialisées et centres de chirurgie ambulatoire.

Aperçu régional du marché des dispositifs d'autotransfusion

Les tendances régionales et les facteurs influençant le marché des dispositifs d'autotransfusion tout au long de la période de prévision ont été analysés en détail par les analystes de The Insight Partners. Cette section aborde également les segments et la géographie du marché des dispositifs d'autotransfusion en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et en Amérique centrale.

Portée du rapport sur le marché des dispositifs d'autotransfusion

| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2021 | US$ 1 Billion |

| Taille du marché par 2028 | US$ 1.33 Billion |

| TCAC mondial (2021 - 2028) | 4.2% |

| Données historiques | 2019-2020 |

| Période de prévision | 2022-2028 |

| Segments couverts |

By Type

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des dispositifs d'autotransfusion : comprendre son impact sur la dynamique commerciale

Le marché des dispositifs d'autotransfusion connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux, due à des facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une meilleure connaissance des avantages du produit. Face à cette demande croissante, les entreprises élargissent leur offre, innovent pour répondre aux besoins des consommateurs et capitalisent sur les nouvelles tendances, ce qui alimente la croissance du marché.

- Obtenez le Marché des dispositifs d'autotransfusion Aperçu des principaux acteurs clés

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires