Dispositivos de autotransfusión Descripción general del mercado, crecimiento, tendencias, análisis, informe de investigación (2021-2028)

Dispositivos de autotransfusión Descripción general del mercado, crecimiento, tendencias, análisis, informe de investigación (2021-2028)

- Estado : Publicada

- Código de informe : TIPRE00006521

- Categoría : Ciencias de la vida

- Número de páginas : 178

- Formatos de informe disponibles :

- Fecha de última actualización : June 17, 2024

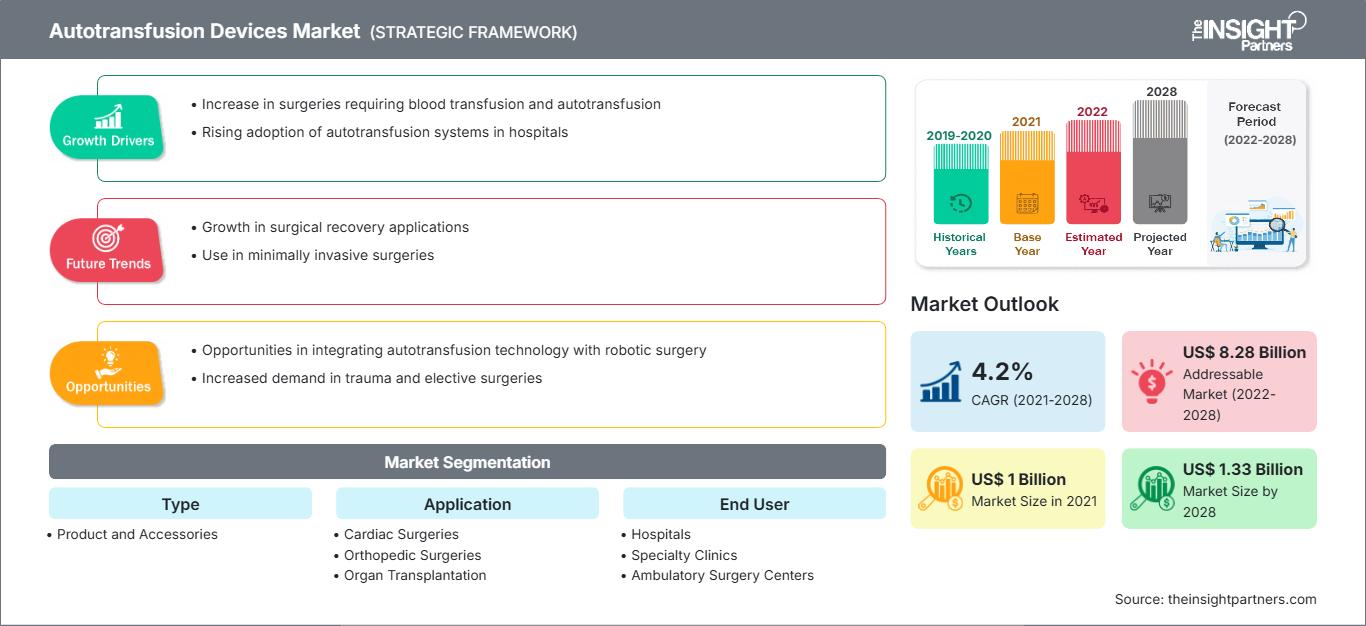

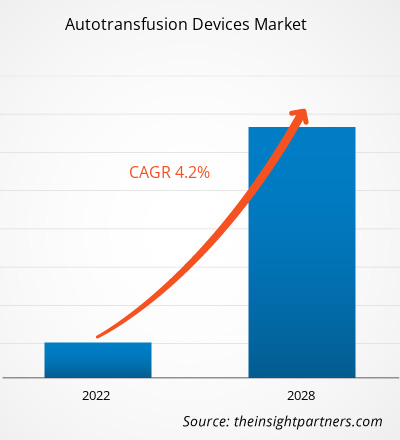

Se espera que el mercado de dispositivos de autotransfusión crezca de US$ 1.000,26 millones en 2021 a US$ 1.331,99 millones en 2028; se estima que crecerá a una CAGR del 4,2% entre 2021 y 2028.

El trasplante de órganos es un procedimiento quirúrgico que se realiza en caso de insuficiencia orgánica. Generalmente, se trasplantan órganos como el corazón, el hígado y el riñón; sin embargo, debido al aumento de enfermedades crónicas, se requieren trasplantes para otros órganos como pulmones, páncreas, córnea y tejidos vasculares. Estos procedimientos suelen durar horas y conllevan una gran pérdida de sangre, siendo la autotransfusión uno de los métodos más eficaces para prevenirla. Según la Red Unida para la Intercambio de Órganos (UNOS), los trasplantes de órganos realizados en EE. UU. han aumentado continuamente, con más de 41 000 en 2021. Asimismo, según datos del Registro Mundial de Trasplantes, España representó el 20 % de todas las donaciones de órganos en la UE en 2019 y el 6 % de las donaciones mundiales. La tasa de donantes de órganos de Australia ha mejorado en los últimos años, alcanzando los 21,8 donantes por millón de habitantes en 2019.

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de dispositivos de autotransfusión: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

De igual manera, Canadá cuenta con 22,2 donantes por millón de habitantes y su cifra está mejorando constantemente, en parte gracias a la figura de los "médicos de donación", médicos de cuidados intensivos responsables de la donación de órganos. Según el Registro Mundial de Trasplantes, China contaba con 5.818 donantes en 2019, equivalente a 4,1 por millón de habitantes, y la India con 715 donantes, equivalente a 0,5 por millón de habitantes. Por otro lado, Rusia registró una tasa ligeramente superior, de 5,1 donantes por millón de habitantes. La colaboración público-privada con los coordinadores de trasplantes ha contribuido significativamente a la mejora del trasplante de órganos. Tanto los países en desarrollo como los desarrollados han experimentado un aumento en las cirugías de trasplante de órganos. Por ejemplo, países en desarrollo como la India y Singapur se están consolidando como destinos de turismo médico en Asia Pacífico. Los países están progresando en la prestación de tratamientos médicos de mayor calidad y tecnología. Por lo tanto, la creciente necesidad de trasplantes de órganos es uno de los factores clave que impulsa la demanda de diagnósticos para trasplantes, como los dispositivos de autotransfusión.

El proceso de autotransfusión implica la reinfusión de la sangre del paciente. La sangre se extrae de la cavidad peritoneal o del tórax. El proceso puede realizarse antes, durante y después de la cirugía mediante el sistema de autotransfusión. Procedimientos médicos, como el reemplazo articular, las cirugías de columna y las cirugías cardíacas, entre otros, requieren autotransfusión. Esta ayuda a reducir el riesgo de infección y a eliminar los problemas y complicaciones asociados con el almacenamiento y la administración de sangre de donantes homólogos. Ayuda a prevenir la transmisión de enfermedades de transmisión sanguínea relacionadas con las transfusiones en los pacientes.

Perspectivas del mercado:

Desarrollos tecnológicos en dispositivos de autotransfusión

Los dispositivos de autotransfusión suelen emplearse durante cirugías de larga duración, como trasplantes de riñón, y en casos de emergencia. Estas cirugías conllevan la posibilidad de una pérdida excesiva de sangre, lo que dificulta su reposición con sangre nueva, especialmente en el caso de grupos sanguíneos poco comunes. Debido a la amplia demanda, los principales actores del mercado de dispositivos de autotransfusión ofrecen dispositivos avanzados y totalmente automatizados que reducen la intervención humana. Por ejemplo, en abril de 2021, la Administración de Alimentos y Medicamentos de EE. UU. aprobó el B-Capta de LivaNova PLC. Durante cirugías complejas de derivación cardiopulmonar en niños y adultos, este dispositivo facilita la monitorización rápida y precisa de los parámetros venosos y de gases en sangre. De igual manera, en abril de 2019, BD lanzó a nivel mundial su medio de control de calidad BD BACTEC para ayudar a identificar unidades de plaquetas contaminadas durante las transfusiones.

Además, muchas empresas emplearon estrategias como adquisiciones, asociaciones y otras para captar el mercado. Por ejemplo, Medtronics adquirió AV Medical Technologies en octubre de 2019. En diciembre de 2019, Getinge adquirió Applikon Biotechnology, líder mundial en el desarrollo y suministro de sistemas de biorreactores innovadores, desde el laboratorio hasta la escala industrial. Por lo tanto, es probable que estos avances impulsen nuevas tendencias en el mercado de dispositivos de autotransfusión en los próximos años.

Perspectivas basadas en aplicaciones

Según la aplicación, el mercado de dispositivos de autotransfusión se segmenta en cirugías cardíacas, cirugías ortopédicas, trasplantes de órganos, procedimientos traumatológicos y otros. El segmento de cirugías cardíacas tuvo la mayor participación de mercado en 2021, mientras que se estima que el segmento de trasplantes de órganos registrará la mayor tasa de crecimiento anual compuesta (TCAC) del mercado durante el período de pronóstico.

Los actores del mercado de dispositivos de autotransfusión adoptan estrategias orgánicas, como el lanzamiento y la expansión de productos, para expandir su presencia y cartera de productos a nivel mundial y satisfacer la creciente demanda. Los desarrollos de las empresas en este mercado se han caracterizado por ser orgánicos e inorgánicos. Varias empresas se centran en estrategias orgánicas, como el lanzamiento y la expansión de productos. Las estrategias de crecimiento inorgánico observadas en el mercado de dispositivos de autotransfusión se basaron en alianzas y colaboraciones. Estas estrategias de crecimiento han ayudado a los actores del mercado de dispositivos de autotransfusión a expandir sus negocios y a fortalecer su presencia geográfica. Además, estrategias de crecimiento como adquisiciones y alianzas contribuyeron a fortalecer su base de clientes y a ampliar su cartera de productos. Las empresas han maximizado su crecimiento con diversas estrategias inorgánicas para mejorar el valor y la posición de mercado de los dispositivos de autotransfusión. Los desarrollos orgánicos representan el 66,67 % del total de desarrollos estratégicos en el mercado de dispositivos de autotransfusión, mientras que las estrategias inorgánicas representan el 33,33 % del crecimiento de las empresas.

El mercado de dispositivos de autotransfusión se ha segmentado de la siguiente manera:

El mercado de dispositivos de autotransfusión se segmenta según el tipo, la aplicación y el usuario final. Según el tipo, se divide en productos y accesorios. Según la aplicación, se segmenta en cirugías cardíacas, cirugías ortopédicas, trasplantes de órganos, procedimientos traumatológicos, entre otros.

El mercado de dispositivos de autotransfusión, según el usuario final, se divide en hospitales, clínicas especializadas y centros quirúrgicos ambulatorios.

Perspectivas regionales del mercado de dispositivos de autotransfusión

Los analistas de The Insight Partners han explicado detalladamente las tendencias regionales y los factores que influyen en el mercado de dispositivos de autotransfusión durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de dispositivos de autotransfusión en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

Alcance del informe de mercado de dispositivos de autotransfusión

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2021 | 1.000 millones de dólares estadounidenses |

| Tamaño del mercado en 2028 | 1.330 millones de dólares estadounidenses |

| CAGR global (2021-2028) | 4,2% |

| Datos históricos | 2019-2020 |

| Período de pronóstico | 2022-2028 |

| Segmentos cubiertos |

Por tipo

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de dispositivos de autotransfusión: comprensión de su impacto en la dinámica empresarial

El mercado de dispositivos de autotransfusión está creciendo rápidamente, impulsado por la creciente demanda del usuario final debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y un mayor conocimiento de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una descripción general de los principales actores clave del mercado de dispositivos de autotransfusión

Perfiles de empresas en el mercado de dispositivos de autotransfusión

- BD

- Braile Biomédica

- Fresenius SE & Co. KGaA

- Corporación Haemonetics

- LivaNova PLC

- Medtronic

- Redax SpA

- SARSTEDT AG y Co. KG

- Teleflex Incorporated

- Zimmer Biomet

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias