Autotransfusion Devices Market Drivers and Forecasts by 2028

Autotransfusion Devices Market Forecast to 2028 - Analysis By Type (Product and Accessories); Application (Cardiac Surgeries, Orthopedic Surgeries, Organ Transplantation, Trauma Procedures, and Others); End User (Hospitals, Specialty Clinics, and Ambulatory Surgery Centers)

- Status : Published

- Report Code : TIPRE00006521

- Category : Life Sciences

- No. of Pages : 178

- Available Report Formats :

- Last update date : June 17, 2024

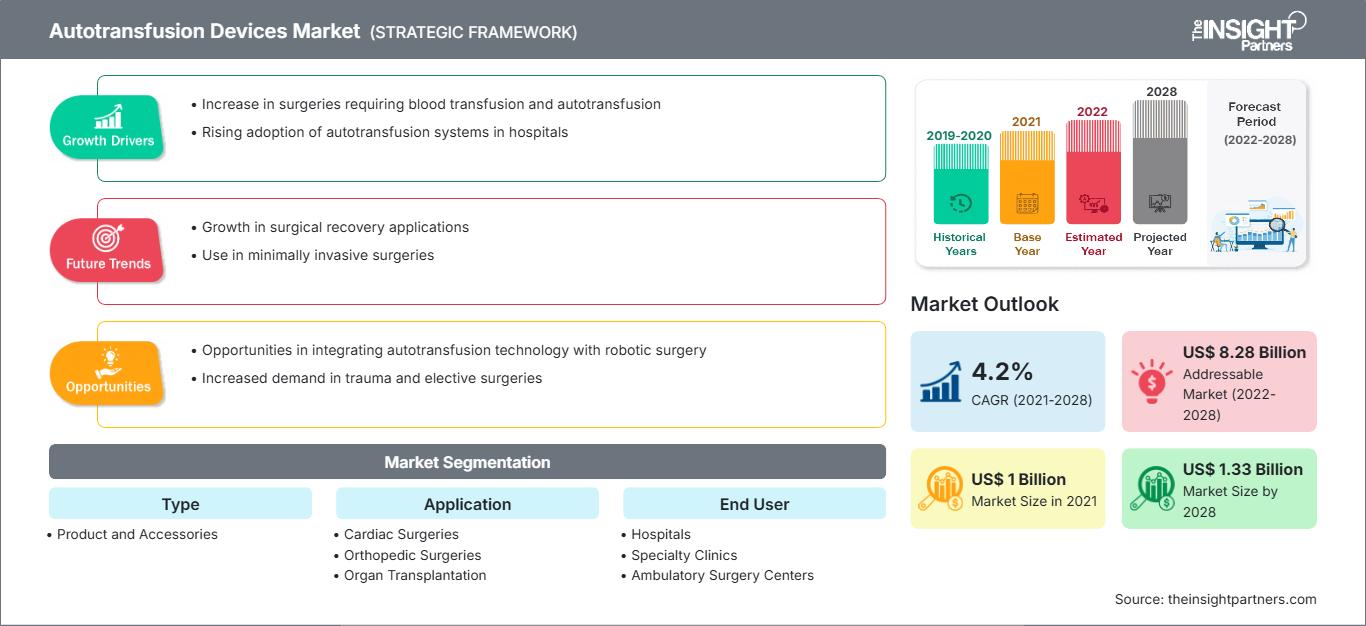

2021 Market Size

US$ 1 Bn

Base year value

2028 Forecast

US$ 1.33 Bn

Projected by 2028

CAGR 2022-2028

4.2 %

Growth rate

Addressable Market

US$ 8.28 Bn

(2022-2028)

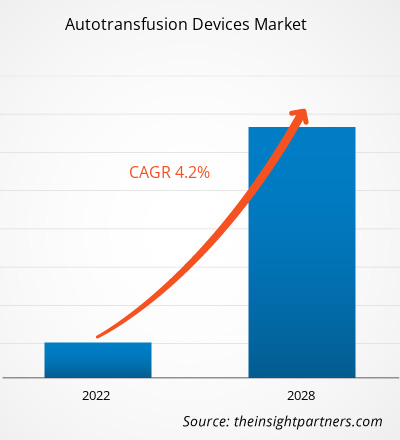

The autotransfusion devices market is expected to grow from US$ 1,000.26 million in 2021 to US$ 1,331.99 million by 2028; it is estimated to grow at a CAGR of 4.2% from 2021 to 2028.

Organ transplantation is a surgical procedure performed in case of organ failure. Usually, organ transplantation is conducted for organs such as the heart, liver, and kidney; however, with rising cases of chronic diseases, transplantation is needed for other organs such as lungs, pancreas, cornea, and vascular tissues. These procedures generally take hours, and there is a lot of blood loss, and autotransfusion is one of the valuable methods to prevent blood loss. According to the United Network for Organ Sharing (UNOS), organ transplants conducted in the US have continuously increased, with over 41,000 transplants performed in 2021. Similarly, according to World Transplant Registry data, Spain accounted for 20% of all organ donations in the EU in 2019 and 6% of worldwide donations. Australia's organ donor rate has improved in recent years, rising to 21.8 donors per million population in 2019.

Market Research Highlights

- North America dominated the market with 32.6% share in 2019.

- Asia Pacific is poised to grow at a CAGR of 4.7% over the forecast period.

- United States market is projected to grow at a CAGR of 4.6% over the forecast period.

- By Type, the Accessories segment accounted for the largest market share of 55.1% in 2019.

- By Application, the Organ Transplantation segment is anticipated to witness the fastest growth, registering a CAGR of 6.1% over the forecast period

- By End User, the Hospitals segment accounted for the largest market share of 64% in 2019.

- The report profiles key industry players such as Teleflex Inc, Fresenius SE & Co KGaA, BD, Medtronic Plc, Zimmer Biomet Holdings Inc, Redax SpA, Braile Biomedica Industry, Commerce and Representations Ltd, Haemonetics Corp, SARSTEDT AG & Co KG, LivaNova Plc, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Autotransfusion Devices Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Similarly, Canada has 22.2 donors per million population and is steadily improving, partially attributed to the figure of "Donation Physicians" - intensive care doctors who are responsible for organ donation. According to the World Transplant Registry, China had 5,818 donors in 2019, or 4.1 per million population and India had 715 donors or 0.5 per million population in 2019. On the other hand, Russia had a slightly higher rate of 5.1 donors per million people. The public-private partnership in collaboration with transplant coordinators has made a significant contribution to the improvement of organ transplantation. Both developing and developed countries have seen an increase in organ transplant surgeries. For example, developing countries such as India and Singapore are emerging as medical tourism destinations in Asia Pacific. Countries are progressing in terms of providing better and advanced medical treatments. Thus, the rising need for organ transplantation is among the key factors driving the demand for transplant diagnostics such as autotransfusion devices.

The autotransfusion process involves the reinfusion of the patient's blood. Blood is collected from the peritoneal cavity or thorax region. The process can be carried out before surgery or during and after the surgery using the autotransfusion system. Medical procedures, like joint replacement, spinal surgeries, and cardiac, among others, require autotransfusion. It helps to reduce the risk of infection, and also it eliminates the problems and complications associated with the banking and administration of homologous donor blood. It helps to prevent the transmission of transfusion-related blood-borne diseases in patients.

Market Insights

Technological Developments in Autotransfusion Devices

Autotransfusion devices are usually deployed during long-hour surgeries, such as kidney transplantation, and in cases of emergencies. These surgeries are associated with the chances of excessive blood loss, which makes it difficult to make up the blood loss with new blood, especially in case of rare blood groups. Owing to the ample demand, the key players in the autotransfusion devices market offer advanced and fully automated autotransfusion devices that reduce human interventions. For instance, in April 2021, LivaNova PLC's B-Capta has been approved by the US Food and Drug Administration. During complex paediatric and adult cardiopulmonary bypass surgeries, this device aids in the rapid and accurate monitoring of venous and blood gas parameters. Similarly, in April 2019, BD launched their BD BACTEC quality control media worldwide to help identify contaminated platelet units during transfusions.

Moreover, many companies employed strategic activities such as acquisitions, partnership and others to capture the market. For instance, Medtronics acquired AV Medical Technologies, in October 2019. In December 2019, Getinge purchased Applikon Biotechnology, a global leader in the development and supply of innovative bioreactor systems from the laboratory to the industrial scale. Thus, such advancements are likely to bring new trends in the autotransfusion devices market in the coming years.

Application–Based Insights

Based on application, the autotransfusion devices market is segmented into cardiac surgeries, orthopedic surgeries, organ transplantation, trauma procedures, and others. The cardiac surgeries segment held the largest share of the market in 2021, while the organ transplantation segment is also estimated to register the highest CAGR in the market during the forecast period.

The autotransfusion devices market players adopt organic strategies such as product launch and expansion to expand their footprint and product portfolio globally and meet the growing demand. The developments by the companies in the autotransfusion devices market have been characterized as organic and inorganic developments. Various companies are focusing on organic strategies, such as product launch and expansion. Inorganic growth strategies witnessed in the autotransfusion devices market were partnerships and collaborations. These growth strategies have aided the autotransfusion devices market players in the expansion of their businesses and enhanced their geographic presence. Additionally, growth strategies such as acquisitions and partnerships helped in strengthening their customer base and increasing the product portfolio. The companies have maximized their growth with several inorganic strategies to enhance the autotransfusion devices market value and position in the autotransfusion devices market. Organic developments hold 66.67% of the total strategic developments in the autotransfusion devices market. Whereas inorganic strategies account for 33.33% of the growth of the companies.

The autotransfusion devices market has been segmented as follows:

The autotransfusion devices market is segmented based on type, application, and end user. Based on type, the autotransfusion devices market is bifurcated into products and accessories. The autotransfusion devices market, based on application, is segmented into cardiac surgeries, orthopedic surgeries, organ transplantation, trauma procedures, and others.

The autotransfusion devices market, based on end user, is divided into hospitals, specialty clinics, and ambulatory surgical centers.

Autotransfusion Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 1 Billion |

| Market Size by 2028 | US$ 1.33 Billion |

| Global CAGR (2021 - 2028) | 4.2% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2028 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Autotransfusion Devices Market Players Density: Understanding Its Impact on Business Dynamics

The Autotransfusion Devices Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Company Profiles in Autotransfusion Devices Market

- BD

- Braile Biomedica

- Fresenius SE & Co. KGaA

- Haemonetics Corporation

- LivaNova PLC

- Medtronic

- Redax S.p.A.

- SARSTEDT AG and Co. KG

- Teleflex Incorporated

- Zimmer Biomet

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends