Croissance, taille, part, tendances, analyse des principaux acteurs et prévisions du marché des dérivés du plasma sanguin jusqu’en 2028

Prévisions du marché des dérivés du plasma sanguin jusqu'en 2028 - Impact de la COVID-19 et analyse mondiale par type (albumine, facteur VIII, facteur IX, immunoglobuline, hyperimmunoglobuline et autres), application (hémophilie, hypogammaglobulinémie, déficits immunitaires, maladie de von Willebrand et autres) et utilisateur final (hôpitaux, cliniques et autres)

- Statut : Publié

- Code du rapport : TIPRE00007250

- Catégorie : Sciences de la vie

- Nombre de pages : 209

- Formats de rapport disponibles :

- Date de dernière mise à jour : June 17, 2024

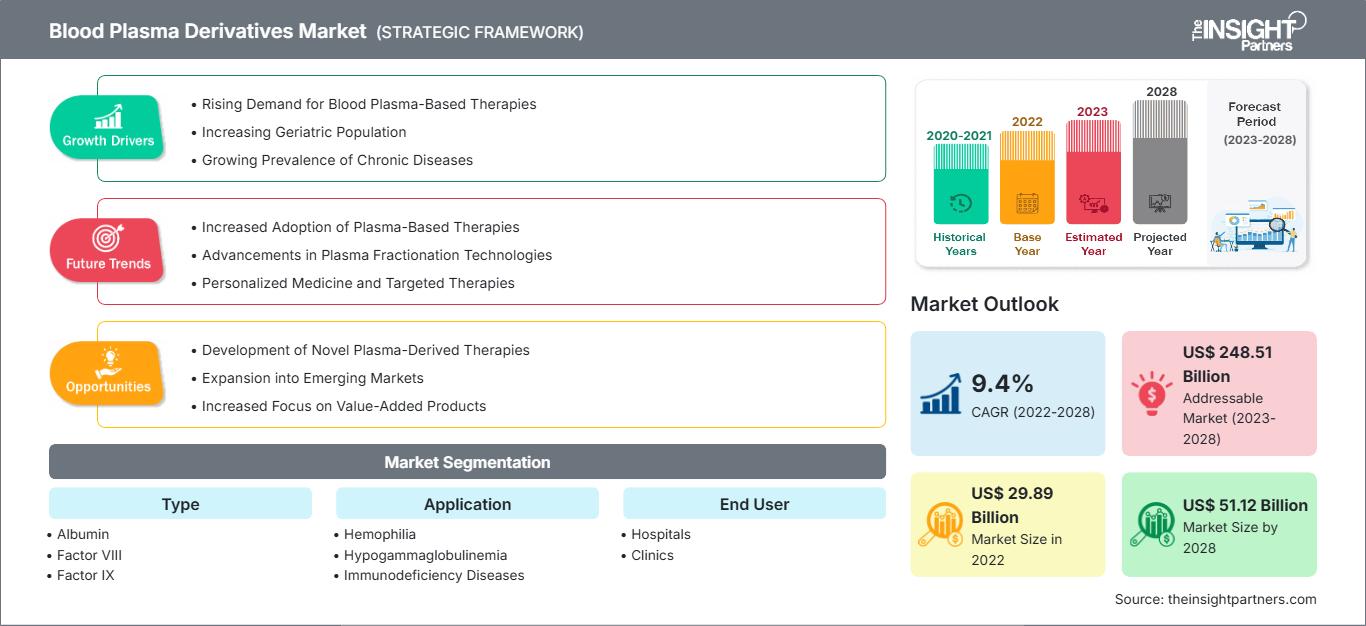

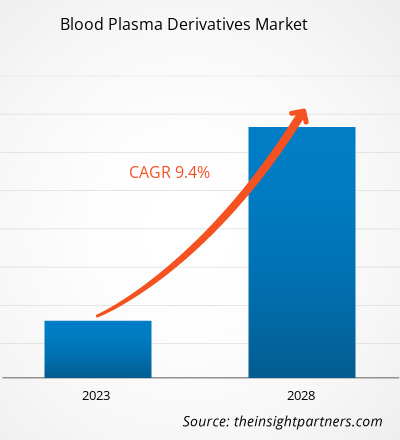

[Rapport de recherche] Le marché des dérivés du plasma sanguin devrait atteindre 51 119,24 millions de dollars américains d'ici 2028, contre 29 886,12 millions de dollars américains en 2022 ; il devrait enregistrer un TCAC de 9,4 % entre 2022 et 2028.

Les dérivés du plasma sont obtenus à partir de protéines plasmatiques explicites par le cycle de fractionnement. Ils contiennent une grande quantité de protéines, de sels, de minéraux, d'hormones, de vitamines et d'inhibiteurs de protéase. Ainsi, ils sont couramment utilisés pour détruire les virus responsables des troubles de la coagulation, de l'hépatite B, de l'hépatite C, de l'hémophilie A, de l'immunodéficience, de l'hypogammaglobulinémie, de l'hémophilie B et du virus de l'immunodéficience humaine.

Le marché des dérivés du plasma sanguin est segmenté en fonction du type, de l'application, de l'utilisateur final et de la géographie. Géographiquement, le marché est largement segmenté en Amérique du Nord, Europe, Asie-Pacifique, Moyen-Orient et Afrique, et Amérique du Sud et centrale. Le rapport offre des informations et une analyse approfondie du marché, en mettant l'accent sur des paramètres tels que les tendances, les avancées technologiques et la dynamique du marché, ainsi que sur l'analyse du paysage concurrentiel des principaux acteurs mondiaux.

Vous bénéficierez d’une personnalisation sur n’importe quel rapport - gratuitement - y compris des parties de ce rapport, ou une analyse au niveau du pays, un pack de données Excel, ainsi que de profiter d’offres exceptionnelles et de réductions pour les start-ups et les universités

Marché des dérivés du plasma sanguin: Perspectives stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Aperçu du marché – Marché des dérivés du plasma sanguin

L'utilisation croissante de l'immunoglobuline G dans de multiples traitements offrira des opportunités pour le marché des dérivés du plasma sanguin dans les années à venir

Les thérapies à base d'immunoglobuline G (IgG) sont largement utilisées pour traiter les déficits immunitaires primaires causés par des anomalies génétiques. La demande d'IgG n'a cessé d'augmenter ces dernières années en raison de la sensibilisation croissante à la thérapie par IgG. D'après des essais contrôlés réalisés par Network Meta Analysis (NMA), la thérapie par IgG a été approuvée pour le traitement du syndrome de Guillain-Barré (SGB), de la polyneuropathie inflammatoire démyélinisante chronique (PIDC), de la neuropathie motrice multifocale (NMM) et de la dermatomyosite. Les thérapies par IgG sont également efficaces pour traiter les exacerbations de la myasthénie grave et le syndrome de la personne raide. De plus, il offre une efficacité convaincante dans les maladies auto-immunes telles que l'épilepsie, la neuromyélite et l'encéphalite auto-immune.

- En 2022, Grifols a conclu une entente avec la Société canadienne du sang. Cette entente accélère l'autosuffisance en immunoglobulines pour le Canada. En vertu de cette entente, Grifols collaborera avec la Société canadienne du sang pour augmenter progressivement l'approvisionnement en plasma au Canada afin d'atteindre des volumes de 2,4 millions de grammes de médicaments Ig par an d'ici 2026.

- En 2021, la Food and Drug Administration (FDA) a approuvé Cutaquig pour un usage médical. Il est utilisé comme traitement de remplacement de l'immunodéficience humorale primaire (IP) chez les adultes et les patients pédiatriques de 2 ans et plus. Cutaquig est une solution d'immunoglobulines prête à l'emploi pour perfusion sous-cutanée. Le produit est disponible en flacons à usage unique de 1 g, 1,65 g, 2 g, 3,3 g, 4 g ou 8 g.

- En août 2020, Kedrion Biopharma (Italie) a commencé à améliorer un traitement induit par plasma pour le traitement des patients atteints de la COVID-19. Le traitement pourrait être accessible aux patients d'ici trois à six ans.

Une grande partie des IgG est utilisée dans des spécialités autres que l'immunologie, telles que l'oncologie, la neurologie, l'hématologie et la rhumatologie. Comparée à toutes les autres, la neurologie est la spécialité qui connaît la croissance la plus rapide sur le marché mondial. La croissance du marché de l'immunoglobuline G est attribuée à son approbation pour une utilisation sur AMM pour la polyneuropathie inflammatoire démyélinisante chronique (PIDC), suivie de son utilisation hors AMM dans les déficits immunitaires secondaires causés par le lymphome, le myélome et la leucémie et dans certaines thérapies immunosuppressives, en particulier les thérapies ciblant les lymphocytes B. Ainsi, la large gamme d'utilisation des IgG dans de multiples traitements, pour des prescriptions conformes et hors AMM, stimulera la demande mondiale d'IgG dans les années à venir.

Informations sur l'utilisateur final

Selon l'utilisateur final, le marché mondial des dérivés du plasma sanguin est segmenté en hôpitaux, cliniques et autres. Le segment hospitalier détenait la plus grande part de marché en 2022 et devrait enregistrer le TCAC le plus élevé au cours de la période de prévision. L'augmentation du nombre d'admissions à l'hôpital et la prévalence croissante de la maladie de von Willebrand, des troubles immunodéficients et de l'hémophilie devraient stimuler la croissance du marché pour le segment hospitalier au cours de la période de prévision. De plus, les pays émergents connaissent une forte demande en environnements hospitaliers avancés pour faire face à l'augmentation du nombre de patients et aux préoccupations croissantes en matière de santé publique. Par ailleurs, diverses thérapies de substitution par immunoglobulines sont menées dans les hôpitaux afin d'observer les doses et les effets indésirables liés au traitement et de surveiller les résultats cliniques du produit. Les hôpitaux sont les principaux centres de fourniture de thérapies de substitution par immunoglobulines, qui sont développées à l'aide de nouvelles technologies. Les patients recevant des traitements par immunoglobulines à l'hôpital perçoivent les avantages d'une plus grande sécurité, d'une surveillance plus étroite et du soutien des professionnels de santé et des experts. Ainsi, les avantages offerts par les hôpitaux, tels que des soins appropriés centrés sur le patient et la disponibilité des mécanismes de remboursement, devraient alimenter la croissance du marché pour ce segment au cours de la période de prévision.

Les lancements de produits et les fusions et acquisitions font partie des stratégies largement adoptées par les acteurs du marché mondial des dérivés du plasma sanguin. Voici quelques-uns des développements clés récents en matière de produits :

- En avril 2022, Grifols a annoncé la finalisation de l'acquisition de 100 % du capital social de Tiancheng (Allemagne) Pharmaceutical Holdings AG. Tiancheng (Allemagne) Pharmaceutical Holdings AG est une société allemande qui détient 89,88 % des actions ordinaires et 1,08 % des actions privilégiées de Biotest AG. Suite à la clôture de l'offre publique d'achat (OPA) et à la clôture de l'acquisition, Grifols contrôle 96,20 % des droits de vote et détient 69,72 % du capital social de Biotest AG.

| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2022 | US$ 29.89 Billion |

| Taille du marché par 2028 | US$ 51.12 Billion |

| TCAC mondial (2022 - 2028) | 9.4% |

| Données historiques | 2020-2021 |

| Période de prévision | 2023-2028 |

| Segments couverts |

By Type

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des dérivés du plasma sanguin : comprendre son impact sur la dynamique des entreprises

Le marché des dérivés du plasma sanguin connaît une croissance rapide, porté par une demande croissante des utilisateurs finaux, due à des facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une meilleure connaissance des avantages du produit. Face à cette demande croissante, les entreprises élargissent leur offre, innovent pour répondre aux besoins des consommateurs et capitalisent sur les nouvelles tendances, ce qui alimente la croissance du marché.

- Obtenez le Marché des dérivés du plasma sanguin Aperçu des principaux acteurs clés

Dérivés du plasma sanguin – Segmentation du marché

Selon le type, le marché des dérivés du plasma sanguin est segmenté en albumine, facteur VIII, facteur IX, immunoglobuline, hyperimmunoglobuline, et autres. Le marché des immunoglobulines est lui-même segmenté en IgG, IgM, IgA, IgD et IgE. Par application, le marché des dérivés du plasma sanguin est segmenté en hémophilie, hypogammaglobulinémie, maladies d'immunodéficience, maladie de von Willebrand, et autres applications. Le marché, par utilisateur final, est segmenté en hôpitaux, cliniques, et autres. Sur le plan géographique, le marché des dérivés du plasma sanguin est segmenté en Amérique du Nord (États-Unis, Canada et Mexique), Europe (France, Allemagne, Royaume-Uni, Italie, Espagne et reste de l'Europe), Asie-Pacifique (Chine, Japon, Inde, Australie, Corée du Sud et reste de l'Asie-Pacifique), Moyen-Orient et Afrique. Afrique (Arabie saoudite, Afrique du Sud, Émirats arabes unis et reste du Moyen-Orient et de l'Afrique) et Amérique du Sud et centrale (Brésil, Argentine et reste de l'Amérique du Sud et centrale).

Profils d'entreprise - Marché des dérivés du plasma sanguin

- Grifols, SA

- SK Plasma Co., Ltd.

- Fusion Healthcare

- Biotest AG

- Green Cross Corp

- Kedrion

- LFB SA

- Octapharma AG

- CSL Limited

- Takeda Pharmaceutical Company Limited

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires