Rapport sur le marché des services pour champs pétrolifères 2031 par segments, géographie, dynamique, développements récents et perspectives stratégiques

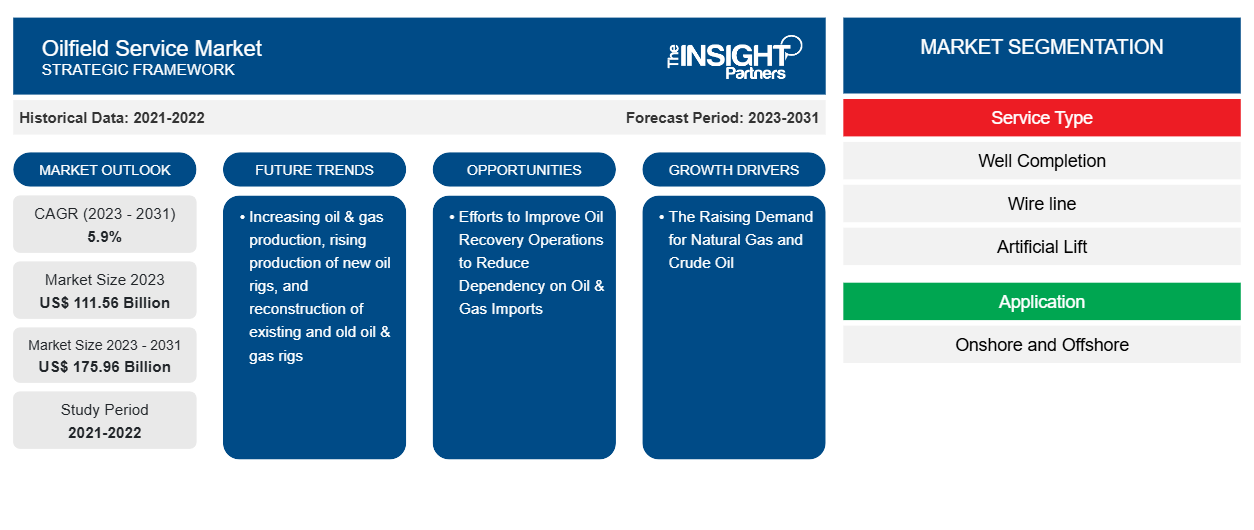

Données historiques : 2021-2022 | Année de référence : 2023 | Période de prévision : 2023-2031Taille et prévisions du marché des services pétroliers (2021-2031), parts mondiales et régionales, tendances et opportunités de croissance. Couverture du rapport d'analyse : par type de service (complétion de puits, ligne de câble, levage artificiel, perforation, fluides de forage et de complétion, et autres), application (onshore et offshore) et géographie.

- Statut : Données publiées

- Code du rapport : TIPMC100001361

- Catégorie : Énergie et puissance

- Nombre de pages : 150

- Formats de rapport disponibles :

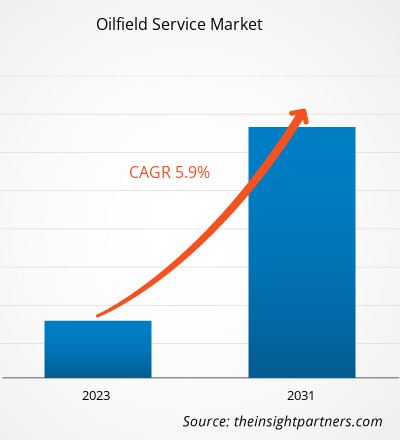

La taille du marché des services pétroliers devrait atteindre 175,96 milliards USD d'ici 2031, contre 111,56 milliards USD en 2023. Le marché devrait enregistrer un TCAC de 5,9 % au cours de la période 2023-2031. L'augmentation de la production de pétrole et de gaz, la hausse de la production de nouvelles plates-formes pétrolières et la reconstruction des plates-formes pétrolières et gazières existantes et anciennes devraient rester les principales tendances du marché.

Analyse du marché des services pétroliers

Le marché des services pétroliers devrait connaître une croissance considérable au cours de la période analysée en raison du nombre croissant de projets de gaz naturel ainsi que de la découverte de nouveaux champs pétrolifères, en particulier dans des endroits reculés. En outre, l'épuisement des réserves de pétrole et de gaz existantes dans divers pays a créé une demande de pipelines transfrontaliers pour l'approvisionnement en produits liés au pétrole et au gaz, ce qui stimule la croissance du marché des services pétroliers. La demande croissante de méthodes de transport rentables pour le pétrole et le gaz est l'un des principaux facteurs qui devraient stimuler la demande de services pétroliers dans le secteur pétrolier et gazier d'outre-mer à travers le monde.

Aperçu du marché des services pétroliers

Avec l'augmentation de la population et de l'industrialisation, la demande en énergie augmente également au niveau mondial. L'augmentation de la consommation d'énergie a également stimulé le besoin en pétrole et en gaz dans les économies en développement et développées. Cela a entraîné une augmentation de la demande de services pétroliers dans le monde entier. En outre, la grande population, le revenu par habitant élevé et l'industrialisation rapide stimulent le marché des raccords et brides de conduites pétrolières et gazières offshore en Asie-Pacifique. La région est le plus grand consommateur de pétrole brut et de gaz. En outre, les pays hautement industrialisés de l'Asie-Pacifique, notamment le Japon, la Chine, l'Inde et la Corée du Sud, signalent une augmentation de la consommation globale d'énergie. Ces pays se concentrent de plus en plus sur la stimulation de la production pétrolière nationale grâce à diverses techniques de récupération assistée du pétrole, ce qui soutient la croissance du marché de l'APAC pour répondre à la demande croissante de pétrole.

Personnalisez ce rapport en fonction de vos besoins

Vous bénéficierez d'une personnalisation gratuite de n'importe quel rapport, y compris de certaines parties de ce rapport, d'une analyse au niveau des pays, d'un pack de données Excel, ainsi que d'offres et de remises exceptionnelles pour les start-ups et les universités.

Marché des services pétroliers : perspectives stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Facteurs moteurs et opportunités du marché des services pétroliers

La demande croissante de gaz naturel et de pétrole brut favorise le marché

La demande de pétrole et de gaz naturel connaît une augmentation constante dans le monde entier. Les États-Unis et la Chine ont enregistré la croissance la plus importante. La forte augmentation de la demande de produits pétrochimiques aux États-Unis a entraîné une augmentation de la consommation. L'augmentation de la production industrielle, ainsi que la forte demande de services de transport par camion, stimulent la demande de produits pétrochimiques , alimentant ainsi la croissance du marché des services pétroliers. En outre, la croissance du trafic aérien dans le monde, en particulier dans les économies en développement d'Asie, est un autre facteur important entraînant une augmentation de la consommation de pétrole.

Efforts visant à améliorer les opérations de récupération du pétrole afin de réduire la dépendance aux importations de pétrole et de gaz

La méthode d'injection de vapeur a été exploitée commercialement au cours des dernières décennies pour améliorer la récupération des réservoirs de pétrole lourd conventionnels dans leurs derniers stades de développement. La vapeur injectée augmente la pression globale d'un réservoir de pétrole offshore, ce qui contribue à améliorer le taux de mobilité du pétrole brut et lui permet de s'écouler efficacement. En conséquence, les méthodes de récupération améliorée du pétrole aident à revitaliser les processus d'extraction dans les puits de pétrole offshore existants. Divers pays investissent dans des efforts pour rajeunir leurs ressources pétrolières existantes afin de stimuler la production nationale de pétrole et de réduire leur dépendance aux importations de pétrole. Ainsi, l'expansion prévue de leurs opérations pétrolières et gazières devrait offrir des opportunités de croissance prometteuses pour les acteurs du marché des services pétroliers dans les années à venir.

Analyse de segmentation du rapport sur le marché des services pétroliers

Les segments clés qui ont contribué à l’élaboration de l’analyse du marché des services pétroliers sont le type de service et l’application.

- En fonction du type de service, le marché des services pétroliers est divisé en complétion de puits, câblage, levage artificiel, perforation, fluides de forage et de complétion, et autres. Le segment des autres détenait la plus grande part de marché des services pétroliers en 2023.

- Par type de matériau, le marché est segmenté en onshore et offshore. Le segment onshore détenait la plus grande part du marché des services pétroliers en 2023.

Analyse des parts de marché des services pétroliers par zone géographique

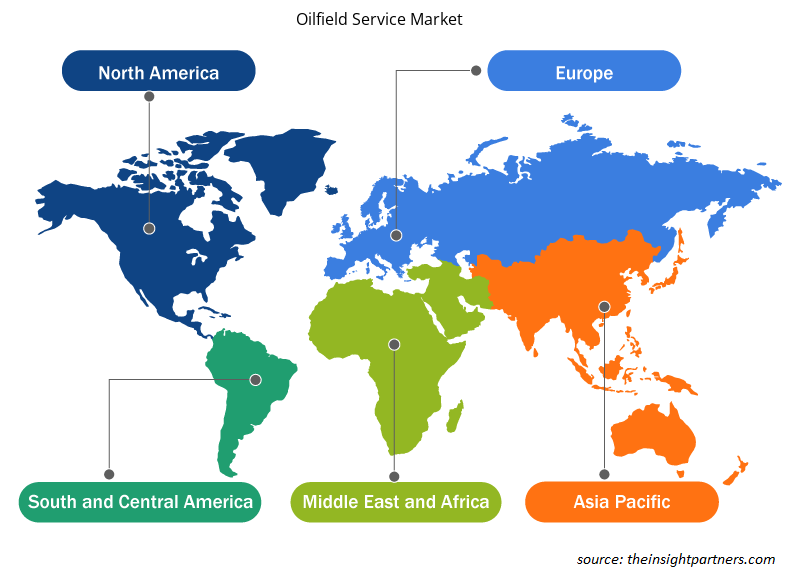

La portée géographique du rapport sur le marché des services pétroliers est principalement divisée en cinq régions : Amérique du Nord, Asie-Pacifique, Europe, Moyen-Orient et Afrique, et Amérique du Sud et centrale.

Le marché des services pétroliers en Amérique du Nord est sous-segmenté en États-Unis, Canada et Mexique. La région domine le marché mondial des services pétroliers en raison de vastes projets d'exploration et de production de pétrole et de gaz et d'une augmentation des nouvelles activités aux États-Unis, dans le golfe du Mexique et au Canada. Il y avait 912 962 puits de pétrole et de gaz aux États-Unis cette année-là. Une augmentation du nombre de puits horizontaux aux États-Unis et une augmentation de la production de pétrole et de gaz de schiste par plate-forme contribuent à la croissance du marché des services pétroliers dans le pays. L'émergence de systèmes de services pétroliers intelligents avancés, tels que les systèmes de contrôle d'entrée auto-adaptatifs haut de gamme, propulserait la croissance du marché en Amérique du Nord dans les années à venir. La forte demande d'équipements terrestres en raison des perspectives importantes dans le bassin permien et le Dakota du Nord, en particulier dans un nombre de plus en plus important de projets non conventionnels, stimulerait la croissance du marché des services pétroliers pour le segment terrestre.

Aperçu régional du marché des services pétroliers

Les tendances et facteurs régionaux influençant le marché des services pétroliers tout au long de la période de prévision ont été expliqués en détail par les analystes d'Insight Partners. Cette section traite également des segments et de la géographie du marché des services pétroliers en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et en Amérique centrale.

- Obtenez les données régionales spécifiques au marché des services pétroliers

Portée du rapport sur le marché des services pétroliers

| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2023 | 111,56 milliards de dollars américains |

| Taille du marché d'ici 2031 | 175,96 milliards de dollars américains |

| Taux de croissance annuel composé mondial (2023-2031) | 5,9% |

| Données historiques | 2021-2022 |

| Période de prévision | 2023-2031 |

| Segments couverts |

Par type de service

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché : comprendre son impact sur la dynamique des entreprises

Le marché des services pétroliers connaît une croissance rapide, tirée par la demande croissante des utilisateurs finaux en raison de facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une plus grande sensibilisation aux avantages du produit. À mesure que la demande augmente, les entreprises élargissent leurs offres, innovent pour répondre aux besoins des consommateurs et capitalisent sur les tendances émergentes, ce qui alimente davantage la croissance du marché.

La densité des acteurs du marché fait référence à la répartition des entreprises ou des sociétés opérant sur un marché ou un secteur particulier. Elle indique le nombre de concurrents (acteurs du marché) présents sur un marché donné par rapport à sa taille ou à sa valeur marchande totale.

Les principales entreprises opérant sur le marché des services pétroliers sont :

- Schlumberger Limitée

- Weatherford International Plc

- La société Baker Hughes

- Société Halliburton

- National Oilwell Varco, Inc.

- TechnipFMC

Avis de non-responsabilité : les sociétés répertoriées ci-dessus ne sont pas classées dans un ordre particulier.

- Obtenez un aperçu des principaux acteurs du marché des services pétroliers

Actualités et développements récents du marché des services pétroliers

Le marché des services pétroliers est évalué en collectant des données qualitatives et quantitatives issues de recherches primaires et secondaires, qui comprennent d'importantes publications d'entreprises, des données d'associations et des bases de données. Quelques-uns des développements sur le marché des services pétroliers sont énumérés ci-dessous :

- Baker Hughes a annoncé l'expansion de son activité de services et d'équipements pour champs pétrolifères en Guyane. Baker Hughes est prêt à développer un nouveau supercentre en Guyane pour les services et équipements pour champs pétrolifères. (Source : Baker Hughes, communiqué de presse, février 2022)

- Schlumberger Limited a annoncé le lancement du service de cartographie multicouche en cours de forage Periscope Edge. Le service fournit de nouvelles mesures et un processus d'inversion de pointe combiné à des solutions cloud pour fournir un pilotage géographique précis dans les réservoirs pendant le forage. (Source : Schlumberger Limited, communiqué de presse, août 2021)

Rapport sur le marché des services pétroliers : couverture et livrables

Le rapport « Taille et prévisions du marché des services pétroliers (2021-2031) » fournit une analyse détaillée du marché couvrant les domaines ci-dessous :

- Taille et prévisions du marché des services pétroliers aux niveaux mondial, régional et national pour tous les segments de marché clés couverts par le périmètre

- Tendances du marché des services pétroliers ainsi que dynamique du marché telles que les facteurs moteurs, les contraintes et les opportunités clés

- Analyse PEST et SWOT détaillée

- Analyse du marché des services pétroliers couvrant les principales tendances du marché, le cadre mondial et régional, les principaux acteurs, les réglementations et les développements récents du marché

- Analyse du paysage industriel et de la concurrence couvrant la concentration du marché, l'analyse de la carte thermique, les principaux acteurs et les développements récents du marché des services pétroliers

- Profils d'entreprise détaillés

Nivedita est un expert en recherche versierte mit über 9 Jahren Erfahrung in Marktforschung und Unternehmensberatung. Vous êtes à la recherche d'un gestionnaire de projet dans l'agence IKT de The Insight Partners qui s'occupe et s'occupe des connaissances générales dans le cadre de la lecture et de la formation des syndicats, des spécialistes, des abonnements et des programmes de formation en sous-traitance. Technologiesektoren.

Mit einer nachgewiesenen Erfolgsbilanz bei der Bereitstellung datengestützter Analysen and umsetzbarer Erkenntnisse war Nivedita maßgeblich an mehreren kritischen Projekten beteiligt. Ihre Arbeit umfasst die vollständige Projektabwicklung – vom Verständnis der Kundenziele über die Analyse von Markttrends bis hin zur Ableitung strategischer Empfehlungen. Vous avez participé à des études de formation d'entreprises IKT et à vos études de marché, ainsi qu'à des services de branche pour mes clients.

Nivedita a un MBA en gestion de l'IMS, Dehradun. Pour votre travail chez The Insight Partners, nous avons travaillé ensemble sur MarketsandMarkets et Future Market Insights à Pune, nous avons des positions de recherche approfondies et un fondement solide dans l'analyse des branches et l'élaboration des liens.

- Analyse historique (2 ans), année de base, prévision (7 ans) avec TCAC

- Analyse PEST et SWOT

- Taille du marché Valeur / Volume - Mondial, Régional, Pays

- Industrie et paysage concurrentiel

- Ensemble de données Excel

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires

Débloquez des remises exclusives sur les rapports

Demander maintenant

Obtenez un échantillon gratuit pour - Marché des services pétroliers

Obtenez un échantillon gratuit pour - Marché des services pétroliers