Analisi e previsioni del mercato della patologia anatomica per dimensione, quota, crescita, tendenze 2031

Rapporto di analisi su dimensioni e previsioni del mercato dell'anatomia patologica (2021-2031), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per prodotto e servizi [servizi (istopatologia e citopatologia), strumenti (microtomi e criostati, coloratori automatici, processori di tessuti e altri) e materiali di consumo], applicazione (diagnosi di malattie, scoperta e sviluppo di farmaci e altri), utente finale (ospedali, laboratori di ricerca, laboratori diagnostici e altri) e area geografica (Nord America, Europa, Asia Pacifico, Sud e Centro America e Medio Oriente e Africa)

- Stato : Edito

- Codice del report : TIPRE00002999

- Categoria : Scienze della vita

- Numero di pagine : 178

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : August 28, 2024

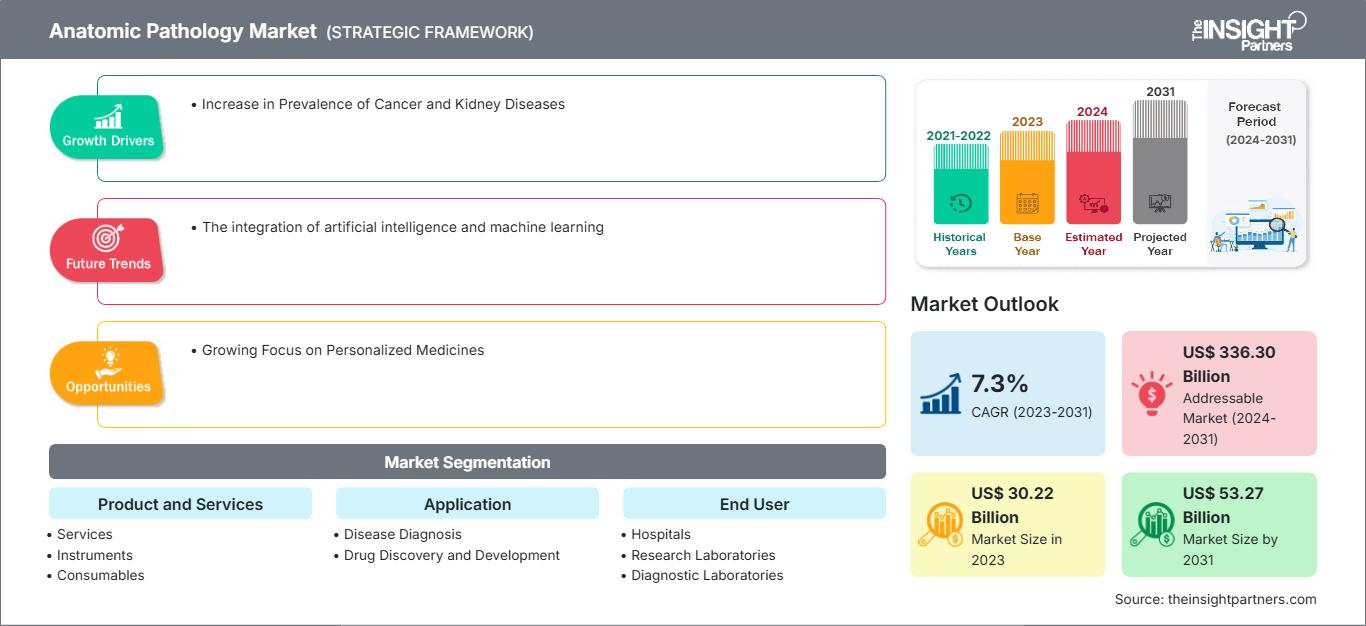

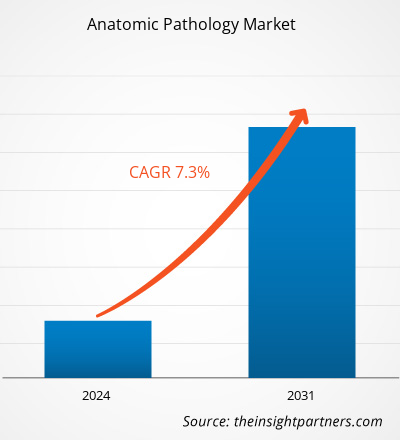

Si prevede che il mercato dell'anatomia patologica raggiungerà i 53,27 miliardi di dollari entro il 2031, rispetto ai 30,22 miliardi di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 7,3% tra il 2023 e il 2031. L'integrazione dell'intelligenza artificiale e dell'apprendimento automatico sarà probabilmente una tendenza futura del mercato.

Analisi del mercato dell'anatomia patologica

Le innovazioni nelle tecniche diagnostiche, tra cui patologia digitale, diagnostica molecolare e tecnologie di imaging, migliorano l'accuratezza e l'efficienza dei servizi di patologia, stimolando la crescita del mercato dell'anatomia patologica. L'invecchiamento della popolazione è più suscettibile a diverse malattie, con conseguente aumento della domanda di servizi di patologia per una diagnosi accurata e una pianificazione del trattamento. Inoltre, una maggiore consapevolezza sui problemi di salute, solidi programmi di screening che contribuiscono alla diagnosi precoce, quadri normativi di supporto e politiche di rimborso favorevoli stanno alimentando la crescita del mercato dell'anatomia patologica.

Panoramica del mercato dell'anatomia patologica

Si prevede che l'India registrerà il CAGR più elevato nel mercato complessivo. Il rapporto 2020 del National Cancer Registry Programme prevedeva che i casi di cancro in India avrebbero raggiunto i 14,61 milioni nel 2022. Il rapporto affermava inoltre che si stima che l'incidenza del cancro aumenterà del 12,8% entro il 2025 rispetto al 2020. Con la crescente prevalenza del cancro e i progressi nelle infrastrutture sanitarie, le autorità governative indiane si stanno concentrando sull'offrire alle persone un accesso più ampio alle soluzioni sanitarie. Secondo i dati del Dipartimento per la Promozione dell'Industria e del Commercio Interno (DPIIT), l'afflusso di investimenti diretti esteri (IDE) nel settore farmaceutico e farmaceutico ha raggiunto i 17,74 miliardi di dollari USA da aprile 2000 a dicembre 2020. Inoltre, aziende, organizzazioni, governi, ecc., investono in modo significativo in servizi diagnostici e strutture diagnostiche moderne. Pertanto, tali investimenti nel settore sanitario sostengono la crescita del mercato dell'anatomia patologica in India.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dell'anatomia patologica: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità di mercato dell'anatomia patologica

Aumento della prevalenza di cancro e malattie renali

L'anatomia patologica è utile per identificare anomalie che possono aiutare a diagnosticare malattie, come malattie autoimmuni, malattie renali ed epatiche e cancro. L'istopatologia, che consiste nello studio delle alterazioni tissutali causate da malattie, è una parte fondamentale dell'anatomia patologica. Il cancro ha un impatto significativo sulla società in tutto il mondo. Il peso del cancro sui sistemi sanitari sta aumentando significativamente in tutto il mondo, essendo tra le principali cause di morte. L'Organizzazione Mondiale della Sanità (OMS) classifica il cancro come la seconda causa di mortalità a livello mondiale. Secondo i dati pubblicati dal World Cancer Research Fund International, nel 2022 sono stati registrati circa 20 milioni di nuovi casi di cancro a livello globale. Inoltre, secondo i dati pubblicati dall'Organizzazione Mondiale della Sanità (OMS), nel 2020 quasi 10 milioni di decessi in tutto il mondo sono stati causati dal cancro. I dati del National Center for Health Statistics stimano che la diagnosi di nuovi casi di cancro negli Stati Uniti raggiungerà probabilmente i 2 milioni nel 2024. Inoltre, circa 0,61 milioni di persone potrebbero morire di cancro nel 2024 negli Stati Uniti. Secondo i dati pubblicati da Macmillan Cancer Support, ogni anno nel Regno Unito circa 392.000 persone ricevono una diagnosi di cancro, mentre circa 167.000 muoiono a causa della malattia.

La prevalenza della malattia renale cronica è in aumento a causa dell'aumento della popolazione geriatrica. Secondo i Centers for Disease Control and Prevention, nel 2023 circa 35,5 milioni di persone negli Stati Uniti soffrivano di malattie renali croniche. La biopsia, una tecnica di anatomia patologica, viene utilizzata per la diagnosi di cancro e malattia renale cronica. A causa della crescente prevalenza di cancro e malattie renali, agenzie governative, operatori sanitari e istituzioni sono costretti a contribuire a iniziative di diagnosi e trattamento delle malattie. Pertanto, un aumento della prevalenza di cancro e di altre malattie mirate, come le malattie autoimmuni e le malattie renali ed epatiche, sta trainando la crescita del mercato globale dell'anatomia patologica.

Crescente attenzione alla medicina personalizzata per offrire opportunità di mercato

La medicina personalizzata è progettata principalmente tenendo conto del profilo genetico individuale per orientare le decisioni relative alla prevenzione, alla diagnosi e al trattamento di una malattia. Offre alle aziende farmaceutiche l'opportunità di sviluppare agenti mirati a gruppi di pazienti che non rispondono ai farmaci come previsto o che non rispondono come previsto alle pratiche sanitarie tradizionali. Numerose prove indicano che una parte sostanziale della variabilità nella risposta ai farmaci dipende da fattori geneticamente controllati, tra cui età, nutrizione, esposizione ambientale e stato di salute. La genomica svolge un ruolo importante nell'emergere della medicina personalizzata, poiché la conoscenza del profilo genetico di un paziente aiuterebbe i medici a selezionare il farmaco più adatto. La medicina personalizzata contribuisce a migliorare l'assistenza sanitaria consentendo a ciascun paziente di ricevere diagnosi precoci, valutazioni del rischio e trattamenti ottimali.

I patologi svolgono un ruolo importante nello sviluppo e nell'implementazione di test molecolari e genomici nella pratica clinica. La medicina personalizzata è utilizzata nel trattamento di malattie come il cancro al seno e le malattie cardiovascolari. I farmaci antitumorali personalizzati presentano effetti collaterali minori e meno gravi rispetto ad altri tipi di trattamento, poiché sono progettati per un'azione più specifica. Inoltre, con i continui progressi nella ricerca e negli studi clinici, è probabile che la medicina personalizzata raggiunga un potenziale ancora maggiore per migliorare la qualità dell'assistenza ai pazienti. Pertanto, si prevede che la crescente attenzione alla medicina personalizzata stimolerà la crescita del mercato dell'anatomia patologica.

Analisi della segmentazione del rapporto sul mercato dell'anatomia patologica

I segmenti chiave che hanno contribuito all'analisi del mercato dell'anatomia patologica sono prodotti e servizi, applicazioni e utenti finali.

- In base a prodotti e servizi, il mercato dell'anatomia patologica è segmentato in strumenti, materiali di consumo e servizi. Il segmento dei servizi è ulteriormente suddiviso in istopatologia e citopatologia. Il segmento degli strumenti è ulteriormente suddiviso in microtomi e criostati, coloratori automatici, processatori di tessuti e altri. Il segmento degli strumenti ha detenuto la quota di mercato maggiore nel 2023.

- In base all'applicazione, il mercato è segmentato in diagnosi di malattie, scoperta e sviluppo di farmaci e altri. Il segmento della diagnosi di malattie ha detenuto la quota di mercato maggiore nel 2023.

- In base all'utente finale, il mercato dell'anatomia patologica è suddiviso in ospedali, laboratori di ricerca, laboratori diagnostici e altri. Il segmento ospedaliero ha detenuto la quota di mercato maggiore nel 2023.

Analisi della quota di mercato dell'anatomia patologica per area geografica

L'ambito geografico del rapporto sul mercato dell'anatomia patologica è suddiviso principalmente in cinque regioni: Nord America, Asia-Pacifico, Europa, America meridionale e centrale e Medio Oriente e Africa. Il Nord America ha dominato il mercato nel 2023. La crescita del mercato in questa regione è attribuita alla crescente prevalenza del cancro, alle crescenti iniziative governative per lo screening dei pazienti oncologici, alla crescente attenzione per una diagnosi efficiente delle malattie e alla crescente necessità di sistemi sanitari avanzati. Inoltre, i maggiori sforzi di ricerca e sviluppo intrapresi dagli operatori del mercato, insieme al lancio di prodotti, guideranno probabilmente la crescita del mercato dell'anatomia patologica in Nord America durante il periodo di previsione. Gli operatori che operano nel mercato statunitense dell'anatomia patologica si concentrano costantemente sullo sviluppo di strumenti e materiali di consumo innovativi e pratici per le procedure patologiche. Nel novembre 2023, Illumina Inc., Stati Uniti, leader mondiale nel sequenziamento del DNA e nelle tecnologie basate su array, ha introdotto TruSight Oncology 500 ctDNA v2 (numero di piastra 1 ctDNA v2), una nuova versione del suo test di biopsia liquida distribuita che consente una profilazione genomica non invasiva completa del DNA tumorale circolante dal sangue, integrando i test basati sui tessuti. Si prevede che l'area Asia-Pacifico registrerà il CAGR più elevato durante il periodo di previsione.

Approfondimenti regionali sul mercato dell'anatomia patologica

Le tendenze regionali e i fattori che influenzano il mercato dell'anatomia patologica durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato dell'anatomia patologica in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America meridionale e centrale.

Ambito del rapporto di mercato sull'anatomia patologica

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2023 | US$ 30.22 Billion |

| Dimensioni del mercato per 2031 | US$ 53.27 Billion |

| CAGR globale (2023 - 2031) | 7.3% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

By Prodotti e servizi

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato dell'anatomia patologica: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dell'anatomia patologica è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato dell'anatomia patologica Panoramica dei principali attori chiave

Notizie e sviluppi recenti sul mercato dell'anatomia patologica

Il mercato dell'anatomia patologica viene valutato raccogliendo dati qualitativi e quantitativi a seguito di ricerche primarie e secondarie, che includono importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi del mercato:

- Agilent Technologies Inc. ha stretto una partnership con Hamamatsu Photonics KK, fornitore leader di sistemi di imaging per vetrini interi. La collaborazione ha comportato l'integrazione della gamma NanoZoomer di Hamamatsu, incluso il sistema di scansione per vetrini S360MD, nella soluzione di patologia digitale di Agilent. L'aggiunta dei sistemi di scansione per vetrini NanoZoomer, che convertono i vetrini in dati digitali ad alta risoluzione tramite scansione ad alta velocità, ha completato l'offerta di Agilent di un flusso di lavoro di patologia digitale aperto e agnostico, volto ad accelerare le innovazioni nella medicina di precisione. (Fonte: Agilent Technologies Inc., sito web aziendale, marzo 2023)

- Epredia, una sussidiaria di PHC Corporation, e NovaScan, Inc., un'azienda che sviluppa tecnologie innovative per la rilevazione e la stratificazione del cancro, hanno annunciato la firma di una lettera di intenti per un accordo di distribuzione commerciale esclusiva negli Stati Uniti per MarginScan, un dispositivo medico che supporterà i medici nella rilevazione in tempo reale del tumore della pelle non melanoma. Epredia ha incaricato Avantik, un'azienda specializzata nel supporto ai laboratori diagnostici nelle loro attività, di fornire questo nuovo dispositivo ai chirurghi Mohs. (Fonte: PHC Corporation, sito web aziendale, maggio 2024)

Copertura e risultati del rapporto sul mercato dell'anatomia patologica

Il rapporto "Dimensioni e previsioni del mercato dell'anatomia patologica (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato dell'anatomia patologica a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato dell'anatomia patologica, nonché dinamiche di mercato come fattori trainanti, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi del mercato dell'anatomia patologica che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e i recenti sviluppi per il mercato dell'anatomia patologica

- Profili aziendali dettagliati

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative