Analyse et prévisions du marché de la pathologie anatomique par taille, part, croissance et tendances 2031

Analyse de la taille et des prévisions du marché de l'anatomopathologie (2021-2031), des parts mondiales et régionales, des tendances et des opportunités de croissance. Couverture du rapport : par produit et service (services (histopathologie et cytopathologie), instruments (microtomes et cryostat, colorateurs automatiques, processeurs de tissus et autres) et consommables), application (diagnostic des maladies, découverte et développement de médicaments et autres), utilisateur final (hôpitaux, laboratoires de recherche, laboratoires de diagnostic et autres) et zone géographique (Amérique du Nord, Europe, Asie-Pacifique, Amérique du Sud et centrale, et Moyen-Orient et Afrique).

- Statut : Publié

- Code du rapport : TIPRE00002999

- Catégorie : Sciences de la vie

- Nombre de pages : 178

- Formats de rapport disponibles :

- Date de dernière mise à jour : August 28, 2024

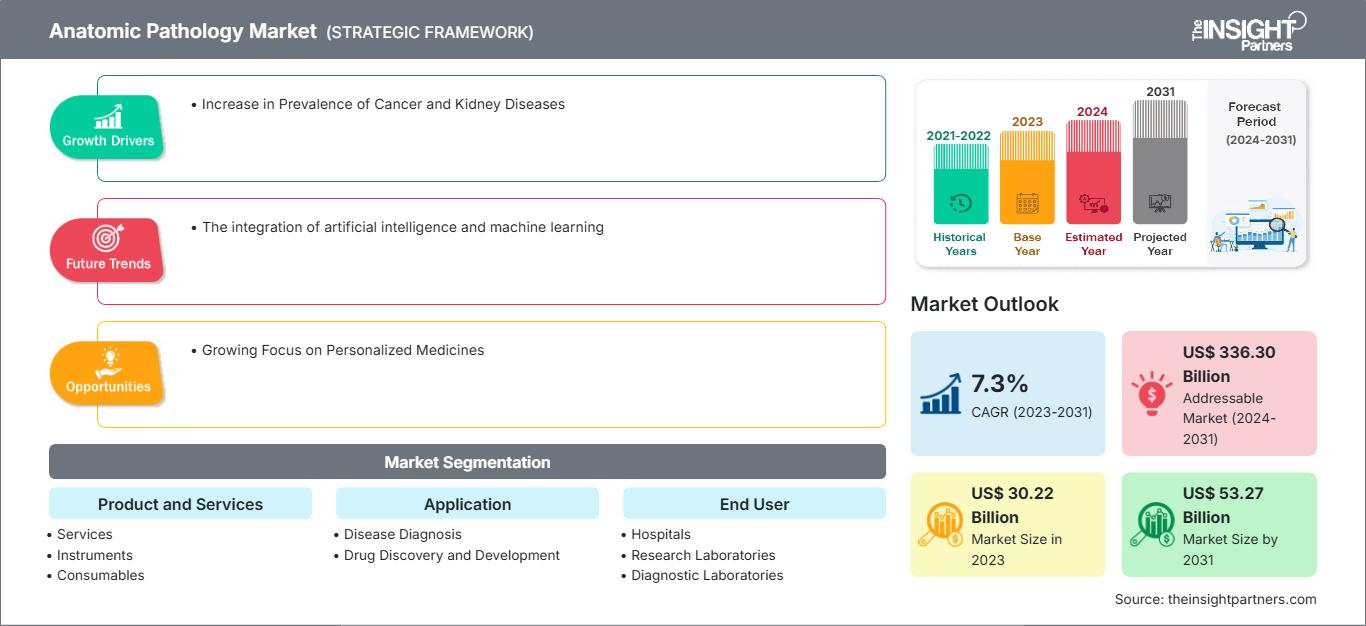

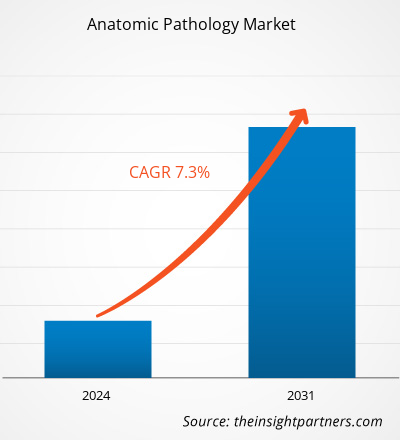

Le marché de la pathologie anatomique devrait atteindre 53,27 milliards de dollars américains d'ici 2031, contre 30,22 milliards de dollars américains en 2023. Le marché devrait enregistrer un TCAC de 7,3 % entre 2023 et 2031. L'intégration de l'intelligence artificielle et de l'apprentissage automatique devrait constituer une tendance future sur le marché.

Analyse du marché de la pathologie anatomique

Les innovations dans les techniques de diagnostic, notamment la pathologie numérique, les diagnostics moléculaires et les technologies d'imagerie, améliorent la précision et l'efficacité des services de pathologie, propulsant ainsi la croissance du marché de la pathologie anatomique. Une population vieillissante est plus sensible à diverses maladies, ce qui entraîne une demande accrue de services de pathologie pour un diagnostic et une planification des traitements précis. Français De plus, une sensibilisation accrue aux problèmes de santé, des programmes de dépistage robustes contribuant à un diagnostic précoce, des cadres réglementaires favorables et des politiques de remboursement favorables alimentent la croissance du marché de l'anatomopathologie.

Aperçu du marché de l'anatomopathologie

L'Inde devrait enregistrer le TCAC le plus élevé du marché global. Le rapport 2020 du programme national d'enregistrement du cancer prévoit que les cas de cancer en Inde atteindront 14,61 millions en 2022. Le rapport indique également que l'incidence du cancer devrait augmenter de 12,8 % d'ici 2025 par rapport à 2020. Avec la prévalence croissante du cancer et les progrès des infrastructures de santé, les autorités gouvernementales indiennes s'efforcent d'offrir à la population un accès étendu aux solutions de santé. Selon les données du Département de la promotion de l'industrie et du commerce intérieur (DPIIT), les investissements directs étrangers (IDE) dans l'industrie pharmaceutique ont totalisé 17,74 milliards de dollars américains entre avril 2000 et décembre 2020. De plus, les entreprises, les organisations et les gouvernements, entre autres, investissent massivement dans les services et les installations de diagnostic modernes. Ainsi, ces investissements dans le secteur de la santé soutiennent la croissance du marché de l'anatomopathologie en Inde.

Vous bénéficierez d’une personnalisation sur n’importe quel rapport - gratuitement - y compris des parties de ce rapport, ou une analyse au niveau du pays, un pack de données Excel, ainsi que de profiter d’offres exceptionnelles et de réductions pour les start-ups et les universités

Marché de l'anatomopathologie: Perspectives stratégiques

-

Obtenez les principales tendances clés du marché de ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Moteurs et opportunités du marché de l'anatomopathologie

Augmentation de la prévalence du cancer et des maladies rénales

L'anatomopathologie est utile pour identifier les anomalies qui peuvent aider à diagnostiquer des maladies, telles que les maladies auto-immunes, les maladies rénales et hépatiques, et le cancer. L'histopathologie, qui consiste à étudier les modifications tissulaires causées par les maladies, est un élément essentiel de l'anatomopathologie. Le cancer a un impact majeur sur la société dans le monde entier. Le fardeau du cancer sur les systèmes de santé augmente considérablement dans le monde entier, car il est l'une des principales causes de décès. L'Organisation mondiale de la santé (OMS) classe le cancer comme la deuxième cause de mortalité dans le monde. Selon les données publiées par le World Cancer Research Fund International, environ 20 millions de nouveaux cas de cancer ont été enregistrés en 2022 dans le monde. Français De plus, selon les données publiées par l'Organisation mondiale de la santé (OMS), près de 10 millions de décès dans le monde ont été causés par le cancer en 2020. Les données du Centre national des statistiques de la santé estiment que le diagnostic de nouveaux cas de cancer aux États-Unis devrait atteindre 2 millions en 2024. De plus, environ 0,61 million de personnes devraient mourir en 2024 aux États-Unis des suites d'un cancer. Selon les données publiées par Macmillan Cancer Support, environ 392 000 personnes au Royaume-Uni reçoivent un diagnostic de cancer chaque année, tandis qu'environ 167 000 personnes en meurent chaque année.

La prévalence de l'insuffisance rénale chronique augmente en raison de l'augmentation de la population gériatrique. Selon les Centres pour le contrôle et la prévention des maladies, en 2023, environ 35,5 millions de personnes aux États-Unis souffraient d'insuffisance rénale chronique. La biopsie, une technique d'anatomopathologie, est utilisée pour la détection du cancer et de l'insuffisance rénale chronique. En raison de la prévalence croissante du cancer et des maladies rénales, les agences gouvernementales, les prestataires de soins de santé et les institutions sont contraints de contribuer aux initiatives de diagnostic et de traitement des maladies. Ainsi, l'augmentation de la prévalence du cancer et d'autres maladies ciblées, telles que les maladies auto-immunes, rénales et hépatiques, stimule la croissance du marché mondial de l'anatomopathologie.

L'intérêt croissant pour les médicaments personnalisés offre des opportunités de marché

Les médicaments personnalisés sont principalement conçus en tenant compte du profil génétique des individus afin d'orienter les décisions en matière de prévention, de diagnostic et de traitement d'une maladie. Ils offrent aux fabricants de médicaments l'opportunité de développer des agents ciblant les groupes de patients qui ne répondent pas aux médicaments comme prévu ou qui ne répondent pas comme prévu aux pratiques de santé traditionnelles. De nombreuses données indiquent qu'une part importante de la variabilité de la réponse aux médicaments dépend de facteurs génétiquement contrôlés, notamment l'âge, la nutrition, l'exposition environnementale et l'état de santé. La génomique joue un rôle important dans l'émergence des médicaments personnalisés, car la connaissance du profil génétique d'un patient aiderait les médecins à choisir le médicament le plus adapté. Les médicaments personnalisés contribuent à améliorer les soins de santé en permettant à chaque patient de bénéficier d'un diagnostic plus précoce, d'une évaluation des risques et de traitements optimaux.

Les pathologistes jouent un rôle important dans le développement et la mise en œuvre de tests moléculaires et génomiques. Les médicaments personnalisés sont utilisés dans le traitement de maladies telles que le cancer du sein et les maladies cardiovasculaires. Les médicaments anticancéreux personnalisés présentent moins d'effets secondaires et moins graves que les autres types de traitement, car ils sont conçus pour une action plus spécifique. De plus, grâce aux progrès constants de la recherche et des études cliniques, les médicaments personnalisés sont susceptibles d'atteindre un potentiel encore plus important pour améliorer la qualité des soins aux patients. Ainsi, l'intérêt croissant pour les médicaments personnalisés devrait stimuler la croissance du marché de l'anatomopathologie.

Analyse de segmentation du rapport sur le marché de l'anatomopathologie

Les principaux segments ayant contribué à l'élaboration de l'analyse du marché de l'anatomopathologie sont les produits et services, les applications et l'utilisateur final.

- Sur la base des produits et services, le marché de l'anatomopathologie est segmenté en instruments, consommables et services. Le segment des services est subdivisé en histopathologie et cytopathologie. Le segment des instruments est lui-même subdivisé en microtomes et cryostats, colorateurs automatiques, processeurs de tissus, etc. Le segment des instruments détenait la plus grande part de marché en 2023.

- Par application, le marché est segmenté en diagnostic des maladies, découverte et développement de médicaments, etc. Le segment du diagnostic des maladies détenait la plus grande part de marché en 2023.

- En fonction de l'utilisateur final, le marché de l'anatomopathologie est divisé en hôpitaux, laboratoires de recherche, laboratoires de diagnostic, etc. Le segment des hôpitaux détenait la plus grande part de marché en 2023.

Analyse des parts de marché de l'anatomopathologie par zone géographique

La portée géographique du rapport sur le marché de l'anatomopathologie est principalement divisée en cinq régions : Amérique du Nord, Asie-Pacifique, Europe, Amérique du Sud et centrale, et Moyen-Orient et Afrique. L'Amérique du Nord a dominé le marché en 2023. La croissance du marché dans cette région est attribuée à la prévalence croissante du cancer, à l'intensification des initiatives gouvernementales en matière de dépistage des patients atteints de cancer, à l'importance croissante accordée à un diagnostic efficace des maladies et au besoin croissant de systèmes de santé avancés. De plus, les efforts accrus de recherche et développement déployés par les acteurs du marché, associés aux lancements de produits, devraient stimuler la croissance du marché de l'anatomopathologie en Amérique du Nord au cours de la période de prévision. Les acteurs opérant sur le marché américain de l'anatomopathologie se concentrent en permanence sur le développement d'instruments et de consommables innovants et pratiques pour les procédures pathologiques. En novembre 2023, Illumina Inc., États-Unis, leader mondial du séquençage de l'ADN et des technologies basées sur les puces, a lancé TruSight Oncology 500 ctDNA v2 (plaque numéro 1 ctDNA v2), une nouvelle version de son test de biopsie liquide distribuée qui permet un profilage génomique non invasif complet de l'ADN tumoral circulant à partir du sang, en complément des tests tissulaires. L'Asie-Pacifique devrait enregistrer le TCAC le plus élevé au cours de la période de prévision.

Aperçu régional du marché de l'anatomopathologie

Les tendances régionales et les facteurs influençant le marché de l'anatomopathologie tout au long de la période de prévision ont été analysés en détail par les analystes de The Insight Partners. Cette section aborde également les segments et la géographie du marché de l'anatomopathologie en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et en Amérique centrale.

Portée du rapport sur le marché de la pathologie anatomique

| Attribut de rapport | Détails |

|---|---|

| Taille du marché en 2023 | US$ 30.22 Billion |

| Taille du marché par 2031 | US$ 53.27 Billion |

| TCAC mondial (2023 - 2031) | 7.3% |

| Données historiques | 2021-2022 |

| Période de prévision | 2024-2031 |

| Segments couverts |

By Produits et services

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché de l'anatomopathologie : comprendre son impact sur la dynamique des entreprises

Le marché de l'anatomopathologie connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux, due à des facteurs tels que l'évolution des préférences des consommateurs, les avancées technologiques et une meilleure connaissance des avantages du produit. Face à cette demande croissante, les entreprises élargissent leur offre, innovent pour répondre aux besoins des consommateurs et capitalisent sur les nouvelles tendances, ce qui alimente la croissance du marché.

- Obtenez le Marché de l'anatomopathologie Aperçu des principaux acteurs clés

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires