Rapporto sul mercato Carrello di atterraggio per elicotteri 2031 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Rapporto di analisi sulle dimensioni e le previsioni del mercato dei carrelli di atterraggio per elicotteri (2021-2031), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per tipo (pattini e ruote), materiale (set di carrelli di atterraggio in alluminio, set di carrelli di atterraggio in acciaio, set di carrelli di atterraggio in composito e titanio), applicazione (elicottero civile ed elicottero militare) e geografia.

- Stato : Dati rilasciati

- Codice del report : TIPRE00019420

- Categoria : Aerospaziale e difesa

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : February 15, 2025

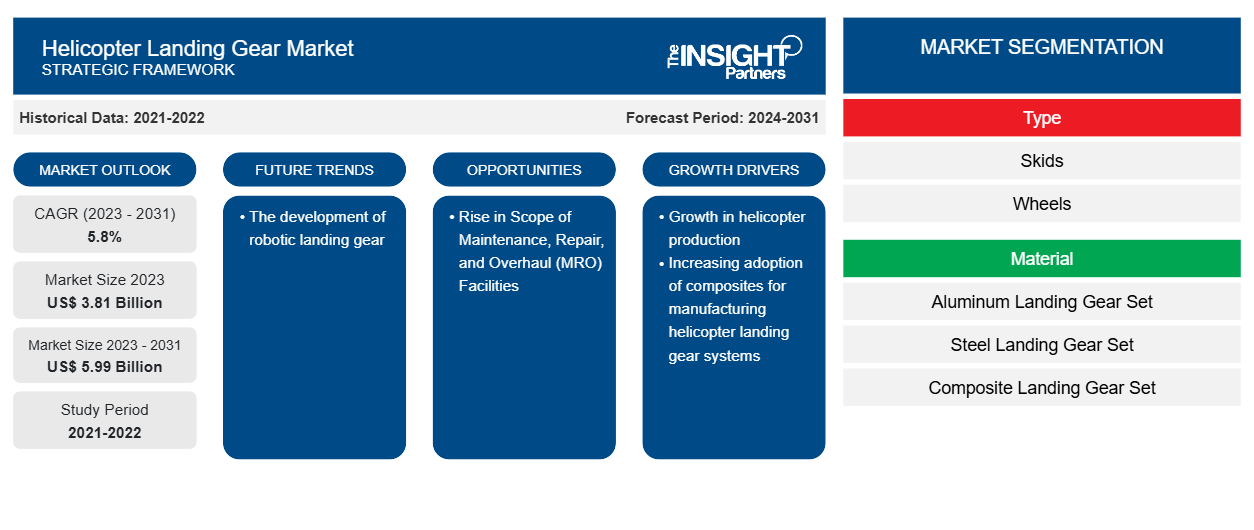

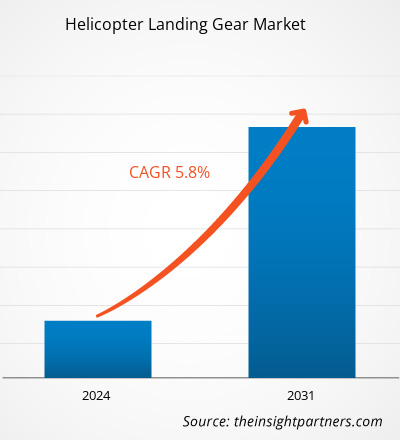

Si prevede che la dimensione del mercato dei carrelli di atterraggio per elicotteri raggiungerà i 5,99 miliardi di dollari entro il 2031, rispetto ai 3,81 miliardi di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 5,8% nel periodo 2023-2031. È probabile che lo sviluppo di carrelli di atterraggio robotizzati rimanga una tendenza chiave nel mercato.

Analisi del mercato del carrello di atterraggio per elicotteri

L'industria globale di produzione o retrofitting di elicotteri è caratterizzata dalla presenza di produttori di elicotteri noti e finanziariamente forti come Airbus e Bell Helicopter. Per questo motivo, il potere contrattuale degli acquirenti nel mercato dei carrelli di atterraggio per elicotteri è piuttosto elevato al momento, tuttavia, si stima che il potere contrattuale degli acquirenti si ridurrà a un livello moderato nei prossimi anni. Le aziende produttrici di elicotteri come Airbus, Bell Helicopters, Sikorsky Aircraft Corporation tra le altre hanno una forte rivalità competitiva tra loro e richiedono un miglioramento costante dei loro velivoli per mantenere la loro roccaforte nel mercato. Per questo motivo, queste aziende hanno un'elevata tendenza a cambiare appaltatori di componenti per elicotteri nel corso del tempo, al fine di migliorare l'intero sistema dell'elicottero. Quindi, a causa della natura consolidata dell'industria manifatturiera di elicotteri con la presenza di pochi grandi produttori di elicotteri, si prevede che il potere contrattuale degli acquirenti rimarrà elevato nei prossimi anni.

Panoramica del mercato dei carrelli di atterraggio per elicotteri

Il mercato dei carrelli di atterraggio per elicotteri è costituito da un gran numero di aziende affermate e riconosciute come Safran SA, Liebherr Group, Héroux-Devtek Inc., Circor International, Inc. e Triumph Group Inc. tra molte altre. Questi attori del mercato hanno una posizione di marchio consolidata e una presenza a lungo termine nel mercato globale dei carrelli di atterraggio. I produttori di elicotteri fanno molto affidamento sul valore del marchio dei produttori di componenti per elicotteri e, per questo motivo, la maggior parte dei contatti viene assegnata ai produttori di carrelli di atterraggio per elicotteri affermati e riconosciuti dal settore, creando così uno spazio minimo per l'ingresso di nuovi produttori nel mercato. Oltre a ciò, gli investimenti di capitale iniziali necessari per entrare nel mercato dei carrelli di atterraggio per elicotteri sono piuttosto elevati, il che funge da barriera all'ingresso per i nuovi entranti.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato del carrello di atterraggio per elicotteri: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato dei carrelli di atterraggio per elicotteri

Aumento della produzione globale di elicotteri

L'aumento del numero di elicotteri prodotti e consegnati in tutto il mondo è uno dei principali fattori che supportano l'adozione di carrelli di atterraggio per elicotteri civili e militari in diverse regioni del mondo. Ad esempio, secondo la General Aviation Manufacturers Association (GAMA), nel 2022 sono stati consegnati circa 1072 elicotteri civili rispetto ai 1007 elicotteri del 2021. Inoltre, secondo GAMA, le consegne di elicotteri a pistoni hanno registrato una crescita di circa il 7,7% nel 2023 con 209 unità consegnate in tutto il mondo; mentre gli elicotteri a turbina civili-commerciali hanno registrato un aumento di circa il 9,9% con 811 unità nel 2023. Tale crescita nelle consegne e nella produzione di elicotteri sta guidando la crescita del mercato dei carrelli di atterraggio per elicotteri in tutto il mondo.

Aumento della portata delle strutture di manutenzione, riparazione e revisione (MRO)

La crescita esponenziale degli elicotteri ha completato la creazione di strutture MRO nel mondo nel corso degli anni. Si prevede che la portata delle strutture MRO aumenterà in diverse parti del mondo, soprattutto in Asia. Grazie alla crescente adozione di elicotteri civili per vari scopi commerciali come la lotta agli incendi, la facilitazione della copertura di notizie e traffico, la conduzione di missioni di ricerca e soccorso e il pattugliamento di gasdotti e oleodotti, anche la creazione di strutture MRO sta assistendo a un trend positivo. Il crescente utilizzo di elicotteri sta rapidamente accelerando la portata delle attività di manutenzione degli elicotteri. Paesi come Singapore e India stanno assistendo alla presenza di aziende che offrono servizi MRO associati al carrello di atterraggio per elicotteri. Tentacle Aerologistix Pvt. Ltd. è entrata nel settore MRO con l'obiettivo di creare un punto di riferimento nella manutenzione degli aeromobili. Inoltre, diversi paesi emergenti hanno anche annunciato i loro piani per creare un hub MRO nelle rispettive regioni. Ad esempio, il governo indiano ha annunciato di rendere il paese un hub MRO per l'aviazione, il che dovrebbe ulteriormente stimolare la domanda di sistemi di carrello di atterraggio per elicotteri in tutta la regione.

Analisi della segmentazione del rapporto di mercato del carrello di atterraggio per elicotteri

I segmenti chiave che hanno contribuito alla derivazione dell'analisi di mercato del carrello di atterraggio per elicotteri sono tipologia, materiale e applicazione.

- In base al tipo, il mercato dei carrelli di atterraggio per elicotteri è diviso in skid e ruote. Il segmento skid ha detenuto una quota di mercato maggiore nel 2023.

- In base al materiale, il mercato del carrello di atterraggio per elicotteri è segmentato in set di carrelli di atterraggio in alluminio, set di carrelli di atterraggio in acciaio, set di carrelli di atterraggio in composito e titanio . Il segmento composito ha detenuto una quota di mercato maggiore nel 2023.

- In base all'applicazione, il mercato del carrello di atterraggio per elicotteri è diviso in elicotteri civili ed elicotteri militari. Il segmento degli elicotteri militari ha detenuto una quota di mercato maggiore nel 2023.

Analisi della quota di mercato del carrello di atterraggio per elicotteri per area geografica

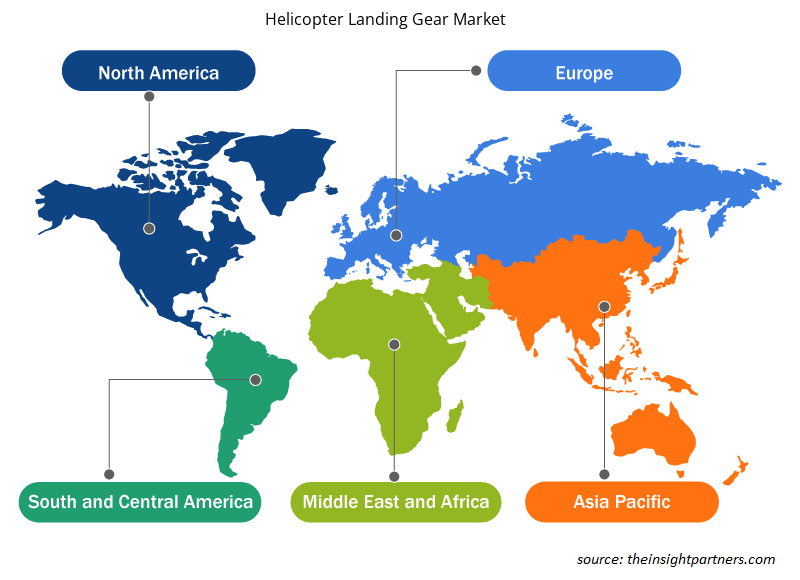

L'ambito geografico del rapporto sul mercato dei carrelli di atterraggio per elicotteri è suddiviso principalmente in cinque regioni: Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e Sud America.

Il Nord America ha dominato il mercato nel 2023, seguito da Europa e regioni dell'Asia Pacifica. Inoltre, è probabile che anche l'Asia Pacifica registri il CAGR più elevato nei prossimi anni. Gli Stati Uniti hanno dominato il mercato dei carrelli di atterraggio per elicotteri del Nord America nel 2023. L'aeronautica militare statunitense è una delle forze armate più potenti e tecnologicamente avanzate al mondo. Il governo degli Stati Uniti investe costantemente nello sviluppo di una base industriale di difesa nel paese, a causa di una significativa attenzione all'espansione delle capacità militari come priorità strategica. Nel 2023, la spesa militare degli Stati Uniti è stata di 916 miliardi di dollari, con un aumento del 4,4 percento rispetto all'anno precedente. Si prevede che gli Stati Uniti saranno il maggiore contributore di entrate nel mercato mondiale dei carrelli di atterraggio per elicotteri grazie alla continua spesa in R&S per il rafforzamento del settore militare, nonché alla presenza di alcuni dei principali produttori di elicotteri da combattimento e carrelli di atterraggio. CIRCOR Aerospace e Safran sono tra i principali produttori che operano nel mercato statunitense dei carrelli di atterraggio. Pertanto, si prevede che il mercato dei carrelli di atterraggio per elicotteri crescerà durante il periodo previsto come risultato dei fattori sopra menzionati.

Ambito del rapporto di mercato sul carrello di atterraggio per elicotteri

Approfondimenti regionali sul mercato dei carrelli di atterraggio per elicotteri

Le tendenze regionali e i fattori che influenzano il mercato degli elicotteri per l'intero periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato degli elicotteri per il Nord America, l'Europa, l'Asia Pacifica, il Medio Oriente e l'Africa e l'America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato del carrello di atterraggio per elicotteri

Ambito del rapporto di mercato sul carrello di atterraggio per elicotteri

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 3,81 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 5,99 miliardi di dollari USA |

| CAGR globale (2023-2031) | 5,8% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per tipo

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità dei giocatori del mercato del carrello di atterraggio per elicotteri: comprendere il suo impatto sulle dinamiche aziendali

Il mercato del carrello di atterraggio per elicotteri sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato dei carrelli di atterraggio per elicotteri sono:

- Circor Aerospace Inc

- Sika Interplant Systems Limited

- DART AEROSPAZIALE

- Società Eurocarbon BV

- Trelleborg

- Rostec

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato dei carrelli di atterraggio per elicotteri

Notizie e sviluppi recenti sul mercato dei carrelli di atterraggio per elicotteri

Il mercato dei carrelli di atterraggio per elicotteri viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati associativi e database. Di seguito sono elencati alcuni degli sviluppi nel mercato dei carrelli di atterraggio per elicotteri:

- Safran Landing Systems è a bordo del programma di aeromobili tiltrotor di Bell, come parte del progetto Future Long-Range Assault Aircraft (FLRAA) dell'esercito americano. Secondo il contratto, Safran Landing Systems progetterà e svilupperà il sistema di atterraggio completamente integrato. Questi sforzi condivisi stabiliranno solide basi per soddisfare tutti i requisiti futuri. (Fonte: Safran, comunicato stampa, settembre 2023)

- Trelleborg Sealing Solutions lancia il suo materiale composito Orkot® C620, sviluppato specificamente per soddisfare le esigenze del settore aerospaziale, in particolare la necessità di un materiale resistente e leggero per sopportare gli elevati carichi e sollecitazioni a cui sono soggetti i carrelli di atterraggio. (Fonte: Trelleborg Sealing Solutions, comunicato stampa, febbraio 2022)

Copertura e risultati del rapporto sul mercato del carrello di atterraggio per elicotteri

Il rapporto "Dimensioni e previsioni del mercato del carrello di atterraggio per elicotteri (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato del carrello di atterraggio per elicotteri a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato del carrello di atterraggio per elicotteri e dinamiche di mercato come conducenti, sistemi di ritenuta e opportunità chiave

- Analisi dettagliata delle cinque forze di Porter

- Analisi di mercato del carrello di atterraggio per elicotteri che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti per il mercato dei carrelli di atterraggio per elicotteri

- Profili aziendali dettagliati

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative