Rapporto sul mercato dei dispositivi elettronici induriti dalle radiazioni 2031 per segmenti, geografia, dinamiche, sviluppi recenti e approfondimenti strategici

Dimensioni e previsioni del mercato dell'elettronica resistente alle radiazioni (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per componente (componenti di gestione dell'alimentazione, dispositivi a segnale misto analogici e digitali, memoria e controller e processori), tecnica di produzione [indurimento dalle radiazioni tramite progettazione (RHBD) e indurimento dalle radiazioni tramite processo (RHBP)] e applicazione (aerospaziale e difesa, centrali nucleari, spazio e altri) e geografia.

- Stato : Dati rilasciati

- Codice del report : TIPRE00011821

- Categoria : Elettronica e semiconduttori

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : February 15, 2025

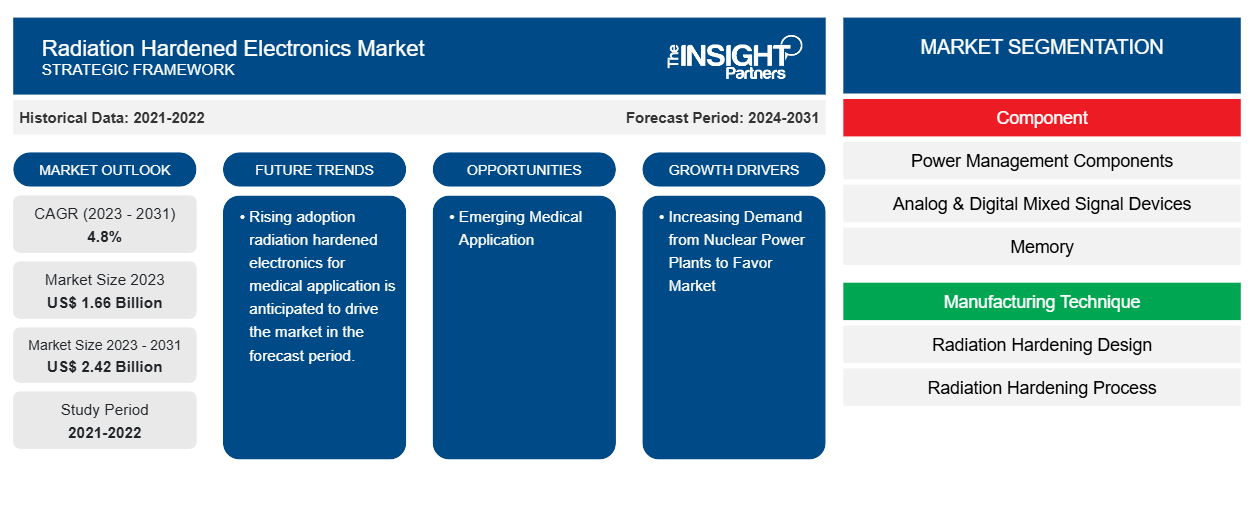

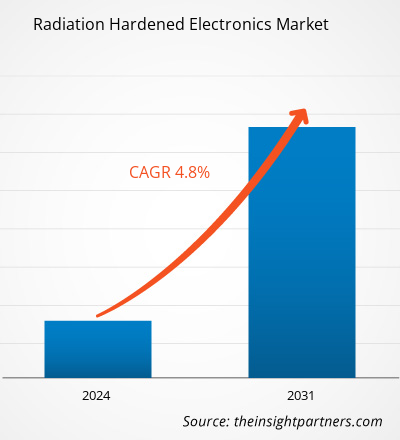

Si prevede che la dimensione del mercato dell'elettronica indurita dalle radiazioni raggiungerà i 2,42 miliardi di dollari entro il 2031, rispetto agli 1,66 miliardi di dollari del 2023. Si prevede che il mercato registrerà un CAGR del 4,8% nel periodo 2023-2031. È probabile che l'adozione crescente di elettronica indurita dalle radiazioni e l'aumento degli investimenti nei programmi spaziali rimangano tendenze e driver chiave nel mercato.

Analisi del mercato dell'elettronica resistente alle radiazioni

Si prevede che la crescente domanda di sensori di feedback resistenti alle radiazioni tra i produttori di apparecchiature e sistemi critici in tutto il mondo stimolerà il mercato dei sensori di feedback resistenti alle radiazioni durante il periodo di previsione. I sensori di feedback resistenti alle radiazioni sono ampiamente integrati nei sistemi aerospaziali e di difesa, veicoli spaziali, satelliti, sonde spaziali, apparecchiature mediche e altri. I progressi tecnologici, la miniaturizzazione dei sensori di feedback resistenti alle radiazioni, la crescente domanda di energia rinnovabile e le crescenti attività di R&S stanno spingendo il mercato dei sensori di feedback resistenti alle radiazioni.

Panoramica del mercato dell'elettronica resistente alle radiazioni

I sensori di feedback resistenti alle radiazioni sono dispositivi progettati per resistere a livelli elevati di radiazioni, più comunemente riscontrati in ambienti nucleari e spaziali. Questi sensori impiegano un meccanismo di feedback per monitorare costantemente le loro prestazioni e si regolano di conseguenza, assicurando operazioni affidabili e accurate in radiazioni intense. I sensori utilizzano loop di feedback per rilevare eventuali deviazioni dal comportamento previsto causate da danni indotti dalle radiazioni.

Personalizza questo report in base alle tue esigenze

Riceverai la personalizzazione gratuita di qualsiasi report, comprese parti di questo report, o analisi a livello nazionale, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dell'elettronica resistente alle radiazioni: approfondimenti strategici

-

Scopri le principali tendenze di mercato in questo rapporto.Questo campione GRATUITO includerà analisi di dati che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato dell'elettronica resistente alle radiazioni

La crescente domanda di centrali nucleari favorisce il mercato

Le centrali nucleari sono coinvolte nella generazione di elettricità attraverso il processo di fissione nucleare. In questo processo, viene prodotta una notevole quantità di energia, che genera una notevole quantità di radiazioni. Questa radiazione è dannosa per gli esseri umani e può danneggiare le apparecchiature elettroniche, aumentando la domanda di sensori di feedback resistenti alle radiazioni. I sensori di feedback resistenti alle radiazioni sono posizionati strategicamente in tutto l'impianto per monitorare le variazioni di temperatura in aree critiche, come i sistemi di raffreddamento, il nocciolo del reattore e vari componenti. Questi sensori forniscono un feedback continuo ai sistemi di controllo, consentendo agli operatori dell'impianto di adottare le misure necessarie per mantenere l'intervallo di temperatura desiderato e prendere decisioni informate per migliorare le prestazioni del sistema. Diverse aziende stanno effettuando investimenti significativi nello sviluppo di centrali elettriche. Ad esempio, secondo i dati del Dipartimento dell'energia degli Stati Uniti (DOE) pubblicati a gennaio 2024, il DOE ha investito circa 12 miliardi di dollari nell'impianto Vogtle per fornire alla rete oltre 1.100 megawatt di energia pulita una volta in funzione.Vogtle to provide more than 1,100 megawatts of clean power to the grid once in operation.

Applicazione medica emergente.

I sensori di feedback resistenti alle radiazioni svolgono un ruolo cruciale nel garantire la sicurezza, l'accuratezza e l'affidabilità delle apparecchiature mediche utilizzate nel settore sanitario. Questi sensori sono integrati in una varietà di apparecchiature mediche, tra cui raggi gamma, raggi X e fasci di elettroni, rendendoli resistenti a livelli elevati di radiazioni. I sensori di feedback resistenti alle radiazioni sono principalmente integrati nelle apparecchiature per radioterapia per supportare i medici nel trattamento dei pazienti oncologici. La radioterapia , nota anche come radioterapia, è la modalità di trattamento più comune per i pazienti oncologici, in cui vengono utilizzati fasci di radiazioni ad alta energia per colpire e distruggere le cellule cancerose, che richiedono sensori di feedback resistenti alle radiazioni per monitorare vari parametri, tra cui somministrazione della dose, densità del fascio e posizionamento del fascio. Gli operatori sanitari utilizzano sensori di feedback resistenti alle radiazioni per garantire la somministrazione di un trattamento accurato e preciso riducendo al minimo i danni ai tessuti sani. Ad esempio, nell'aprile 2022, Maxon Group ha introdotto gli encoder ENX GAMA progettati per l'uso in prossimità di acceleratori lineari medici su apparecchiature come i collimatori multi-lama. Gli encoder ENX GAMA sono encoder resistenti alle radiazioni integrati con motori CC altamente adatti per dispositivi di radioterapia.Maxon Group introduced ENX GAMA encoders designed for use in the vicinity of medical linear accelerators on equipment such as multi-leaf collimators. ENX GAMA encoders are radiation-resistant encoders integrated with DC motors that are highly suitable for radiotherapy devices.

Analisi della segmentazione del rapporto di mercato dell'elettronica indurita dalle radiazioni

I segmenti chiave che hanno contribuito alla derivazione dell'analisi del mercato dell'elettronica resistente alle radiazioni sono i componenti, le tecniche di produzione e le applicazioni.

- In base al componente, il mercato dell'elettronica indurita dalle radiazioni è suddiviso in componenti di gestione dell'alimentazione, dispositivi a segnale misto analogici e digitali, memoria e controller e processori. Si prevede che il segmento dei componenti di gestione dell'alimentazione detenga una quota di mercato significativa nel periodo di previsione.

- In base alla tecnica di produzione, il mercato dell'elettronica indurita dalle radiazioni è suddiviso in indurimento dalle radiazioni per progettazione (RHBD) e indurimento dalle radiazioni per processo (RHBP). Si prevede che il segmento dell'indurimento dalle radiazioni per progettazione (RHBD) deterrà una quota di mercato significativa nel periodo di previsione.

- Per applicazioni, il mercato è segmentato in aerospaziale e difesa, centrale nucleare, spazio e altri. Si prevede che aerospaziale e difesa manterranno una quota di mercato significativa nel periodo di previsione.

Analisi della quota di mercato dell'elettronica resistente alle radiazioni per area geografica

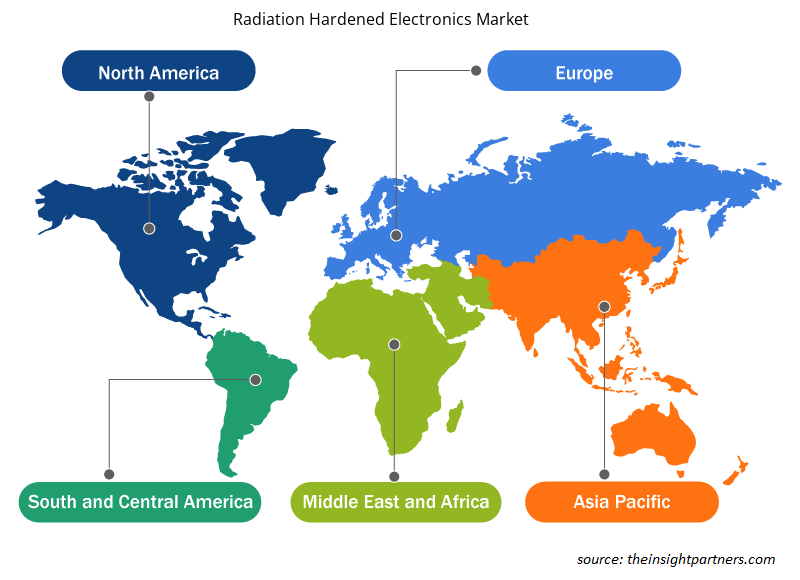

L'ambito geografico del rapporto sul mercato dei dispositivi elettronici resistenti alle radiazioni è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa, e Sud e Centro America.

Il Nord America ha dominato il mercato dell'elettronica resistente alle radiazioni. L'industria spaziale in espansione sta potenziando il mercato dei sensori di feedback resistenti alle radiazioni in Nord America. Gli Stati Uniti sono stati in prima linea nei voli spaziali per oltre 60 anni. Hanno il più grande programma spaziale governativo al mondo. I satelliti registrati negli Stati Uniti hanno rappresentato oltre la metà di tutti i satelliti operativi nel 2022. Gli Stati Uniti sono attualmente l'unico paese con un account tematico per le attività spaziali. Inoltre, una forte enfasi sulla ricerca e sviluppo nelle economie sviluppate di Stati Uniti e Canada sta costringendo gli attori nordamericani a portare sul mercato soluzioni tecnologicamente avanzate. Inoltre, gli Stati Uniti hanno un gran numero di attori del mercato dell'elettronica resistente alle radiazioni che si sono sempre più concentrati sullo sviluppo di soluzioni innovative. Tutti questi fattori contribuiscono alla crescita del mercato dell'elettronica resistente alle radiazioni nella regione.

Approfondimenti regionali sul mercato dell'elettronica resistente alle radiazioni

Le tendenze regionali e i fattori che influenzano il mercato dell'elettronica indurita dalle radiazioni durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di Insight Partners. Questa sezione discute anche i segmenti e la geografia del mercato dell'elettronica indurita dalle radiazioni in Nord America, Europa, Asia Pacifico, Medio Oriente e Africa e America meridionale e centrale.

- Ottieni i dati specifici regionali per il mercato dell'elettronica resistente alle radiazioni

Ambito del rapporto di mercato sui prodotti elettronici resistenti alle radiazioni

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2023 | 1,66 miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 2,42 miliardi di dollari USA |

| CAGR globale (2023-2031) | 4,8% |

| Dati storici | 2021-2022 |

| Periodo di previsione | 2024-2031 |

| Segmenti coperti |

Per componente

|

| Regioni e Paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori del mercato: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dell'elettronica resistente alle radiazioni sta crescendo rapidamente, spinto dalla crescente domanda degli utenti finali dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando le loro offerte, innovando per soddisfare le esigenze dei consumatori e capitalizzando sulle tendenze emergenti, il che alimenta ulteriormente la crescita del mercato.

La densità degli operatori di mercato si riferisce alla distribuzione di aziende o società che operano in un particolare mercato o settore. Indica quanti concorrenti (operatori di mercato) sono presenti in un dato spazio di mercato in relazione alle sue dimensioni o al valore di mercato totale.

Le principali aziende che operano nel mercato dell'elettronica protetta dalle radiazioni sono:

- Sistemi BAE

- Società di dispositivi dati

- Honeywell International Inc.

- Infineon Technologies AG

- Società di elettronica Renesas

- Società per azioni Texas Instruments

Disclaimer : le aziende elencate sopra non sono classificate secondo un ordine particolare.

- Ottieni una panoramica dei principali attori del mercato dell'elettronica resistente alle radiazioni

Notizie e sviluppi recenti sul mercato dell'elettronica resistente alle radiazioni

Il mercato dell'elettronica indurita dalle radiazioni viene valutato raccogliendo dati qualitativi e quantitativi dopo la ricerca primaria e secondaria, che include importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito sono elencati alcuni degli sviluppi nel mercato dell'elettronica indurita dalle radiazioni:

- EPC Space ha presentato l'EPC7009L16SH, un IC driver di gate in nitruro di gallio (GaN) indurito dalle radiazioni. Utilizzando l'esclusiva tecnologia IC eGaN di EPC, questo innovativo driver GaN consente ai progettisti di sfruttare appieno le capacità della tecnologia FET eGaN. (Fonte: EPC Space, sito Web aziendale, aprile 2024)

- Renesas Electronics Corporation, fornitore di soluzioni avanzate per semiconduttori, ha lanciato una nuova linea di dispositivi resistenti alle radiazioni (rad-hard) incapsulati in plastica per sistemi di gestione dell'alimentazione satellitare. I quattro nuovi dispositivi includono il regolatore buck point of load (POL) ISL71001SLHM/SEHM, gli isolatori digitali ISL71610SLHM e ISL71710SLHM e il FET GaN da 100 V ISL73033SLHM e il driver low-side integrato. (Fonte: Renesas Electronics Corporation, sito Web aziendale, luglio 2021)

Copertura e risultati del rapporto sul mercato dell'elettronica indurita dalle radiazioni

Il rapporto "Dimensioni e previsioni del mercato dell'elettronica indurita dalle radiazioni (2021-2031)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato dell'elettronica protetta dalle radiazioni a livello globale, regionale e nazionale per tutti i principali segmenti di mercato interessati dall'indagine.

- Tendenze del mercato dell'elettronica protetta dalle radiazioni e dinamiche di mercato quali fattori trainanti, limitazioni e opportunità chiave.

- Analisi dettagliata delle cinque forze PEST/Porter e SWOT.

- Analisi del mercato dell'elettronica protetta dalle radiazioni che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato.

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa di calore, i principali attori e gli sviluppi recenti per il mercato dell'elettronica protetta dalle radiazioni.

- Profili aziendali dettagliati.

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative