Domanda, tendenze e previsioni del mercato IP dei semiconduttori entro il 2034

Dimensioni e previsioni del mercato IP per semiconduttori (2021-2034), quota globale e regionale, trend e analisi delle opportunità di crescita. Copertura del rapporto: per tipologia (SIP per processori, SIP per interfacce, SIP fisico, SIP analogico e altri), fonte (licenze e royalty) e settore verticale (telecomunicazioni, automobilistico, industriale, elettronico, medicale e altri).

- Stato : Dati rilasciati

- Codice del report : TIPEL00002043

- Categoria : Elettronica e semiconduttori

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : March 17, 2026

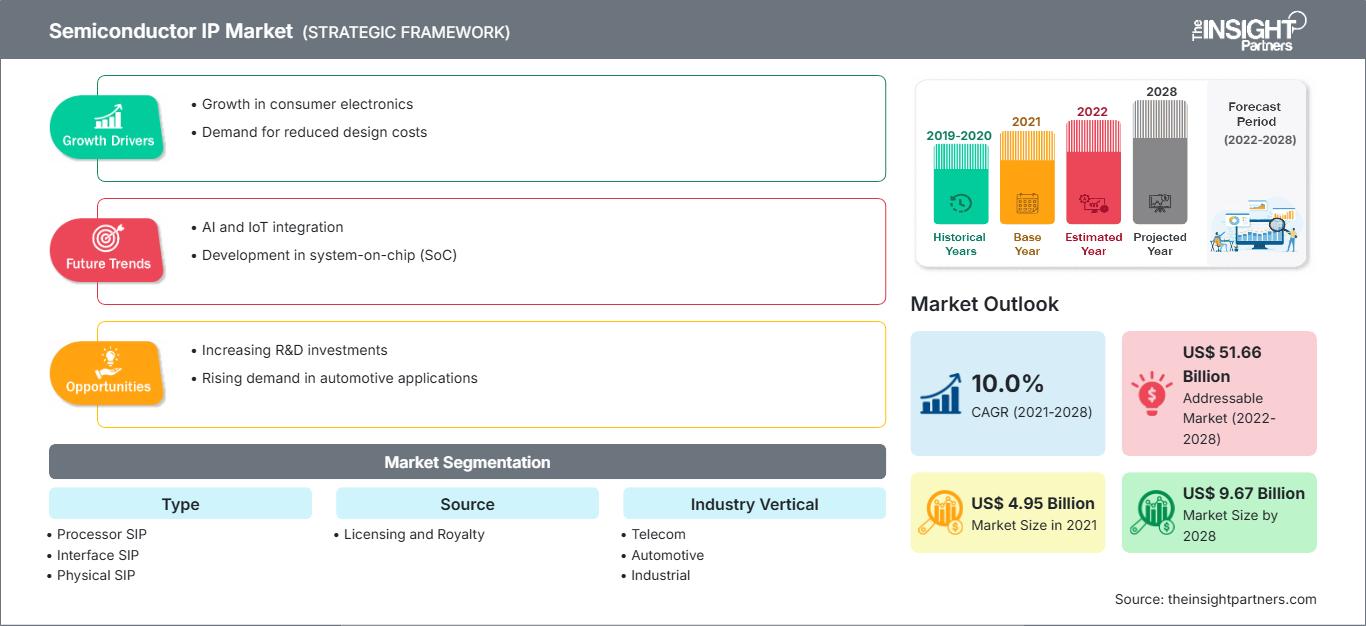

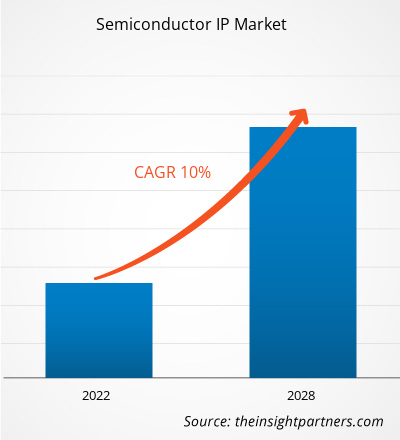

Si prevede che il mercato globale della proprietà intellettuale dei semiconduttori raggiungerà un valore di 17,31 miliardi di dollari entro il 2034, rispetto ai 7,5 miliardi di dollari del 2025. Si prevede inoltre che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 10,15% durante il periodo di previsione 2026-2034.

Tra le principali dinamiche di mercato si annoverano la massiccia espansione del calcolo ad alte prestazioni (HPC) per l'intelligenza artificiale generativa, la transizione strutturale verso i veicoli definiti dal software (SDV) e la rapida standardizzazione delle interconnessioni basate su chiplet. Inoltre, si prevede che il mercato trarrà vantaggio dall'aumento delle iniziative di sovranità dei semiconduttori a livello globale, dai crescenti investimenti nei cluster nazionali di progettazione di chip nelle economie emergenti e dalla crescente domanda di architetture di memoria avanzate come HBM3 e GDDR7.

Analisi del mercato della proprietà intellettuale dei semiconduttori

L'analisi del mercato IP dei semiconduttori indica un cambiamento cruciale verso la modularità e le architetture a standard aperto come RISC-V per contrastare l'aumento dei costi di licenza proprietari. Il mercato mostra un punto di svolta in cui i progettisti si stanno allontanando dai progetti SoC monolitici a favore dell'integrazione eterogenea tramite chiplet. Stanno emergendo opportunità strategiche nell'integrazione di funzionalità di intelligenza artificiale edge direttamente nei chip IoT, consentendo l'inferenza locale e riducendo la latenza dei dati per le applicazioni industriali intelligenti. L'analisi rileva inoltre che l'espansione del mercato è sempre più guidata da collaborazioni incentrate sui servizi, in cui i fornitori di IP offrono strumenti di integrazione e gestione del ciclo di vita personalizzati per garantire l'integrità del segnale nei nodi a 3 nm e 2 nm. La differenziazione competitiva emerge ora per i fornitori che offrono blocchi IP pre-verificati e certificati ISO 26262 per la sicurezza automobilistica, poiché l'affidabilità hardware sta diventando un requisito primario per la prossima generazione di sistemi di trasporto autonomi.

Panoramica del mercato della proprietà intellettuale dei semiconduttori

La proprietà intellettuale dei semiconduttori si è trasformata da strumento di supporto alla progettazione a motore principale della differenziazione a livello di silicio. La proprietà intellettuale dei semiconduttori comprende unità di elaborazione neurale (NPU) specializzate, interfacce wireless a bassissimo consumo per dispositivi indossabili e motori di crittografia sicuri ancorati all'hardware. Sia i leader tradizionali dell'EDA (Electronic Design Automation) che le startup emergenti nel settore open-core competono in questo mercato, utilizzando un mix di canoni di licenza una tantum e flussi di royalty ricorrenti che scalano con i volumi di produzione. La crescente domanda di data center hyperscale e di edge computing decentralizzato ha aumentato la popolarità di sottosistemi IP specializzati che ottimizzano le prestazioni per watt. Il Nord America continua a essere leader in termini di intensità di ricerca e sviluppo e ricavi da licenze, mentre l'Asia-Pacifico rimane il maggiore consumatore di blocchi IP grazie al suo dominio incontrastato nella capacità di fonderia e nell'assemblaggio di elettronica di consumo. La concorrenza tra i marchi sta alimentando una rapida evoluzione nei progetti multi-core e l'adozione di gemelli digitali per prevedere le prestazioni del silicio prima dell'inizio della fabbricazione fisica.

Il mercato statunitense funge da centro nevralgico globale per l'innovazione, trainato da un fitto ecosistema di progettisti fabless e pionieri della tecnologia. L'attenzione strategica al calcolo ad alte prestazioni, all'intelligenza artificiale generativa e ai sistemi automobilistici avanzati sostiene la leadership nazionale. I robusti incentivi governativi e la concentrazione di importanti licenziatari accelerano ulteriormente lo sviluppo di architetture specializzate e standard di silicio di nuova generazione.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato della proprietà intellettuale dei semiconduttori: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo report.Questo campione GRATUITO includerà un'analisi dei dati, che spazierà dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato della proprietà intellettuale dei semiconduttori

Fattori trainanti del mercato:

- Espansione dell'infrastruttura di IA generativa: l'aumento dei carichi di lavoro basati sull'IA nei data center sta creando un'urgente necessità di memoria HBM ad alta larghezza di banda e di IP di processori specializzati in grado di gestire attività di elaborazione parallela su larga scala.

- Transizione ai veicoli definiti dal software: il passaggio dell'industria automobilistica ad architetture di calcolo centralizzate richiede blocchi IP sofisticati per l'elaborazione dei dati in tempo reale e la comunicazione V2X veicolo-tutto.

- Proliferazione di endpoint IoT: la diffusione di miliardi di dispositivi connessi nelle città intelligenti e nel settore sanitario alimenta la domanda di connettività a basso consumo, economicamente vantaggiosa e di IP analogici.

Opportunità di mercato:

- Hardware open source e adozione di RISC-V: la crescente fiducia del settore in RISC-V offre alle aziende un'opportunità strategica per sviluppare core CPU altamente personalizzabili e senza royalty per carichi di lavoro specializzati.

- Innovazione nella progettazione basata su chiplet: il passaggio ai chiplet modulari consente ai fornitori di IP di offrire blocchi di silicio fisici, creando nuovi flussi di entrate nel packaging avanzato e nelle IP per la comunicazione tra die.

- Sostenibilità e progettazione attenta alle emissioni di carbonio: per i produttori si prospetta un'opportunità crescente di rivolgersi ai segmenti delle tecnologie verdi attraverso IP ad alta efficienza energetica che aiutano i data center e i produttori di dispositivi mobili a rispettare le rigide normative ambientali e ESG.

Analisi di segmentazione del mercato della proprietà intellettuale dei semiconduttori.

La quota di mercato della proprietà intellettuale dei semiconduttori viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

Per tipologia:

- Segmento SIP per processori: rimane il segmento dominante, comprendente CPU, GPU e acceleratori AI specializzati, essenziali per l'informatica moderna.

- Interfaccia SIP: il settore in più rapida crescita, trainato dalla necessità di standard di connettività ad alta velocità come PCIe 7.0 e Ethernet ad alta velocità nei data center.

- SIP fisico: fondamentale per i nodi avanzati, fornisce l'interfaccia del livello fisico per la memoria e il trasferimento dati ad alta velocità.

- SIP analogico: un driver a volume costante ampiamente utilizzato nella gestione dell'alimentazione e nelle interfacce dei sensori per l'elettronica medica e industriale.

Per fonte:

- Licenze e royalty: un modello ibrido che bilancia i costi iniziali di sviluppo con i guadagni a lungo termine basati sul volume dei chip prodotti.

Per settore verticale:

- Telecomunicazioni: trainate dalla ricerca sul 5G-Advanced e sul 6G, che richiedono IP di rete ad alta larghezza di banda.

- Settore automobilistico: si concentra sui sistemi ADAS e sulla gestione della catena cinematica dei veicoli elettrici.

- Settore industriale: include proprietà intellettuale per la robotica e l'automazione intelligente delle fabbriche.

- Elettronica: comprende beni di consumo ad alto volume come smartphone e visori per realtà aumentata/virtuale.

- Settore medico: segmento emergente per la diagnostica a distanza e i dispositivi indossabili per il monitoraggio della salute.

Per area geografica:

- America del Nord

- Europa

- Asia Pacifico

- Sud e Centro America

- Medio Oriente e Africa

Ambito del rapporto sul mercato della proprietà intellettuale dei semiconduttori

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 7,5 miliardi di dollari |

| Dimensioni del mercato entro il 2034 | 17,31 miliardi di dollari |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 10,15% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

| Segmenti trattati |

Per tipologia

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori nel mercato della proprietà intellettuale dei semiconduttori: comprenderne l'impatto sulle dinamiche di business.

Il mercato della proprietà intellettuale dei semiconduttori (IP) è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi offerti dai prodotti. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Analisi della quota di mercato della proprietà intellettuale dei semiconduttori per area geografica

Si prevede che la regione Asia-Pacifico registrerà la crescita più rapida nei prossimi anni, con Cina e India impegnate in una decisa espansione delle proprie capacità di progettazione a livello nazionale. Anche i mercati emergenti in Medio Oriente e Africa offrono numerose opportunità inesplorate, grazie agli investimenti in infrastrutture per città intelligenti e all'ammodernamento delle telecomunicazioni, volti a ridurre la dipendenza da tecnologie importate.

Il mercato della proprietà intellettuale dei semiconduttori sta attraversando una profonda trasformazione, passando da ecosistemi chiusi tradizionali a un panorama più aperto e modulare. La crescita è trainata dall'ascesa del calcolo basato sull'intelligenza artificiale, dalla diversificazione della catena di fornitura del settore automobilistico e dall'espansione dei dispositivi intelligenti. Di seguito è riportato un riepilogo delle quote di mercato e delle tendenze per regione:

1. Nord America

- Quota di mercato: detiene una quota considerevole, fungendo da polo principale per la concessione di licenze IP per processori di alto valore e per la ricerca e sviluppo.

-

Fattori chiave:

- Massicci investimenti da parte dei colossi del settore (Google, Amazon, Microsoft) in acceleratori di intelligenza artificiale personalizzati e chip per server.

- Forte sostegno governativo, tramite il CHIPS Act, per il rientro in patria di capacità avanzate di progettazione e produzione.

- Ruolo di leadership nello sviluppo di strumenti EDA di nuova generazione e di IP di verifica.

- Tendenze: Un passaggio alla progettazione interna di chip da parte di aziende non operanti nel settore dei semiconduttori e la rapida adozione di IP con elevati standard di sicurezza.

2. Europa

- Quota di mercato: Detiene una presenza significativa, profondamente radicata nei settori dei semiconduttori industriali e automobilistici.

-

Fattori chiave:

- Le rigide normative in materia di sicurezza funzionale stanno alimentando la domanda di blocchi IP certificati per il settore automobilistico.

- Comprovata esperienza nelle tecnologie IP wireless e analogiche a basso consumo per l'IoT industriale e la gestione delle energie rinnovabili.

- Sostegno proattivo all'European Chips Act per raddoppiare la quota di produzione globale della regione.

- Tendenze: crescente attenzione verso RISC-V per garantire l'indipendenza tecnologica e l'integrazione di IP edge-AI nei sistemi di automazione industriale.

3. Asia-Pacifico

- Quota di mercato: Il più grande mercato regionale, alimentato dai vasti ecosistemi di fonderie in Corea del Sud e Cina.

-

Fattori chiave:

- Concentrazione senza pari di produttori a contratto (fonderie) e fornitori di servizi di assemblaggio e collaudo di semiconduttori in outsourcing (OSAT).

- Rapida espansione delle aziende di design nazionali in India e Cina, supportata da missioni nazionali come l'India Semiconductor Mission (ISM) 2.0.

- Crescente domanda di IP per 5G, telefonia mobile ed elettronica di consumo in una popolazione in rapida urbanizzazione.

- Tendenze: predominio nel segmento IP delle memorie (HBM3/HBM4) e forte dipendenza da modelli basati su royalty a causa dell'elevato volume di dispositivi spediti.

4. Sud e Centro America

- Quota di mercato: un mercato emergente con una presenza in crescita in Brasile e Argentina per l'assemblaggio di componenti automobilistici e di consumo.

-

Fattori chiave:

- Nuovi accordi di cooperazione (ad esempio, tra Intel e i governi regionali) per rafforzare le catene di approvvigionamento locali.

- La crescente diffusione di contatori intelligenti e dispositivi IoT richiede IP di connettività standardizzati.

- Tendenze: Espansione dei modelli "design-lite", in cui le aziende locali personalizzano la proprietà intellettuale esistente anziché svilupparla da zero.

5. Medio Oriente e Africa

- Quota di mercato: mercato in via di sviluppo, focalizzato sulle infrastrutture di telecomunicazione e su progetti locali di smart city.

-

Fattori chiave:

- Investimenti strategici in iniziative di trasformazione digitale nella regione del Consiglio di Cooperazione del Golfo (GCC).

- Crescente domanda di IP hardware sicuro nei programmi governativi di sicurezza informatica e di gestione dell'identità.

- Tendenze: Implementazione di IP specializzati per le comunicazioni satellitari e crescita dei centri di calcolo ad alte prestazioni (HPC).

Elevata densità di mercato e concorrenza

La concorrenza si sta intensificando a causa della presenza di leader affermati come ARM Limited, Synopsys e Cadence Design Systems. Anche esperti regionali e operatori di nicchia come Faraday Technology Corporation e Imagination Technologies, insieme a innovatori come CEVA e Rambus, contribuiscono a un panorama di mercato diversificato e in rapida espansione.

Questo contesto competitivo spinge i fornitori a differenziarsi attraverso:

- Personalizzazione e supporto tecnico: Andare oltre la semplice vendita di un progetto standard per offrire servizi di personalizzazione che ottimizzino la proprietà intellettuale in base a specifici obiettivi di prestazioni o consumo energetico.

- Disponibilità presso più fonderie: garantire la validazione della proprietà intellettuale presso diverse fonderie per offrire ai clienti flessibilità nella catena di fornitura e mitigare i rischi geopolitici.

- Soluzioni di sicurezza end-to-end: integrazione di root-of-trust e acceleratori crittografici nei core IP standard per proteggere da contraffazione e accessi non autorizzati.

Opportunità e mosse strategiche

- Sfruttate la rivoluzione dei chiplet: collaborate con i leader nel packaging avanzato per sviluppare IP di interfaccia die-to-die (D2D) (come UCIe), che consentiranno la prossima generazione di processori modulari multi-chip.

- Sfruttare l'ondata RISC-V: integrare core conformi a RISC-V nei portfolio esistenti per attrarre i progettisti alla ricerca di architetture di set di istruzioni esenti da royalty o altamente personalizzabili.

- Migliorare la sicurezza hardware: integrare acceleratori hardware e crittografici nei blocchi IP standard per affrontare la crescente preoccupazione globale per il furto di proprietà intellettuale e le violazioni dei dati.

Le principali aziende operanti nel mercato della proprietà intellettuale dei semiconduttori sono:

- Arm Holdings Plc

- Faraday Technology Corporation

- Ceva, Inc.

- eMemory Technology Inc

- Imagination Technologies Group Plc

- Lattice Semiconductor Corporation

- Rambus Inc.

- Intel Corporation

- Xilinx, Inc.

- Cadence Design Systems, Inc.

- Sinossi

- Verisilicon Holdings Co. Ltd.

Nota: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e ultimi sviluppi del mercato della proprietà intellettuale dei semiconduttori

- Nel gennaio 2026, Ceva, Inc. ha annunciato che BOS Semiconductors aveva concesso in licenza la sua architettura SensPro™ AI DSP per il System-on-Chip (SoC) ADAS standalone Eagle-A. Eagle-A è progettato per sistemi avanzati di assistenza alla guida e di guida autonoma, combinando una NPU, una CPU e una GPU di fascia alta con interfacce di rilevamento dedicate per la fusione di dati provenienti da telecamera, LiDAR e radar. Il SensPro AI DSP di Ceva è ottimizzato per la pre-elaborazione di dati LiDAR e radar, consentendo una gestione efficiente dei dati grezzi dei sensori e riducendo la latenza nelle pipeline di percezione. La strategia a chiplet di BOS Semiconductors migliora ulteriormente la scalabilità, con Eagle-A progettato per funzionare insieme all'acceleratore AI Eagle-N in configurazioni multi-die connesse tramite UCIe e PCIe.

- Nel giugno 2025, Faraday Technology Corporation ha annunciato la disponibilità del suo IP SerDes a 10G sulla tecnologia di processo a 22 nm di UMC. Progettato per soddisfare le crescenti esigenze di trasmissione dati ad alta velocità, il nuovo IP SerDes supporta un'ampia gamma di protocolli standard di settore ed è ottimizzato per applicazioni nell'automazione industriale, nell'AIoT, nei modem 5G, nella fibra fino a casa (FTTH) e nelle reti avanzate.

Copertura e risultati del rapporto sul mercato della proprietà intellettuale dei semiconduttori.

Il rapporto "Dimensioni e previsioni del mercato della proprietà intellettuale dei semiconduttori (2021-2034)" fornisce un'analisi dettagliata del mercato, coprendo le seguenti aree:

- Dimensioni e previsioni del mercato IP dei semiconduttori a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato della proprietà intellettuale dei semiconduttori, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave.

- Analisi PEST e SWOT dettagliata

- Analisi del mercato della proprietà intellettuale dei semiconduttori, che comprende le principali tendenze di mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato.

- Analisi del panorama industriale e della concorrenza, con particolare attenzione alla concentrazione del mercato, all'analisi tramite mappa termica, ai principali operatori e ai recenti sviluppi nel mercato della proprietà intellettuale dei semiconduttori.

- Profili aziendali dettagliati

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative