自動車用タイヤアフターマーケットの市場シェア、成長率、需要予測(2034年まで)

自動車用タイヤアフターマーケット市場規模と予測(2021年~2034年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:タイヤタイプ(ラジアルタイヤとバイアスタイヤ)、流通チャネル(純正部品サプライヤーとIAM)、リムサイズ(13~15インチ、16~18インチ、19~21インチ、21インチ以上)、車両タイプ(乗用車、小型商用車、大型商用車)、および地域別

- ステータス : 公開されたデータ

- レポートコード : TIPRE00028388

- カテゴリー : 自動車・輸送

- ページ数 : 150

- 利用可能なレポート形式 :

- 最終更新日 : April 09, 2026

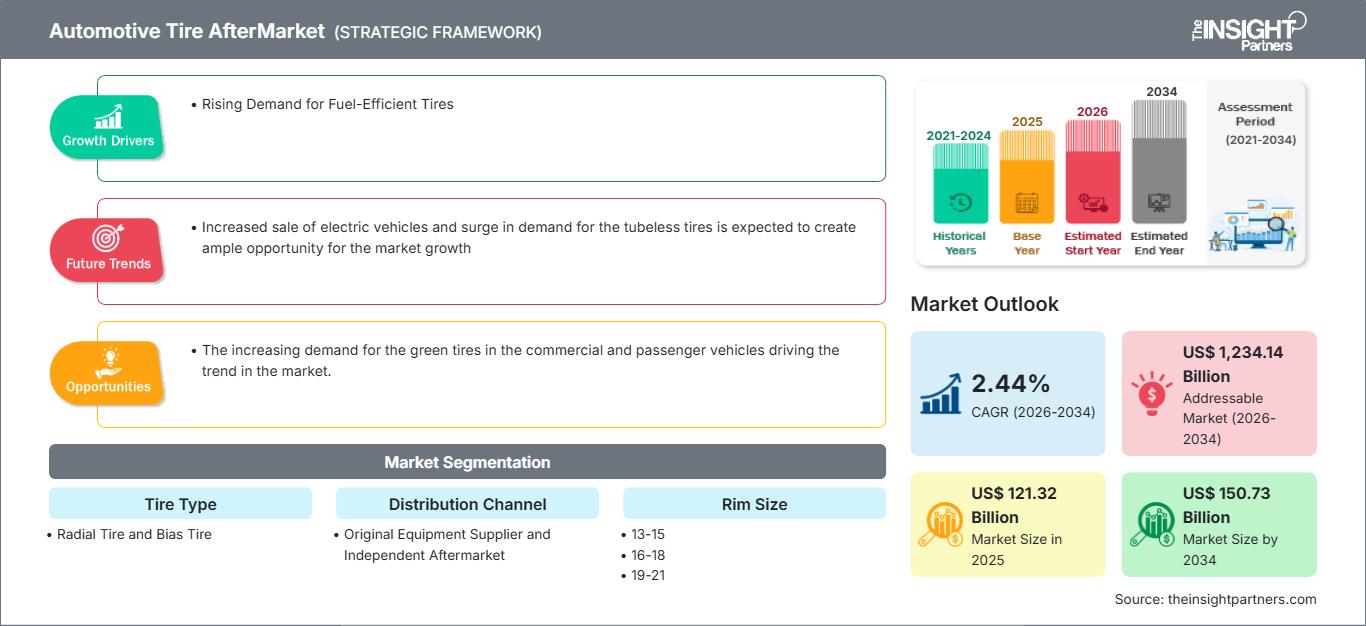

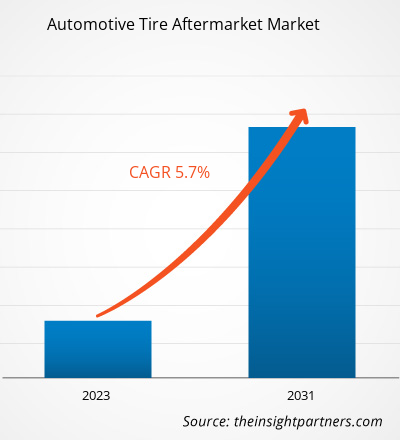

自動車用タイヤアフターマーケットの規模は、2025年の1,213億2,000万米ドルから2034年には1,507億3,000万米ドルに達すると予測されています。同市場は、2026年から2034年の予測期間中に年平均成長率(CAGR)2.44%を記録すると見込まれています。

自動車用タイヤアフターマーケット市場分析

ブレーキ摩擦製品の製造業者は、車両部品の寿命が長くなるにつれて、大きな課題に直面しています。OEMは、摩擦制御、摩耗の低減、騒音の低減、粗さの低減により、フェードが遅くなる長寿命のブレーキ摩擦製品を好みます。さらに、OEMと製造業者は、ブレーキ摩擦製品を開発する際に、耐水性、幅広い使用温度範囲、ブレーキキャリパー部品のクリーンな組み立て、道路汚染物質、酸化に対する耐久性を考慮します。近年、回生ブレーキはバッテリー駆動の電気自動車で使用されています。電気自動車メーカーは、車両をスムーズに走行させるために、高度な摩擦製品を採用しています。電気自動車の製造には金属製のローターディスクが使用されています。電気自動車の販売台数の増加に伴い、これらのブレーキ摩擦製品は軽量で高効率であるため、予測期間中、自動車用タイヤアフターマーケット市場の需要は急速に成長しています。したがって、電気自動車の需要が高まっている環境に優しい輸送手段への需要の高まりに伴い、自動車用タイヤアフターマーケット市場の成長には十分な機会があると予想されます。

自動車用タイヤアフターマーケット市場の概要

車両において最も重要な部品はタイヤであり、ホイールリムに取り付けられ、車両の推進力を伝達します。タイヤはまた、様々な路面状況による衝撃を吸収・軽減する役割も担っています。自動車用タイヤの製造には、布地、ワイヤー、天然ゴム、カーボンブラック、合成ゴム、その他の化学化合物などの材料が使用されます。タイヤメーカーは、高性能タイヤの開発とナノテクノロジーのタイヤ製造への導入を目指し、研究開発に継続的に投資しています。

自動車用タイヤは、トレッドとボディで構成されています。トレッドはトラクションを提供し、ボディは圧縮空気を保持する役割を果たします。ゴムが開発される以前は、初期のタイヤは、摩耗を防ぐために木製の車輪に金属のバンドを巻き付けただけのシンプルなものでした。初期のゴムタイヤはソリッドタイヤ(空気入りではない)でした。現在では、自動車、自転車、オートバイ、バス、トラック、重機、航空機など、多くの車両に空気入りタイヤが使用されています。機関車や鉄道車両には今でも金属タイヤが使用されていますが、キャスター、カート、芝刈り機、手押し車など、自動車以外のさまざまな用途では、ソリッドゴム(またはその他のポリマー)タイヤが使用されています。

市場調査のハイライト

- 自動車用タイヤアフターマーケットの世界市場規模は、2025年には1,213億2,000万米ドルと評価される見込みです。

- 年間市場規模は2034年までに1507億3000万米ドルに達すると予測されている。

- 2026年から2034年までの潜在市場規模(TAM)は、約1兆2341億4000万米ドルに達すると予測されています。

- 市場は予測期間中に年平均成長率(CAGR)2.44%を記録すると予想されている。

- 米国は、燃費効率の良いタイヤに対する需要の高まりと、進化する業界動向に支えられた重要な市場である。

- 市場分析は、北米、ヨーロッパ、アジア太平洋、南米、中米、中東、アフリカを対象とし、予測期間全体にわたる成長を評価しています。

- 商用車および乗用車におけるグリーンタイヤの需要増加が市場のトレンドを牽引するなど、市場機会は市場のダイナミクスと対象市場に影響を与えると予想されます。

- 本レポートでは、アポロタイヤ株式会社、コンチネンタルAG、ピレリおよびCSPA、住友ゴム工業株式会社、グッドイヤータイヤ株式会社、横浜ゴム株式会社、中策ゴム集団株式会社、ネクセンタイヤアメリカ株式会社、ブリヂストン株式会社、ミシュランなどの業界参加企業を紹介するとともに、競争戦略とイノベーションの動向を分析しています。

お客様のご要望に合わせてこのレポートをカスタマイズしてください

無料カスタマイズ自動車用タイヤアフターマーケット市場:戦略的洞察

-

本レポートの主要市場トレンドをご覧ください。この無料サンプルには、市場動向から予測、見通しまで、幅広いデータ分析が含まれています。

自動車用タイヤアフターマーケットの市場推進要因と機会

燃費効率の良いタイヤへの需要の高まり

燃料は、価格が常に変動する商品のひとつです。近年、価格は下落するどころか上昇し続けています。消費者は、燃費の良いタイヤを車に装着することで、費用を節約できる可能性があります。燃費の良いタイヤは、低転がり抵抗タイヤとも呼ばれます。転がり抵抗とは、自動車を一定の速度で走行させ続けるために必要な力のことです。タイヤにかかる摩擦の度合いによって、使用される燃料とエネルギーの量が決まります。低転がり抵抗タイヤは、転がりを維持するために必要な動力が少なく、結果として燃料消費量を削減できます。低転がり抵抗タイヤは、消費者の需要の高まり、気候変動、そして燃費の良いタイヤの二酸化炭素排出量が標準タイヤよりも少ないことから、需要が高まっています。例えば、ミシュランのエナジーセーバーA/Sオールシーズンタイヤは、最も燃費の良いタイヤの1つとして広く認識されており、多くのドライバーに人気があります。これらの要因が、自動車用タイヤのアフターマーケットの成長につながっています。

電気自動車の販売増加とチューブレスタイヤの需要急増により、市場成長のための十分な機会が生まれると予想される。

電気自動車には専用のタイヤが必要です。自動車メーカーによると、そのタイヤは内燃機関車よりも重量が大きく、停止後に走行する際に路面に伝達するトルクが大きい必要があります。電気自動車はパワートレインがほぼ無音であるため、主にエンジン音に隠れてしまい、タイヤノイズが内燃機関車よりも目立ちます。電気自動車の登場と、その推進騒音の大幅な低減により、内燃機関の推進システムでは通常測定結果が妨げられるような速度でも、巡航測定によってタイヤと路面の騒音をより正確に評価できるようになりました。欧州連合のタイヤラベルで提供される転がり抵抗評価は、電気自動車用タイヤの候補を選定する際の主要な基準として使用されています。

自動車用タイヤアフターマーケット市場レポートのセグメンテーション分析

自動車用タイヤアフターマーケット市場の分析に貢献した主要なセグメントは、タイヤの種類、流通チャネル、リムサイズ、車種、および地域である。

- タイヤの種類に基づくと、市場はラジアルタイヤとバイアスタイヤに分けられます。このうち、ラジアルタイヤは自動車生産の増加に伴い、2023年にはより大きなシェアを占める見込みです。

- 流通チャネルに基づくと、市場はOESとIAMに分けられます。2023年において、これらのうちOESが最大のシェアを占めています。

- リムのサイズによって、市場は13~15、16~18、19~21、そして21以上という4つのカテゴリーに分けられます。

- 車種によって、市場は乗用車、小型商用車、大型商用車に分けられます。その中でも、2023年には乗用車がより大きなシェアを占める見込みです。これは、世界中で乗用車の販売台数が増加しているためです。

自動車用タイヤアフターマーケットの地域別市場シェア分析

自動車用タイヤアフターマーケット市場レポートの地理的範囲は、主に北米、アジア太平洋、ヨーロッパ、中東・アフリカ、南米・中米の5つの地域に分けられます。

アジア太平洋地域は、世界で最も急速に成長している経済圏とされており、中国とインドはそれぞれ世界第1位と第3位の成長率を誇る経済大国です。日本は同地域で最も技術的に進んだ国であり、自動車用タイヤ市場の発展に大きな可能性を秘めています。ベトナム、マレーシア、インドネシアといった東南アジアの新興国では乗用車販売台数が伸びており、自動車用タイヤのアフターマーケット需要の増加が見込まれています。

自動車産業は、欧州の繁栄において重要な役割を果たしています。欧州のGDPのかなりの部分を占め、多くの人々に雇用を提供しているからです。こうした背景から、欧州委員会は欧州における自動車産業の発展のために、CARS 2020アクションプランやGEAR 2030など、様々な施策を実施してきました。欧州政府によるこれらの施策は、欧州における自動車産業の持続的な成長を支えるものと期待されています。このことは、欧州の自動車タイヤアフターマーケット市場の成長をさらに後押しするでしょう。

自動車用タイヤアフターマーケット

自動車用タイヤアフターマーケット市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2025年の市場規模 | 1213億2000万米ドル |

| 2034年までの市場規模 | 1507億3000万米ドル |

| 世界の年間平均成長率(2026年~2034年) | 2.44% |

| 履歴データ | 2021年~2024年 |

| 予測期間 | 2026年~2034年 |

| 対象分野 |

タイヤの種類別

|

| 対象地域および国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

自動車用タイヤアフターマーケットにおける市場プレーヤー密度:ビジネスダイナミクスへの影響を理解する

自動車用タイヤのアフターマーケット市場は、消費者の嗜好の変化、技術革新、製品のメリットに対する認識の高まりといった要因によるエンドユーザー需要の増加を背景に、急速に成長しています。需要の高まりに伴い、企業は製品ラインナップを拡充し、消費者のニーズに応えるべく革新を進め、新たなトレンドを活用することで、市場の成長をさらに加速させています。

自動車用タイヤアフターマーケットの市場ニュースと最新動向

自動車用タイヤアフターマーケット市場は、主要な企業出版物、業界団体のデータ、データベースなど、一次調査および二次調査に基づいて定性的および定量的データを収集することで評価されます。自動車用タイヤアフターマーケット市場における主な動向を以下に示します。

- インド最大のタイヤメーカーであるMRFは、高性能モーターサイクル向けの新製品「STEEL BRACEラジアルタイヤ」を発売しました。STEEL BRACEラジアルタイヤは、極限条件下で卓越した性能が求められるハイエンドモーターサイクル向けに特別に開発されたタイヤです。(出典:同社ウェブサイト、2023年7月)

- コンチネンタルは本日、これまでで最もサステナブルなシリーズタイヤ「UltraContact NXT」を発表しました。再生可能、リサイクル、マスバランス認証を受けた素材を最大65%使用することで、非常に高い割合のサステナブル素材と最高の安全性および性能を両立させています。コンチネンタルは、高い割合のサステナブル素材とEUタイヤラベルの最高性能を両立させたタイヤを量産で発売した最初のメーカーです。(出典:プレスリリース、2023年6月)

自動車用タイヤアフターマーケット市場レポートの対象範囲と成果物

「自動車用タイヤアフターマーケット市場規模と予測(2021年~2031年)」レポートは、以下の分野を網羅した市場の詳細な分析を提供します。

- 自動車用タイヤアフターマーケットの市場規模と予測(グローバル、地域、国レベル)を、調査範囲に含まれるすべての主要市場セグメントについて分析します。

- 自動車用タイヤアフターマーケットの市場動向、および推進要因、阻害要因、主要な機会などの市場ダイナミクス

- 詳細なPEST分析とSWOT分析

- 自動車用タイヤアフターマーケット市場の分析。主要な市場動向、世界および地域的な枠組み、主要企業、規制、および最近の市場動向を網羅。

- 自動車タイヤアフターマーケット市場における市場集中度、ヒートマップ分析、主要プレーヤー、および最近の動向を網羅した業界概況と競争分析

- 詳細な企業プロフィール

Naveenは、カスタム、シンジケート、コンサルティングの各プロジェクトにおいて9年以上の実績を持つ、経験豊富な市場調査およびコンサルティングのプロフェッショナルです。現在はアソシエイトバイスプレジデントを務め、プロジェクトバリューチェーン全体にわたるステークホルダー管理を成功させ、100件以上の調査レポートと30件以上のコンサルティング案件を執筆しています。産業および政府機関のプロジェクトに幅広く携わり、クライアントの成功とデータに基づく意思決定に大きく貢献しています。

Naveenは、カルナータカ州VTUで電子通信工学の学位を取得し、マニパル大学でマーケティング&オペレーションズのMBAを取得しています。IEEEの会員として9年間活動し、会議や技術シンポジウムへの参加、セクションレベルおよび地域レベルでのボランティア活動に積極的に取り組んでいます。現職以前は、IndustryARCでアソシエイト戦略コンサルタント、Hewlett Packard(HP Global)で産業用サーバーコンサルタントを務めていました。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応