バイオプロダクション市場戦略、トッププレーヤー、成長機会、分析、2030年までの予測

バイオプロダクション市場の規模と予測(2020年 - 2030年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:製品別(生物製剤およびバイオシミラー、ワクチン、細胞および遺伝子治療、核酸治療、その他)、用途別(関節リウマチ、血液疾患、がん、糖尿病、心血管疾患、その他)、機器別(上流機器、下流機器、バイオリアクター、消耗品および付属品)、エンドユーザー別(バイオ医薬品会社、契約製造組織、その他)、および地域別(北米、ヨーロッパ、アジア太平洋、中東およびアフリカ、南米および中米)

- ステータス : 出版

- レポートコード : TIPRE00030322

- カテゴリー : ライフサイエンス

- ページ数 : 209

- 利用可能なレポート形式 :

- 最終更新日 : June 12, 2024

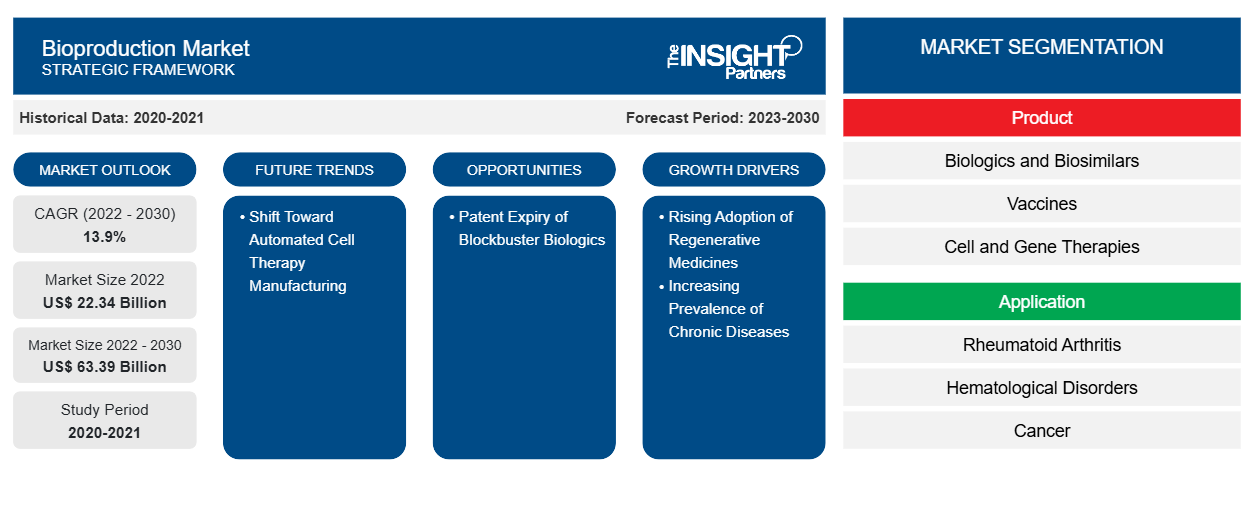

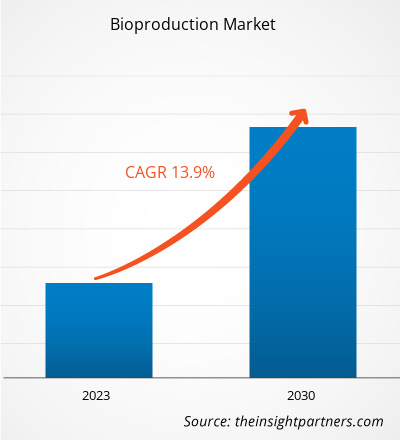

[調査レポート] バイオ生産市場規模は、2022年の223億3,724万米ドルから2030年には633億9,393万米ドルに成長すると予測されており、2022年から2030年にかけて市場は13.9%のCAGRを記録すると予測されています。

市場洞察とアナリストの見解:

自動化は、細胞療法の開発者に、汚染リスクの低減、一貫性の向上、生産コストの削減など、多くのメリットをもたらします。多くの企業が自動化を可能にするデバイスを提供しています。たとえば、Lonza Cocoon や Miltenyi の CliniMACS Prodigy システムは、CAR-T プロセスのほとんどの連続ユニット操作を単一システム内で自動化できるように設計されています。細胞療法の増加により、細胞療法製品の生産は世界中で少量から大量へと移行しています。さらに、細胞療法が学術および臨床の場から大量生産および商業化へと進化したことで、製造における自動化の需要が高まっています。細胞療法の研究活動の増加により、高度な製造ソリューションの需要が高まっています。これを考慮して、多くのプレーヤーが学術研究者や大手バイオテクノロジー企業のデジタルニーズを満たす製品を提供しています。たとえば、2019 年 5 月、GE Healthcare は細胞療法のワークフロー全体をサポートする Chronicle Web アプリケーションをリリースしました。 Chronicle 自動化ソフトウェアは、複雑な細胞治療プロセスの開発と製造を最適化するように設計された、適正製造基準 (GMP) に準拠したデジタル ソリューションです。

企業はまた、細胞療法の自動化に向けた戦略的および技術的な開発に参入しています。たとえば、2020年7月、サーモフィッシャーサイエンティフィック社とライエルイムノファーマ社は、がん患者に効果的な細胞療法を設計するためのプロセスの開発と製造で提携しました。この提携の下、両社はT細胞の適応性を向上させ、試薬、消耗品、機器とともに、cGMP(現在の適正製造基準)に準拠した統合プラットフォーム(システムとソフトウェア)の開発をサポートすることを目指しています。2019年3月、ロンザ社はイスラエルのシェバ医療センターと提携し、ポイントオブケアのコクーン細胞療法製造プラットフォームを使用して、自動化されたクローズドCAR-T製造を提供しました。このように、細胞療法メーカーによる自動化の採用の増加は、バイオプロダクション市場を牽引すると予想されます。

成長の原動力:

大ヒット生物製剤の特許切れがバイオ生産市場にチャンスをもたらす

生物製剤は、これまで治療不可能だった病気に対する有望な新しい治療法であり、医薬品市場において非常に重要になりつつあります。先駆的な生物製剤の特許は、今後数年で失効すると予想されています。

ベストセラーの生物製剤の推定特許および独占権の有効期限を次の表に示します。

|

生物製剤

|

有効期限

|

|

アバスチン |

2022年1月 |

|

シラムザ |

2023年5月 |

|

アドセトリス |

2023年8月 |

|

アブスラックス |

2024年10月 |

|

ガジヴァ/ガジヴァロ |

2024年11月 |

|

ダーザレックス |

2026年5月 |

|

オクレヴス |

2027年4月 |

|

エムガリティ |

2028年9月 |

|

ヘムリブラ |

2028年2月 |

|

リュメトリ |

2028年3月 |

|

イムフィンジ |

2028年9月 |

|

ミロターグ |

2028年4月 |

|

イムフィンジ |

2028年9月 |

|

ミロターグ |

2028年4月 |

|

シルヴァント |

2034年7月 |

出典: ジェネリック医薬品・バイオシミラー・イニシアチブ (GaBI) ジャーナル

先発生物製剤の特許切れやその他の知的財産権の失効により、将来的には新たなバイオシミラーの導入が必要になるでしょう。その結果、今後数年間で業界内の市場プレーヤー間の競争が激化するでしょう。したがって、ブロックバスター生物製剤の特許失効により、予測期間中にバイオ製造市場に有利な機会が生まれることが期待されます。

要件に合わせてレポートをカスタマイズする

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

バイオプロダクション市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

レポートのセグメンテーションと範囲:

「バイオプロダクション市場」は、製品、用途、設備、エンドユーザーに基づいてセグメント化されています。バイオプロダクション市場は、製品別に、生物製剤およびバイオシミラー、ワクチン、細胞および遺伝子治療、核酸治療、その他に細分化されています。生物製剤およびバイオシミラーセグメントは2022年に最大の市場シェアを保持し、細胞および遺伝子治療セグメントは、2022年から2030年の間に市場で最高のCAGRを記録すると予測されています。用途に基づいて、バイオプロダクション市場は、関節リウマチ、血液疾患、がん、糖尿病、心血管疾患、その他に分かれています。がんセグメントは2022年に最大の市場シェアを保持し、2022年から2030年の間に最高のCAGRを記録すると予測されています。設備の面では、バイオプロダクション市場は、消耗品およびアクセサリ、下流設備、バイオリアクター、上流設備に細分化されています。消耗品および付属品セグメントは2022年に最大の市場シェアを占め、2022年から2030年にかけて最も速いペースで成長すると予想されています。バイオプロダクション市場は、エンドユーザー別に、バイオ医薬品会社、契約製造組織、その他に分類されています。バイオ医薬品会社セグメントは2022年に最大の市場シェアを占めました。契約製造組織セグメントは、2022年から2030年にかけて市場で最も高いCAGRを記録すると予測されています。

セグメント分析:

バイオプロダクション市場は、製品別に、生物製剤およびバイオシミラー、ワクチン、細胞および遺伝子治療、核酸治療、その他に分類されています。生物製剤およびバイオシミラーセグメントは、2022年に最大の市場シェアを占めました。細胞および遺伝子治療セグメントは、2022年から2030年の間に市場で最も高いCAGRを記録すると予測されています。細胞治療と遺伝子治療は、生物医学的治療と研究において重複する分野です。両方の治療法は、病気を予防、治療、または潜在的に治癒することを目的としています。さらに、両方の治療法は、遺伝性疾患と後天性疾患の根本的な原因を改善できます。細胞治療は、患者に注入する前に体外でいくつかの細胞セットを修復または変更するか、細胞を使用して体全体に治療を施すことによって、病気を治療することを目的としています。遺伝子治療は、体外(ex vivo)または体内(in vivo)のいずれかで、細胞に新しい遺伝子を修復または導入することで病気を治療することを目的としています。遺伝子治療は、特定の種類の細胞の遺伝子を調整し、それを体内に組み込むことによって機能します。

用途別に見ると、バイオプロダクション市場は、関節リウマチ、血液疾患、がん、糖尿病、心血管疾患、その他に分類されます。がんセグメントは2022年に最大の市場シェアを占め、2022年から2030年にかけて最高のCAGRを記録すると予想されています。医療費の上昇は、がん治療の進歩と一致しています。バイオシミラーの開発は、高価な腫瘍薬の全体的なコストを削減する戦略と、米国および世界中で優先されているコスト抑制技術の結果です。いくつかの理由から、生物学的製剤はがんの治療に不可欠です。生物学的医薬品は、患者の体ががん細胞を認識して戦うのに役立ちます。特定の生物学的製剤は、がん細胞の増殖シグナルを妨害することで、がん細胞を直接標的とします。化学療法の後、さまざまな生物学的製剤が感染症との戦いに役立ちます。米国では、結腸がん、胃がん、乳がんなどの悪性腫瘍は、FDA承認のバイオシミラーで治療できます。また、白血球数の減少による感染症への脆弱性など、がん治療の副作用に対処するためにも使用できます。生物学的製剤は、がん治療において治療薬としても支持療法薬としても使用されています。トラスツズマブ (ハーセプチン) は生物学的医薬品の一例であり、進行した胃がんや乳がんの治療に使用される標的がん治療薬です。この薬のバイオシミラーには、Herzuma や Ontruzant などがあります。

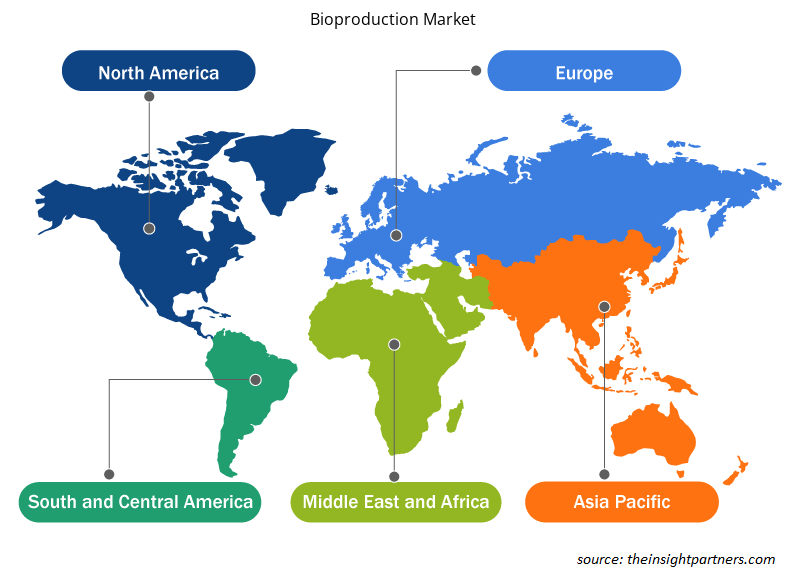

地域分析:

地理的に見ると、世界のバイオ生産市場は、北米、ヨーロッパ、アジア太平洋、中南米、中東およびアフリカに分かれています。2022年には、北米が世界のバイオ生産市場で最大のシェアを占めました。アジア太平洋地域は、2022年から2030年にかけて最高のCAGRを記録すると予想されています。この地域の市場成長は、優れた治療ソリューションに対するニーズの高まり、研究開発活動への重点の増加、および有利な規制シナリオに起因しています。さらに、研究活動を促進するための投資の増加とヘルスケアインフラストラクチャの開発は、2022年から2030年にかけてアジア太平洋地域のバイオ生産市場を牽引すると予測されています。

北米のバイオ生産市場は、さらに米国、カナダ、メキシコに分かれています。この地域の市場成長は、糖尿病や不妊症の発症率の増加、およびバイオシミラーの製品開発の増加に起因しています。

遺伝性疾患や細胞性疾患の発生率の増加により、細胞療法の需要が高まっています。細胞および遺伝子療法パイプラインに関する 2020 年の PhRMA レポートによると、米国ではがんから遺伝性疾患、神経疾患まで、さまざまな疾患や症状を対象とする 400 種類の細胞および遺伝子療法が開発中です。2020 年 2 月現在、米国ではがん、眼疾患、まれな遺伝性疾患の治療薬として 9 種類の細胞または遺伝子療法製品が承認されています。また、米国では細胞療法の革新に取り組むスタートアップ企業が増えています。

米国では、バイオシミラーは、がん、腎臓病、糖尿病、およびクローン病や関節リウマチなどの他の自己免疫疾患の患者の治療に使用されています。カーディナルヘルスによると、米国では合計33のバイオシミラーがFDAに承認されており、21が市販されています。市場の21のバイオシミラーのうち、17はがん関連の治療に、3は自己免疫疾患の治療に、1は糖尿病の治療に使用されています。バイオシミラーの価格は、生物学的製剤よりも15%から30%低くなると予想されています。2020年だけで、バイオシミラーによって79億ドルが節約され、今後数年間でさらに多くのバイオシミラーが市場に投入されるにつれて、節約額は大幅に増加すると予測されています。カーディナル・ヘルスによれば、バイオシミラーは2025年までに米国の医薬品支出を1,330億ドル削減すると予想されています。さらに、政府からの支援の拡大により細胞療法の成長が促進され、バイオ生産市場の成長に影響を与えています。

Cancer Medical Scienceによると、がんは2020年にメキシコで死亡原因の第3位にランクされています。メキシコの男性に最も多く見られるがんは、前立腺がん、大腸がん、精巣がん、肺がん、胃がんであり、女性では主に乳がん、甲状腺がん、子宮頸がん、子宮体がん、大腸がんを患っていると報告されています。メキシコでは、バイオシミラーはバイオコンパレータとも呼ばれています。GaBIによると、メキシコでは現在、赤血球生成刺激剤、顆粒球コロニー刺激因子、内因性成長ホルモン、卵胞刺激ホルモン(FSH)、インスリン、腫瘍壊死因子(TNF)阻害剤、抗ウイルス薬およびインターフェロンの治療クラスで13のバイオコンパレータが承認されています。このように、がん疾患の数とバイオシミラー製品の承認数の増加が、メキシコのバイオ製品市場の成長を牽引しています。

バイオプロダクション市場の地域別洞察

予測期間を通じてバイオプロダクション市場に影響を与える地域的な傾向と要因は、Insight Partners のアナリストによって徹底的に説明されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東、アフリカ、南米、中米にわたるバイオプロダクション市場のセグメントと地理についても説明します。

- バイオプロダクション市場の地域別データを入手

バイオプロダクション市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2022年の市場規模 | 223.4億米ドル |

| 2030年までの市場規模 | 633.9億米ドル |

| 世界のCAGR(2022年 - 2030年) | 13.9% |

| 履歴データ | 2020-2021 |

| 予測期間 | 2023-2030 |

| 対象セグメント |

製品別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業プロフィール |

|

市場プレーヤーの密度:ビジネスダイナミクスへの影響を理解する

バイオプロダクション市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認識の高まりなどの要因により、エンドユーザーの需要が高まり、急速に成長しています。需要が高まるにつれて、企業は提供を拡大し、消費者のニーズを満たすために革新し、新たなトレンドを活用し、市場の成長をさらに促進しています。

市場プレーヤー密度とは、特定の市場または業界内で活動している企業または会社の分布を指します。これは、特定の市場スペースに、その市場規模または総市場価値に対してどれだけの競合相手 (市場プレーヤー) が存在するかを示します。

バイオプロダクション市場で事業を展開している主要企業は次のとおりです。

- サーモフィッシャーサイエンティフィック

- メルク

- F.ホフマン・ラ・ロシュ株式会社

- バイオ・ラッド・ラボラトリーズ

- ロンザグループAG

免責事項:上記の企業は、特定の順序でランク付けされていません。

- バイオプロダクション市場のトップキープレーヤーの概要を入手

業界の発展と将来の機会:

バイオ生産市場で活動する主要企業によるさまざまな戦略的展開を以下に示します。

- 2023年3月、ロンザは、スイスのフィスプに計画していたcGMP臨床および商業用医薬品生産ラインが完成したと発表しました。この新ラインは、臨床用と商業用の両方の医薬品の幅広い生産需要を持つ顧客に対応することになります。この1,200平方メートルのcGMP施設には、無菌製品の製造に関するGMP Annex 1の要件を満たす、複数のモダリティに対応する最新の液体および凍結乾燥バイアル充填アイソレーターラインがあります。このラインはすでに完全に稼働しており、cGMPライセンスを取得しています。2023年4月に、最初の顧客バッチが充填される予定です。

- バイオ生産および細胞治療製造用の無血清および化学的に定義された細胞培養培地の開発と製造の世界的リーダーであるFUJIFILM Irvine Scientific Incは、2022年5月に中国蘇州新区にイノベーションおよびコラボレーションセンターが完成したことを発表しました。

- 2021年12月、バイオ製造および細胞療法製造用の無血清および化学的に定義された細胞培養培地の開発と製造の世界的リーダーであるFUJIFILM Irvine Scientific Incは、中国の蘇州新区にイノベーションおよびコラボレーションセンターを設立すると発表しました。この新しいセンターを通じて、専門家は顧客と協力して、バイオ製造のニーズを満たす上流の細胞培養プロセスを設計します。

- 2023年3月、BiVACOR IncのCormorant Asset ManagementとOneVenturesは、OneVentures Healthcare Fund IIIを通じて、同社に1,800万米ドルの資本金を拠出しました。この資金は、重要な幹部の雇用、進行中の研究開発、および人体実験での早期実現可能性調査の支援に役立ちます。この資金援助を使用して、同社は事業規模を2倍にする取り組みの一環として、研究開発の専門家や経営幹部などの重要な役割の候補者を採用します。BiVACOR Incはさらに、2023年末までにヒトを対象とする完全人工心臓の早期実現可能性調査を初めて実施したいと考えています。

競争環境と主要企業:

Lonza Group AG、bbi-biotech GmbH、Danaher Corp、Sartorius AG、FUJIFILM Irvine Scientific Inc、Thermo Fisher Scientific Inc、Merck KGaA、F. Hoffmann-La Roche Ltd、Bio-Rad Laboratories Inc は、バイオ製造市場の著名な企業です。これらの企業は、新しい技術、既存製品のアップグレード、および世界中で高まる消費者の需要を満たす地理的拡大に重点を置いています。

ムリナル氏は、ライフサイエンス分野の市場インテリジェンスとコンサルティングで8年以上の経験を持つ、経験豊富なリサーチアナリストです。戦略的な思考と揺るぎない卓越性へのコミットメントに基づき、医薬品市場予測、市場機会評価、業界ベンチマークの開発において深い専門知識を培ってきました。彼女の業務は、クライアントが情報に基づいた戦略的意思決定を行えるよう、実用的なインサイトを提供することに重点を置いています。

ムリナル氏の強みは、複雑な定量データセットを有意義なビジネスインテリジェンスへと変換することにあります。彼女の分析力は、医薬品および医療機器分野における市場開拓(GTM)戦略の策定と成長機会の発掘に大きく貢献しています。信頼できるコンサルタントとして、ワークフロープロセスの合理化とベストプラクティスの確立に常に注力し、クライアントのイノベーションと業務効率の向上に貢献しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応