欧州ジェネリック医薬品市場の概要、成長、動向、分析、調査レポート(2025-2031年)

過去データ : 2021-2023 | 基準年 : 2024 | 予測期間 : 2025-2031ヨーロッパのジェネリック医薬品市場規模と予測(2021年 - 2031年)地域別シェア、トレンド、成長機会分析レポートの対象範囲:分子タイプ(抗うつ薬、抗ヒスタミン薬、鎮痛薬、抗生物質、抗ウイルス薬、利尿薬、その他)、適応症(代謝性疾患、がん、免疫疾患、呼吸器疾患、心血管疾患、神経疾患、希少疾患、その他)、タイプ(処方薬およびOTC薬)、流通チャネル(病院薬局、小売薬局、オンライン薬局)

- レポート日 : Oct 2025

- レポートコード : TIPRE00040934

- カテゴリー : ライフサイエンス

- ステータス : 出版

- 利用可能なレポート形式 :

- ページ数 : 210

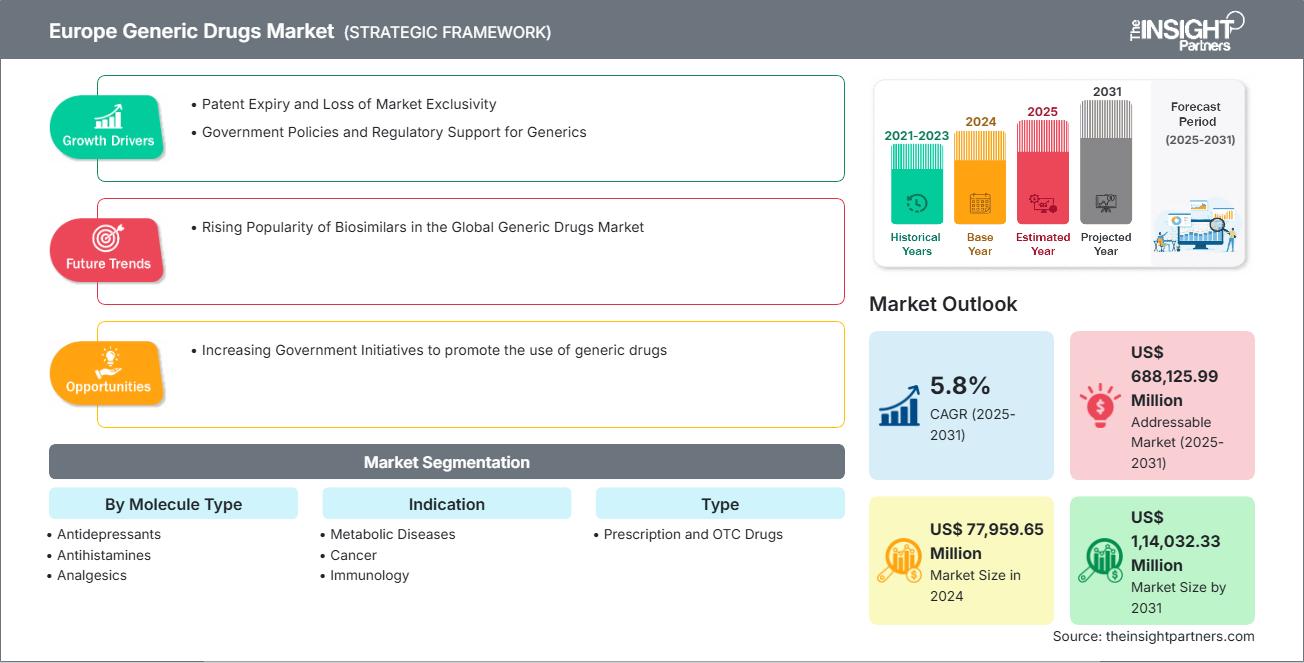

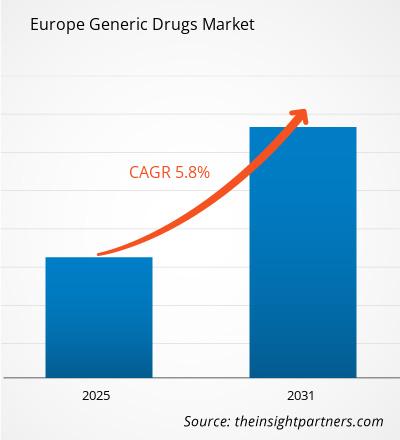

欧州のジェネリック医薬品市場規模は、2024年の779億5,965万米ドルから2031年には1140億3,233万米ドルに達すると予想されています。市場は2025年から2031年にかけて5.8%のCAGRを記録すると予測されています。

エグゼクティブサマリーと欧州ジェネリック医薬品市場分析:

欧州のジェネリック医薬品市場は、確立された医療インフラ、高齢化社会、革新的治療法への投資増加に支えられ、力強い成長が見込まれています。欧州は依然として製薬企業やバイオテクノロジー企業の拠点であり、糖尿病やがんなどの慢性疾患の治療薬開発に積極的に取り組んでいます。WHOによると、2024年7月時点でWHO欧州地域では成人約6,400万人、小児・青少年約30万人が糖尿病を患っており、3分の1は未診断です。そのため、ジェネリック医薬品などの手頃な価格の治療ソリューションに対する明確なニーズが生じています。2045年までには欧州人の10人に1人が糖尿病を患う可能性があり、欧州は既に1型糖尿病の負担が世界で最も大きい地域です。がんも大きな健康問題であり、WHOは2022年には欧州で447万人以上の新規症例と約200万人のがん関連死を報告しています。人口の高齢化と慢性疾患率の上昇に伴い、費用対効果の高い代替薬の需要が高まっています。

要件に合わせてレポートをカスタマイズ

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

欧州ジェネリック医薬品市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

欧州ジェネリック医薬品市場のセグメンテーション分析:

ヨーロッパのジェネリック医薬品市場分析の導出に貢献した主要なセグメントは、分子タイプ、適応症、タイプ、流通チャネルです。

- 分子タイプに基づいて、欧州のジェネリック医薬品市場は、抗うつ薬、抗ヒスタミン薬、鎮痛薬、抗生物質、抗ウイルス薬、利尿薬、その他に分類されています。2024年には、抗生物質セグメントが市場最大のシェアを占めました。

- 欧州のジェネリック医薬品市場は、適応症別に、代謝性疾患、がん、免疫疾患、呼吸器疾患、心血管疾患、神経疾患、希少疾患、その他に分類されています。2024年には、がん領域が市場最大のシェアを占めました。

- 欧州のジェネリック医薬品市場は、種類別に処方薬と市販薬に分かれています。2024年には、処方薬セグメントが市場シェアを拡大しました。

- 欧州のジェネリック医薬品市場は、適応症別に、病院薬局、小売薬局、オンライン薬局に分類されます。2024年には、病院薬局セグメントが最大の市場シェアを占めました。

欧州ジェネリック医薬品市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2024年の市場規模 | 779億5,965万米ドル |

| 2031年までの市場規模 | 1,14,032.33百万米ドル |

| CAGR(2025年~2031年) | 5.8% |

| 履歴データ | 2021-2023 |

| 予測期間 | 2025~2031年 |

| 対象セグメント |

分子の種類別

|

| 対象地域と国 |

ヨーロッパ

|

| 市場リーダーと主要企業の概要 |

|

欧州ジェネリック医薬品市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

欧州のジェネリック医薬品市場は、消費者の嗜好の変化、技術の進歩、製品ベネフィットに対する認知度の高まりといった要因によるエンドユーザーの需要増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のためのイノベーション、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- ヨーロッパのジェネリック医薬品市場における主要プレーヤーの概要を入手

欧州ジェネリック医薬品市場の見通し

ジェネリック医薬品市場における大きなビジネスチャンスは、医療システムのデジタルトランスフォーメーションと公共調達プラットフォームの拡大から生まれており、特に発展途上国および中所得国において顕著です。政府や保険会社が価値に基づくケアの導入とコスト抑制に注力するにつれ、ブランド医薬品に代わる高品質で低コストの代替品への需要が高まっています。このトレンドは、ジェネリック医薬品メーカーにとって、国の医療サプライチェーンへの統合、一括入札の獲得、そして長期契約の確保といった機会をもたらします。

さらに、eファーマシーや遠隔医療プラットフォームの台頭により、特に医療サービスが行き届いていない地域や遠隔地において、ジェネリック医薬品の新たな販売チャネルが創出されています。デジタル配信への投資、現地の規制遵守の確保、官民連携の推進に取り組む企業は、これらのトレンドを活用してリーチを拡大し、ジェネリック医薬品を第一選択薬として信頼を築くことができます。

欧州ジェネリック医薬品市場の国別分析

国別に見ると、ヨーロッパのジェネリック医薬品市場は、英国、ドイツ、フランス、イタリア、スペイン、そしてその他ヨーロッパ諸国で構成されています。2024年にはその他ヨーロッパ諸国が最大のシェアを占めました。

ノルウェー、デンマーク、スウェーデン、ポーランド、ウクライナ、ルーマニア、ベルギー、チェコ共和国は、その他欧州地域のジェネリック医薬品市場で主要な国です。この地域は、医療需要の増加、コスト抑制政策、慢性疾患負担の拡大により、着実な成長を遂げています。これらの国々は、堅牢な医療インフラ、バイオテクノロジーへの投資の増加、公的機関と民間セクターのプレーヤー間の積極的な協力の恩恵を受けています。国家医療予算への圧力が高まる中、ジェネリック医薬品は、手頃な価格で持続可能な医薬品へのアクセスを確保するための戦略的ソリューションとして採用されています。EUの医薬品エコシステムで中心的な役割を果たしているオランダやベルギーなどの国々は、高い水準のケアを維持しながら治療費を管理するため、ジェネリック医薬品やバイオシミラーの使用をますます支持しています。主な需要促進要因は、がんや肝炎などの慢性疾患の罹患率の増加です。ユーロスタットによると、2021年にEU加盟国で死亡した人の26%以上ががんによるもので、デンマークでは28.2%、アイルランドでは27.7%、スロベニアでは27.1%、オランダでは26.6%でした。これらの国では、新規がん症例も相当数報告されており、デンマークでは48,840人、アイルランドでは31,242人、スロベニアでは14,402人、オランダでは132,319人でした。こうした統計は、費用対効果の高い治療選択肢の必要性を浮き彫りにしており、ジェネリックの抗がん剤は国民保健システムにおいてますます重要な役割を果たすようになっています。並行して、地元企業は低コストの医薬品開発におけるイノベーションを強化しています。例えば、AstriVax Therapeutics(ベルギー)は主にワクチン開発に重点を置いていますが、この地域の科学力を示す好例です。AstriVaxなどの企業はジェネリック医薬品を直接製造しているわけではありませんが、近い将来、ジェネリック生物製剤やバイオシミラーの開発にも活用できる強力なバイオテクノロジー環境を浮き彫りにしています。

欧州ジェネリック医薬品市場における企業プロファイル

市場で活動する主要企業には、Teva Pharmaceutical Industries Ltd、Viatris Inc、Dr. Reddy's Laboratories Ltd、Novartis AG、Sun Pharmaceutical Industries Ltd、AbbVie Inc、AstraZeneca Plc、Sanofi SA、Aurobindo Pharma Ltd、Glenmark Pharmaceuticals Ltdなどが挙げられます。これらの企業は、事業拡大、製品イノベーション、合併・買収といった様々な戦略を採用することで、革新的な製品を消費者に提供し、市場シェアを拡大しています。

ヨーロッパのジェネリック医薬品市場調査方法:

このレポートで提示されたデータの収集と分析には、次の方法論が採用されています。

二次調査

調査プロセスは、包括的な二次調査から始まります。社内外の情報源を活用し、各市場の定性データと定量データを収集します。一般的に参照される二次調査の情報源には、以下のようなものがあります(ただし、これらに限定されるものではありません)。

- 企業のウェブサイト、年次報告書、財務諸表、ブローカー分析、投資家向けプレゼンテーション。

- 業界の業界誌およびその他の関連出版物。

- 政府文書、統計データベース、市場レポート。

- 市場で活動している企業に特化したニュース記事、プレスリリース、ウェブキャスト。

注記:

企業プロフィールセクションに含まれるすべての財務データは米ドルに標準化されています。他の通貨で報告している企業については、該当年度の為替レートに基づいて米ドルに換算されています。

一次調査

Insight Partnersは、データ分析の検証と貴重な洞察を得るために、毎年、業界のステークホルダーや専門家を対象に多数の一次インタビューを実施しています。これらの調査インタビューは、以下の目的で実施されています。

- 二次調査からの調査結果を検証し、改良します。

- 分析チームの専門知識と市場理解を強化します。

- 市場規模、トレンド、成長パターン、競争力、将来の見通しに関する洞察を得ることができます。

一次調査は、Eメールや電話インタビューを通じて実施され、様々な地域にわたる様々な市場、カテゴリー、セグメント、サブセグメントを対象としています。調査対象者は通常、以下のとおりです。

- 業界の利害関係者: 副社長、事業開発マネージャー、市場情報マネージャー、全国販売マネージャー

- 外部専門家: 業界特有の専門知識を持つ評価専門家、リサーチアナリスト、主要オピニオンリーダー

ムリナル氏は、ライフサイエンス分野の市場インテリジェンスとコンサルティングで8年以上の経験を持つ、経験豊富なリサーチアナリストです。戦略的な思考と揺るぎない卓越性へのコミットメントに基づき、医薬品市場予測、市場機会評価、業界ベンチマークの開発において深い専門知識を培ってきました。彼女の業務は、クライアントが情報に基づいた戦略的意思決定を行えるよう、実用的なインサイトを提供することに重点を置いています。

ムリナル氏の強みは、複雑な定量データセットを有意義なビジネスインテリジェンスへと変換することにあります。彼女の分析力は、医薬品および医療機器分野における市場開拓(GTM)戦略の策定と成長機会の発掘に大きく貢献しています。信頼できるコンサルタントとして、ワークフロープロセスの合理化とベストプラクティスの確立に常に注力し、クライアントのイノベーションと業務効率の向上に貢献しています。

- 過去2年間の分析、基準年、CAGRによる予測(7年間)

- PEST分析とSWOT分析

- 市場規模価値/数量 - 世界、地域、国

- 業界と競争環境

- Excel データセット

最新レポート

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応

無料サンプルを入手 - 欧州ジェネリック医薬品市場

無料サンプルを入手 - 欧州ジェネリック医薬品市場