2030年インプラント医療機器市場レポート:セグメント、地域、動向、最近の動向、戦略的洞察

インプラント医療機器市場の規模と予測(2020年 - 2030年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:性質別(能動インプラントおよび受動インプラント)、製品タイプ別(診断および治療)、材料タイプ別(金属、セラミック、ポリマー)、用途別(整形外科インプラント、心血管インプラント、乳房インプラント、脳インプラントなど)、エンドユーザー別(病院、専門クリニック、ASCなど)

- ステータス : 出版

- レポートコード : TIPMD00002673

- カテゴリー : ライフサイエンス

- ページ数 : 207

- 利用可能なレポート形式 :

- 最終更新日 : June 13, 2024

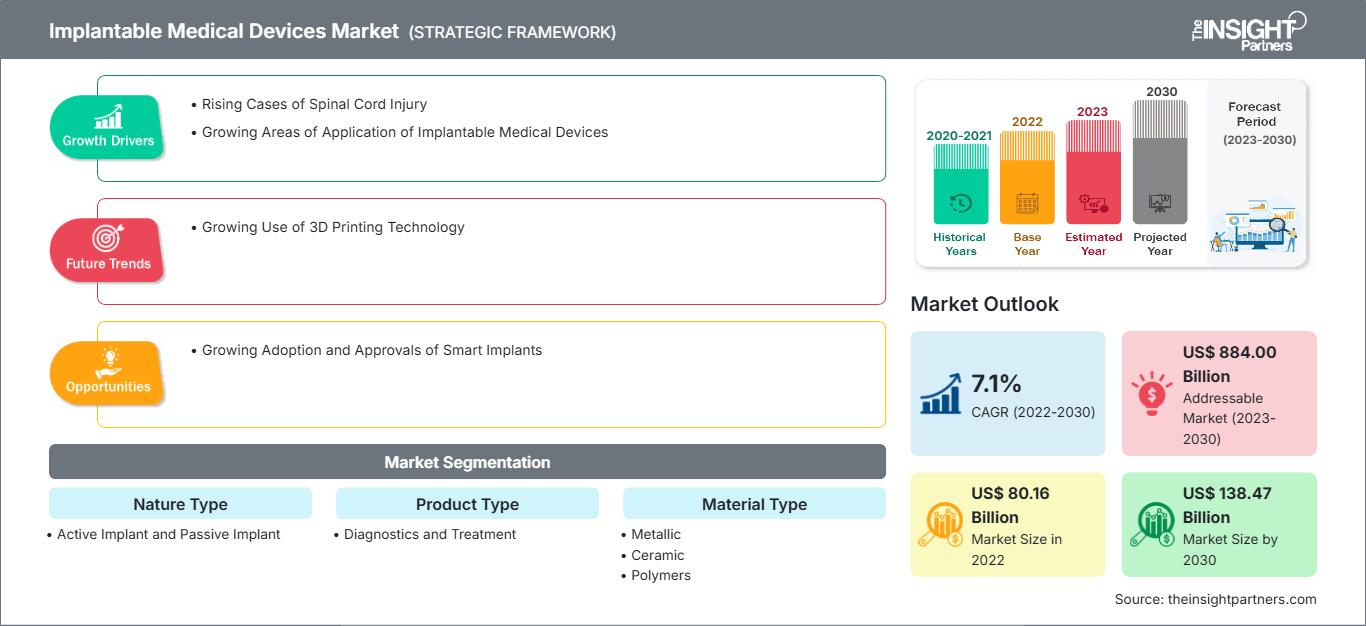

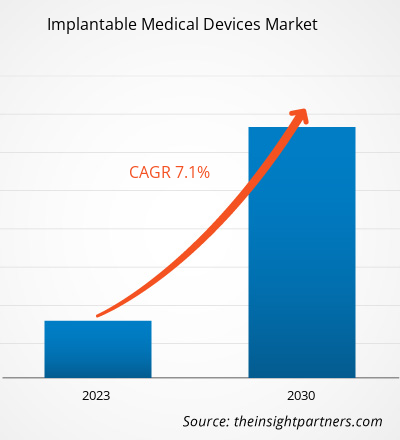

[調査レポート] インプラント医療機器市場は、2022年の801億5,600万米ドルから2030年には1,384億7,435万米ドルに成長すると予想されています。また、2022年から2030年にかけて7.1%のCAGR(年平均成長率)を記録すると予想されています。

市場分析とアナリストの見解:

インプラント医療機器とは、体内に完全にまたは部分的に埋め込まれる機器です。これらの医療機器は、医師による外科手術中に埋め込まれることがよくあります。外科手術用医療機器と比較すると、インプラント医療機器は手術後も体内に残ります。埋め込み型医療機器市場の成長を牽引する主な要因としては、埋め込み型医療機器の適用分野の拡大と脊髄損傷の増加が挙げられます。

成長の牽引要因と抑制要因:

WHOによると、2022年には米国でてんかん症例が5,000万件、片頭痛症例が10億件、脊髄損傷症例が40万件記録されました。脊髄刺激療法は、主に脊髄神経が痛みの感覚を制御する解剖学的および機能的能力を持っているため、慢性的な腰痛の治療において最も好まれる技術の1つです。脊髄損傷の発生率は過去10年間で急増しています。国立脊髄損傷統計センター(NSCISC)の2021年ファクトシートによると、脊髄損傷の年間発生率は100万人あたり60件です。 2022年4月に発表された論文「外傷性脊髄損傷の疫学:大規模人口ベース研究」によると、2021年における外傷性脊髄損傷の年齢・性別標準化発生率は人口100万人あたり26.5人で、男女ともに年齢と相関関係にあることが示されています。同じ情報源によると、高齢者(65歳以上)では、男性100万人あたり59.2人、女性100万人あたり23.3人となっています。脊髄刺激装置は、脊椎手術に伴う術後疼痛の管理に広く使用されています。 「脊髄損傷の事実と統計」と題された報告書によると、2021年には年間17,700人のアメリカ人が脊髄損傷を患っており、そのうち78%が平均年齢43歳の男性です。高齢者や成人の脊髄損傷の発生率が高いことが、埋め込み型神経刺激装置の需要を高め、市場の成長を後押ししています。

埋め込み型医療機器の使用は、痛みや不快感を軽減すると同時に、可動性を回復させ、患者の健康状態を改善するため、命を救う可能性があります。しかし、矯正インプラント手術に伴う骨折固定、機器の故障、関節形成術の合併症(肩、肘、股関節、膝関節の脱臼など)など、いくつかの合併症があります。さらに、インプラントの拒絶反応、関節インプラントの感染症、血栓、関節インプラントの緩み、神経血管損傷などが、整形外科用インプラントに伴う合併症。

要件に合わせてレポートをカスタマイズ

レポートの一部、国レベルの分析、Excelデータパックなどを含め、スタートアップ&大学向けに特別オファーや割引もご利用いただけます(無償)

埋め込み型医療機器市場: 戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

さらに、静脈内および脊髄内の薬剤投与や、がん治療に関連する多様な併存疾患や合併症の管理のための様々なデバイスがあります。これらのデバイスには、中心静脈アクセスデバイス(CVAD)、心臓植え込み型電子機器(CIED)、オマヤリザーバー、体外脳室ドレーン(EVD)、乳房インプラントと組織拡張器(TE)、経皮的腎瘻チューブ(PCNT)などがあります。

これらのデバイスに関連する感染症は一般的であり、医療費の増加や患者の腫瘍管理における短期的および長期的な合併症につながります。これは通常、感染症が治癒するまで、その後のがん治療の遅延につながります。これらの感染症の治療とデバイスの交換または除去がしばしば必要になります。しかし、インプラントの除去は困難な場合があり、患者の基礎疾患である血小板減少症、併存疾患、血管アクセスの欠如、免疫抑制、過去の外科的介入などにより、除去が不可能となる場合もあります。また、これらの感染症の治療に対する償還額は低いため、術後合併症が市場の成長を阻害しています。

レポートのセグメンテーションと範囲:

世界のインプラント医療機器市場は、性質、製品タイプ、材料タイプ、用途、およびエンドユーザーに基づいて分類されています。性質に基づいて、インプラント医療機器市場は能動インプラントと受動インプラントに分かれています。製品タイプに基づいて、インプラント医療機器は診断用と治療用に分けられます。材料タイプに基づいて、市場は金属、セラミック、およびポリマーに分割されています。アプリケーション別に見ると、埋め込み型医療機器市場は、心血管インプラント、整形外科用インプラント、心血管インプラント、乳房インプラント、義肢インプラント、脳インプラント、その他に分類されています。エンドユーザー別に見ると、市場は病院、専門クリニック、ASC、その他に分類されています。地域別に見ると、埋め込み型医療機器市場は、北米(米国、カナダ、メキシコ)、欧州(ドイツ、フランス、イタリア、英国、ロシア、その他欧州)、アジア太平洋(オーストラリア、中国、日本、インド、韓国、その他アジア太平洋)、中東およびアフリカ(南アフリカ、サウジアラビア、UAE、その他中東およびアフリカ)、南アフリカおよび中央アフリカ(California)に分類されています。中央アメリカ(ブラジル、アルゼンチン、その他中南米)。

セグメント分析:

埋め込み型医療機器市場は、その性質上、能動インプラントと受動インプラントの2つに分けられます。受動インプラントセグメントは2022年に大きな市場シェアを占めました。ただし、能動インプラントセグメントは2022~2030年に高いCAGRを記録すると予想されています。受動インプラントには電子部品や磁気部品がなく、機能するために外部電源を必要としません。受動インプラントの例には、カテーテル、電気リード、動脈瘤クリップ、ステント、外部固定器具、人工股関節、下大静脈(IVC)フィルターなどがあります。MRIは、加熱、回転、変位、磁化などのメカニズムを通じて受動インプラントに影響を及ぼす可能性があります。

埋め込み型医療機器市場は、製品タイプ別に、診断と治療の2つに分けられます。また、同セグメントは2022年から2030年にかけて高いCAGRを記録すると予想されています。埋め込み型医療機器は、薬剤を送達し、特定の臓器の機能をサポートするために体内に埋め込まれます。埋め込み型医療機器は、心臓疾患の治療に一般的に使用されています。さらに、整形外科用インプラントや歯科用インプラントなど、さまざまな種類の義肢が、損傷した身体の一部を置き換えるために使用されます。

埋め込み型医療機器市場は、材料タイプ別に、金属、セラミック、ポリマーに分類されています。金属セグメントは2022年に最大の市場シェアを占め、ポリマーセグメントは2022年から2030年にかけて最高のCAGRを記録すると予想されています。金属インプラントは、歯科、心臓デバイス、整形外科手術、婦人科手術で広く使用されています。例えば、コバルト-クロム-モリブデン合金は、整形外科用インプラントや義歯フレームワークに使用されています。同様に、コバルトとその合金は除細動器の製造に使用されています。さらに、エチレン酢酸ビニルコポリマー(EVA)、シリコーン、ポリエーテルエーテルケトン(PEEK)ポリマー、超高分子量ポリエチレン(UHMW-PE)などのポリマーは、製造の容易さ、柔軟性、生体適合性のため、医療用インプラントの製造に広く使用されています。

インプラント型医療機器市場は、用途別に、歯科インプラント、整形外科用インプラント、心血管インプラント、乳房インプラント、脳インプラント、その他に分類されています。整形外科用インプラントセグメントは2022年に最大の市場シェアを占め、同じセグメントは2022~2030年に最高のCAGRを記録すると予想されています。整形外科用インプラントは、変形または損傷による軟骨、骨、または関節の置換に使用されます。ほとんどの整形外科用インプラントはチタン合金とステンレス鋼で作られており、いくつかはプラスチックで覆われている場合もあります。プラスチックのライニングは人工軟骨として機能し、金属構造はインプラントに必要な強度を提供します。通常、インプラントは所定の位置に固定され、骨がインプラントに成長して強度が向上するようにサポートします。チタンなどの金属合金は、膝関節や股関節の置換を含む人工器官として使用される整形外科用インプラントで最も一般的に使用される材料です。金属合金は、骨プレートや骨ネジにも使用されます。セラミックやポリマーは、整形外科用インプラントの合成に使用されるその他の材料です。

埋め込み型医療機器市場は、エンドユーザー別に、病院、専門クリニック、ASC、その他に分類されています。2022年には、病院セグメントが最大の市場シェアを占め、同じセグメントが2022~2030年の間に最高のCAGRを記録すると予想されています。

地域分析:

地理に基づいて、世界の埋め込み型医療機器市場は、北米、ヨーロッパ、アジア太平洋、南米および中米、中東およびアフリカの5つの主要地域に分類されています。 2022年、北米は世界のインプラント医療機器市場規模で最大のシェアを占めました。アジア太平洋地域は、2022年から2030年にかけて最も高いCAGRを記録すると予測されています。

米国は、2022年から2030年にかけてインプラント医療機器市場で最大のシェアを占めると予測されています。パーキンソン病などの神経疾患の発症率の上昇、神経疾患に対する意識の高まり、経頭蓋刺激装置の開発への投資の増加は、米国のインプラント医療機器市場全体を牽引する主な要因です。パーキンソン病の主な原因には、ドーパミン値の低下やその他の遺伝的要因があります。アルツハイマー病協会が発表した「2022年アルツハイマー病の事実と数字」と題された調査によると、2022年には65歳以上のアメリカ人約650万人がアルツハイマー病と診断されました。この数は2060年までに1,380万人に達すると予測されています。脳動脈瘤財団が2019年に発表したデータによると、米国では約600万人が未破裂の脳動脈瘤を患っています。また、年間の破裂率は10万人あたり約8~10人で、米国では約3万人が脳動脈瘤破裂を患っています。脳深部刺激(DBS)装置は、パーキンソン病に伴う振戦を効果的に抑制することが確認されています。

パーキンソン病財団によると、米国では約100万人がパーキンソン病を患っており、2030年までに120万人に増加すると予想されています。技術の進歩と新製品の発売が、埋め込み型医療機器市場を牽引しています。2020年1月、アボット社のInfinity DBSシステムは、パーキンソン病の治療薬として米国食品医薬品局(FDA)の承認を取得しました。このシステムは、パーキンソン病の症状に関連する脳の特定の領域、淡蒼球内(GPi)を標的とした治療を可能にします。したがって、神経疾患の罹患率の増加と技術の進歩が、米国の埋め込み型医療機器市場の成長を促進しています。

業界の発展と将来の機会:

世界の埋め込み型医療機器市場で事業を展開している主要企業によるさまざまな取り組みを以下に示します。

- 2023 年 8 月、Medtronic plc は、Inceptiv 閉ループ充電式脊髄刺激装置 (SCS) で CE (Conformite Europeenne) マーク承認を取得しました。これは、各人の独自の生物学的信号を感知し、必要に応じて刺激を瞬間ごとに調整して、日常生活の動作と調和した治療を維持する閉ループ機能を提供する最初の Medtronic SCS デバイスです。

- 2023 年 5 月、BIOTRONIK は、心臓リズム管理ポートフォリオに Amvia Sky と Amvia Edge を新たに追加すると発表しました。BIOTRONIK は、最新技術である Amvia Sky と Amvia Edge で CE マークを取得しました。

- デンツプライシロナは、左脚ペーシング用に承認された世界初のペースメーカーおよびCRT-Pです。Amvia SkyとAmvia Edgeは最先端のイノベーションを象徴し、最新の心臓病のトレンドを取り入れています。

- 2023年3月、デンツプライシロナはEVインプラントファミリーの最新メンバーであるDS OmniTaperインプラントシステムを発表しました。DS OmniTaperインプラントシステムは、デンツプライシロナのEVインプラントファミリーの実証済みの技術と、効率性と汎用性を実現する新機能を組み合わせた革新的なソリューションです。

- 2023年2月、メドトロニックは、突然の心停止につながる可能性のある危険なほど速い心拍リズムを治療するためのAurora EV-ICD MRI SureScan(血管外植込み型除細動器)およびEpsila EV MRI SureScan除細動リードでCE(Conformite Europeenne)マークを取得しました。 Aurora EV-ICDシステムは、従来のICDの救命効果に加え、リード(細いワイヤー)が心臓や静脈の外側に配置されるため、特定のリスクを回避できます。

- 2023年1月、アボットは、米国食品医薬品局(FDA)が、糖尿病の合併症である糖尿病性末梢神経障害(DPN)の痛みを伴う治療薬として、Proclaim XR脊髄刺激(SCS)システムを承認したと発表しました。Proclaim XR SCSシステムは、経口薬などの従来の治療法に代わる治療法を必要とするDPN患者の症状緩和に役立ちます。Proclaim XR SCSシステムによる治療を受ける人は、アボットのNeuroSphere Virtual Clinic(医師と遠隔でコミュニケーションを取り、治療の調整を受けることができるコネクテッドケアアプリ)も利用できるようになります。

インプラント医療機器市場の地域別分析

予測期間を通じてインプラント医療機器市場に影響を与える地域的な動向と要因については、The Insight Partnersのアナリストが詳細に解説しています。本セクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米におけるインプラント医療機器市場のセグメントと地域についても解説します。

インプラント医療機器市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| の市場規模 2022 | US$ 80.16 Billion |

| 市場規模別 2030 | US$ 138.47 Billion |

| 世界的なCAGR (2022 - 2030) | 7.1% |

| 過去データ | 2020-2021 |

| 予測期間 | 2023-2030 |

| 対象セグメント |

By 性質タイプ

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

インプラント医療機器市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

埋め込み型医療機器市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認知度の高まりといった要因によるエンドユーザーの需要増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のためのイノベーション、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- 入手 埋め込み型医療機器市場 主要プレーヤーの概要

競争環境と主要企業:

アボット・ラボラトリーズ、ボストン・サイエンティフィック、デンツプライ・シロナ、ジョンソン・エンド・ジョンソン、メドトロニック、インスティテュート・ストラウマン、スミス・アンド・ネフュー、バイオトロニックSE&Co、リヴァノヴァ、メドエル・エレクトロメディジン・ゲラーテGmbHは、インプラント医療機器市場で事業を展開する主要企業です。これらの企業は、世界中で高まる消費者需要に対応し、専門分野における製品ラインナップを拡大するため、新技術の導入、既存製品の改良、そして地理的拡大に注力しています。

ムリナル氏は、ライフサイエンス分野の市場インテリジェンスとコンサルティングで8年以上の経験を持つ、経験豊富なリサーチアナリストです。戦略的な思考と揺るぎない卓越性へのコミットメントに基づき、医薬品市場予測、市場機会評価、業界ベンチマークの開発において深い専門知識を培ってきました。彼女の業務は、クライアントが情報に基づいた戦略的意思決定を行えるよう、実用的なインサイトを提供することに重点を置いています。

ムリナル氏の強みは、複雑な定量データセットを有意義なビジネスインテリジェンスへと変換することにあります。彼女の分析力は、医薬品および医療機器分野における市場開拓(GTM)戦略の策定と成長機会の発掘に大きく貢献しています。信頼できるコンサルタントとして、ワークフロープロセスの合理化とベストプラクティスの確立に常に注力し、クライアントのイノベーションと業務効率の向上に貢献しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応