Flow Cytometry Segment to Lead Minimal Residue Disease Testing Market During 2023–2031

According to our new research study on “Minimal Residue Disease Testing Market Forecast to 2031 – COVID-19 Impact and Global Analysis – by Technique, Cancer Type, End Use, and Geography,” the market size is expected to grow from US$ 3.55 billion in 2023 to US$ 8.94 billion by 2031; it is projected to register a CAGR of 12.24% during 2023–2031. The market growth is attributed to the surging prevalence of cancer and the increasing use of next-generation sequencing technology. Further, rising investments and research and development (R&D) by companies are likely to offer opportunities for the market growth. However, complex regulatory framework, high cost, and unclear reimbursement scenarios and policies hinder the minimal residue disease testing market growth.

Patients achieving complete hematologic remission after blood cancer treatment may foster residual cancer cells in the bone marrow or peripheral blood. These cells can result in relapse, as they persist at levels so low that they cannot be detected by conventional cytomorphology. Similar is the case with several other cancer conditions, including solid tumors and multiple myeloma. Minimal residual disease testing is employed to detect and quantify cancer cells existing in small numbers in a patient's body. This testing is performed by using sensitive technologies such as polymerase chain reaction (PCR), next-generation sequencing (NGS), and flow cytometry to identify measurable residual disease at the molecular level. Minimal residual disease testing is clinically important because it helps monitor response to treatment, predicts risk of relapse, guides personalized therapies, and serves as an endpoint in clinical trials. Healthcare providers can strive for better patient outcomes and higher survival rates by identifying and addressing minimal residual disease. The minimal residue disease testing market report emphasizes the key factors impacting the market and showcases the developments of prominent players.

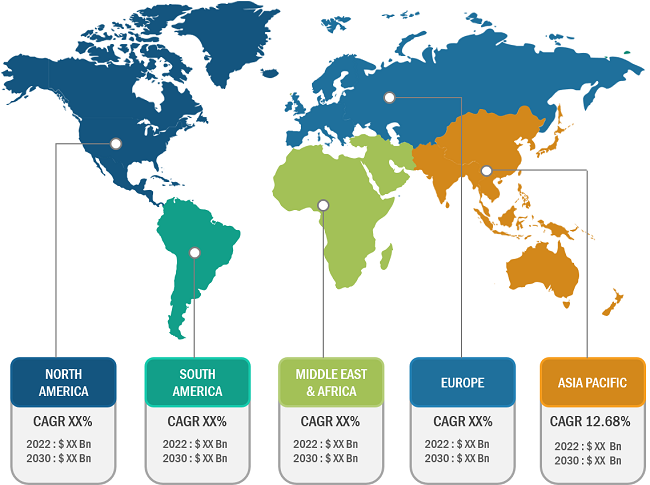

Minimal Residue Disease Testing Market, by Region, 2023 (%)

Minimal Residue Disease Testing Market Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Technique (Flow Cytometry, PCR, NGS, and Others), Cancer Type (Leukemia, Lymphoma, Solid Tumors, and Multiple Myeloma), End User (Hospitals, Specialty Clinics, Diagnostic Laboratories, and Others), and Geography (North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa)

Minimal Residue Disease Testing Market by Size, Share 2031

Download Free Sample

Source: The Insight Partners Analysis

Based on technique, the minimal residue disease testing market is segmented into flow cytometry, PCR, NGS, and others. The flow cytometry segment held the largest market share in 2023. However, the PCR segment is predicted to register the highest CAGR of 12.39% during 2023–2031. Based on end use, the market is segmented into hospitals, specialty clinics, diagnostic laboratories, and others. The hospitals segment held the largest minimal residue disease testing market share in 2023 and is estimated to register the highest CAGR of 12.79% during 2023–2031. Doctors and other professionals employed in hospitals can use their expertise to select appropriate minimal residual disease tests for patients. Factors leading to growth of the market for this segment include the increasing prevalence of the target disease, availability of multiple testing options, and introduction of new tests for better and more effective screening of patients. In addition, hospital facilities provide better decision-making capabilities, allowing doctors and healthcare professionals to analyze patients and offer them better treatment options.

Rising Use of Personalized Medicines for Treatment to Bring New Trends in Market in Coming Years

Personalized medicine is a novel and exciting approach emerging in the medical and healthcare industries. It focuses on studying a person's genome and determining a treatment based on their data. Personalized medicine for cancer patients involves studying individuals' genetic makeup to know tumor growth dynamics. Studying patients’ genetic makeup allows oncologists to customize treatments based on their specific genetic mutations. For instance, familial adenomatous polyposis (FAP) and hereditary nonpolyposis colorectal cancer (HNPCC) are two of the most common inherited colorectal cancer syndromes include. Determining the type of mutations in cancer patients provides crucial information on the treatment that fits the needs of patients.

In precision medicine, biomarker testing is performed to analyze the genetic makeup of a tumor. Test results also provide patients and their medical teams with important information about the type of treatment that could be the best fit for patients. Further, the development of next-generation sequencing technologies has made it possible to detect genetic changes associated with certain tumors with greater sensitivity. In November 2023, Invitae, a leading medical genetics company, launched its Invitae personalized cancer monitoring platform with enhanced chemistry specifications; the product helps detect circulating tumor DNA (ctDNA) as a malignancy biomarker. The detection of ctDNA can provide real-time insights into patient response or disease progression, aid in patient prognostic stratification, and enable early residual disease detection. Thus, the increasing use of personalized medicine is expected to lead to notable minimal residue disease testing market trends in the coming years.

Complex Regulatory Framework, High Cost, and Unclear Reimbursement Scenario and Policies Restrain Market Growth

The official and legal requirements for minimum residual tests are gaining stringency. The process of obtaining premarket approvals, particularly concerning 510(k) applications, has become more time-consuming and capital-intensive; the FDA faces challenges when there is no standardized method of measuring for an analyte. On the other hand, implementing MRD testing products in diagnostic laboratories requires large capital investments. For example, the cost of MRD testing products ranges from US$ 20,000 and US$ 50,000. In developing countries such as India and Brazil, small and medium-sized organizations and academic laboratories need more financial aid to afford advanced and expensive MRD kits. Moreover, the processes of paying for expensive molecular tests and interpreting test results as well as developing treatment programs are complicated and inconsistent. This is specifically problematic with more expensive modern methods such as liquid biopsy. The breakdown of molecular testing service costs is often unknown to physicians, pathologists, and patients despite completing invoicing or payments, which creates the need for clear conversation between patients and providers. Therefore, it becomes difficult to evaluate and keep track of the different insurance policies, which is expected to restrain the minimal residue disease testing market growth.

Key players identified and evaluated while performing minimal residue disease testing market analysis are Adaptive Biotechnologies; Natera; Bio-Rad Laboratories; F-Hoffmann La Roche Ltd; Guardant Health; LabCorp; Sysmex Corporation; ARUP Laboratories; Invivoscribe, Inc.; NeoGenomics Laboratories, Inc.; and Mission Bio, Inc.

The market, by technique, the market is segmented into flow cytometry, PCR, NGS, and others. The market, based on cancer type, is divided into leukemia, lymphoma, solid tumors, and multiple myeloma. In terms of end user, the market is categorized into hospitals, specialty clinics, diagnostic laboratories, and others.

The scope of the minimal residue disease testing market report encompasses North America (US, Canada, and Mexico), Europe (France, Germany, UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, India, Japan, Australia, South Korea, and Rest of Asia Pacific), the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America). North America holds the largest minimal residue disease testing market share. The minimal residue disease testing market size in North America is projected to reach US$ 2.34 billion by 2031; the market is expected to register a CAGR of 12.12% during 2023–2031. The market in Asia Pacific is expected to record the highest CAGR during the forecast period. The projected market growth in this region is attributed to the increasing incidence of hematological cancer, the surging geriatric population, and strategic initiatives taken to meet customer demand. China presents significant opportunities for the minimal residue disease testing market in Asia Pacific with increasing investments in screening and supportive reimbursement policies.

Contact Us

Phone: +1-646-491-9876

Email Id: sales@theinsightpartners.com