Torque Vectoring Market Trends, Share & Demand by 2034

Coverage: By Technology (Passive Torque Vectoring System (Ptvs), Active Torque Vectoring System (Atvs)); Propulsion (Rear-Wheel Drive (Rwd), Front-Wheel Drive (Fwd), All-Wheel Drive (Awd)); Electric Vehicle (Hybrid Electric Vehicle, Battery Electric Vehicle) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPAT00002317

- Category : Automotive and Transportation

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 27, 2026

2025 Market Size

US$ 11.0 Bn

Base year value

2034 Forecast

US$ 42.03 Bn

Projected by 2034

CAGR 2026-2034

16.0 %

Growth rate

Addressable Market

US$ 223.54 Bn

(2026-2034)

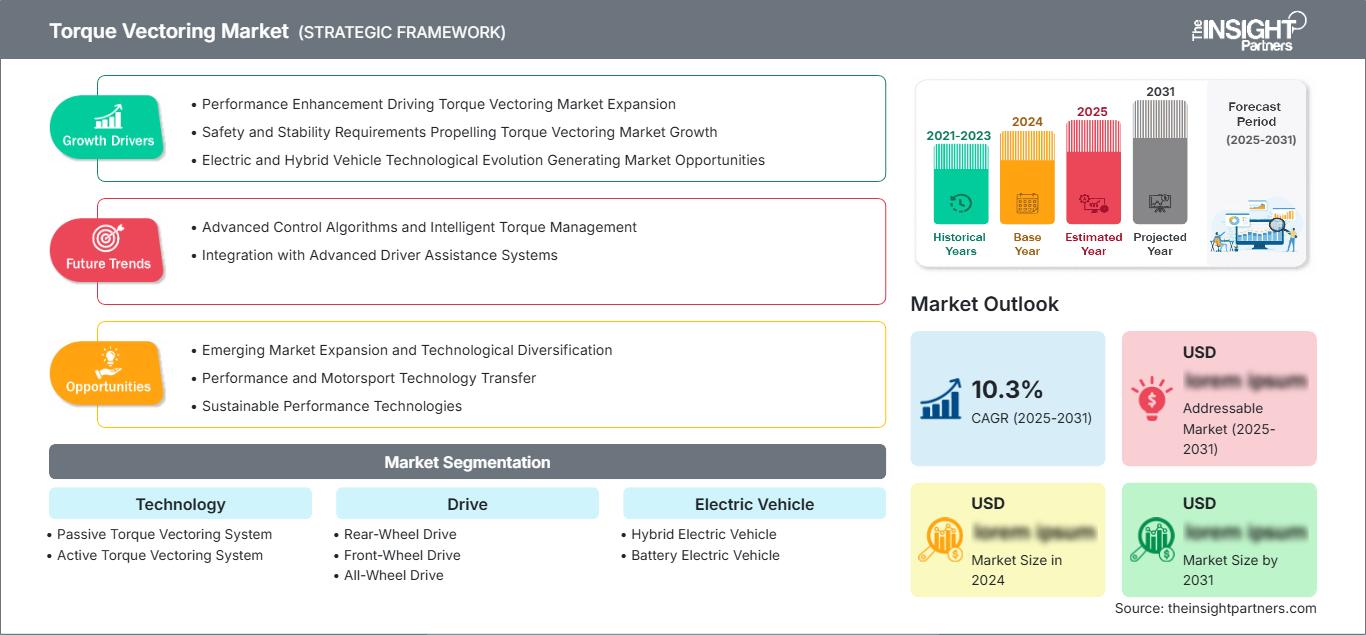

The global torque vectoring market size is projected to reach US$ 42.03 billion by 2034 from US$ 11 billion in 2025. The market is anticipated to register a CAGR of 16.0% during the forecast period 2026–2034.

Key market dynamics include the rapid global adoption of electric vehicles, where independent motor control enables highly precise power distribution, a heightening focus on active vehicle safety systems, and rising consumer expectations for superior handling in premium SUVs. Additionally, the market is expected to benefit from advancements in sensor fusion technology, the integration of torque management into autonomous driving suites, and the increasing use of software-defined drivelines that allow for over-the-air performance updates.

Torque Vectoring Market Analysis

The torque vectoring market analysis reveals a decisive shift toward electronically controlled and software-driven systems as manufacturers prioritize agility and energy efficiency. While traditional mechanical systems remain relevant for heavy-duty applications, electronic and brake-based solutions are dominating the high-volume passenger car segment. Strategic opportunities are emerging in the development of multi-motor e-axles, which eliminate the need for traditional differentials and provide instantaneous response. The analysis also notes that market expansion is heavily influenced by the luxury vehicle sector, where torque vectoring is a key performance differentiator. Competitive differentiation now depends on the ability to integrate torque distribution with electronic stability control and advanced driver assistance systems to provide a seamless, safe, and athletic driving experience in all weather conditions.

Torque Vectoring Market Overview

Torque vectoring systems have transitioned from specialized racing technology to essential components of modern vehicle dynamics. The torque vectoring includes a wide array of applications ranging from high-end active differentials to cost-efficient electronic brake-force distribution. Both Tier-1 automotive suppliers and technology-focused startups compete in this space, leveraging innovations in microelectronics and materials science. Growing demand for all-wheel drive stability among urban drivers in North America and Europe has bolstered the popularity of torque vectoring as a safety-first solution. Asia-Pacific leads in revenue due to its massive automotive production infrastructure, while Europe drives the market through its concentration of premium performance brands. The global market is further accelerated by the emergence of hyper-performance electric vehicles that utilize dedicated motors for each wheel to achieve unprecedented levels of cornering precision.

The US market is a major revenue contributor, anchored by widespread adoption of SUVs and light-duty pickups. Growth is driven by the rapid transition toward high-performance electric vehicles, extensive penetration of all-wheel drive systems, and a strong consumer preference for advanced safety features and personalized, software-enhanced driving dynamics.

Market Research Highlights

- Global market for Torque Vectoring was valued at US$ 11.00 Billion in 2025

- Annual market size is expected to reach US$ 42.03 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 223.54 Billion

- Market is anticipated to register a CAGR of 16% during the forecast period

- The United States represents a key market, supported by Performance Enhancement Driving Torque Vectoring Market Expansion, Safety and Stability Requirements Propelling Torque Vectoring Market Growth, Electric and Hybrid Vehicle Technological Evolution Generating Market Opportunities, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Emerging Market Expansion and Technological Diversification, Performance and Motorsport Technology Transfer, Sustainable Performance Technologies are expected to influence market dynamics and addressable market

- Report profiles industry participants, including American Axle and Manufacturing, Inc., BorgWarner Inc., Dana Incorporated, GKN, JTEKT Corporation, Magna International Inc., Prodrive, Robert Bosch GmbH, Schaeffler AG, ZF Friedrichshafen AG, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Torque Vectoring Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Torque Vectoring Market Drivers and Opportunities

Market Drivers:

- Proliferation of Electric and Hybrid Powertrains: Electric motors offer near-instantaneous torque response, making them the ideal platform for advanced torque vectoring. As the world shifts toward electrification, the natural compatibility between e-motors and vectoring software is driving significant volume growth.

- Increasing Safety and Stability Mandates: Global regulatory bodies are continuously tightening vehicle safety standards. Torque vectoring improves cornering stability and reduces the risk of skidding, helping manufacturers meet high safety ratings and consumer demand for secure handling.

- Growth of the Luxury and Performance SUV Segment: The global trend toward larger vehicles with higher centers of gravity has increased the need for technologies that maintain stability and car-like handling, sustaining demand for active torque management systems.

Market Opportunities:

- Integration with Autonomous Vehicle Sensors: Self-driving systems require precise control over vehicle path and orientation. Torque vectoring provides a critical layer of control that can be integrated with AI-driven path planning to improve safety in emergency maneuvers.

- Software-Defined Performance Upgrades: The rise of connected vehicles allows manufacturers to offer torque vectoring refinements and specialized driving modes as digital upgrades, creating new post-sale revenue streams.

- Expansion into Light and Heavy Commercial Segments: There is a growing opportunity to apply torque vectoring to commercial fleets to improve fuel efficiency through optimized power delivery and enhance safety for vehicles carrying shifting loads.

Torque Vectoring Market Report Segmentation Analysis

The Torque Vectoring Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Technology:

- Passive Torque Vectoring System: Primarily uses the existing braking system to slow down the inner wheel during a turn. This cost-effective solution is widely adopted in mid-range passenger vehicles to improve agility without adding heavy mechanical components.

- Active Torque Vectoring System: Features dedicated electronic or hydraulic clutches and actuators to actively transfer power between wheels. This segment is the primary driver of performance in the luxury and electric vehicle markets.

By Drive:

- All-Wheel Drive: The largest segment by volume, as these systems benefit most from the ability to distribute torque across all four wheels for maximum traction in diverse environments.

- Front-Wheel Drive: Increasingly utilizing electronic vectoring to combat understeer, making mass-market hatchbacks and sedans feel more responsive and stable.

- Rear-Wheel Drive: A core segment for high-performance sports cars and luxury sedans where torque vectoring is used to optimize power delivery and enhance the athletic feel of the vehicle.

By Electric Vehicle:

- Battery Electric Vehicle: The fastest-growing sub-segment, where multi-motor configurations allow for software-controlled torque vectoring at each wheel, significantly enhancing both performance and energy regeneration efficiency.

- Hybrid Electric Vehicle: Utilizes a combination of traditional mechanical systems and electric motor assistance to provide balanced torque distribution, appealing to consumers seeking both efficiency and high-end driving dynamics.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Torque Vectoring Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 11.0 Billion |

| Market Size by 2034 | US$ 42.03 Billion |

| Global CAGR (2026 - 2034) | 16.0% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Technology

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Torque Vectoring Market Players Density: Understanding Its Impact on Business Dynamics

The Torque Vectoring Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Torque Vectoring Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years, serving as the primary hub for electric vehicle innovation and high-volume automotive production. Emerging markets in South & Central America, the Middle East, and Africa also present significant untapped opportunities for performance-oriented drivetrain components as infrastructure improves and demand for stable, all-weather vehicles rises.

The torque vectoring market is undergoing a significant transformation, moving from a niche performance feature for sports cars to a global safety and efficiency standard for mass-market electric and premium vehicles. Growth is driven by the rapid expansion of dual-motor EV platforms, a surge in demand for active safety systems, and the global popularity of the SUV segment. Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds a substantial share, driven by the widespread adoption of All-Wheel Drive (AWD) SUVs, pickup trucks, and high-end electric vehicles.

- Key Drivers:

- Rising consumer preference for advanced stability control in harsh weather conditions.

- Presence of leading EV innovators and a robust market for performance-oriented luxury crossovers.

- Increased integration of software-defined drivelines that allow for handling-on-demand features.

- Trends: Scaling of dual-motor electric drivetrains in light-duty trucks and the successful adoption of over-the-air (OTA) software updates to refine vehicle dynamics.

2. Europe

- Market Share: Holds the largest high-value share globally, anchored by a dense concentration of premium automotive manufacturers in Germany, Italy, and the UK.

- Key Drivers:

- High domestic consumption of performance brands like BMW, Audi, and Mercedes-Benz, which utilize torque vectoring as a core differentiator.

- Established processing infrastructure for high-precision active differentials and electronic clutch systems.

- Stringent Euro NCAP safety standards favoring advanced electronic stability control (ESC) enhancements.

- Trends: A strategic shift toward e-vectoring for high-margin electric hypercars and a growing focus on brake-free torque distribution to improve energy efficiency in long-range EVs.

3. Asia-Pacific

- Market Share: The fastest-growing region, with China acting as the primary engine for the entire continent, particularly in the mass-market electric vehicle segment.

- Key Drivers:

- Massive consumer base seeking premium, high-tech features in affordable electric and hybrid sedans.

- Government-supported industrial initiatives focused on high-value smart mobility and domestic parts manufacturing.

- Rapid urbanization leading to a preference for compact, agile vehicles equipped with electronic torque-management systems.

- Trends: Heavy reliance on local supplier ecosystems and B2B contracts for integrated e-axles used in the rapidly expanding domestic SUV market.

4. South and Central America

- Market Share: Emerging market with a growing demand for stable utility vehicles in countries like Brazil and Argentina.

- Key Drivers:

- Increasing awareness of vehicle safety and the benefits of torque-selective braking for rugged terrain.

- Modernization of regional assembly plants to include global drivetrain standards for export and domestic use.

- Rising interest in sporty crossovers among middle-to-high income urban segments.

- Trends: Growth of brake-based vectoring solutions as a cost-effective way to offer premium handling in regional vehicle models.

5. Middle East and Africa

- Market Share: Developing market with deep-seated interest in high-performance luxury SUVs and specialized off-road vehicles.

- Key Drivers:

- Traditional demand for powerful AWD systems capable of navigating desert and arid climates.

- Strategic investments in smart city infrastructure and high-end automotive retail in the Gulf region.

- High demand for durable, active-differential systems in the premium utility segment.

- Trends: Implementation of modern electronic control units (ECUs) to improve the maneuverability of heavy armored and luxury desert-touring vehicles.

High Market Density and Competition

The competitive landscape is dominated by Tier-1 suppliers who provide integrated drivetrain solutions to global OEMs. Market leaders focus on miniaturization, software integration, and the development of high-speed actuators.

This competitive environment pushes vendors to differentiate through:

- Hardware and Software Synergy: Leading players are developing proprietary algorithms that work in tandem with lightweight actuators to provide smoother and faster torque transitions.

- E-Axle Integration: Suppliers are increasingly offering all-in-one electric drive units that include the motor, transmission, and torque vectoring hardware in a single compact package.

- Sustainability and Efficiency: Companies are focusing on reducing the parasitic power loss of torque vectoring systems to maximize the range of electric and hybrid vehicles.

Opportunities and Strategic Moves

- Partner with high-end EV startups and established OEMs to tap into the surging demand for independent-motor control and smart drivetrains in the North American and Asian markets.

- Incorporate lightweight materials and energy-efficient designs to appeal to environmentally conscious manufacturers seeking to maximize electric range without sacrificing vehicle performance.

Major Companies operating in the Torque Vectoring Market are:

- American Axle and Manufacturing, Inc.

- BorgWarner Inc.

- Dana Incorporated

- GKN

- JTEKT Corporation

- Magna International Inc.

- Prodrive

- Robert Bosch GmbH

- Schaeffler AG

- ZF Friedrichshafen AG

Disclaimer: The companies listed above are not ranked in any particular order.

Torque Vectoring Market News and Recent Developments

- In February 2026, BorgWarner secured a new electric cross differential (eXD) program with a leading Chinese original equipment manufacturer (OEM). The eXD solution is designed for a 48V system and is integrated with the customer’s 48V electrical and electronic (E/E) architecture. This program represents BorgWarner’s first 48V eXD application within its global portfolio and expands the company’s torque management capabilities for electric vehicles.

- In May 2024, BorgWarner is first-to-market with its electric Torque Vectoring and Disconnect (eTVD) system for battery electric vehicles (BEVs) with launches for Polestar and an additional major European OEM. The eTVD is part of BorgWarner’s electric torque management system (eTMS) solutions portfolio, which is designed to intelligently control wheel torque to increase stability, provide superior dynamic performance, and improve traction during launch and acceleration. The eTVD is currently in production on the Polestar 3 SUV, and production for the major European OEM

Torque Vectoring Market Report Coverage and Deliverables

The Torque Vectoring Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Torque Vectoring Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Torque Vectoring Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Torque Vectoring Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Torque Vectoring Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends