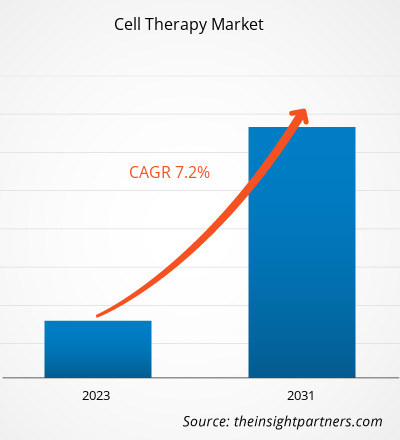

The cell therapy market size is projected to reach US$ 16.72 billion by 2031 from US$ 9.59 billion in 2023. The market is expected to register a CAGR of 7.2% during 2023–2031. Advancements in cell-based therapeutics and the introduction of novel products by key manufacturers will likely remain key trends in the cell therapy market.

Cell Therapy Market Analysis

Regenerative therapies induce the regeneration of cells, tissues, and organs, followed by aiding the restoration of their functions. According to the Alliance for Regenerative Medicine, 520 clinical trials utilizing cell therapy medicine were underway globally (192 Phase I, 125 Phase II, 36 Phase III) as of Q4 2023. Further, the approval and commercialization of Kymriah in 2017, the first cell therapy of its kind, is marked as a significant event contributing to the continued prominence of cell therapy in the field of cell and gene therapy (C>). The development of CAR-T cell (i.e., chimeric antigen receptor T cell) therapy has transformed the approach to the treatment of some cancers. CAR-T cell therapies have been the subject of the most research and innovation efforts worldwide; five additional products based on this technology, i.e., Yescarta, Abecma, Tecartus, Breyanzi, and Carvykti, have been approved for the treatment of various blood cancers. Thus, the expanding range of regenerative medicine applications fuels the cell therapy market growth.

Cell Therapy Market Overview

CAR T-cell therapy has been proven to be a promising method for treating cancer. Every year, a huge number of preclinical and clinical trials are conducted to study its use in newer therapeutic applications. In addition to autologous and allogeneic products, new in-vivo CAR-T cell gene therapies and their efficacy in indications other than hematologic malignancies are likely to be the prime focus of research in the future.

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Cell Therapy Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Cell Therapy Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Cell Therapy Market Drivers and Opportunities

Increase in Prevalence of Cancer Favors Market Growth

A sedentary lifestyle, changes in dietary habits, etc., are well-known risk factors for prominent chronic diseases such as neurological disorders, cancer, autoimmune diseases, and cardiovascular diseases. According to the Centers for Disease Control and Prevention, one or more chronic illnesses, including diabetes, cancer, heart disease, or stroke, affect 6 out of every 10 Americans. Chronic illnesses are among the main causes of death and disability in the US. Genetic predisposition, processed food, pollution, and altered lifestyles are the factors contributing to the surging prevalence of cancer. According to the American Cancer Society, nearly 19.3 million new cancer cases were registered globally in 2020. Cell therapy has emerged as a new cancer treatment method in the last few decades. T cells are modified in a laboratory setup and then administered into the body to target cancer cells. CAR-T cell therapy is employed to treat adult and pediatric leukemia cases, and a few types of lymphoma. Additionally, it is being researched as a potential treatment for other cancer conditions, including solid tumors developing in the chest. Thus, an increase in the number of patients suffering from cancer drives the demand for CAR-T cell therapies, thereby contributing to the growth of the cell therapy market.

Research and Development Funding

Researchers are motivated to investigate ways to enhance the effectiveness of cell therapy due to the complete response rates and progression-free survival observed in patients with relapsed/refractory malignancies who had received prior treatment. Researchers are looking into elements such as antigen loss that could lead to immune escape and are coming up with ways to deal with them. Designing cell therapies to simultaneously target several antigens is one beneficial approach. The California Institute for Regenerative Medicine (CIRM), the largest regenerative medicine organization in the world, has granted US$ 43.8 million to power initiatives supporting gene therapy and stem cell research in California. The award supports the projects in clinical, discovery, and infrastructure programs of the institute.

Cell Therapy Market Report Segmentation Analysis

Key segments contributing to the derivation of the cell therapy market analysis are therapy type, product, technology, application, and end user.

- Based on therapy type, the cell therapy market is divided into allogeneic and autologous. The allogeneic segment held a larger market share in 2023.

- By product, the market is segmented into consumables, equipment, and systems and software. The equipment segment held the largest share of the market in 2023.

- In terms of technology, the market is divided into viral vector technology, genome editing technology, somatic cell technology, cell immortalization technology, cell plasticity technology, and three-dimensional technology.

- By application, the market is segmented into oncology, cardiovascular, orthopedic, wound management, and other applications. The oncology segment held the largest share of the market in 2023.

- Based on end user, the cell therapy market is categorized into research institutes, hospitals, and others. The hospitals segment held the largest market share in 2023.

Cell Therapy Market Share Analysis by Geography

The geographic scope of the cell therapy market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America dominates the market. In North America, the US held the largest share of the cell therapy market in 2023. Market growth is attributed to the increased research and development, coupled with the surging adoption of cell therapies such as stem cell, gene, and immune therapies. Rising incidences of genetic and cellular disorders, and burgeoning focus on expanding the development and manufacturing capacities of cell therapies further favor the cell therapy market progress. Bayer AG has established its first Cell Therapy Launch Facility in Berkeley to enable the delivery of cell therapies to patients worldwide. The US$ 250 million, 100,000-square-foot facility will provide the materials needed for late-stage clinical trials to facilitate the commercial launch of bemdaneprocel (BRT-DA01), an experimental cell therapy being tested by BlueRock Therapeutics to treat Parkinson's disease and other conditions. Asia Pacific is anticipated to record the highest CAGR in the cell therapy market during the forecast period.

Cell Therapy Market Regional Insights

The regional trends and factors influencing the Cell Therapy Market throughout the forecast period have been thoroughly explained by the analysts at Insight Partners. This section also discusses Cell Therapy Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Get the Regional Specific Data for Cell Therapy Market

Cell Therapy Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 9.59 Billion |

| Market Size by 2031 | US$ 16.72 Billion |

| Global CAGR (2023 - 2031) | 7.2% |

| Historical Data | 2021-2022 |

| Forecast period | 2023-2031 |

| Segments Covered |

By Therapy Type

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

Cell Therapy Market Players Density: Understanding Its Impact on Business Dynamics

The Cell Therapy Market market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Market players density refers to the distribution of firms or companies operating within a particular market or industry. It indicates how many competitors (market players) are present in a given market space relative to its size or total market value.

Major Companies operating in the Cell Therapy Market are:

- Vericel Corporation

- MEDIPOST

- NuVasive Inc

- Mesoblast Limited

- JCR Pharmaceuticals Co. Ltd.

- Smith & Nephew

Disclaimer: The companies listed above are not ranked in any particular order.

- Get the Cell Therapy Market top key players overview

Cell Therapy Market News and Recent Developments

The cell therapy market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in cell therapy market are listed below:

- Ginkgo Bioworks, a company engaged in building a leading platform for cell programming and biosecurity, announced the acquisition of Modulus Therapeutics' cell therapy platform assets, including their CAR and switch receptor libraries. (Source: Ginkgo Bioworks Company Name, Press Release, 2024)

- AstraZeneca entered into a definitive agreement to acquire Gracell Biotechnologies Inc., a global clinical-stage biopharmaceutical company developing innovative cell therapies for the treatment of cancer and autoimmune diseases. (Source: AstraZeneca Company Name, Press ReleaseNewsletter, 2024)

Cell Therapy Market Report Coverage and Deliverables

The “Cell Therapy Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Cell therapy market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Cell therapy market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Cell therapy market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the cell therapy market

- Detailed company profiles

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Therapy Type, Product, Technology, Application, End User

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

Argentina, Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, Mexico, Saudi Arabia, South Africa, South Korea, Spain, United Arab Emirates, United Kingdom, United States

Get Free Sample For

Get Free Sample For