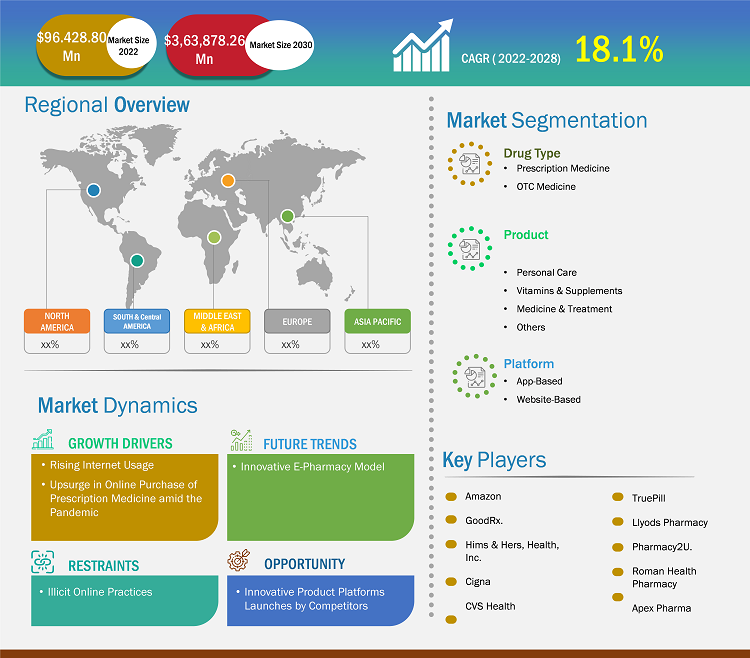

The digital pharmacy market size is expected to grow from US$ 96,428.80 million in 2022 to US$ 3,63,878.26 million by 2030; the market is estimated to register a CAGR of 18.1% from 2022 to 2030.

Analyst’s Viewpoint

The digital pharmacy market analysis explains market drivers such as rising internet usage, access to web-based and online services, and an upsurge in the online purchase of prescription medicines during the COVID-19 pandemic. Further, an innovative e-pharmacy model is expected to introduce new market trends during the forecast period. Based on drug type, the digital pharmacy market is bifurcated into prescription medicines and OTC medicines. The prescription medicine segment held a larger market share in 2022 and is anticipated to register a higher CAGR during 2022–2030. Based on product, the digital pharmacy market is segregated into personal care, vitamins and supplements, medicines and treatments, and others. The medicines and treatments segment held the largest market share in 2022. By platform, the digital pharmacy market is categorized into app-based and website-based. The app-based segment held a larger share of the market in 2022.

A digital pharmacy is a licensed pharmacy combining high-tech and efficient solutions by giving its services a personal touch, which helps commercialize new, existing, and digital therapies. The state-of-the-art solutions simplify the process of filling prescriptions, enhance stakeholders' experiences, and clarify the prescription journey with actionable insights for biopharma manufacturers. Digital pharmacies can help biopharma companies remove barriers, enabling dispensing pharmacies to receive clean and ready-to-dispense prescriptions.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Digital Pharmacy Market: Strategic Insights

Market Size Value in US$ 96,428.80 million in 2022 Market Size Value by US$ 3,63,878.26 million by 2030 Growth rate CAGR of 18.1% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Akshay

Have a question?

Akshay will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Digital Pharmacy Market: Strategic Insights

| Market Size Value in | US$ 96,428.80 million in 2022 |

| Market Size Value by | US$ 3,63,878.26 million by 2030 |

| Growth rate | CAGR of 18.1% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Akshay

Have a question?

Akshay will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Market Insights

Rising Internet Usage and Access to Web-Based Services & Online Services Propels Digital Pharmacy Market Growth

Health information technology (HIT) involves information processing through computer hardware and software, enabling the storage; retrieval; sharing; and use of healthcare information, data, and knowledge for communication and decision-making. For example, research published in a Centers for Disease Control and Prevention (CDC) report on HIT reveals that 74% of adults in the US use the Internet, among which 61% use the Internet to search for healthcare or medical information. Also, adults from the age group of 18–49 are more likely to utilize HIT than senior adults.

The National Institute of Health report reveals that the use of the Internet for purchasing products and services has risen over the past two decades. Also, there has been an increase in the trend of purchasing online medicines globally. Online medicine purchases have evolved in various ways with the introduction of different models worldwide due to diverse regulatory, economic, and cultural environments. For example, in the US, Internet pharmacies operate majorly as a prescription-based model, while in Europe, they operate via a non-prescription-based model.

Market Trend

Innovative E-Pharmacy Model

According to the Sustaining Health Outcomes through the Private Sector (SHOPS) Plus report published in December 2019, a project team in India has announced a partnership with the State Government of Madhya Pradesh and Medlife International (a pharma company) to launch an innovative, drug-to-doorstep e-pharmacy model as a part of the fight against tuberculosis (TB). The SHOPS Plus Prohect team has designed the service delivery model to strengthen the TB services through an e-pharmacy model/platform. Despite the mitigating TB epidemic in India, the country still holds the most significant number of TB patients, with half a million cases carried undiagnosed annually. Therefore, SHOP Plus is working to utilize technology to provide diagnosis and treatment support services at the patient's doorstep through an e-pharmacy model. With advancements in e-pharmacy platforms designed by the SHOP Plus project, doctors can prescribe home sputum testing materials for TB patients, and the test can be performed remotely. An agent from an e-pharmacy would pick up these materials and deliver them to the lab facility. After processing the sputum material, the lab would upload the patient's report on the e-pharmacy platform. TB patients can view the report, and physicians can prescribe the treatment for the patient accordingly. The e-pharmacy platform also features communication technology to follow up with patients' treatment adherence and future orders. Such innovative e-pharmacy models are likely to provide a lucrative opportunity for the growth of the digital pharmacy market during the forecast period.

Report Segmentation and Scope

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Drug Type-Based Insights

Based on drug type, the digital pharmacy market is bifurcated into prescription medicine and OTC medicine. The prescription medicine segment held the largest market share in 2022 and is anticipated to register the highest CAGR for the forecast period 2022–2030. A doctor fills out a digital prescription online and sends it directly to prescription centers over the internet. Prescription centers are electronic databases that issue and process medicines, baby food, and medical devices. Prescriptions are by default public, but they can only be changed by the concerned doctor. In the private prescription, only patients are allowed to purchase prescribed medicines, while in the authorized prescription, prescription medicines can be purchased at a pharmacy by the patient or by people authorized by the patient on the online portal. Individuals purchasing the prescribed medicines need to show the pharmacist their identity documents, including a photograph and an identification number. If the medicine is purchased for another person, the buyer must also know their personal identification number. Post buyers’ verification, pharmacists would locate the correct prescription in the prescription center based on the buyer's identification code (mentioned in the prescription).

Product-Based Insights

Based on product, the digital pharmacy market is segregated into personal care, vitamins and supplements, medicine and treatment, and others. The medicine & treatment segment held the largest market share in 2022. "Express Scripts" offered by Cigna provides home delivery for medicines. Express Scripts Pharmacy has made it easy for consumers to order or renew prescriptions by reducing waiting time at stores. The platform allows transferring prescriptions, easily tracking orders, and interacting with pharmacists. It also offers free standard shipping along with a hassle-free automatic refill program, helpful digital tools to make it easier to keep track of medications, and 24×7 access to pharmacists.

Platform-Based Insights

In terms of platform, the digital pharmacy market is categorized as app-based and website-based. The app-based segment held a larger share of the market in 2022 and is anticipated to register a higher CAGR during 2022–2030. Mobile device technologies have led to remarkable advancements in the healthcare sector. For example, rising smartphone users with internet connectivity, customers are getting discounts on prices, home delivery, and easy access to online pharmacies. "Closeloop," a leading medicine delivery app, provides consumers with the ability to search or filter out medicines [prescription-based or over-the-counter (OTC)], upload prescriptions, make online transactions and payments, set reminders, and get refilling and re-ordering done. Therefore, companies designing innovative apps for e-pharmacies provide easy access to consumers to allow them to order medicines through online channels.

Surgical Navigation Systems Market, by Drug Type – 2022 and 2030

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

Regional Analysis

North America accounts the largest share for the digital pharmacy market. The market in North America is subsegmented into the US, Canada, and Mexico. The US holds the largest share of the digital pharmacy market in this region. Several start-ups in the US have entered the online pharmacy space after receiving substantial venture capital funding. For example, Amazon, an e-commerce giant, has partnered with different online pharmacies to enter into the e-pharmacy segment, while many physical stores are launching their online services. Small pharmacies and distributors in the US have established online shops, which have reported small-scale online sales. An upsurge in the popularity of online platforms and e-commerce has triggered the digitalization of pharmacy [prescription drugs and over-the-counter (OTC) medication] in the US.

Nimble, formerly operating as a conventional physical pharmacy, is now adapting to online presence. The company raised ~US$ 60 million in funding from Y Combinator, Sequoia Capital, DAG Ventures, First Round Capital, and Khosla Ventures. It further seeks to partner with physical pharmacies to offer delivery services. In 2020, Walmart acquired the startup CareZone and purchased its prescription management technology to make Walmart’s online channel more competitive. The CareZone mobile app helps individuals and families manage a variety of chronic illnesses and medications. Families can access their insurance information and scan labels, aiding speedy and convenient operations. Through this acquisition, Walmart plans to boost its digital health and wellness tools.

The majority of people in the US live within 5 miles of community pharmacies, but rural and urban patients have difficulty accessing pharmacy services. Moreover, store shutdowns, transportation problems, disability related problems, and economic challenges further hamper the access to medicines, leading to pharmacy deserts, as stated by the US Department of Agriculture. A study published in 2023 in the Journal of the American Medical Association reported that states that adopted telepharmacy policies experienced a decrease in pharmacy deserts, and telepharmacies are virtually closer to people with high medical needs than traditional pharmacies. There are currently 28 states in the US that permit the practice of telepharmacy, with differing statuses and regulations.

The integration of artificial intelligence (AI) and machine learning allows the automation of processes such as medication monitoring, smart reminders, and personalized treatment recommendations. Moreover, the advent of advanced communication platforms and the integration of augmented reality (AR) and virtual reality (VR) with telepharmacy has the potential to revolutionize medicine dispensation, consultations, and patient care, in turn, addressing the surging demands for convenient healthcare services.

The report profiles leading players operating in the global digital pharmacy market. These include Amazon.com Inc, Goodrx Holdings Inc, the Cigna Group, CVS Health Corp, Walmart Inc, Hims & Hers Health Inc, Roman Health Pharmacy LLC, Apex Pharmacy Inc, LloydsPharmacy Ltd, Pharmacy2U Ltd, Docmorris NV, and Truepill. In September 2023, GoodRx announced a collaboration with MedImpact to offer a seamless experience for MedImpact members at pharmacy counters. Additionally, companies in collaboration plan to offer a program for seamless data integration. Based on MedImpact's rigorous drug safety review, the program would also notify patients about any negative drug interactions.

Company Profiles

- Amazon.com Inc

- Goodrx Holdings Inc

- The Cigna Group

- CVS Health Corp

- Walmart Inc

- Hims & Hers Health Inc

- Roman Health Pharmacy LLC

- Apex Pharmacy Inc

- LloydsPharmacy Ltd

- Pharmacy2U Ltd

- Docmorris NV

- Truepill

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Drug Type, Product, Platform, and Geography

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

The List of Companies - Digital Pharmacy Market

- Amazon.com Inc.

- Good Rx Holdings

- The Cigna Group

- CVS Health Corp

- Walmart Inc.

- Hims & Hers Health Inc.

- Roman Health Pharmacy LLC

- Apex Pharmacy Inc.

- LloydsPharmacy Ltd.

- Pharmacy2U Ltd.

- Docmorris NV

- Truepill

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Digital Pharmacy Market

Nov 2023

Emergency Call Systems Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Application (Fall Prevention and Detection, Workflow Optimization, Patient Care Reminders, Alarms and Communication Management, Wander Management, Reporting and Analytics, Real-Time Staff Locating, and Others), End User (Hospital and Clinics, Assisted Living and Independent Living Facilities, Ambulatory Surgical Centers, and Others), Technology (Wired and Wireless), Offering (Hardware, Software, and Services), Product Type (Nurse Call Systems, Call Box Systems, Emergency Stanchions, Intercom System, and Others),, and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Nov 2023

Outpatient Central Fulfillment Market

Size and Forecast (2020 - 2030), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Automated Medication Dispensing Systems, Automated Packaging and Labeling Systems, Automated Tabletop Counters, Automated Storage and Retrieval Systems, and Others), End User (Hospital Pharmacies, Retail Pharmacies, and Mail-Order Pharmacies), and Geography (North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa)

Nov 2023

Well-Being Platform Market

Forecast to 2030 - Global Analysis by Service (Health Risk Assessment, Fitness, Smoking Cessation, Health Screening, Nutrition & Weight Management, Stress Management, Comprehensive Well-Being, and Others), Category (Fitness and Nutrition Consultant, Psychological Therapists, and Organizations/Employers), Delivery Model (Onsite and Offsite), End User (Small-Scale Organizations, Medium-Scale Organizations, Large-Scale Organizations, and Home Use), and Geography

Nov 2023

Product Design and Development Services Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Services (Research, Strategy, and Concept Generation; Concept and Requirement Development; Detailed Design and Process Development; Process Validation, Manufacturing Transfer, and Design Validation; and Other Services), Application (Diagnostic Equipment, Therapeutic Equipment, Surgical Instruments, Clinical Laboratory Equipment, Biological Storage, Consumables, and Others), and End User (Medical Companies, Pharmaceutical Companies, Biotechnology Companies, and Contract Research Organizations)

Nov 2023

Patient Engagement Technology Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Component (Services, Hardware, and Software), Therapeutic Area (Fitness, Chronic Diseases, Women’s Health, and others), Delivery Mode (Cloud-Based and On-Premises), Application (Health Management, Financial Health Management, Home Healthcare Management, and Others), and End User (Patients, Payers, Providers, and Others)

Nov 2023

IVD Contract Research Organization Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Type (Clinical Chemistry, Molecular Diagnostics, Immunochemistry, Companion Diagnostics, Hematology, Histology & Cytology, Microbiology, and Others), Services (Clinical Research, Biostatistics & Data Management Services, Therapeutic Expertise, Regulatory Services, Reimbursement Support Services, Assay Development Services, and Others), and Geography

Nov 2023

Dental CAD/CAM Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Product [Dental CAD/CAM Materials (Glass Ceramics, Alumina-Based Ceramics, Lithium Disilicate, Zirconia, and Others) and Dental CAD/CAM Systems], Type (In-Office Systems and In-Lab Systems), Components [Hardware (Dental Printers, Milling Machines, Scanners, and Others) and Software], Application (Dental Prosthesis, Dental Implants, and Others), and End User (Dental Clinics, Dental Laboratories, Milling Centers, and Others)

Nov 2023

Emergency Medical Software Market

Forecast to 2028 - COVID-19 Impact and Global Analysis By Product [Early Warning and Vulnerability Alert System (EWVAS), EMS Computer Aided Dispatch (CAD) System, Incident Response Software, Ambulance Management Software, and Others], Mode of Delivery [On Premises and Software as a Service (SaaS)], Platform (Android, iOS, Windows, and Others), and End User (Commercial, Municipal, State City Agencies, and Others)