Dyspnea Treatment Market Demand, Size & Forecast by 2034

Dyspnea Treatment Market Size and Forecasts (2021 - 2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Therapy (Supplemental Oxygen Therapy, Relaxation Therapy); Drugs (Antianxiety Drugs, Antibiotics, Anticholinergic Agents, Corticosteroids); End Users (Hospitals, Home Care, Specialty Centres); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040122

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 03, 2026

2025 Market Size

US$ 10.53 Bn

Base year value

2034 Forecast

US$ 18.64 Bn

Projected by 2034

CAGR 2026-2034

6.55 %

Growth rate

Addressable Market

US$ 131.90 Bn

(2026-2034)

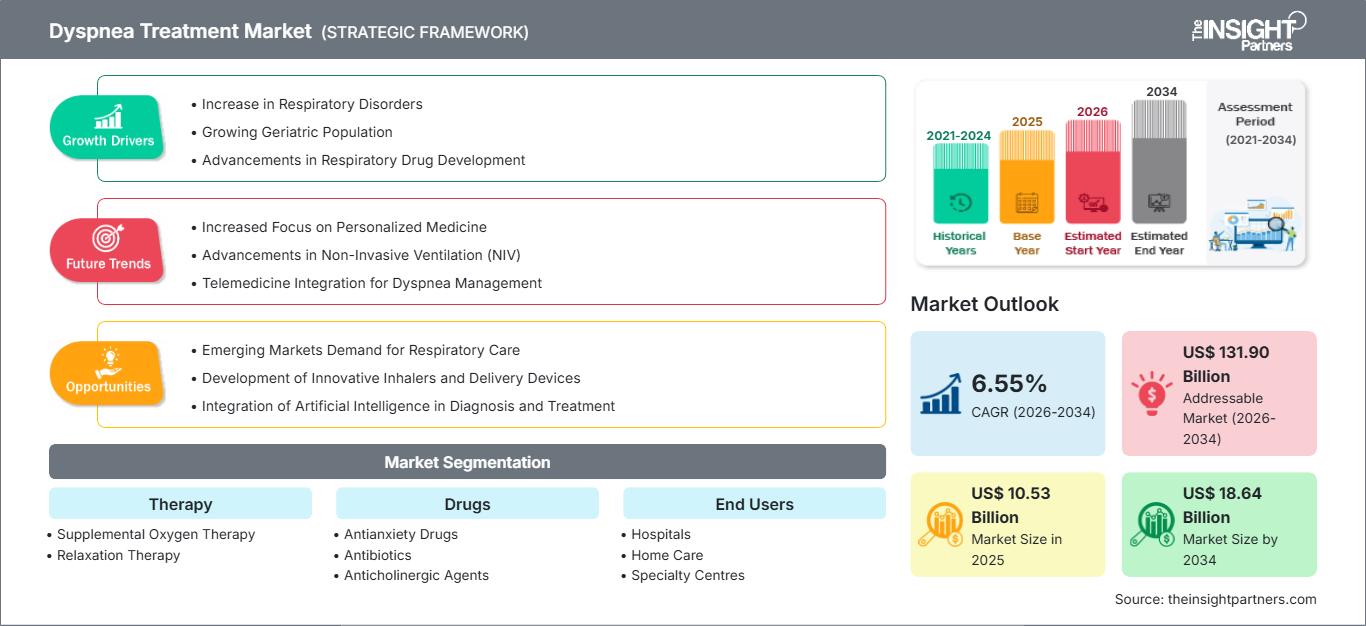

The Dyspnea Treatment Market was valued at US$ 10.53 Billion in 2025 and is projected to reach US$ 18.64 Billion by 2034, growing at a CAGR of 6.55% during 2026–2034. The market covers therapeutic approaches and drug-based interventions designed to manage breathing discomfort associated with respiratory, cardiovascular, and systemic conditions. Increasing prevalence of chronic respiratory disorders, aging populations, and advancements in supportive care solutions are shaping long-term market expansion.

North America is expected to maintain a significant position in the Dyspnea Treatment Market, supported by advanced healthcare infrastructure, higher adoption of respiratory therapies, and strong clinical research activity. The region is anticipated to register growth within an estimated CAGR range of 6.0–7.0% during 2026–2034, driven by rising respiratory disease burden, home-based care adoption, and increasing availability of specialized treatment options.

Dyspnea Treatment Market Assessment and Insights

- North America: The region demonstrates strong adoption of dyspnea management solutions due to established healthcare systems, advanced respiratory care facilities, and high treatment accessibility. North America accounted for a 34–38% share in 2025 and is expected to grow at a CAGR of 6.0–7.0% during 2026–2034.

- US: The US market benefits from strong pharmaceutical presence, respiratory disorder management programs, and increasing home care utilization. The country represented a 75–80% share of North America in 2025 and is projected to expand at a CAGR of 6.2–7.2% during 2026–2034.

- Europe: Europe continues to experience demand growth due to rising chronic obstructive pulmonary disease prevalence and healthcare modernization initiatives across Germany, the UK, France, Italy, and Spain. The region held a 27–31% share in 2025 and is estimated to grow at a CAGR of 5.8–6.8% during 2026–2034.

- Asia Pacific: Asia Pacific is witnessing increasing adoption of respiratory treatment solutions due to healthcare expansion, urbanization, and improving access in China, Japan, India, and South Korea. The region captured a 22–26% share in 2025 and is expected to register a CAGR of 7.0–8.0% during 2026–2034.

- Largest Segment: Drugs represent the largest segment due to widespread clinical usage of pharmacological therapies for respiratory symptom management. The segment held a 55–60% market share in 2025 and is projected to grow at a CAGR of 6.3–7.3% during 2026–2034.

- High Growth Segment: Home Care under end users represents a high-growth segment due to increasing preference for remote monitoring and patient-centered treatment models. The segment accounted for a 25–30% market share in 2025 and is expected to grow at a CAGR of 7.2–8.2% during 2026–2034.

- Key companies analyzed in detail: GlaxoSmithKline plc, Novartis AG, Merck & Co., Inc., Boehringer Ingelheim International GmbH, AstraZeneca PLC, Teva Pharmaceutical Industries Ltd., Chiesi Farmaceutici S.p.A., Sanofi, Regeneron Pharmaceuticals, Inc., ResMed Inc.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Dyspnea Treatment Market has seen continuous developments in terms of improvements in respiratory medicines, oxygen therapy, and individualized treatments for symptoms. The inclusion of technology has enabled better monitoring of patients, whereas advancements in pharmaceutical products have led to an increase in the availability of different types of treatments within the areas of respiratory medicines and supportive care medicines. There is increasing emphasis on using multidisciplinary treatment that includes medicines, oxygen therapy, and behavioral modifications. Production dynamics of the market are impacted by the capacity for manufacturing of pharmaceuticals, adherence to regulations, and increasing demand for customized treatment approaches.

The future development of the Dyspnea Treatment Market is expected to be impacted by new healthcare eco-systems, investments in respiratory illness treatments, and supportive regulatory environment. The growing use of digital health solutions, improved diagnostics, and establishment of specialist respiratory centers in developing nations are among some of the potential growth opportunities for the market.

Dyspnea Treatment Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 10.53 Billion |

| Market Size by 2034 | US$ 18.64 Billion |

| Global CAGR (2026 - 2034) | 6.55% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Dyspnea Treatment Market Analysis

There is an increased demand for dyspnea treatment solutions as a result of rising incidences of respiratory diseases, heart disorders, and aging related breathing problems. The market environment includes drug companies, medical devices suppliers, healthcare facilities and at home health care facilities. Demand is influenced by developments in oxygen therapy equipment, medication formulation techniques and distribution channels. Increasing spending on healthcare and growing facilities for respiratory care services are creating opportunities for availability of treatment solutions.

The value chain consists of product development, regulation, production, distribution and clinical application. The pharmaceuticals companies are developing drugs for inflammatory respiratory diseases, airway obstruction and symptomatic treatments. The hospitals and specialized care centers continue to be significant delivery points; however, there have been changes with respect to home care delivery of these services. According to Dyspnea Treatment Market report, integrated care models and patient monitoring systems would play a role in future strategies.

The competition in the industry encompasses worldwide pharmaceutical companies and other healthcare firms that offer a portfolio of respiratory products, innovations in therapy, and collaborations. Firms like GlaxoSmithKline plc, Novartis AG, Merck & Co., Inc., Boehringer Ingelheim International GmbH, and AstraZeneca PLC are developing their portfolio of respiratory-based products using innovation and research and development activities. Other companies like Teva Pharmaceutical Industries Ltd., Chiesi Farmaceutici S.p.A., Sanofi, Regeneron Pharmaceuticals, Inc., and ResMed Inc. add value to the industry through pharmaceuticals, biotech companies, and respiratory services.

Some investment trends in the market focus on innovations in drug development, connected respiratory devices, and patient management systems. The strategic positions for firms in the industry revolve around increasing accessibility of treatments, improving clinical operations, and meeting different needs of respiratory care. Other possible trends include personalizing medicine and incorporating digital health technologies.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Dyspnea Treatment Market: Strategic Insights

Regional Insights

North America Dyspnea Treatment Market

North America represented a 34–38% share of the Dyspnea Treatment Market in 2025 and is projected to expand at a CAGR of 6.0–7.0% during 2026–2034. The region benefits from established healthcare infrastructure, high awareness of respiratory disorders, and strong adoption of advanced treatment approaches. The US remains the leading contributor, supported by pharmaceutical innovation, reimbursement frameworks, and widespread availability of respiratory care services.

Healthcare providers across North America are increasingly integrating oxygen therapy, pharmacological interventions, and home-based respiratory management solutions. Demand is supported by the presence of specialized respiratory centers, increasing chronic disease prevalence, and aging demographics. Companies including GlaxoSmithKline plc, AstraZeneca PLC, ResMed Inc., and other healthcare innovators continue to influence regional treatment advancements through research, product development, and technology adoption.

U.S. Dyspnea Treatment Market

The U.S. Dyspnea Treatment Market accounted for 75–80% of the North American market in 2025 and is expected to grow at a CAGR of 6.2–7.2% during 2026–2034. The country benefits from strong healthcare spending, advanced clinical research capabilities, and high adoption of respiratory treatment technologies across hospitals and home care settings.

The presence of major pharmaceutical and medical technology companies supports continuous innovation in respiratory care applications. Increasing utilization of home oxygen solutions, remote monitoring systems, and personalized treatment approaches is influencing market expansion. Companies such as GlaxoSmithKline plc, ResMed Inc., and AstraZeneca PLC maintain significant application relevance through respiratory-focused portfolios and healthcare collaborations.

Europe Dyspnea Treatment Market

Europe held a 27–31% share of the Dyspnea Treatment Market in 2025 and is anticipated to grow at a CAGR of 5.8–6.8% during 2026–2034. Germany represents one of the leading countries due to strong healthcare infrastructure, respiratory disease management capabilities, and adoption of advanced therapies. The region is supported by increasing healthcare modernization and clinical research activities.

The UK market is influenced by increasing respiratory disease awareness, structured healthcare programs, and adoption of integrated care models. Germany continues to demonstrate strong demand due to advanced hospitals, pharmaceutical innovation, and specialist treatment facilities supporting respiratory disorder management.

France, Italy, and Spain are experiencing gradual expansion driven by aging populations, improved access to respiratory therapies, and healthcare system investments. These countries are strengthening respiratory care pathways through hospital-based treatment improvements and wider adoption of supportive therapies. Europe remains an important region due to established pharmaceutical capabilities and increasing focus on chronic disease management.

APAC Dyspnea Treatment Market

APAC accounted for a 22–26% share of the Dyspnea Treatment Market in 2025 and is estimated to grow at a CAGR of 7.0–8.0% during 2026–2034. China represents a leading country due to expanding healthcare infrastructure and increasing respiratory disease management initiatives.

Japan and South Korea are adopting advanced respiratory technologies supported by healthcare innovation. India is experiencing increased demand due to improving medical accessibility and growing awareness. Australia contributes through developed healthcare systems and respiratory care adoption.

Industrial expansion, government healthcare programs, and increasing investments in medical infrastructure are expected to support regional market development. APAC’s growing patient population and improving treatment availability create significant long-term opportunities.

Middle East & Africa Dyspnea Treatment Market

The Middle East & Africa Dyspnea Treatment Market is expected to expand at a CAGR of 5.0–6.0% during 2026–2034, supported by healthcare infrastructure development and increasing respiratory care investments. Saudi Arabia represents a leading country due to healthcare modernization programs and increased hospital capacity.

The UAE is strengthening specialized healthcare services through infrastructure development and technology adoption. South Africa contributes through established healthcare networks and growing respiratory disorder management requirements.

The Rest of MEA region is influenced by healthcare accessibility improvements and public health investments. Energy-driven economies are supporting medical infrastructure expansion, while regional initiatives continue improving availability of respiratory treatment solutions.

Segmentation Analysis

Therapy

The Therapy segment is expected to grow at a CAGR of 5.8–6.8% during 2026–2034. This segment includes non-pharmaceutical approaches that support symptom management and improve patient comfort. Increasing adoption of supportive care methods, oxygen-based interventions, and patient-focused respiratory management strategies is contributing to segment development. Healthcare providers are combining therapeutic approaches with medication-based treatments to improve outcomes across different care environments.

- Supplemental Oxygen Therapy: Supplemental oxygen therapy remains an important approach for patients requiring improved oxygen availability. Demand is supported by respiratory disease prevalence, home-based treatment adoption, and increasing use of portable oxygen solutions.

- Relaxation Therapy: Relaxation therapy supports symptom management by addressing anxiety-related breathing discomfort. Its role is increasing within integrated care models focused on improving patient comfort and overall respiratory management outcomes.

Drugs

The Drugs segment is expected to expand at a CAGR of 6.3–7.3% during 2026–2034. It represents the largest segment due to extensive clinical use of pharmacological therapies for respiratory symptoms and related conditions. Growth is supported by continued drug innovation, increasing chronic respiratory disease burden, and adoption across hospitals and specialty care centers. Pharmaceutical companies are focusing on improved formulations and targeted treatment approaches.

- Antianxiety Drugs: Antianxiety drugs contribute to dyspnea management by addressing psychological factors associated with breathing difficulties. Demand is influenced by integrated respiratory care approaches and increasing focus on symptom-related patient support.

- Antibiotics: Antibiotics maintain importance in cases where respiratory infections contribute to breathing complications. Their application remains linked with infection management strategies and clinical treatment protocols across healthcare settings.

- Anticholinergic Agents: Anticholinergic agents are widely used in respiratory care due to their role in airway management. Continued demand is supported by chronic respiratory condition treatment and physician preference.

- Corticosteroids: Corticosteroids remain significant for managing inflammatory respiratory conditions. Their strategic importance is linked with established clinical usage and ongoing respiratory disease treatment requirements.

End Users

The End Users segment is projected to grow at a CAGR of 6.5–7.5% during 2026–2034. Healthcare delivery patterns are shifting toward flexible treatment environments, increasing demand across hospitals, home care providers, and specialty centers. Expansion of remote monitoring capabilities and patient-centered care models is supporting wider adoption across different healthcare settings.

- Hospitals: Hospitals represent a major care setting due to advanced diagnostic capabilities, emergency respiratory management, and access to specialized healthcare professionals. Demand remains strong across acute and chronic respiratory care.

- Home Care: Home care adoption is increasing due to patient preference for convenient treatment environments and advancements in portable respiratory technologies. It supports long-term symptom management and reduces dependence on hospital-based care.

- Specialty Centres: Specialty centres provide focused respiratory management through advanced expertise and treatment programs. Their importance is increasing with demand for comprehensive evaluation and disease-specific care pathways.

Opportunity Snapshot

| Segment Name | Revenue Contribution (High/Medium/Low) | Trend Tag | Adoption Stage (Emerging/Scaling/Mature) |

| Hospitals | High | Advanced Care | Mature |

| Home Care | Medium | Remote Monitoring | Scaling |

| Specialty Centres | Medium | Respiratory Clinics | Scaling |

Dyspnea Treatment Market Growth Drivers and Impact Analysis

Rising Burden of Chronic Respiratory and Cardiovascular Disorders

Increasing prevalence of chronic obstructive pulmonary disease, asthma, cardiovascular disorders, and age-related respiratory complications is strengthening demand for dyspnea management solutions. Healthcare systems are focusing on early diagnosis and symptom control to reduce hospitalization pressure and improve patient outcomes. The growing elderly population is particularly influencing treatment requirements because respiratory symptoms frequently accompany multiple chronic conditions. This driver is encouraging pharmaceutical companies and healthcare providers to expand treatment portfolios, improve patient monitoring approaches, and develop integrated care pathways. The market impact includes higher utilization of drug therapies, oxygen support solutions, and specialized respiratory services across hospitals and home care environments. Increasing awareness among patients and healthcare professionals is further supporting consistent demand.

Expansion of Home-Based Respiratory Care Models

The movement towards a patient-focused care delivery system will increase the use of at-home dyspnea treatment solutions. With innovations in portable oxygen devices, remote monitoring technology, and healthcare solutions, patients can receive ongoing care even outside conventional healthcare settings. Healthcare practitioners are increasingly adopting home care models for convenience, reduced healthcare costs, and effective disease management. This trend is shaping the product development process for manufacturers as they develop small, affordable, and easy-to-use respiratory care devices. Telehealth-powered monitoring will further strengthen this environment by enabling healthcare providers to monitor patients' status remotely. As healthcare systems continue emphasizing value-based care, home-based treatment models are expected to become an increasingly important contributor to market development.

Advancements in Respiratory Drug Development and Treatment Approaches

Advancements in the respiratory drug industry will continue to offer opportunities to improve the management of dyspnea. Drug companies are making progress through innovations in advanced formulations, disease targeting, and drug combinations to address difficult respiratory problems. Innovations in drug delivery mechanisms are increasing efficacy and patient compliance. Research into inflammation, airway management, and symptom reduction is shaping future therapeutic options. Regulatory support for innovation in respiratory medicines will spur companies to invest more in research and products. Market implications will include greater access to medicines, improved disease management, and increased competition among health care providers and pharmaceutical companies.

Dyspnea Treatment Market Future Trends

Integration of Digital Health and Remote Patient Monitoring

The integration of digital health is anticipated to be a key future trend, driven by the increasing use of connected solutions for respiratory health monitoring. Remote patient monitoring services, wearable devices, and digital health tools enable continuous monitoring of signs of respiratory illnesses and treatment efficacy. Digital tools help with early intervention, reducing the need for emergency care, and facilitating patient-doctor communication. Future developments in the market will be characterized by increased cooperation between medical device manufacturers, pharmaceutical companies, and digital health companies. The use of AI-enabled analysis can further personalize the treatment plan. As decentralization in healthcare becomes more prominent, digital respiratory care platforms will shape treatment approaches.

Personalized Respiratory Treatment Strategies

Personalized medicine is a promising trend in respiratory care, as there is growing recognition that patients experience breathing difficulties for different reasons and to varying degrees of severity. Diagnostic techniques, biomarker studies, and patient assessments can be used to create more customized treatment regimens. In the future, personalized treatments will include using certain medications based on patients' characteristics, the progression of their condition, and other parameters. Drug companies are likely to focus on developing tailored products to improve treatment accuracy. This trend may change how decisions are made in healthcare, as healthcare professionals will prescribe medications and therapies based on patients' needs.

Dyspnea Treatment Market Opportunities

Growth Potential in Emerging Healthcare Markets

Developing economies offer substantial opportunities owing to the presence of healthcare infrastructure, improved diagnosis options, and heightened understanding of respiratory disease management. Healthcare modernization efforts are underway in many countries across Asia Pacific, the Middle East, and Africa, offering market players opportunities to expand their distribution channels and enhance treatment availability. Urbanization trends and environmental concerns are responsible for the rising demand for respiratory healthcare treatments. Market participants could leverage opportunities by designing cost-effective treatment solutions, building partnerships in the region, and customizing offerings according to regional healthcare requirements. The development of specialty care facilities and better healthcare access would be instrumental in the adoption of dyspnea treatment solutions. These opportunities may encourage strategic investments focused on regional growth and healthcare system development.

Innovation in Integrated Respiratory Care Solutions

Opportunity Area – Integrated Respiratory Care Solutions

One key area of opportunity for companies to explore is integrated respiratory care solutions that incorporate medications, treatments, monitoring, and patient needs. The rise in demand for integrated care models is driving the development of solutions that help manage not only the clinical aspects of respiratory disorders but also their lifestyle aspects. In addition, investment in connected devices, treatment process optimization, and patient engagement will create new opportunities for business growth. Organizations focusing on improving treatment accessibility and care continuity are positioned to address evolving healthcare priorities. This opportunity area is expected to influence future competitive strategies as the market moves toward more holistic respiratory care models.

Recent Developments

- December 2025: Cytokinetics announced that the FDA has approved MYQORZO (aficamten) for the treatment of adults with symptomatic obstructive hypertrophic cardiomyopathy (oHCM). As a selective, reversible cardiac myosin inhibitor, aficamten reduces excessive cardiac contractility and alleviates left ventricular outflow tract (LVOT) obstruction, a key driver of symptoms in oHCM. The approval is particularly relevant to the dyspnea treatment market, as reducing LVOT obstruction can improve exercise capacity and lessen shortness of breath, one of the most common and debilitating symptoms experienced by patients with symptomatic oHCM. This approval expands the therapeutic landscape for managing cardiomyopathy-associated dyspnea and highlights the growing role of targeted cardiac therapies in improving patient quality of life.

- May 2024: DevPro Biopharma and Bespak announced the completion of early feasibility studies on DP007, a new formulation of albuterol in a pressurized metered dose inhaler (pMDI) which shows comparable performance to Ventolin® HFA but with a significant reduction in greenhouse gas emissions. This breakthrough pMDI is being developed by DevPro Biopharma, a respiratory-focused clinical development accelerator, and Bespak, a leading contract development and manufacturing organization (CDMO) focused on orally inhaled and nasal drug-device combination products.

- December 2024: Teva Pharmaceuticals, Inc., a U.S. affiliate of Teva Pharmaceutical Industries Ltd., announced the launch of a new patient access program, in partnership with Direct Relief, to supply inhalers to eligible patients in the United States free of charge.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends