Embolic Protection Devices Market Size, Trends & Growth by 2034

Coverage: By Type (Distal Occlusion Devices, Distal Filter Devices and Proximal Occlusion Devices); Material (Polyurethane and Nitinol); Application (Neurovascular Diseases, Peripheral Vascular Diseases and Cardiovascular Diseases); End User (Hospitals, Ambulatory Surgical Centers and Other End User) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00005182

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 08, 2026

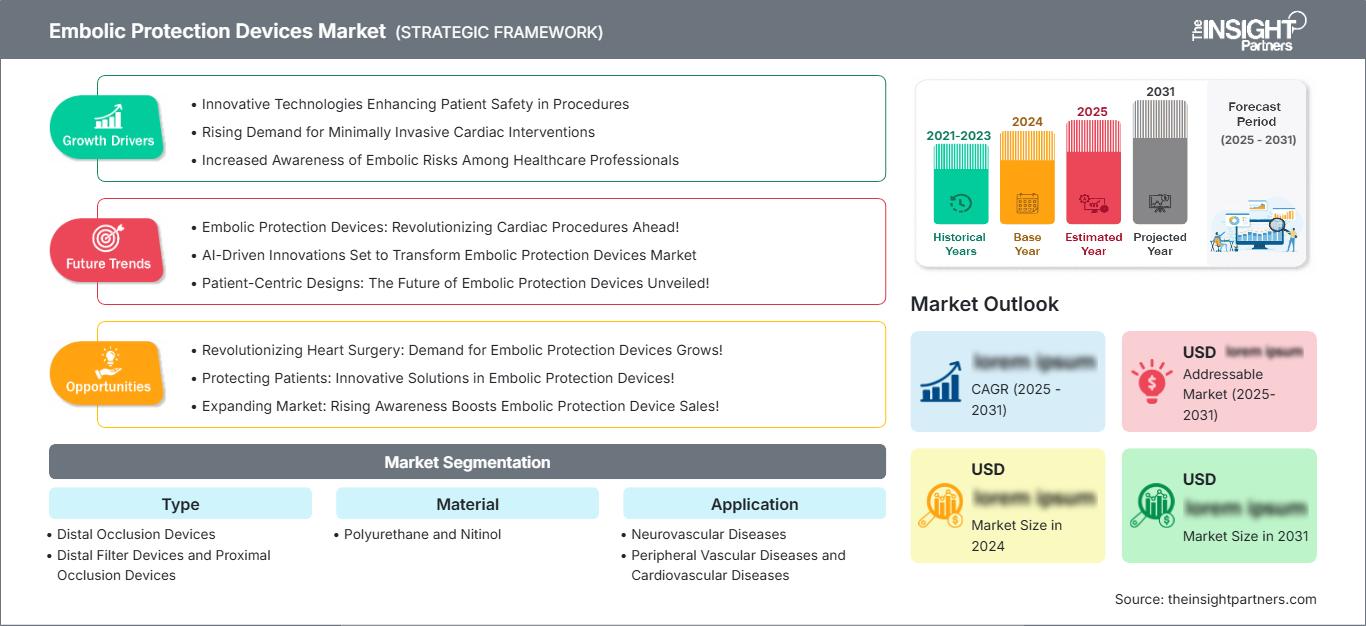

2025 Market Size

US$ 410.00 Mn

Base year value

2034 Forecast

US$ 811.00 Mn

Projected by 2034

CAGR 2026-2034

7.87 %

Growth rate

Addressable Market

US$ 5,492.95 Mn

(2026-2034)

The Embolic Protection Devices Market size was valued at US$ 410.00 Million in 2025 and is projected to reach US$ 811.00 Million by 2034, expanding at a CAGR of 7.87% during 2026–2034. Market expansion is supported by the growing adoption of minimally invasive vascular procedures, increasing diagnosis of cardiovascular and neurovascular disorders, and continuous improvements in embolic capture technologies that enhance procedural safety across diverse interventional applications.

North America is expected to maintain its leadership in the embolic protection devices market forecast, registering an estimated CAGR of 7.2–7.8% between 2026 and 2034. The region benefits from extensive adoption of endovascular interventions, favorable reimbursement structures, advanced hospital infrastructure, and widespread availability of experienced interventional cardiologists and vascular specialists, supporting consistent demand for embolic protection devices across complex cardiovascular and peripheral vascular procedures.

Embolic Protection Devices Market Assessment and Insights

- North America: Holds 39–43% of the embolic protection devices market share in 2025, growing at a CAGR of 7.2–7.8% during 2026–2034, driven by expanding transcatheter interventions and favorable reimbursement supporting the adoption of advanced embolic protection devices.

- US: Accounts for 84–88% of the North American market in 2025, expanding at a 7.3–7.9% CAGR due to increasing catheter-based cardiovascular procedures, advanced healthcare infrastructure, and continued adoption of minimally invasive vascular interventions.

- Europe: Represents 27–31% share in 2025, growing at a 7.0–7.6% CAGR, led by Germany, France, and the UK through mature vascular care networks, increasing minimally invasive procedures, and advanced cardiovascular treatment capabilities.

- Asia Pacific: Holds 21–25% share in 2025, expanding at a 8.7–9.3% CAGR, led by China, Japan, and India with rising healthcare investments, expanding patient access, and increasing prevalence of cardiovascular diseases.

- Largest Segment: Cardiovascular Diseases Application holds the largest market share in 2025, growing at a 7.6–8.2% CAGR due to increasing catheter-based cardiac interventions requiring effective embolic protection during complex vascular procedures.

- High Growth Segment: Distal Filter Devices are projected to register the fastest growth at a CAGR of 8.4–9.0% during 2026–2034, driven by physician preference for maintaining blood flow while efficiently capturing embolic debris during endovascular interventions.

- Key companies analyzed in detail: Abbott; Allium Medical Solutions Ltd.; Boston Scientific Corporation; Cardinal Health, Inc.; Contego Medical, LLC; Getinge AB; Medtronic plc; Silk Road Medical, Inc.; Transverse Medical, Inc.; W. L. Gore & Associates, Inc.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Continual innovation has developed embolic protection products from rather basic systems of occlusion to more complicated systems of filtration and flow control tailored to a wide array of vascular procedures. Innovation in nitinol frame design, low-profile delivery systems, advanced filter designs, and better compatibility with procedures has increased the level of physician confidence, which, together with the development of more efficient ways of production, has led to greater adoption in cardiovascular, peripheral vascular, and neurovascular treatments.

Future growth of the embolic protection devices market will be associated with investments into developing healthcare systems, training of physicians, and advanced interventional therapies regulatory approval. Development of healthcare infrastructure in such regions as Asia Pacific and some Middle Eastern countries will increase the number of procedures performed, while continued scientific evidence in favor of embolic protection during complex procedures will drive adoption.

Embolic Protection Devices Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 410.00 Million |

| Market Size by 2034 | US$ 811.00 Million |

| Global CAGR (2026 - 2034) | 7.87% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Embolic Protection Devices Market Analysis

Growing incidence of cardiovascular disease, carotid artery stenosis, peripheral arterial disease, and ischemic stroke continues to increase demand for embolic protection devices worldwide. As minimally invasive interventions become standard clinical practice, physicians increasingly prioritize technologies that reduce embolic complications while preserving procedural efficiency. Device manufacturers collaborate closely with healthcare providers, component suppliers, regulatory agencies, and contract manufacturing organizations to strengthen product quality, improve supply resilience, and accelerate commercialization of next-generation embolic protection platforms.

Material innovation remains central to value creation across the market. Nitinol and polyurethane continue supporting improved flexibility, durability, and deployment precision while reducing procedural complexity. Growing integration between imaging technologies and interventional devices further enhances procedural planning and clinical outcomes, encouraging hospitals to adopt advanced embolic protection solutions across increasingly complex vascular interventions.

Competition within the embolic protection devices market remains technology driven, with established multinational medical device manufacturers competing alongside specialized vascular innovators. Abbott, Boston Scientific Corporation, Medtronic plc, Getinge AB, and W. L. Gore & Associates, Inc. continue strengthening portfolios through product refinement, physician education initiatives, and expanded clinical evidence. Meanwhile, other key players mentioned in the embolic protection devices market report, including Contego Medical, LLC, Silk Road Medical, Inc., Transverse Medical, Inc., Cardinal Health, Inc., and Allium Medical Solutions Ltd. pursue differentiated strategies focused on specialized vascular applications and procedural efficiency.

Investment activity increasingly emphasizes research and development targeting lower-profile delivery systems, enhanced embolic capture efficiency, and broader compatibility with evolving catheter technologies. Companies are also expanding manufacturing capabilities, strengthening regional distribution partnerships, and pursuing regulatory approvals across high-growth international markets. These strategic initiatives are expected to intensify competition while supporting continued innovation and wider clinical adoption throughout the forecast period.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Embolic Protection Devices Market: Strategic Insights

Regional Insights

North America Embolic Protection Devices Market

North America accounted for 39–43% of the global embolic protection devices market in 2025 and is projected to register a CAGR of 7.2–7.8% during 2026–2034. Strong procedural volumes, favorable reimbursement policies, and early adoption of advanced endovascular technologies continue to reinforce regional market leadership.

Healthcare providers are increasingly integrating embolic protection devices into cardiovascular and peripheral vascular interventions to reduce procedural complications. Continuous investment in hybrid operating rooms, physician training, and clinical research further supports sustained embolic protection devices market expansion across the region.

U.S. Embolic Protection Devices Market

The U.S. represented 84–88% of the embolic protection devices market in North America in 2025 and is expected to expand at a CAGR of 7.3–7.9% through 2034. High prevalence of cardiovascular disorders and widespread availability of specialized interventional centers continue to support market growth.

Leading manufacturers maintain extensive commercial operations, clinical collaborations, and physician education programs across the country. Growing utilization of embolic protection devices during carotid artery stenting, transcatheter cardiovascular procedures, and complex peripheral vascular interventions continues to strengthen long-term demand.

Europe Embolic Protection Devices Market

Europe captured 27–31% of embolic protection devices market revenue in 2025 and is anticipated to register a CAGR of 7.0–7.6% through the forecast period. The region benefits from mature healthcare infrastructure, standardized treatment pathways, and increasing utilization of minimally invasive vascular procedures. Germany remains the leading national market owing to strong hospital capabilities and high procedural volumes.

The United Kingdom continues to experience steady market expansion supported by increasing adoption of image-guided vascular interventions, investments in specialized cardiovascular centers, and greater awareness regarding stroke prevention. Continuous modernization of hospital infrastructure also contributes to wider adoption of embolic protection technologies.

Germany maintains a leading regional position through advanced cardiovascular treatment facilities, strong clinical research capabilities, and early implementation of innovative interventional technologies. Favorable reimbursement mechanisms and experienced vascular specialists encourage routine utilization of embolic protection devices during complex endovascular procedures.

France, Italy, and Spain collectively contribute substantial demand as healthcare systems continue expanding access to minimally invasive cardiovascular and neurovascular treatments. Ongoing investments in catheterization laboratories, physician training, and procedural efficiency support gradual market growth across Southern Europe.

APAC Embolic Protection Devices Market

Asia Pacific accounted for 21–25% of the global market in 2025 and is projected to achieve the fastest regional expansion with a CAGR of 8.7–9.3%. China leads the regional market, supported by expanding healthcare infrastructure, increasing procedural capacity, and favorable investment in advanced medical technologies.

China continues strengthening domestic cardiovascular treatment capabilities through hospital modernization and increasing adoption of minimally invasive procedures. Japan benefits from advanced clinical expertise and an aging population requiring vascular interventions. South Korea, India, and Australia are expanding procedure volumes through healthcare investment, regulatory support, and broader physician access to advanced embolic protection technologies.

Middle East & Africa Embolic Protection Devices Market

The Middle East & Africa embolic protection devices market is projected to expand at a CAGR of 6.6–7.2% during 2026–2034. Rising healthcare expenditure, improving cardiovascular care infrastructure, and increasing awareness of minimally invasive treatment options are supporting gradual market development across the region.

Saudi Arabia leads regional demand through continued healthcare modernization and investment in specialized cardiac centers. The United Arab Emirates is strengthening advanced interventional capabilities, while South Africa remains an important market supported by established tertiary hospitals. The Rest of the Middle East & Africa is witnessing progressive expansion as healthcare infrastructure and access to specialized vascular care continue improving.

Segmentation Analysis

Type

The Type segment in the embolic protection devices market is expected to maintain a CAGR of 7.8–8.4% during 2026–2034, supported by continuous technological innovation and growing physician preference for devices that improve procedural safety while maintaining efficient blood flow management during endovascular interventions.

- Distal Occlusion Devices: These devices temporarily interrupt blood flow during vascular interventions, minimizing distal embolization risk. They remain valuable in selected carotid and peripheral procedures requiring effective embolic containment before debris removal.

- Distal Filter Devices: Distal filter devices represent the fastest-growing product category because they maintain blood perfusion while capturing embolic particles. Continuous improvements in filter design, flexibility, and deployment systems support increasing physician adoption.

- Proximal Occlusion Devices: Proximal occlusion devices establish cerebral protection by reversing or interrupting blood flow before crossing vascular lesions. Their clinical value is expanding in complex carotid artery interventions requiring enhanced embolic management.

Material

- Polyurethane: Polyurethane remains widely utilized due to its flexibility, durability, and compatibility with filter membranes. Material advancements continue improving embolic capture efficiency while supporting reliable device deployment during minimally invasive vascular procedures.

- Nitinol: Nitinol provides exceptional shape memory, flexibility, and fatigue resistance, enabling consistent expansion and precise positioning of embolic protection devices. These characteristics support broad application across complex cardiovascular and peripheral vascular interventions.

Application

- Neurovascular Diseases: Increasing incidence of ischemic stroke and expanding neurointerventional procedures continue supporting demand for embolic protection technologies that reduce procedural complications and improve neurological treatment outcomes.

- Peripheral Vascular Diseases: Rising diagnosis of peripheral artery disease and increasing adoption of minimally invasive vascular interventions are encouraging greater utilization of embolic protection devices during lower extremity and peripheral procedures.

- Cardiovascular Diseases: This segment accounts for the largest market share because of expanding catheter-based cardiac procedures, increasing treatment of carotid artery disease, and growing emphasis on reducing embolic complications during cardiovascular interventions.

End User

- Hospitals: Hospitals remain the primary end users due to high procedure volumes, comprehensive cardiovascular service lines, advanced imaging capabilities, and multidisciplinary teams performing complex endovascular interventions.

- Ambulatory Surgical Centers: Ambulatory surgical centers are experiencing increasing adoption as outpatient vascular procedures expand and healthcare providers seek efficient, cost-effective treatment environments for appropriately selected patients.

- Other End User: Other healthcare facilities contribute incremental demand by expanding access to specialized vascular procedures and supporting referral-based interventional care across developing healthcare systems.

Opportunity Snapshot

| Segment Name | Revenue Contribution | Trend Tag | Adoption Stage |

| Neurovascular Diseases | Medium | Stroke Care | Scaling |

| Peripheral Vascular Diseases | Medium | Limb Salvage | Scaling |

| Cardiovascular Diseases | High | Carotid Stenting | Mature |

Embolic Protection Devices Market Growth Drivers and Impact Analysis

Rising Volume of Minimally Invasive Cardiovascular Procedures

One of the key factors propelling the embolic protection devices market is the rising tendency towards the use of minimal invasive procedures involving blood vessels. The methods including stenting of the carotid arteries, transcatheter aortic valve replacement, and peripheral vascular procedures demand new technology, which will minimize the risks of embolism formation without adding to the duration of the procedure. In view of the increased focus of healthcare practitioners on improving patient outcomes and reducing the number of days spent in the hospital, there is an increasing need for incorporating these devices in the treatment process. The growth in the capabilities of the catheterization laboratories along with the physicians' experience further facilitates this trend.

Increasing Burden of Cardiovascular and Neurovascular Diseases

The increasing prevalence worldwide of conditions like cardiovascular disease, carotid artery stenosis, ischemic stroke, and peripheral arterial disease contributes to an ever-growing number of patients that can be treated through the use of embolic protection devices. Age-related issues, lack of physical activity, diabetes, high blood pressure, and obesity result in increased prevalence of diseases that require invasive interventions. The healthcare system focuses on early detection and treatment to limit disabilities and costs. As a result, doctors use embolic protection solutions in order to avoid problems during complicated interventions.

Continuous Technological Innovation in Device Design

Technological advancements have greatly contributed to increasing the clinical performance of the embolic protection devices. Companies are designing smaller delivery systems, better filters, better nitinol frames, and better retrieval systems for easy handling and effectiveness in catching emboli. Improved compatibility with newer guidewires, catheters, and imaging systems makes it possible for doctors to carry out more complicated procedures. It also reduces the complexity of the procedure, enhances patient safety, and ensures the acceptance of the device by many doctors from different vascular fields. Further development in the field of research and design will see the increase of its clinical uses and market coverage.

Embolic Protection Devices Market Future Trends

Integration of Advanced Imaging with Embolic Protection Technologies

The future generation of vascular intervention procedures is likely to involve a combination of embolic protection devices with imaging and navigation technology advances. With high-resolution intravascular imaging, artificial intelligence-based procedure planning, and visualization, physicians will be able to choose the right approach for embolic protection by analyzing lesion features and vascular structures. It is anticipated that such integration will increase the accuracy of procedures and will contribute to the process of personalizing treatments. Future device manufacturing will ensure seamless integration of embolic protection devices into new imaging platforms expanding the embolic protection devices market trends.

Expansion of Clinical Evidence for Broader Procedure Adoption

Greater investments in multicenter clinical trials are likely to add to the body of evidence supporting the use of embolic protection devices for other vascular procedures. In light of the rising use of clinical outcome and real-world evidence by health care professionals, companies have been trying to prove the safety of the procedure, low complication rate, and economic viability of the device. Good results in clinical trials might result in broader guideline recommendations as well as greater uptake among physicians beyond the usual carotid procedures.

Embolic Protection Devices Market Opportunities

Expanding Commercial Opportunities in Emerging Healthcare Markets

Modernization of health care systems in Asia Pacific, Latin America, and chosen Middle Eastern nations offers great potential for companies dealing with the production of embolic protection devices. Health care organizations are implementing modern cardiovascular treatment techniques, building new hospitals, and ensuring better availability of minimally invasive procedures. With the development of programs to train physicians and catheterization labs, the need for reliable embolic protection devices is likely to grow. Those businesses that set up manufacturing and distribution operations in regions, as well as educational activities, will have good chances to succeed in their endeavors.

Development of Next-Generation Multi-Application Protection Platforms

The manufacturers will have substantial potential in developing embolic protection systems that are flexible enough to be used in different vascular interventions using an adaptable platform. Products that have the capability to adapt to changing needs of physicians by being flexible, easy to deploy, compatible with various catheters, and efficient in capturing emboli will help to fulfill the changing requirements in cardiovascular, neurovascular, and peripheral vascular interventions. Development of versatile product platforms will help to decrease the inventory management complexities of the hospitals, as well as increase procedure efficiency.

Recent Developments

- November 2025: Contego Medical, LLC announced late-breaking results from the PERFORMANCE III TCAR-IEP study evaluating its Neuroguard IEP System. Across 146 patients treated at 26 clinical sites, investigators reported zero strokes, zero myocardial infarctions, and zero neurological deaths at 30 days, reinforcing the clinical performance of the integrated embolic protection platform for carotid interventions.

- October 2025: Medtronic plc commenced full U.S. distribution of the Neuroguard IEP System under its exclusive distribution agreement with Contego Medical. The integrated carotid stenting platform combines a nitinol stent, dilation balloon, and embolic protection filter, expanding Medtronic's carotid intervention portfolio following a successful limited market rollout.

- January 2025: Medtronic plc entered into an exclusive U.S. distribution agreement with Contego Medical, LLC for its commercially available carotid and peripheral vascular products, including the FDA-approved Neuroguard IEP System. The agreement also included increased investment in Contego and an option for future acquisition, strengthening Medtronic's position in carotid intervention technologies.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends