FPGA Market Share, Size, Trends, Segmentation and Forecast by 2031

Historic Data: 2021-2023 | Base Year: 2024 | Forecast Period: 2025-2031Coverage: FPGA Market covers analysis By Configuration (Low-end FPGA, Mid-range FPGA, High-end FPGA); Technology (SRAM-based FPGA, Flash-based FPGA, Antifuse-based FPGA); End User Industry (IT and Telecommunication, Aerospace and Defence, Industrial, Others), and Geography

- Report Date : Aug 2025

- Report Code : TIPRE00030099

- Category : Electronics and Semiconductor

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

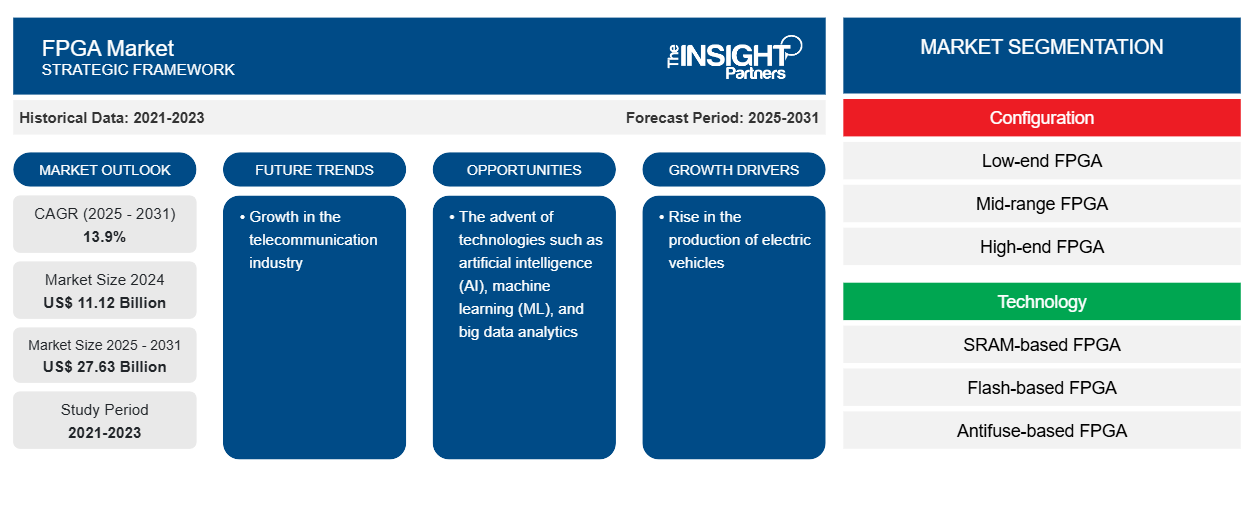

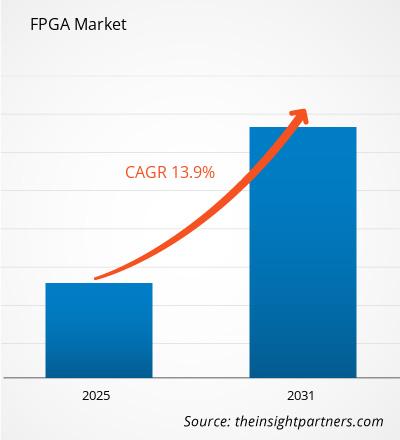

The FPGA market size is projected to reach US$ 27.63 billion by 2031 from US$ 9.76 billion in 2023. The market is expected to register a CAGR of 13.9% in 2023–2031. The growing adoption of FPGA in electric vehicles and the growth in the telecommunication industry are likely to remain key to FPGA market trends.

FPGA Market Analysis

The demand for semiconductors has experienced a surge in recent years, owing to factors such as the growing digitalization, rising adoption of 5G technology, and growing industrialization. The inclination towards the growing demand for FPGA architecture is due to FPGA capabilities, such as low power consumption and high compute density. The surge in demand for efficient data flow and streaming data processing for various applications bolsters the FPGA market.

The growth in the telecommunication sector will generate the demand for FPGA. FPGA is the most versatile processor and can be fit into hardware to process applications such as edge networking and other low latency applications. In addition, using FPGA also helps lower the power consumption and latency of the devices.

FPGA Market Overview

Field Programmable Gate Arrays (FPGAs) are integrated circuits that can reconfigure the hardware to meet some specific use case requirements after the manufacturing process. It consists of an array of programmable logic blocks and interconnects that can be configured to perform various digital functions. The FPGA market has witnessed significant growth in recent years, driven by technological advancements, rising connectivity, and the increasing demand for semiconductors.

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

FPGA Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

FPGA Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

FPGA Market Drivers and Opportunities

Rise in the production of electric vehicles

As a step towards sustainability and to reduce carbon footprint, the governments of various countries are emphasizing the production of electric vehicles. For instance, in September 2022, the US government announced its plan to boost the manufacturing of electric vehicles. By 2031, the country is expected to record 50% of the total electric vehicle sales share. The UAE government plans to launch 42,000 electric cars, which will be on the roads by 2031.

In electric vehicles, FPGAs can be used for fine-tuned motor control, power conversion, battery management systems, and inverters due to their support for high-performance PWM (pulse width modulation), which further helps to maximize power and efficiency to extend the range of the vehicle. Thus, the rising production of electric vehicles fosters the FPGA market.

Growth in the telecommunication industry

The growing investments and advancements in telecommunication infrastructure across developed and developing countries are fostering the growth of the global telecom industry. The telecommunication sector is experiencing a paradigm shift owing to the constantly changing technology landscape and growing penetration of smartphones and connected devices worldwide. The growing penetration of LTE networks coupled with increasing 5G deployments are some of the key factors that are fueling the growth of the telecommunications industry. Technologies such as IoT, AI, and edge computing are further contributing to the changing customer demands & preferences; these technologies are offering great opportunities and challenges for telecommunication companies.

In addition, the operational needs of telecommunication equipment/hardware and demand for secure communications are rising at a fast pace owing to the complex operations of the telecom industry and rising customer demands. The advantages offered by FPGAs, such as easy reconfigurability, low latency operations, flexibility, and efficient hardware acceleration, are expected to drive the growth of FPGAs in the growing telecommunication sector in the forecasted period.

FPGA Market Report Segmentation Analysis

Key segments that contributed to the derivation of the FPGA market analysis are configuration, technology, and end user industry.

- By configuration, the market is segmented into low-end FPGA, mid-range FPGA, and high-end FPGA. The high-end FPGA segment is expected to grow with the highest CAGR.

- Based on the technology, the market is segmented into SRAM-based FPGA, flash-based FPGA, and antifuse-based FPGA. The SRAM-based FPGA segment held the largest market share in 2023.

- By end user industry, the market is segmented into IT and telecommunication, aerospace and defence, industrial, and others. The others segment held the largest market share in 2023.

FPGA Market Share Analysis by Geography

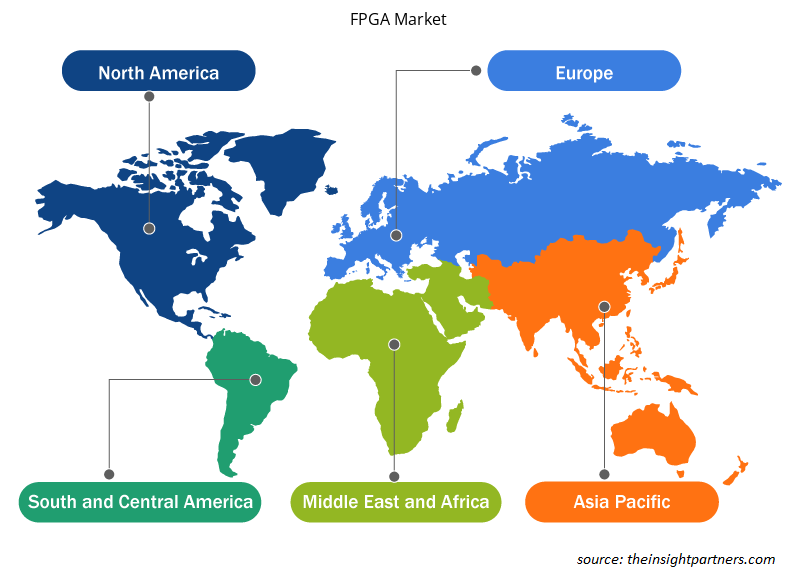

The geographic scope of the FPGA market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South America/South & Central America.

Asia Pacific region is expected to grow with the highest CAGR. The region has one of the robust semiconductors which major countries such as China, India, Taiwan, and Japan. Under government initiatives such as ‘Make In India’ and ‘Made in China 2031’, the government plans to increase its domestic semiconductor production, which fuels the FPGA market in the region.

FPGA Market Regional Insights

The regional trends and factors influencing the FPGA Market throughout the forecast period have been thoroughly explained by the analysts at Insight Partners. This section also discusses FPGA Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Get the Regional Specific Data for FPGA Market

FPGA Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 11.12 Billion |

| Market Size by 2031 | US$ 27.63 Billion |

| Global CAGR (2025 - 2031) | 13.9% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Configuration

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

FPGA Market Players Density: Understanding Its Impact on Business Dynamics

The FPGA Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Market players density refers to the distribution of firms or companies operating within a particular market or industry. It indicates how many competitors (market players) are present in a given market space relative to its size or total market value.

Major Companies operating in the FPGA Market are:

- Advanced Micro Devices, Inc.

- Intel Corporation

- Microchip Technology Inc.

- Lattice Semiconductor

- Achronix Semiconductor Corporation

- QuickLogic

Disclaimer: The companies listed above are not ranked in any particular order.

- Get the FPGA Market top key players overview

FPGA Market News and Recent Developments

The FPGA Marketis evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. The following is a list of developments in the market:

- In May 2023, Intel’s Programmable Solutions Group launched Intel Agilex 7 with the R-Tile chiplet is shipping production-qualified devices in volume for their customers with the first FPGA with PCIe 5.0 and CXL capabilities and the only FPGA with hard intellectual property (IP) supporting these interfaces. The product was launched to deliver leading technology capabilities with 2 times faster PCIe 5.0 bandwidth as well as 4 times higher CXL bandwidth per port when compared to other competitive FPGA products. In September 2023, Intel expanded its Intel Agilex® FPGA portfolio and broadened its Programmable Solutions Group (PSG) offerings to handle the increased demand for customized workloads, including enhanced AI capabilities, and to provide lower total cost of ownership (TCO) and more complete solutions. (Source: Intel, Press Release, 2023)

FPGA Market Report Coverage and Deliverables

The “FPGA Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market dynamics such as drivers, restraints, and key opportunities

- Key future trends

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Global and regional market analysis covering key market trends, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles

Frequently Asked Questions

What will be the market size of the global FPGA market by 2031?

The global FPGA market is expected to reach US$ 27.63 billion by 2031.

What is the incremental growth of the global FPGA market during the forecast period?

The incremental growth expected to be recorded for the global FPGA market during the forecast period is US$ 17.87 billion.

Which are the key players holding the major market share of the global FPGA market?

The key players holding majority shares in the global FPGA market are Advanced Micro Devices, Inc.; Intel Corporation; Microchip Technology Inc.; Lattice Semiconductor; and Achronix Semiconductor Corporation.

What is the estimated market size for the global FPGA market in 2023?

The global FPGA market was estimated to be US$ 9.76 billion in 2023 and is expected to grow at a CAGR of 13.9% during the forecast period 2023 - 2031.

What are the driving factors impacting the global FPGA market?

The growing adoption of digital technologies by the construction sector and the government mandating the use of building information modeling are the major factors that propel the global FPGA market.

What are the future trends of the global FPGA market?

The advent of technologies such as artificial intelligence (AI), machine learning (ML), and big data analytics is anticipated to play a significant role in the global FPGA market in the coming years.

Market Research & Consulting

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Testimonials

I wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA, MANAGING DIRECTOR, PineCrest Healthcare Ltd.The Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

Yukihiko Adachi CEO, Deep Blue, LLC.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Strategic Planning

- Investment Justification

- Identifying Emerging Markets

- Enhancing Marketing Strategies

- Boosting Operational Efficiency

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Yes! We provide a free sample of the report, which includes Report Scope (Table of Contents), report structure, and selected insights to help you assess the value of the full report. Please click on the "Download Sample" button or contact us to receive your copy.

Absolutely — analyst assistance is part of the package. You can connect with our analyst post-purchase to clarify report insights, methodology or discuss how the findings apply to your business needs.

Once your order is successfully placed, you will receive a confirmation email along with your invoice.

• For published reports: You’ll receive access to the report within 4–6 working hours via a secured email sent to your email.

• For upcoming reports: Your order will be recorded as a pre-booking. Our team will share the estimated release date and keep you informed of any updates. As soon as the report is published, it will be delivered to your registered email.

We offer customization options to align the report with your specific objectives. Whether you need deeper insights into a particular region, industry segment, competitor analysis, or data cut, our research team can tailor the report accordingly. Please share your requirements with us, and we’ll be happy to provide a customized proposal or scope.

The report is available in either PDF format or as an Excel dataset, depending on the license you choose.

The PDF version provides the full analysis and visuals in a ready-to-read format. The Excel dataset includes all underlying data tables for easy manipulation and further analysis.

Please review the license options at checkout or contact us to confirm which formats are included with your purchase.

Our payment process is fully secure and PCI-DSS compliant.

We use trusted and encrypted payment gateways to ensure that all transactions are protected with industry-standard SSL encryption. Your payment details are never stored on our servers and are handled securely by certified third-party processors.

You can make your purchase with confidence, knowing your personal and financial information is safe with us.

Yes, we do offer special pricing for bulk purchases.

If you're interested in purchasing multiple reports, we’re happy to provide a customized bundle offer or volume-based discount tailored to your needs. Please contact our sales team with the list of reports you’re considering, and we’ll share a personalized quote.

Yes, absolutely.

Our team is available to help you make an informed decision. Whether you have questions about the report’s scope, methodology, customization options, or which license suits you best, we’re here to assist. Please reach out to us at sales@theinsightpartners.com, and one of our representatives will get in touch promptly.

Yes, a billing invoice will be automatically generated and sent to your registered email upon successful completion of your purchase.

If you need the invoice in a specific format or require additional details (such as company name, GST, or VAT information), feel free to contact us, and we’ll be happy to assist.

Yes, certainly.

If you encounter any difficulties accessing or receiving your report, our support team is ready to assist you. Simply reach out to us via email or live chat with your order information, and we’ll ensure the issue is resolved quickly so you can access your report without interruption.

Get Free Sample For

Get Free Sample For