Hospital Bed Market Trends, Demand & Growth by 2034

Hospital Bed Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Semi-Electric Beds, Electric Beds, and Manual Beds), Usage (Acute Care Beds, Long-Term Care Beds, Psychiatric Care Beds, and Others), Application (Non-Intensive Care Beds and Intensive Care Beds), and End User (Hospitals & Clinics, Elderly Care Facilities, Ambulatory Surgical Centers, and Home Care Settings)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Status : Upcoming

- Report Code : TIPRE00029326

- Category : Consumer Goods

- No. of Pages : 150

- Available Report Formats :

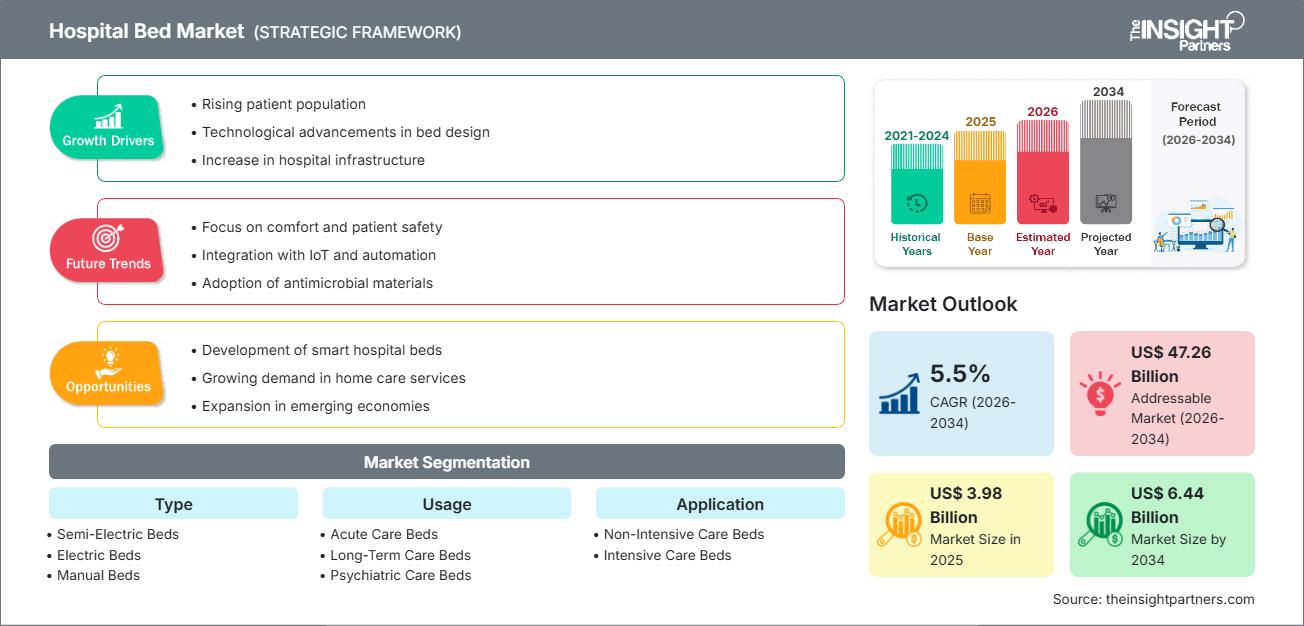

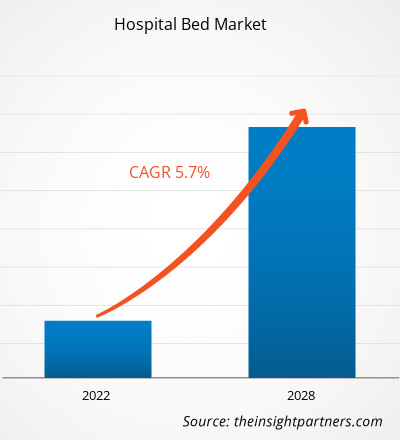

The global hospital bed market size is projected to reach US$ 6.44 billion by 2034 from US$ 3.98 billion in 2025. The market is anticipated to register a CAGR of 5.5% during the forecast period 2026–2034.

Key market dynamics include a heightening global focus on medical infrastructure modernization, rising patient admission rates due to chronic and infectious diseases, and a significant shift toward integrated digital health solutions. Additionally, the market is expected to benefit from the growing geriatric population requiring long-term care, expansion in healthcare capacity across emerging economies, and the increasing inclusion of smart monitoring technologies in high-value intensive care units.

Hospital Bed Market Analysis

The hospital bed market analysis indicates a transformative period where healthcare providers are moving beyond basic mechanical functionality toward integrated clinical ecosystems. Current market data reveals a surge in demand for beds that act as diagnostic hubs, capable of continuous data collection to assist in predictive nursing. While the manual bed segment remains a high-volume staple in cost-sensitive rural and emerging markets, the electric and semi-electric segments are capturing greater value through superior ergonomics and reduced caregiver physical strain. Strategic analysis suggests that market differentiation is increasingly determined by a manufacturer’s ability to integrate pressure injury prevention and fall-detection sensors directly into the bed frame. Furthermore, the market is seeing a localized push for sustainable, eco-designed beds that lower carbon footprints across their lifecycle, aligning with global green healthcare initiatives.

Hospital Bed Market Overview

The hospital bed market has transitioned from providing simple resting platforms to sophisticated medical devices that are central to patient-centric care. Current industry insights highlight that hospital beds are now categorized not just by their power source, but by their specialized clinical application, such as bariatric, psychiatric, or pediatric care. The hospital bed market shows a robust competitive landscape where leading brands are utilizing antimicrobial coatings and modular designs to address the rising threat of hospital-acquired infections (HAIs). In developed regions like North America and Europe, the market is driven by a replacement cycle where aging infrastructure is being traded for smart beds that connect seamlessly to Electronic Health Records (EHR). Meanwhile, in the Asia-Pacific region, rapid hospital construction and the rise of medical tourism are fueling a massive influx of both high-end intensive care units and standard medical-surgical beds, positioning the region as the fastest-growing geographical segment.

The US market is a mature and sophisticated market characterized by advanced healthcare infrastructure and high clinical standards. Growth is propelled by an aging demographic and a rising burden of chronic diseases, necessitating long-term stays. Hospitals increasingly prioritize smart, connected beds to enhance patient safety and operational efficiency.

Market Assessment and Insights

- Global market for Hospital Bed was valued at US$ 3.98 Billion in 2025

- Annual market size is expected to reach US$ 6.44 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 47.26 Billion

- Market is anticipated to register a CAGR of 5.5% during the forecast period

- The United States represents a key market, supported by Rising patient population, Technological advancements in bed design, Increase in hospital infrastructure, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Development of smart hospital beds, Growing demand in home care services, Expansion in emerging economies are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Hill-Rom Holdings, Inc. (Baxter), Stryker, Arjo, Invacare Corporation, PARAMOUNT BED CO., LTD., GF Health Products, Inc., Malvestio SpA, Span America (Savaria Corporation), Savion Industries, Stiegelmeyer GmbH & Co. KG, Medstrom, while analyzing competitive strategies and innovation developments

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONHospital Bed Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Hospital Bed Market Drivers and Opportunities

Market Drivers:

- Increasing Global Geriatric Population: The rise in elderly citizens significantly boosts the demand for specialized beds that cater to mobility issues and long-term age-related health management.

- Technological Integration in Patient Care: The adoption of IoT and AI-driven smart beds that monitor patient vitals and automate repositioning is driving a replacement cycle of outdated manual equipment.

- Expansion of Healthcare Infrastructure: Significant government and private investments in building new multi-specialty hospitals, particularly in developing nations, are creating a steady demand for medical beds.

Market Opportunities:

- Rising Demand for Home Healthcare Solutions: Beyond traditional hospitals, there is a growing opportunity for hospital-grade beds designed for home care settings, focusing on portability and ease of use for family caregivers.

- Growth in Specialized Behavioral Health: Expanding mental health infrastructure presents opportunities for psychiatric care beds designed with specific safety and anti-ligature features.

- Modernization of Intensive Care Units: Strategic partnerships between bed manufacturers and medical software providers can facilitate the deployment of high-margin, connected ICU beds in high-acuity departments.

Hospital Bed Market Report Segmentation Analysis

The Hospital Bed Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Type:

- Semi-Electric Beds: A versatile segment combining manual height adjustment with electric head and foot controls, making them popular in mid-tier clinics and home care.

- Electric Beds: The fastest-growing niche, providing full automation and advanced patient monitoring features favored by high-end acute and intensive care facilities.

- Manual Beds: The dominant volume driver in budget-constrained markets and rural clinics due to their simple mechanical reliability and cost-efficiency.

By Usage:

- Acute Care Beds: Designed for short-term treatment of severe injury or illness, focusing on high patient turnover and ease of sanitization.

- Long-Term Care Beds: Targeted toward nursing homes and rehabilitation centers where comfort and pressure-ulcer prevention are primary requirements.

- Psychiatric Care Beds: Specialized safety-first designs used in behavioral health facilities to minimize patient risk while ensuring durability.

By Application:

- Intensive Care Beds: High-value beds equipped with advanced sensors and support for life-monitoring equipment used in ICUs.

- Non-Intensive Care Beds: Standard medical beds utilized in general wards and recovery rooms for stable patients.

By End User:

- Hospitals & Clinics: The primary revenue contributor, driven by continuous infrastructure upgrades and high patient volumes.

- Elderly Care Facilities: A growing segment fueled by the global demographic shift toward an older population requiring assisted living support.

- Ambulatory Surgical Centers: Benefiting from the trend toward outpatient procedures and the need for high-quality recovery beds.

- Home Care Settings: An emerging high-growth channel for medical beds adapted for residential use.

By Geography:

- North America

- Europe

- Asia-Pacific

- South & Central America

- Middle East & Africa

Hospital Bed Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 3.98 Billion |

| Market Size by 2034 | US$ 6.44 Billion |

| Global CAGR (2026 - 2034) | 5.5% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Hospital Bed Market Players Density: Understanding Its Impact on Business Dynamics

The Hospital Bed Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Hospital Bed Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for medical furniture manufacturers and specialized facility providers to expand.

The hospital bed market is undergoing a significant transformation, moving from traditional manual utility to high-value medical-surgical ecosystems. Growth is driven by the rising prevalence of chronic conditions, a surge in specialized ICU capacity demand, and the expansion of long-term care. Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds a leading share globally, driven by premium technology adoption and high healthcare spending.

- Key Drivers:

- Widespread replacement of traditional beds with smart systems to reduce hospital-acquired conditions

- Strong government funding for critical care upgrades and trauma center expansions

- Rising preference for high-tech home healthcare beds for post-operative recovery

- Trends: Integration of AI-driven sensors for continuous patient monitoring and a focus on bariatric-specific designs to meet demographic needs.

2. Europe

- Market Share: Holds a significant global share, anchored by robust public healthcare systems in Germany, France, and the UK.

- Key Drivers:

- Strict regulatory standards for patient safety and ergonomic protection for nursing staff

- Established processing infrastructure for large-scale hospital bed sterilization and maintenance

- Aging population driving high demand for rehabilitative and long-term care beds

- Trends: A strategic shift toward eco-designed beds using sustainable materials and advanced infection control surfaces to meet European Green Deal standards.

3. Asia-Pacific

- Market Share: The fastest-growing region, with China and India acting as the primary drivers for hospital infrastructure development.

- Key Drivers:

- Massive public and private investments in building smart hospitals and multi-specialty centers

- Rapid urbanization and government initiatives to improve bed-to-patient ratios

- Rising middle-to-high income segments seeking westernized luxury inpatient experiences

- Trends: Heavy reliance on B2B contracts for large-scale bed deployments and the growth of local manufacturing hubs for both manual and electric models.

4. South and Central America

- Market Share: Emerging market with a growing private hospital sector in countries like Brazil and Chile.

- Key Drivers:

- Modernization of existing facilities to attract medical tourism and improve local patient outcomes

- Rising awareness of specialized beds for maternity and psychiatric care

- Transition from manual to semi-electric beds in urban private clinics

- Trends: Growth of boutique ambulatory surgical centers and the introduction of farm-to-bed supply chains for localized equipment maintenance.

5. Middle East and Africa

- Market Share: Developing market transitioning toward formalized healthcare standards through strategic investment.

- Key Drivers:

- Large-scale hospital projects in Saudi Arabia and the UAE (e.g., Neom and Dubai Healthcare City)

- High demand for durable, low-maintenance beds in arid climates

- Strategic focus on increasing local food security and medical supply chain resilience

- Trends: Implementation of modern milking and refrigeration technologies (for therapeutic beds) and a focus on high-nutrient support for pediatric hospital settings.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Baxter International Inc. (Hillrom), Stryker Corporation, and Getinge AB. Regional specialists and niche players like LINET Group SE (Czech Republic) and Paramount Bed Co., Ltd. (Japan), alongside medical equipment innovators, such as Invacare Corporation and Arjo AB, also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Digital Transformation: Positioning hospital beds as smart hubs that collect data, alert nurses of patient movement, and integrate with electronic health records.

- Specialized Application Focus: Offering tailored solutions for specific clinical needs, including pediatric beds, bariatric frames, and specialized ICU platforms.

- Supply Chain Control: Managing the end-to-end process from ergonomic design to local assembly to ensure quality and compliance.

Opportunities and Strategic Moves

- Partner with high-end digital health platforms and IT providers to tap into the surging demand for connected and smart hospital beds in the Asia-Pacific and North American markets.

- Incorporate sustainable manufacturing practices and circular economy certifications to appeal to environmentally conscious healthcare administrators and public health agencies.

Major Companies operating in the Hospital Bed Market are:

- Hill-Rom Holdings, Inc. (Baxter)

- Stryker

- Arjo

- Invacare Corporation

- PARAMOUNT BED CO., LTD.

- GF Health Products, Inc.

- Malvestio SpA

- Span America (Savaria Corporation)

- Savion Industries

- Stiegelmeyer GmbH & Co. KG

- Medstrom

Disclaimer: The companies listed above are not ranked in any particular order.

Hospital Bed Market News and Recent Developments

- In September 2025, Invacare announced the introduction of the New Accent Medical Profiling Bed, designed to improve, rest, sleep, and independence every day. It is providing comfortable solutions that meet the highest safety and quality standards. The new Accent is no exception and offers a simple, affordable quality solution, without compromise.

- In February 2025, Stryker announced the launch of the ProCeed hospital bed, offering simplicity while enhancing care across various regions. ProCeed helps keep patients and care teams safe with various design elements, including low bed height, which supports patient mobility and reduces the risk of injury from falls.

Hospital Bed Market Report Coverage and Deliverables

The Hospital Bed Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Hospital Bed Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Hospital Bed Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Hospital Bed Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Hospital Bed Market

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For