Hospital Supplies Market Growth and Forecast by 2031

Hospital Supplies Market Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Syringes, Patient Examination Devices, Mobility Aids & Transportation Equipment, Operating Room Equipment, Sterilization & Disinfectant Equipment, and Disposable Hospital Supplies), and Geography

Historic Data: 2021-2023 | Base Year: 2021 | Forecast Period: 2023-2031- Report Date : Mar 2026

- Report Code : TIPRE00003520

- Category : Life Sciences

- Status : Data Released

- Available Report Formats :

- No. of Pages : 150

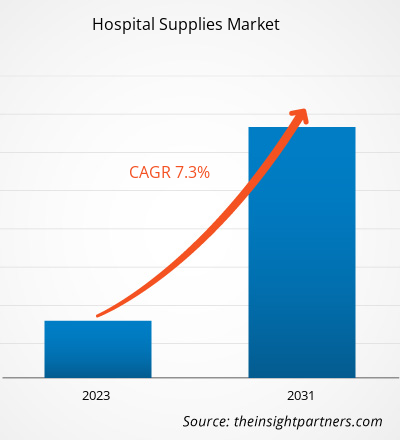

The Hospital Supplies Market was valued at US$ 85.71 billion in 2021 and is expected to reach US$ 166.4 billion by 2031. The market is expected to register a CAGR of 7.3% from 2023–2031. Improved infrastructures of hospitals and integration of novel technologies in healthcare facilities are likely to remain key Hospital Supplies Market trends.

Hospital Supplies Market Analysis

Rising Infectious and Communicable Diseases

The COVID-19 pandemic has warned the extent to which healthcare settings have to contribute to reduce the spread of infections and cause less harm to patients & healthcare workers & visitors. However, if good hygiene and other cost-effective practices are followed, 70% of infectious diseases can be prevented. According to the World Health Organization (WHO) report, out of every 100 patients in acute-care hospitals, seven patients in high-income countries and 15 patients in low and middle-income countries acquire at least one healthcare-associated infection (HAI) during hospital stay.

Therefore, rising infectious and communicable diseases accounts for increase in healthcare burden on low income and middle-income countries. According to the World Health Organization (WHO) report, infectious diseases account for almost half of the overall health spending in low-income countries, whereas in middle-income countries, infectious diseases account for almost one-third of the overall health spending. Further, low-income countries mostly spend their domestic public funds to control infectious diseases, while middle-income countries spend more on noncommunicable diseases.

Source: World Health Organization (WHO)

Therefore, with rising infectious diseases, global demand for hospital medical supplies such as protection kits, medicines, equipment, and among others is increasing exponentially. The aforementioned factors are responsible for influential hospital supplies market growth during 2021-2031.

Hospital Supplies Market Overview

Technology, innovation, and smart technological solutions continue to influence hospital supplies significantly. Rising infectious and communicable diseases and efficient supply chain for medical suppliesare the most influential factors responsible for Hospital Supplies Market growth. Technological advancement is a key trend for Hospital Supplies Market growth. Technological advancements such as AI will provide lucrative market opportunity.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONHospital Supplies Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Hospital SuppliesMarket Drivers and Opportunities

Efficient Supply Chain for Medical Supplies to Favor Market

The evolution of the healthcare supply chain has been substantially driven by regulatory changes, and shifts in healthcare practices. The key developments include technology integration, advancements in logistics & distribution, risk, management & resilience, sustainability & ethical sourcing, and others. Also, hospitals are heavily dependent on regional suppliers for efficient medical supply. Therefore, following efficient supply chain practices for effective supplies management will contribute significantly in the coming years.

Technological Advancements in Hospital Supplies Market– An Opportunity

Inventory management is challenging for hospitals aiming for efficient medical supply to facilities located at diverse location within the hospital premises. Such challenges can result in improper information flow, disruption in core medical supplies within the hospital departments, and improper handling resulting in spread of healthcare-associated infections. To overcome such barriers of unorganized hospital supplies, technological advancements such as AI applications will continue to emerge. For example, leveraging dynamic real-time inventory visibility through IoT-based technologies through AI can drive processes, optimize the minimum and maximum inventory counts, and automatically replenish to match several hospitals' consumption at diverse locations, including operating rooms, catheter labs, nursing floors, and in-hospital pharmacies. Therefore, adoption of technologically-advanced tools such as AI will provide lucrative market opportunities accounting for considerable market share in the coming years for Hospital Suppliesmarket.

Hospital Supplies

Market Report Segmentation Analysis

Key segments that contributed to the derivation of the Hospital Supplies Market analysis are candidature and services.

- Based on type, the Hospital Supplies Market is segmented into syringes, patient examination devices, mobility aids & transportation equipment, operating room equipment, sterilization & disinfectant equipment, and disposable hospital supplies. The sterilization & disinfectant equipment may hold a larger market share in 2023.

Hospital Supplies Market Share Analysis by Geography

The geographic scope of the Hospital SuppliesMarket report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South America/South & Central America.

North America has dominated the Hospital Supplies Market. In North America, US accounts considerable share for hospital supplies. Presence of top medical suppliers present in the US and hospital collaboration with leading suppliers are the most influential factors responsible for market growth. Asia Pacific is anticipated to grow with the highest CAGR in the coming years.

Hospital Supplies

Hospital Supplies Market Regional InsightsThe regional trends and factors influencing the Hospital Supplies Market throughout the forecast period have been thoroughly explained by the analysts at The Insight Partners. This section also discusses Hospital Supplies Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

Hospital Supplies Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 85.71 Billion |

| Market Size by 2031 | US$ 166.4 Billion |

| Global CAGR (2023 - 2031) | 7.3% |

| Historical Data | 2021-2023 |

| Forecast period | 2023-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Hospital Supplies Market Players Density: Understanding Its Impact on Business Dynamics

The Hospital Supplies Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

- Get the Hospital Supplies Market top key players overview

Hospital Supplies Market News and Recent Developments

The Hospital SuppliesMarket is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. The following is a list of developments in them market for Hospital Supplies and strategies:

- In July 2022, Cardinal Health announced signing a contract with Quipt Home Medical Corp for selling and distributing hospital supplies. The contract aims to sell hospital supplies worldwide through Cardinal Health at-Home business unit.

Hospital SuppliesMarket Report Coverage and Deliverables

The “Hospital SuppliesMarket Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market dynamics such as drivers, restraints, and key opportunities

- Key future trends

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Global and regional market analysis covering key market trends, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments

- Detailed company profiles

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Related Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For