Industrial Automation Market Analysis and Opportunities by 2030

Coverage: By Component (Hardware and Software), System (Supervisory Control and Data Acquisition, Distributed Control System, Programmable Logic Control, and Other), and End User (Oil & Gas, Automotive, Food & Beverages, Chemical & Materials, Aerospace & Defense, and Others), and Geography

- Status : Published

- Report Code : TIPRE00025985

- Category : Electronics and Semiconductor

- No. of Pages : 217

- Available Report Formats :

- Last update date : June 20, 2025

2022 Market Size

US$ 171.23 Bn

Base year value

2030 Forecast

US$ 322.67 Bn

Projected by 2030

CAGR 2023-2030

8.2 %

Growth rate

Addressable Market

US$ 1,984.95 Bn

(2023-2030)

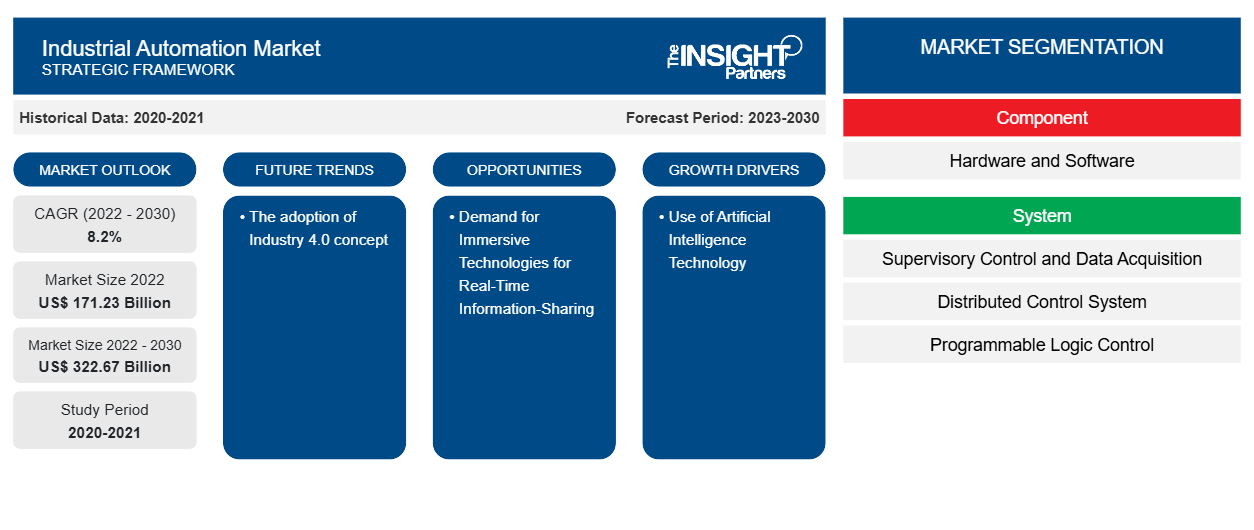

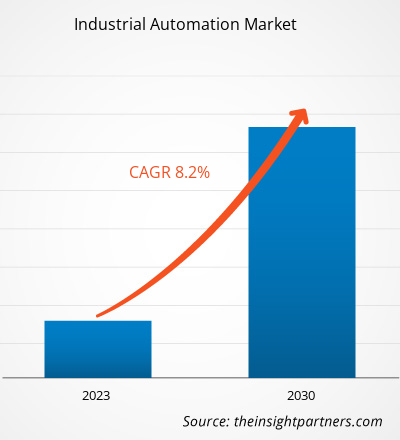

The industrial automation market size is projected to reach US$ 322.67 billion by 2030 from US$ 171.23 billion in 2022. The market is expected to register a CAGR of 8.2% during 2022–2030. The adoption of the Industry 4.0 concept is likely to remain a key trend in the market.

Industrial Automation Market Analysis

In addition to the growing adoption of AI and machine learning, the industrial automation market is being propelled by the increasing convergence of Information Technology (IT) and Operational Technology (OT). This integration is enabling manufacturers to gain greater visibility into operations, improve decision-making, and achieve enhanced control over production processes. Smart sensors, connected devices, and industrial IoT platforms are generating vast amounts of real-time data, which, when analyzed using AI algorithms, support predictive analytics, anomaly detection, and process optimization. Governments in both developed and emerging economies are recognizing the strategic importance of automation in boosting productivity, minimizing human error, and enhancing workplace safety. As a result, several national programs—such as Germany’s Industry 4.0, China’s Made in China 2025, and India’s Make in India initiative—are actively incentivizing investments in automation technologies. Furthermore, the incorporation of machine vision systems with deep learning capabilities is enhancing quality inspection and defect detection across industries such as electronics, automotive, and food & beverage. The growing demand for personalized, high-quality products delivered quickly and cost-effectively is further encouraging businesses to adopt automated and digital manufacturing solutions. As industrial operations become more complex, scalable automation solutions will play a critical role in maintaining competitiveness, agility, and resilience in global markets.

Industrial Automation Market Overview

Industrial automation replaces human intervention by using control systems such as robots, computers, and information technology to operate various machinery in an industry. Depending on the operations involved, industrial automation control systems are divided into two categories: process plant automation and manufacturing automation. Industrial automation improves product quality, reliability, and production rate while lowering manufacturing and design costs through the use of new, innovative, and integrated technologies and services. They have a variety of characteristics, including high productivity, quality, flexibility, and information correctness, which are projected to promote the use of automation in the industrial sector during the forecast period. Furthermore, the spike in the adoption of automation solutions in oil and gas, manufacturing, chemicals and materials, pharmaceuticals, and other industries is pushing industrial automation.

Market Assessment and Insights

- Asia Pacific dominated the market with 39.1% share in 2022.

- Asia Pacific is poised to grow at a CAGR of 9.2% over the forecast period.

- United States market is projected to grow at a CAGR of 8% over the forecast period.

- By Component, the Hardware segment accounted for the largest market share of 68.2% in 2022.

- By Hardware, the Robots segment is anticipated to witness the fastest growth, registering a CAGR of 9.8% over the forecast period

- By System, the DCS segment accounted for the largest market share of 28.8% in 2022.

- By End User, the Automotive segment is anticipated to witness the fastest growth, registering a CAGR of 9.5% over the forecast period

- The report profiles key industry players such as ABB Ltd, Emerson Electric Co, Rockwell Automation Inc, Siemens AG, OMRON Corp, Yokogawa Electric Corp, Hitachi Ltd, Mitsubishi Electric Corp, Koyo Electronic Industries Co., Ltd., Industrial Automation (M) Sdn Bhd, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Industrial Automation Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Industrial Automation Market Drivers and Opportunities

Use of Artificial Intelligence Technology to Favor the Market

Artificial intelligence (AI) is transforming manufacturing in incredible ways. AI enables machines to learn, adapt, and make decisions autonomously. Manufacturers utilize the technology to uncover asset patterns and anomalies to optimize production and save downtime. For example, incorporating AI into industrial robots and drones enhances precision and aids in activities such as inspection, maintenance, and material handling. This decreases the need for human involvement, lowers the danger of accidents, increases maintenance efficiency, and extends equipment life. Moreover, operations technology (OT) engineers who are familiar with operations and equipment are increasingly using sophisticated AI technologies with visual, point-and-click user interfaces (UI). The availability of prebuilt machine learning (ML) apps and industrial demand for automation is fueling the market.

Demand for Immersive Technologies for Real-Time Information-Sharing

Virtual reality (VR) and augmented reality (AR) are immersive technologies that enable real-time information sharing to aid worker training, eliminate human errors, and boost performance. That implies VR and AR may add significant commercial value by improving worker safety, increasing productivity, and reducing downtime. AR can aid industrial enterprises by facilitating return-to-work measures such as remote collaboration, remote assistance, augmented work instructions, and 3D training. AR is also assisting with longer-term, future-of-work strategies aimed at closing the skills gap and driving significant gains. Augmented reality is becoming increasingly important in the workplace.

- Stream Industrial Internet of Things (IIoT) and sensor data to improve condition monitoring, troubleshooting, and repairs.

- View immersive 3D work instructions for assembly, inspection, and maintenance procedures.

- Get step-by-step guidance and on-demand assistance from seasoned professionals.

- Pass comments on the circumstances they observe in the factory or field back into the connected digital thread, enabling closed-loop feedback throughout the company.

- Operators and service technicians use highly demanding augmented reality to streamline operational processes.

Industrial Automation Market Report Segmentation Analysis

Key segments that contributed to the derivation of the industrial automation market analysis are component, system, and end user.

- Based on component, the industrial automation market is divided into hardware and software. The hardware segment held a larger market share in 2022.

- By system, the market is segmented into supervisory control and data acquisition, distributed control systems, programmable logic control, and others. The supervisory control and data acquisition segment is anticipated to expand during the forecast period.

- Based on end users, the market is divided into oil & gas, automotive, food & beverages, chemical & materials, aerospace & defense, and others. The oil & gas segment held the largest market share in 2022.

Industrial Automation Market Share Analysis by Geography

The geographic scope of the industrial automation market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The market in Asia Pacific is projected to expand during the forecast period due to the presence of key players. Omron Corporation, Mitsubishi Electric Corporation, Hitachi Ltd., and others are offering their customers technologically advanced factory automation products that improve their operational efficiencies. Expanding industries and increasing adoption of industrial automation technologies are boosting the market.

Industrial Automation Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2022 | US$ 171.23 Billion |

| Market Size by 2030 | US$ 322.67 Billion |

| Global CAGR (2022 - 2030) | 8.2% |

| Historical Data | 2020-2021 |

| Forecast period | 2023-2030 |

| Segments Covered |

By Component

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Industrial Automation Market Players Density: Understanding Its Impact on Business Dynamics

The Industrial Automation Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Industrial Automation Market News and Recent Developments

The industrial automation market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the industrial automation market are listed below:

- In 2023, Emerson Electric's acquisition of National Instruments for US$ 8.2 billion in April 2023 marked a strategic move to fortify its presence in industrial automation. The deal aligned with Emerson's pursuit of testing and measurement growth, tapping into National Instruments' software-driven automated systems to deliver enhanced profitability and industry diversification. This step reflected the surge in demand for advanced automation solutions. (Source: Emerson Electric Co., Company Website, October 2023)

- ABB India secured a significant contract for the electrification and automation of ArcelorMittal Nippon Steel India's advanced cold rolling mill in Hazira. ABB's technology aimed to enhance energy efficiency, zinc consumption optimization, and corrosion resistance, aligning with AM/NS India's sustainability goals. This collaboration showcased industrial automation's transformative potential. (Source: ABB Ltd, Company Website, June 2023)

Industrial Automation Market Report Coverage and Deliverables

The “Industrial Automation Market Size and Forecast (2020–2030)” report provides a detailed analysis of the market covering below areas:

- Industrial automation market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Industrial automation market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Industrial automation market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the industrial automation market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends