North America Carrier Testing Services Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Coverage: By Type (Expanded Carrier Screening and Targeted Disease Carrier Screening), Medical Conditions (Pulmonary Conditions, Hematological Conditions, Neurological Conditions, and Other Medical Conditions), and End User (Hospital-Based Laboratories, Diagnostic Laboratories, and Other End Users)

- Status : Published

- Report Code : TIPRE00042307

- Category : Life Sciences

- No. of Pages : 172

- Available Report Formats :

- Last update date : April 29, 2026

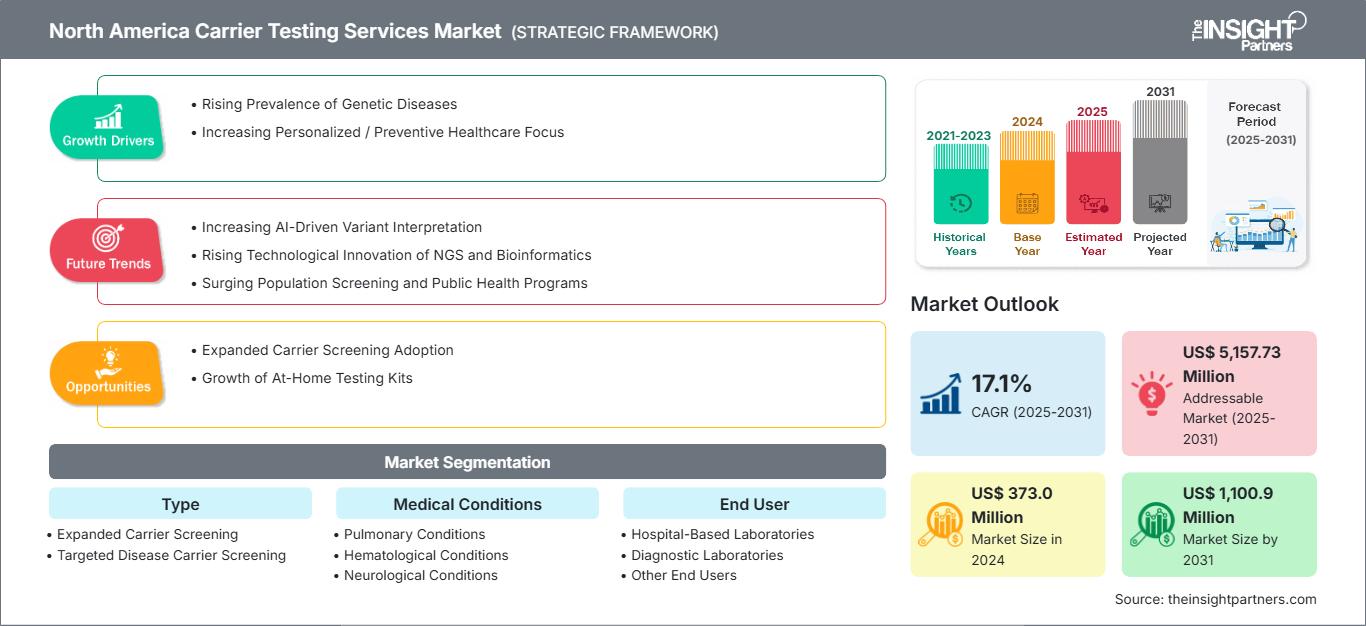

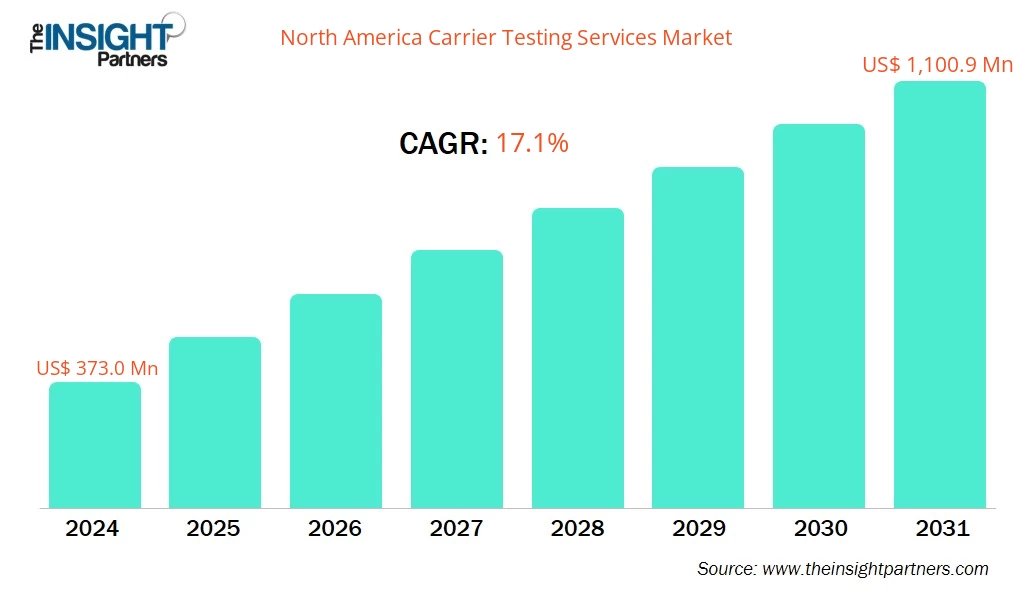

2024 Market Size

US$ 373.0 Mn

Base year value

2031 Forecast

US$ 1,100.9 Mn

Projected by 2031

CAGR 2025-2031

17.1 %

Growth rate

Addressable Market

US$ 5,157.73 Mn

(2025-2031)

The North America Carrier Testing Services Market size is expected to reach US$ 1,100.9 Million by 2031 from US$ 373.0 Million in 2024. The market is estimated to record a CAGR of 17.1% from 2025 to 2031.

Executive Summary and North America Carrier Testing Services Market Analysis:

The North America carrier testing services market is segmented into the US, Canada, and Mexico. North America dominates the carrier testing services market of the most reliable and mature regions. The penetration of carrier screening into reproductive care is a result of the region's advanced healthcare infrastructure, high awareness of genetic disorders, and extensive use of next-generation sequencing. In the US, carrier testing is a standard part of preconception and prenatal procedures, with the assistance of genetic counselors who form a solid network and support couples in understanding their risks. The insurance system and healthcare policy of the region are supportive of gene screening, thereby facilitating testing by individuals. Major testing companies and labs have a strong presence in North America, which is instrumental in achieving quick turnaround times and providing high-quality services. The area is attracting heavy investment from public and private players in research for broader carrier panels, AI-driven interpretation, and more effective sequencing methods. These factors maintain a high demand level among fertility clinics, obstetrics practices, and diagnostic labs, and allow North America to be a trendsetter in preventive reproductive genomics. However, the competitive atmosphere is intense, and companies must consistently generate new ideas to stay ahead of the competition. North America is likely to remain at the forefront of the global carrier testing market, both in terms of volume and technological advancements.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

North America Carrier Testing Services Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

North America Carrier Testing Services Market Segmentation Analysis:

- By Type, the North America Carrier Testing Services Market is segmented into Expanded Carrier Screening and Targeted Disease Carrier Screening. The Expanded Carrier Screening segment dominated the market in 2024.

- By Medical Conditions, the North America Carrier Testing Services Market is segmented into Pulmonary Conditions, Hematological Conditions, Neurological Conditions, and Other Medical Conditions. The Pulmonary Conditions segment dominated the market in 2024.

- By End User, the North America Carrier Testing Services Market is segmented into Hospital-Based Laboratories, Diagnostic Laboratories, and Other End Users. The Hospital-Based Laboratories segment dominated the market in 2024.

North America Carrier Testing Services Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 373.0 Million |

| Market Size by 2031 | US$ 1,100.9 Million |

| CAGR (2025 - 2031) | 17.1% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

North America Carrier Testing Services Market Players Density: Understanding Its Impact on Business Dynamics

The North America Carrier Testing Services Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

North America Carrier Testing Services Market Outlook

AI-driven variant interpretation is changing the way genetic data is handled, comprehended, and shared. In sequencing panels, increasingly comprehensive panels result in a plethora of variants of uncertain significance (VUS). This aspect makes it very difficult for traditional manual workflows to keep pace. As of 2018, there were ~75,000 genetic tests available in the market, with nearly ten new tests entering the market every day. As per the study "Trends in Availability of Genetic Tests in the United States, 2012-2022," published in 2023, ~129,624 and 197,779 genetic tests in the US and globally, respectively, have been made accessible and submitted to the genetic testing registry as of November 2022. These tests have been extended from single-gene tests to panels that look at multiple genes. Nowadays, AI models such as deep learning and transformer-based large language models (LLMs), which have recently been applied to DNA sequences, are gaining increasing attention as valuable tools for predicting the functional impact of these variants. The models do this by "reading" DNA, similar to a natural language.

Machine learning algorithms, according to recent experiments, can classify clinically reportable variants with very high accuracy, which drastically reduces the workload of expert geneticists. New models can justify their predictions through understandable results ("waterfall plots") that give the scientists a clearer idea of the factors influencing the decision. At the same time, the application of AI in disease contexts, such as carrier screening, allowed researchers to predict enzyme activity for variants previously labeled as unknown, thereby increasing actionable insights.

Explainable AI-powered tools are currently simplifying the task of variant analysis in genomic labs working with real-world data. Software such as Emedgene (from Illumina) can reduce the time for variant interpretation by up to 50-75% in rare disease genomics. The idea of AI platforms that seamlessly integrate multi-omics data, utilize predictive analytics, and are in sync with electronic health records - all aimed at providing faster and more clinically relevant interpretations - is gaining traction. This trend opens up a range of implications for the business side of the game. By employing AI-powered interpretation tools, carrier testing companies can enhance their performance, reduce their operating costs, and provide clinicians and patients with more straightforward and reliable reports. Once AI is established as the norm, companies operating in this field will probably differentiate themselves by developing their own interpretation pipelines, creating automated reporting systems, and building decision-support tools. Eventually, it will facilitate the expansion of carrier screening to a broader population, and thus, the industry will be able to meet the increasing demand for personalized reproductive health services.

North America Carrier Testing Services Market Country Insights

By country, the North America Carrier Testing Services Market is segmented into the United States, Canada, and Mexico. The United States held the largest share in 2024.

The healthcare system in the United States is brilliantly sophisticated and it is heavily inclined toward genetic testing and reproductive medicine. Clinical practice regularly combines genetic counseling, next-generation sequencing (NGS), and comprehensive carrier screening panels as part of the routine. A number of reputable laboratory and biotechnology firms invest in CLIA-certified facilities, which enable them to provide highly accurate and reliable carrier screening services. The use of expanded carrier screening in reproductive healthcare has become a norm, and it is frequently applied to preconception planning, prenatal care, and infertility treatments. Legal and ethical measures, such as the Genetic Information Nondiscrimination Act (GINA), ensure that individuals are protected from the negative consequences associated with genetic information and thus, trust in genetic testing grows. The practice of carrier screening is becoming more intertwined with assisted reproductive technologies, especially in vitro fertilization (IVF) as couples are trying to know and mitigate the risk of passing on genetic disorders. In conclusion, the U.S. market is characterized by fierce competition, continuous innovation, and a strong commitment to the development of preventive, personalized methods of reproductive and genetic health.

North America Carrier Testing Services Market Company Profiles

Some of the key players operating in the market include F. Hoffmann-La Roche Ltd, Quest Diagnostics Inc, Eurofins Scientific SE, Myriad Genetics Inc, Laboratory Corp of America Holdings, MedGenome Inc, Gene By Gene Ltd, Thermo Fisher Scientific Inc., Fulgent Genetics, Inc, and Illumina, Inc.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

North America Carrier Testing Services Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends