North America Paracetamol Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Coverage: By Dosage Form (Tablet, Capsule, and Others), Indication (Mild and Moderate Pain, Fever, and Others), Route of Administration (Enteral and Parenteral), and Distribution Channel (Retail Pharmacies, Hospital Pharmacies, and Online Pharmacies)

- Status : Published

- Report Code : TIPRE00042860

- Category : Life Sciences

- No. of Pages : 197

- Available Report Formats :

- Last update date : May 08, 2026

2024 Market Size

US$ 4,408.6 Mn

Base year value

2031 Forecast

US$ 6,246.7 Mn

Projected by 2031

CAGR 2025-2031

5.2 %

Growth rate

Addressable Market

US$ 37,991.93 Mn

(2025-2031)

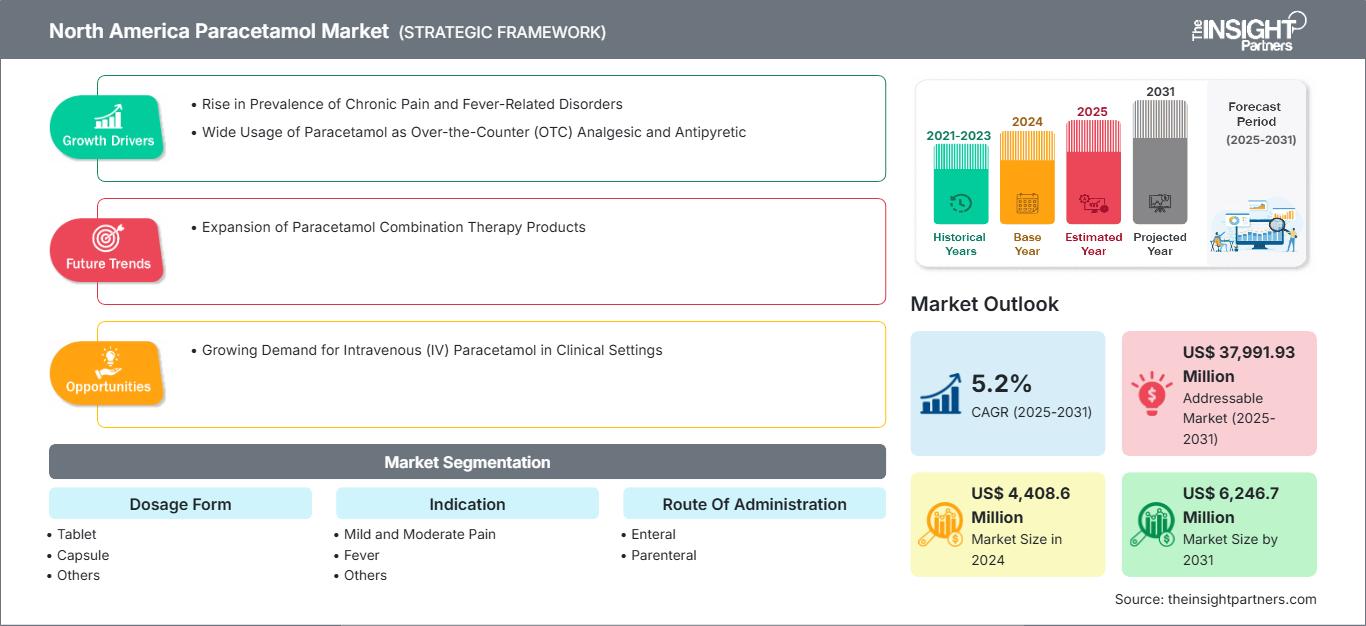

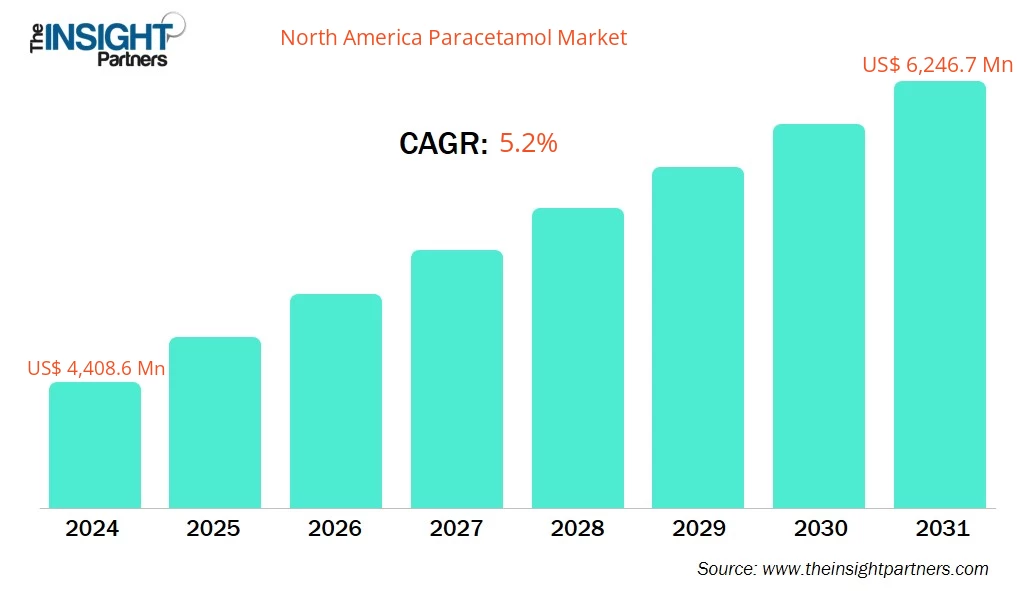

The North America Paracetamol Market size is expected to reach US$ 6,246.7 Million by 2031 from US$ 4,408.6 Million in 2024. The market is estimated to record a CAGR of 5.2% from 2025 to 2031.

Executive Summary and North America Paracetamol Market Analysis:

The North America paracetamol market is segmented into the US, Canada, and Mexico. North America is expected to lead the paracetamol market throughout the forecast period. This growth can be attributed to several factors, including the presence of major industry players, a high prevalence of conditions such as fever, headaches, and migraines in the region, and a well-established healthcare infrastructure. These elements contribute significantly to North America's substantial market share.In particular, the market growth in the US is projected to be strong during this period. As reported in a January 2021 article by the American Migraine Foundation, over 4 million adults in the US live with chronic daily migraines, which means they experience at least 15 headache days each month. Given the increasing patient population and rising disposable income, these statistics suggest that the market for paracetamol in the US is likely to experience significant growth.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

North America Paracetamol Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

North America Paracetamol Market Segmentation Analysis:

- By Dosage Form, the North America Paracetamol Market is segmented into Tablet, Capsule, and Others. The Tablet segment dominated the market in 2024.

- By Indication, the North America Paracetamol Market is segmented into Mild and Moderate Pain, Fever, and Others. The Mild and Moderate Pain segment dominated the market in 2024.

- By Route of Administration, the North America Paracetamol Market is segmented into Enteral and Parenteral. The Enteral segment dominated the market in 2024.

- By Distribution Channel, the North America Paracetamol Market is segmented into Retail Pharmacies, Hospital Pharmacies, and Online Pharmacies. The Retail Pharmacies segment dominated the market in 2024.

North America Paracetamol Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 4,408.6 Million |

| Market Size by 2031 | US$ 6,246.7 Million |

| CAGR (2025 - 2031) | 5.2% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Dosage Form

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

North America Paracetamol Market Players Density: Understanding Its Impact on Business Dynamics

The North America Paracetamol Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

North America Paracetamol Market Outlook

Chronic pain is increasingly recognized as a profound and expanding public health challenge worldwide. It now affects roughly one in five adults globally, equivalent to more than 1.5 billion people. Prevalence estimates vary widely across regions, ranging from 8% to over 40%, depending on factors such as age, socio-economic status, and the definitions used, as reported by the Boston University School of Public Health. Chronic musculoskeletal disorders, including low back pain and neck pain, and headache disorders (notably tension-type headache and migraine), are the predominant contributors, with Global Burden of Disease data reporting over 2.6billion cases of headache disorders and musculoskeletal disorders in 2019. Between 2009 and 2021, global self-reported pain prevalence rose from 26.3% to 32.1%, adding half a billion additional pain sufferers worldwide, with more rapid increases seen among women, younger adults, the least educated, and economically disadvantaged groups.

Moreover, the rise of chronic neuropathic pain syndromes, including chemotherapy-induced peripheral neuropathy (CIPN), which affects over 40% of cancer patients receiving neurotoxic chemotherapies, further expands indications for paracetamol use in multimodal pain control regimens. In the US, approximately 20.9% of adults (about one in five) experienced chronic pain in 2021, and around 6.9% met criteria for high-impact chronic pain, causing difficulty with work or life activities.

Moreover, incidence data showed that in 2020, the rate of new chronic pain diagnoses in the US was 52.4 per 1,000 persons per year, with a growing rate of diabetes or depression, and nearly two-thirds continued to experience pain a year later, according to a study by the National Institutes of Health (NIH). Compounding the issue, chronic pain is often persistently undertreated. According to WHO estimates, approximately 80% of individuals experiencing severe pain worldwide do not receive sufficient relief. This issue is particularly pronounced in low- and middle-income countries, as well as among women and minority groups. Women, in particular, bear a disproportionate share of the burden, yet receive less effective pain management overall due to systemic bias and insufficient research representation.

Conditions such as enteric fever (typhoid) remain prevalent on the fever-related disorders side, while enteric fever mortality has slightly declined since 2017, the residual high incidence continues to drive the demand for antipyretic and analgesic treatments. Environmental and social determinants-such as urbanization, aging populations, sedentary lifestyles, poor ergonomics, mental stress, and climate change-are also taxing health systems by raising the incidence of both pain and fever-triggering infections such as dengue and waterborne diseases, whose frequencies are increasing due to expanding vector ranges and changing climatic conditions. These intersecting trends-a rising population with chronic pain and fever episodes, persistent under-treatment, health inequities, and structural factors accelerating both types of disorders-are driving sustained and increasing consumption of over-the-counter antipyretic/analgesics such as paracetamol. As chronic pain sufferers often rely on OTC relief in the absence of specialist care, and fever conditions frequently prompt immediate symptomatic treatment, paracetamol remains a first-line, low-cost, widely accessible option. Manufacturers respond by widening availability, emphasizing safety messaging, and incorporating paracetamol into a broader range of combination therapies.

North America Paracetamol Market Country Insights

By country, the North America Paracetamol Market is segmented into the United States, Canada, and Mexico. The United States held the largest share in 2024.

The US paracetamol market is one of the world's most robust and mature, reflecting the country's longstanding reliance on paracetamol (acetaminophen) as a primary solution for pain and fever management. Paracetamol's accessibility, effectiveness, and longstanding over-the-counter (OTC) status have kept it at the center of American healthcare for decades. According to a report from the National Library of Medicine, in the US, acetaminophen, commonly known by the brand Tylenol, remains the most widely used over-the-counter analgesic and antipyretic, supported by decades of clinical adoption and consumer familiarity. In 2024, it ranked among the most frequently prescribed medications with over 5 million prescriptions issued, underscoring its entrenched role in pain and fever management. Usage is driven by widespread chronic pain prevalence. About 20% of US adults report chronic pain; low back pain affects roughly 26%, and neck pain about 14%. Acetaminophen is the preferred non-opioid first option among healthcare providers due to concerns about the safety of opioids. Public health guidance and FDA regulations now mandate warning labels regarding hepatotoxicity risk and limit acetaminophen content in prescription combination products to 325 mg per dose to reduce overdose incidence, reflecting ongoing safety vigilance around acute liver failure cases currently estimated at 56,000 emergency visits, 2,600 hospitalizations, and nearly 460 deaths annually in the US due to overdose.

North America Paracetamol Market Company Profiles

Some of the key players operating in the market include GSK Plc, Teva Pharmaceutical Industries Ltd, Sanofi SA, Johnson & Johnson, Cipla Ltd, Sun Pharmaceutical Industries Ltd, Dr. Reddy's Laboratories Ltd, Mallinckrodt Plc, Granules India Ltd, and IOL Chemicals and Pharmaceuticals Ltd.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

North America Paracetamol Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends