Oilfield Service Market Overview and Growth by 2031

Coverage: By Service Type (Well Completion, Wire line, Artificial Lift, Perforation, Drilling and Completion Fluids, and Others), Application (Onshore and Offshore), and Geography

- Status : Data Released

- Report Code : TIPMC100001361

- Category : Energy and Power

- No. of Pages : 150

- Available Report Formats :

- Last update date : February 15, 2025

2023 Market Size

US$ 111.56 Bn

Base year value

2031 Forecast

US$ 175.96 Bn

Projected by 2031

CAGR 2023-2031

5.9 %

Growth rate

Addressable Market

US$ 1,165.12 Bn

(2023-2031)

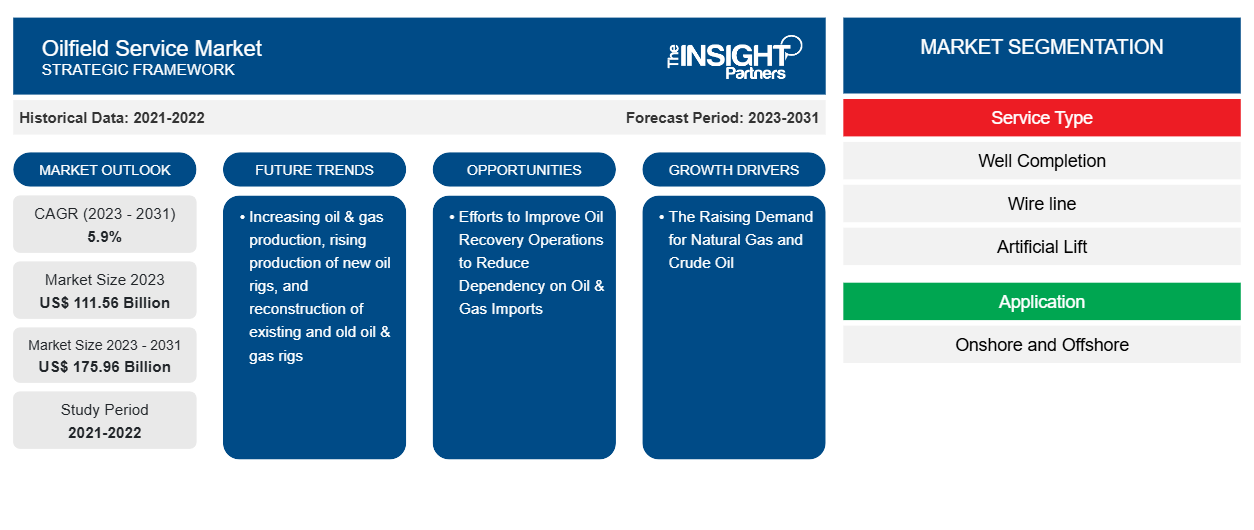

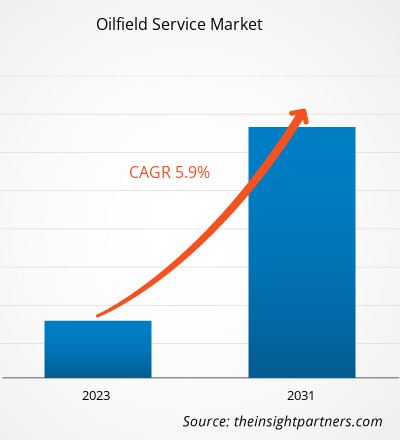

The oilfield Service Market size is projected to reach US$ 175.96 billion by 2031 from US$ 111.56 billion in 2023. The market is expected to register a CAGR of 5.9% during 2023–2031. Increasing oil & gas production, rising production of new oil rigs, and reconstruction of existing and old oil & gas rigs are likely to remain key trends in the market.

Oilfield Service Market Analysis

The oilfield service market is expected to experience considerable growth during the analyzed timeframe owing to the rising number of natural gas projects as well as the discovery of new oil fields, particularly in remote locations. Additionally, the depletion of existing oil & gas reserves in various countries has created a demand for cross-border pipelines for the supply of oil & gas-related products, which is boosting the growth of the oilfield service market. The increasing demand for cost-effective transportation methods for oil and gas is one of the major factors that is expected to boost the demand for oilfield services in the overseas oil & gas sector across the globe.

Oilfield Service Market Overview

With the mounting population and industrialization, the demand for energy is also rising at the global level. The rise in energy consumption also boosted the need for oil and gas in developing and developed economies. This has resulted in driving the demand for oilfield services across the globe. In addition, the Large population, high per capita income, and rapid industrialization are driving the offshore oil & gas pipes fittings and flanges market in the Asia Pacific. The region is the largest consumer of crude oil & gas. Further, highly industrialized countries in the Asia Pacific, including Japan, China, India, & South Korea, are reporting increasing overall energy consumption. These countries are increasing their focus on boosting domestic oil production through various enhanced oil recovery techniques, which is supporting the market growth in APAC to fulfill the growing demand for oil.

Market Research Highlights

- Global market for Oilfield Service was valued at US$ 111.56 Billion in 2023

- Annual market size is expected to reach US$ 175.96 Billion by 2031

- Total addressable market (TAM) during 2023-2031 is projected to reach approximately US$ 1,165.12 Billion

- Market is anticipated to register a CAGR of 5.9% during the forecast period

- The United States represents a key market, supported by The Raising Demand for Natural Gas and Crude Oil, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Efforts to Improve Oil Recovery Operations to Reduce Dependency on Oil & Gas Imports are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Schlumberger Limited, Weatherford International Plc, Baker Hughes Company, Halliburton Company, National Oilwell Varco, Inc., TechnipFMC, Plc, Superior Energy Services, Inc., China Oilfield Services Ltd., Asian Energy Services Limited, Transocean Ltd., while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Oilfield Service Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Oilfield Service Market Drivers and Opportunities

The Raising Demand for Natural Gas and Crude Oil to Favor Market

The demand for oil & natural gas is witnessing a constant increase across the world. The US and China have registered the most considerable growth. The robust increase in petrochemical demand in the US resulted in increased consumption. The surge in industrial production, along with the high demand for trucking services, is boosting the demand for petrochemicals, thereby fuelling the growth of the oilfield service market. Moreover, the growth in air traffic volumes worldwide, particularly in Asia's developing economies, is another significant factor resulting in increased oil consumption.

Efforts to Improve Oil Recovery Operations to Reduce Dependency on Oil & Gas Imports

The steam injection method has been exploited commercially over recent decades to improve recovery from conventional heavy oil reservoirs in their later stages of development. The injected steam increases the overall pressure of an offshore oil reservoir, which helps improve the mobility ratio of crude oil and allows it to flow efficiently. As a result, the enhanced oil recovery methods help revitalize extraction processes in existing offshore oil wells. Various countries are investing in efforts to rejuvenate their existing oil resources to boost domestic oil production and decrease their dependence on oil imports. Thus, the projected expansion of their oil & gas operations is anticipated to offer promising growth opportunities for the oilfield service market players in the coming years.

Oilfield Service Market Report Segmentation Analysis

Key segments that contributed to the derivation of the oilfield service market analysis are service type and application.

- Based on service type, the oilfield service market is divided into well completion, wireline, artificial lift, perforation, drilling and completion fluids, and others. The others segment held the largest oilfield service market share in 2023.

- By material type, the market is segmented into onshore and offshore. The onshore segment held the larger share in the oilfield service market in 2023.

Oilfield Service Market Share Analysis by Geography

The geographic scope of the oilfield service market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The oilfield services market in North America is sub-segmented into the US, Canada, and Mexico. The region dominates the global oilfield service market due to extensive oil and gas exploration and production projects and a surge in new activities in the US, the Gulf of Mexico, and Canada. There were 912,962 oil and gas wells in the US in that year. An increase in the number of horizontal wells in the US and a rise in oil and shale gas production per rig contribute to the oilfield services market growth in the country. The emergence of advanced intelligent oilfield services systems, such as high-end self-adaptive inflow control completion systems, would propel the market growth in North America in the coming years. High demand for onshore equipment due to significant prospects in the Permian Basin and North Dakota, especially in an increasingly large number of unconventional projects, would flourish the oilfield services market growth for the onshore segment.

Oilfield Service Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 111.56 Billion |

| Market Size by 2031 | US$ 175.96 Billion |

| Global CAGR (2023 - 2031) | 5.9% |

| Historical Data | 2021-2022 |

| Forecast period | 2023-2031 |

| Segments Covered |

By Service Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Oilfield Service Market Players Density: Understanding Its Impact on Business Dynamics

The Oilfield Service Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Oilfield Service Market News and Recent Developments

The oilfield service market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the oilfield service market are listed below:

- Baker Hughes announced the expansion of the Oilfield services and equipment business in Guyana. Baker Hughes is all set to develop a new supercentre facility in Guyana for oilfield services and equipment. (Source: Baker Hughes, Press Release, February 2022)

- Schlumberger Limited has announced the launch of the Periscope Edge multilayer mapping-while-drilling service. The service provides new measurements and an industry-leading inversion process combined with cloud solutions to deliver accurate geo steering in reservoirs while drilling. (Source: Schlumberger Limited, Press Release, August 2021)

Oilfield Service Market Report Coverage and Deliverables

The “Oilfield Service Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Oilfield service market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Oilfield service market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Oilfield service market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the oilfield service market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends