Point of Care Diagnostics Market Growth, Size, Share, Trends, Key Players Analysis, and Forecast till 2031

Coverage: By Product (Glucose Monitoring {Blood Glucose Meter, Lancet, and Strips}), Infectious Disease Testing {HIV Testing, Influenza Testing, Sexually Transmitted Diseases Testing, Hepatitis C Virus Testing, Tropical Diseases Testing, Respiratory Infection Testing, Hospital Acquired Infections, and Others}), Cardiometabolic Testing {Cardiac Troponin (cTn) Test, Myoglobin Test, and Others}), Pregnancy and Fertility Testing, Coagulation Testing, Tumor/Cancer Marker Testing, Cholesterol Testing, Urinalysis Testing, Hematology Testing, Thyroid Testing, and Others), Purchase Mode (OTC and Prescription), Sample (Blood, Urine, and Others), End User (Healthcare Facilities {Hospitals and Clinics, Diagnostic Centers, and Others}, Homecare, and Others) and Geography

- Status : Published

- Report Code : TIPRE00006394

- Category : Life Sciences

- No. of Pages : 483

- Available Report Formats :

- Last update date : May 09, 2025

2024 Market Size

US$ 37.93 Bn

Base year value

2031 Forecast

US$ 88.83 Bn

Projected by 2031

CAGR 2024-2031

13.0 %

Growth rate

Addressable Market

US$ 445.95 Bn

(2024-2031)

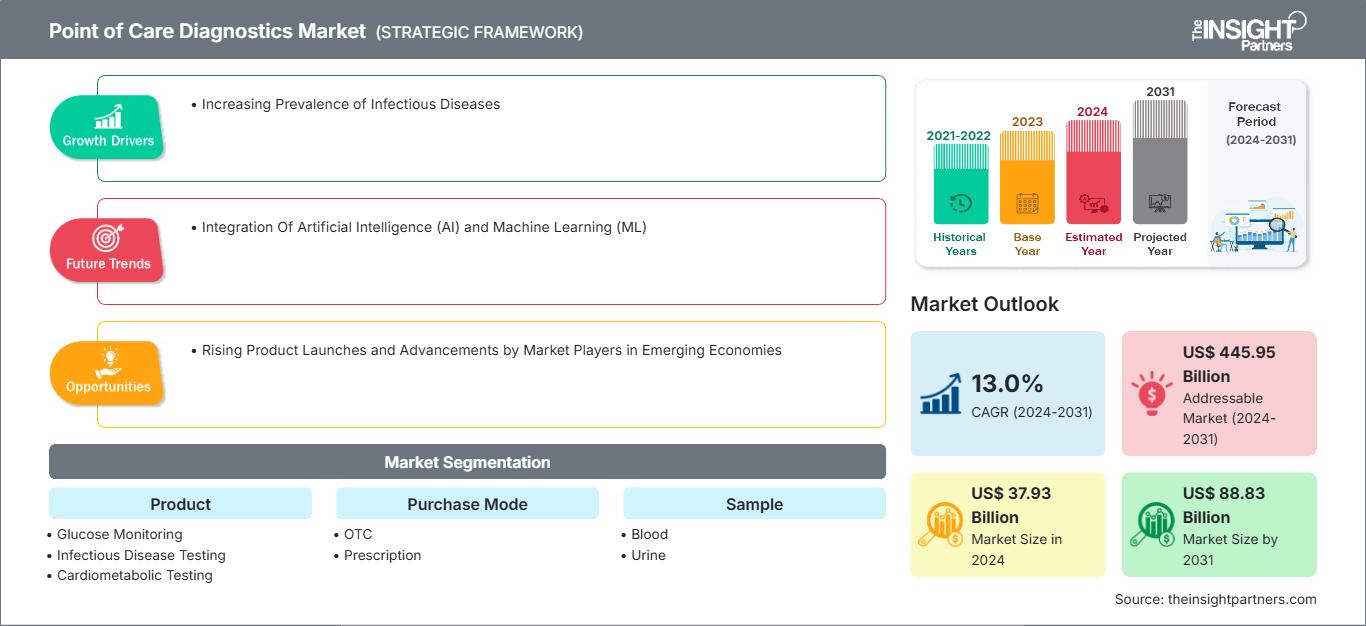

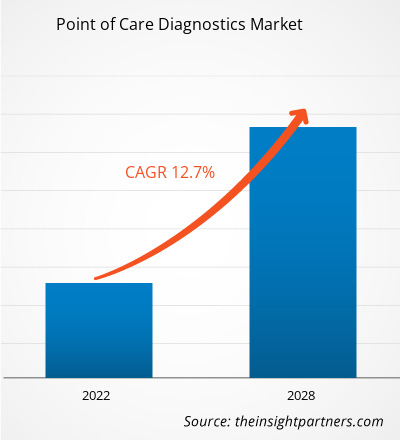

The Point of Care Diagnostics Market size is projected to reach US$ 88.83 billion by 2031 from US$ 37.93 billion in 2024. The market is estimated to register a CAGR of 13.0% during 2024–2031. The Integration Of Artificial Intelligence (AI) and Machine Learning (ML) is likely to bring new trends to the market in the coming years.

Point of Care Diagnostics Market Analysis

The Point of Care (POC) Diagnostics Market growth is driven by the increasing prevalence of infectious diseases, which has heightened the demand for rapid and accurate diagnostic solutions. Technological advancements and the integration of artificial intelligence and machine learning are enhancing the efficiency and accuracy of testing methods. Additionally, the growing need for self-diagnostic tools and the shift toward decentralized healthcare are expected to create future opportunities for market expansion. However, challenges such as the standardization between POC testing and centralized laboratory methods impact the broader adoption of these diagnostic solutions.

Point of Care Diagnostics Market Overview

The Point of Care (POC) Diagnostics Market is evolving, with the increasing demand for immediate and accurate diagnostic solutions. POC testing is conducted near the site of patient care, allowing for quick results that facilitate timely decision-making in clinical settings. This demand for this testing is influenced by the rising prevalence of infectious diseases and chronic conditions, which necessitate rapid diagnostic capabilities.

Innovations such as portable diagnostic devices and integrated digital health solutions enhance testing efficiency and accessibility. The shift toward decentralized healthcare models propels patients and healthcare providers to seek more convenient testing options that can be performed outside traditional laboratory settings.

Overall, the POC diagnostics market is poised for substantial growth, driven by the need for rapid testing solutions and the ongoing advancements in diagnostic technologies.

Market Assessment and Insights

- North America dominated the market with 40.3% share in 2024.

- Asia Pacific is poised to grow at a CAGR of 15.3% over the forecast period.

- United States market is projected to grow at a CAGR of 12.3% over the forecast period.

- By Product, the Glucose Monitoring segment accounted for the largest market share of 30% in 2024.

- By Glucose Monitoring, the Blood Glucose Meter segment is anticipated to witness the fastest growth, registering a CAGR of 17.2% over the forecast period

- By Infectious Disease Testing, the Respiratory Infection Testing segment accounted for the largest market share of 22% in 2024.

- By Cardio Metabolic Testing, the Cardiac Troponin (cTn) Test segment is anticipated to witness the fastest growth, registering a CAGR of 13.3% over the forecast period

- By Purchase Mode, the Prescription segment accounted for the largest market share of 63.7% in 2024.

- By Sample, the Blood segment is anticipated to witness the fastest growth, registering a CAGR of 13.4% over the forecast period

- By End User, the Healthcare Facilities segment accounted for the largest market share of 45.2% in 2024.

- By Healthcare Facilities, the Diagnostic Centers segment is anticipated to witness the fastest growth, registering a CAGR of 13.4% over the forecast period

- The report profiles key industry players such as Siemens AG, Abbott Laboratories, F. Hoffmann-La Roche Ltd, bioMerieux SA, Bio-Rad Laboratories Inc, QIAGEN NV, Nova Biomedical Corporation, Polymer Technology Systems, Inc. (PTS), Danaher Corp, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Point of Care Diagnostics Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Point of Care Diagnostics Market Drivers and Opportunities

Key Product Launches and Developments

The number of point-of-care tests has increased since its introduction. It is expected to grow with new product launches intended at delivering inexpensive care at the facilities at the closest possible distance from the patients' location. New products or technologies are being introduced to enhance the effectiveness of devices with incremental improvements in analytical performance. The growth of the point of care diagnostics market is driven by the introduction of new devices to perform molecular tests. New devices launched in the recent years include:

• In June 2023, Sysmex Corporation launched a point-of-care testing system in Europe to detect antimicrobial susceptibility. The system identifies the presence or absence of bacteria and evaluates the effectiveness of antimicrobials using patient urine samples suspected of having UTIs.

• In January 2023, Cipla Limited launched Cippoint, a point-of-care testing device. This device provides testing parameters such as cardiac markers, infectious diseases, diabetes, fertility, thyroid function, inflammation, metabolic markers, and coagulation markers. The device is CE IVD approved, which indicates that the device is approved by the European In-Vitro Diagnostic Device Directive, providing reliable testing solutions.

• In July 2021, QuantuMDx launched the Q-POC rapid PCR point-of-care diagnostic system, with its first test, a SARS-CoV-2 detection assay, now CE-IVD marked for use in Europe under the In Vitro Diagnostics Directive (98/79/EC).

Thus, increasing product launches by the market players propels the growth of the POC diagnostics market.

Rising Product Launches and Advancements by Market Players in Emerging Economies

For business expansion, market players are focusing on emerging nations, such as India, China, and Brazil, due to the large population suffering from HIV and other infectious diseases. According to the Press Information Bureau 2023 report, ~2.5 million people are living with HIV in India, with a prevalence rate of 0.2%, and 66,400 new HIV infections are reported in India annually. The increasing product launches indicate a potential environment for the adoption of advanced point-of-care diagnostic kits. In January 2022, Mylab launched the CoviSwift POC testing solution in India, which can be used in small labs, in-hospital labs, airports, and villages and allows gold-standard testing at high throughputs anywhere. The solution encompasses the CoviSwift assay and Compact-Q machines that process 16 samples within 40 minutes, which is approximately 4 times faster than traditional RT-PCR testing while maintaining high precision.

Advancements in nanotechnology and genomics are increasing the demand for diagnostics in the healthcare sector, encouraging the introduction of a greater number of point-of-care test systems and facilitating the shift toward personalized medicine. There are new opportunities in infectious disease testing, molecular oncology, and pharmacogenomics in emerging countries. The development of nanomaterials and nanotechnology has promoted the progress of POCT platforms, which are used in colorimetric, optical, electrochemical, magnetic, and catalytic approaches. The point of care testing platforms are used to detect nucleic acids, proteins, pesticides, viruses, bio-markers in disease diagnosis, and even heavy-metal species. Thus, rising product launches and advancements in emerging countries are anticipated to provide ample growth opportunities for the point-of-care diagnostics market during the forecast period.

Point of Care Diagnostics Market Report Segmentation Analysis

Key segments that contributed to the derivation of the Point of Care Diagnostics Market analysis are product, purchase mode, sample, end user, and geography.

- Based on product, the point of care diagnostics market is segmented into glucose monitoring, infectious disease testing, cardiometabolic testing, pregnancy and fertility testing, coagulation testing, tumor/cancer marker testing, cholesterol testing, urinalysis testing, hematology testing, thyroid testing, and others. The glucose monitoring segment held the largest share of the point of care diagnostics market in 2024, and it is expected to register a significant CAGR during 2024–2031.

- By purchase mode, the market is categorized into OTC and prescription. The prescription segment held a larger share of the point of care diagnostics market in 2024.

- As per sample, the point of care diagnostics market is segmented into blood, urine, and others. The blood segment held the largest share of the point of care diagnostics market in 2024, and it is expected to register a significant CAGR during 2024–2031.

- Per end user, the Point of Care Diagnostics Market is segmented into healthcare facilities, homecare, and others. The healthcare facilities segment held the largest share of the Point of Care Diagnostics Market in 2024, and it is expected to register a significant CAGR during 2024–2031.

Point of Care Diagnostics Market Share Analysis by Geography

The geographic scope of the Point of Care Diagnostics Market report is mainly divided into five major regions: North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. North America region is leading the market due to its robust healthcare infrastructure and early adoption of innovative diagnostic technologies. Canada ranks eighth among the largest medical device markets. According to the Government of Canada 2023 report, the prevalence of diabetes is rising at a significant pace. ~3.7 million population of the country (which is 9.4% of the total population) are living with diabetes or prediabetic conditions. The association has stated that every three minutes, a person is diagnosed with diabetes. Additionally, according to a report published by the government of Canada, the prevalence of HIV in Canada has grown by ~35.2% since 2022, and 2,434 new HIV cases reported in 2023. As per the Canadian Cancer Society, cancer was one of the primary reasons for deaths in the country, as the condition caused ~30% of deaths in 2023. Lung, breast, colorectal, and prostate cancer conditions predominated the diagnoses and deaths, with more than 46% share.

In July 2023, Fortis Life Sciences, LLC acquired Toronto-based International Point of Care, Inc. (IPOC). IPOC develops and manufactures components used in diagnostics, including lyophilized reagents, membranes, recombinant proteins, and controls. With this acquisition, Fortis can provide its customers with a customizable, end-to-end solution to advance their immunodiagnostic and molecular diagnostic products. IPOC’s recently expanded 36,000 sq. ft. facility is Fortis’ third GMP and ISO 13485-compliant manufacturing site in North America. Thus, the surging prevalence of cancer, the rising incidence of other diseases, and strategic collaborations fuel the growth of the point of care diagnostics market in the country.

Digital PCR and Real-Time PCR

Point of Care Diagnostics Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 37.93 Billion |

| Market Size by 2031 | US$ 88.83 Billion |

| Global CAGR (2024 - 2031) | 13.0% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Point of Care Diagnostics Market Players Density: Understanding Its Impact on Business Dynamics

The Point of Care Diagnostics Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Point of Care Diagnostics Market News and Recent Developments

The Point of Care Diagnostics Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the market are listed below:

- bioMérieux, a leader in the field of in vitro diagnostics, announced that it has entered into an agreement to acquire SpinChip Diagnostics ASA (“SpinChip”). This privately held Norwegian diagnostics company has developed a game-changing immunoassay diagnostics platform. The small benchtop analyzer is adapted to near patient testing as it can deliver a result from a whole blood sample within 10 minutes with the same high-sensitivity performance as the laboratory instruments. bioMérieux has held a minority stake in SpinChip since March 2024. (Source: bioMérieux, Company Website, January 2025)

- Roche announced the completion of the acquisition of LumiraDx’s Point of Care technology following the receipt of all required antitrust and regulatory clearances. Roche will now integrate the company’s multi-assay point of care platform and the related R&D, operational, and commercial sites into its global organization. (Source: Roche, Company Website, July 2024).

Point of Care Diagnostics Market Report Coverage and Deliverables

The "Point of Care Diagnostics Market Size and Forecast (2021–2031)" report provides a detailed analysis of the market covering below areas:

- Point of Care Diagnostics Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Point of Care Diagnostics Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Digital PCR and real-time PCR market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the digital PCR and real-time PCR market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends