Polyurethane Composites Market Demand, Share & Growth by 2034

Polyurethane Composites Market Size and Forecasts (2021 - 2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Fiber Type (Glass, Carbon); End-user Industry (Transportation, Building & Construction, Electrical & Electronics, Wind Energy); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040283

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 03, 2026

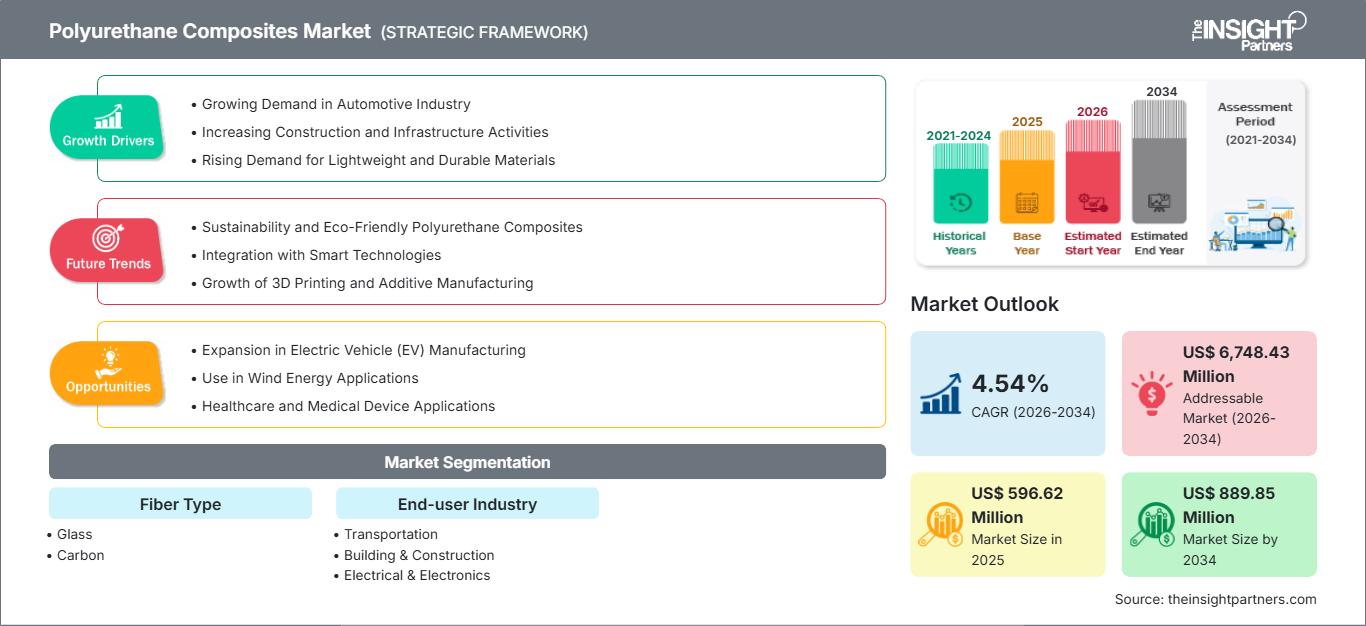

2025 Market Size

US$ 596.62 Mn

Base year value

2034 Forecast

US$ 889.85 Mn

Projected by 2034

CAGR 2026-2034

4.54 %

Growth rate

Addressable Market

US$ 6,748.43 Mn

(2026-2034)

Polyurethane Composites Market was valued at US$ 596.62 Million in 2025 and is projected to reach US$ 889.85 Million by 2034, expanding at a CAGR of 4.54% during 2026–2034. Growth is driven by increasing demand for lightweight, high-strength materials across transportation, construction, and energy applications. Rising substitution of conventional metals with advanced composites further supports steady market expansion, particularly in high-performance engineering environments requiring durability and corrosion resistance.

North America is expected to record a steady CAGR of 4.2–4.8% during the forecast period, supported by advanced manufacturing ecosystems and strong aerospace demand. Expansion in electric mobility and renewable energy infrastructure is further accelerating adoption. Additionally, stringent environmental regulations promoting lightweight and fuel-efficient materials are reinforcing regional uptake of Polyurethane Composites Market solutions across industrial applications.

Polyurethane Composites Market Assessment and Insights

- North America: Accounts for 32–36% share in 2025 and is projected to grow at 4.2–4.8% CAGR (2026–2034). Growth is supported by aerospace modernization and EV lightweighting demand across the United States and Canada.

- US: Holds 24–28% of global share in 2025, expanding at 4.3–4.9% CAGR, driven by defense manufacturing, automotive innovation, and wind energy deployment.

- Europe: Represents 28–32% share in 2025, growing at 4.0–4.6% CAGR, led by Germany, France, and the UK due to strong automotive and wind turbine manufacturing ecosystems.

- Asia Pacific: Accounts for 30–34% share in 2025, expanding at 4.8–5.4% CAGR, driven by China, Japan, South Korea, and India through industrial expansion and construction growth.

- Largest Segment – Transportation: Holds 38–42% share in 2025, growing at 4.3–4.8% CAGR, driven by lightweight vehicle structures and EV adoption.

- High Growth Segment – Wind Energy: Accounts for 12–16% share in 2025, expanding at 5.2–5.8% CAGR due to turbine blade composite integration.

- Key Companies Analyzed: BASF SE, Bayer AG, Covestro AG, Huntsman International LLC, ELANTAS GmbH, Henkel AG & Co. KGaA, Dow Inc., Toray Industries Inc., SEKISUI CHEMICAL CO., LTD., SGL Carbon SE

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Polyurethane composites have come a long way since being developed as specialty polymers to become key structural components embedded within high-tech engineering ecosystems. Initially used primarily for insulation and coating applications, developments in fiber technology and glass and carbon fiber embedding has broadened the applicability range of this product. Resin transfer molding and automated layup methods used in manufacturing today have brought greater reliability to the process making large-scale production in auto and aerospace industries possible.

The future development of this product is likely to follow the trend towards decarbonization and circular material development. Development of bio-polyurethane systems and sustainable composite materials is becoming more popular in Europe and Asia Pacific. Pressure from environmental agencies and sustainability policies of the automotive and construction industries will drive its growth. Offshore wind development and electrification of transportation systems are emerging as the new structural market drivers.

Polyurethane Composites Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 596.62 Million |

| Market Size by 2034 | US$ 889.85 Million |

| Global CAGR (2026 - 2034) | 4.54% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Polyurethane Composites Market Analysis

Polyurethane composites' demand is currently being shaped by the shift towards lightweight, strong, and durable materials around the world in the transportation, construction, renewable energy, aerospace, and manufacturing industries. With the focus on material efficiency, energy savings, and sustainability, polyurethane composites have become one of the solutions due to their great strength-to-weight ratio, impact, corrosion, and heat resistance as well as design capabilities. Car manufacturers are the biggest consumers of polyurethane composite materials since they use them in car bodies, interiors, seats, batteries' protection, and assembly parts in order to make cars lighter and save energy. The increased production of electric cars has driven the demand since lightweight materials help increase the driving distance and enhance performance of the car. Polyurethane composites are being extensively used by the construction industry in structural panels, bridge parts, insulation systems, pipelines, roofing systems, and anti-corrosive construction structures where longevity and maintenance-free properties are important characteristics of construction materials. The manufacturers of wind energy generators are also using this type of composite materials in turbine blades and structural parts. All such applications are continuously helping to increase the demand for these materials across the globe.

The polyurethane composite value chain involves several interrelated activities, starting from the providers of important raw materials used as the base for composite fabrication, such as polyols, isocyanates, catalysts, additives, fillers, pigments, and specialty chemicals. This step precedes the manufacturing of resins and compounds followed by the assembly of advanced composite manufacturers using fiber reinforcements like glass fibers, carbon fibers, aramid fibers, and hybrids. The fabrication of the composites uses the processes of resin transfer molding, compression molding, reaction injection molding, and automated composite manufacturing. Next, the process involves the integration of composites by the original equipment manufacturers, engineering companies, and industrial assemblers. The cooperation among chemical producers, fiber makers, machine suppliers, research organizations, and users is contributing towards further innovations in products, improved processing, and customization of composites according to challenging engineering requirements.

The dynamics in the supply of polyurethane composites are determined primarily by the availability and cost of petrochemical feedstocks utilized in the formation of polyurethanes, as well as the availability of reinforced fibers and specialized additives. Changes in the price of crude oil may affect production expenses and encourage manufacturers to adopt various sources. On the other hand, the current developments in the field of polymer chemistry make it possible for scientists to create polyurethane matrices that have enhanced mechanical and chemical properties and better processing performance. In addition, reinforcing the matrices with carbon and glass fibers provides increased stiffness, fatigue resistance, dimensional stability, and other advantages that widen the use of such materials in aerospace, defense, wind energy, railroad transport, and heavy machinery industries. The automation of the production process through the utilization of robotic laying-up systems, automated fiber placing technology, digital control systems, and sophisticated molds becomes increasingly common practice. These technological improvements are strengthening industrial scalability and supporting the efficient production of high-performance polyurethane composite components across global manufacturing facilities.

Competitive positioning within the polyurethane composites market is dominated by diversified chemical manufacturers, specialty material companies, and advanced composite technology providers that compete through innovation, product differentiation, and strategic partnerships. Companies such as BASF SE, Covestro AG, Dow Inc., Toray Industries Inc., SGL Carbon SE, Huntsman International LLC, Henkel AG & Co. KGaA, ELANTAS GmbH, and SEKISUI CHEMICAL CO., LTD. continue investing substantially in research and development to expand their portfolios of advanced polyurethane formulations and composite technologies. Strategic collaborations between raw material suppliers, fiber manufacturers, automotive OEMs, aerospace companies, and renewable energy equipment producers are accelerating product development cycles and facilitating the commercialization of next-generation lightweight materials. Investment activity is increasingly focused on sustainable material innovation, recyclable composite systems, bio-based polyurethane resins, and low-emission manufacturing technologies that align with evolving environmental regulations and corporate sustainability objectives. Companies are also expanding regional manufacturing facilities, strengthening supply networks, and increasing production capacity to meet rising demand across Asia Pacific, Europe, and North America. As industrial sectors continue emphasizing lightweight engineering, lifecycle performance, and environmental responsibility, the polyurethane composites market is expected to experience sustained growth driven by continuous technological innovation, strategic investments, and expanding global adoption.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Polyurethane Composites Market: Strategic Insights

Regional Insights

North America Polyurethane Composites Market

North America accounts for 32–36% share of the global Polyurethane Composites Market in 2025 and is projected to grow at a CAGR of 4.2–4.8% through 2034. Growth is supported by advanced aerospace manufacturing clusters in the United States and expanding EV production facilities in Canada and Mexico. Strong R&D investments in lightweight materials are further strengthening adoption across high-performance industries.

Industrial demand is driven by transportation electrification and renewable energy infrastructure development. Wind energy installations across the United States are increasing composite consumption, while construction modernization projects are integrating durable polyurethane-based materials. Strong presence of global chemical manufacturers and advanced material suppliers ensures stable supply chains and continuous innovation in composite engineering.

U.S. Polyurethane Composites Market

The United States represents 24–28% share of the global market within North America and is expected to expand at 4.3–4.9% CAGR. Growth is primarily driven by aerospace defense programs, electric vehicle manufacturing, and wind turbine blade production. Companies are increasingly integrating polyurethane composites into structural and semi-structural components to enhance durability and reduce lifecycle costs.

Industrial adoption is further supported by federal incentives for clean energy and advanced manufacturing. Automotive OEMs and aerospace contractors are leading application development, while material suppliers are expanding production capacity. Strong innovation ecosystems in composites engineering continue to reinforce U.S. dominance in high-performance material adoption.

Europe Polyurethane Composites Market

Europe holds 28–32% share of the Polyurethane Composites Market in 2025 and is projected to grow at 4.0–4.6% CAGR. The region benefits from strong automotive manufacturing hubs in Germany, France, Italy, Spain, and the United Kingdom. Sustainability regulations and circular economy initiatives are accelerating demand for recyclable composite materials.

Germany leads due to advanced automotive engineering and industrial automation. The United Kingdom focuses on aerospace composites and offshore wind projects, while France and Italy emphasize transport infrastructure modernization. Spain is expanding wind energy installations, strengthening regional composite consumption across renewable applications.

APAC Polyurethane Composites Market

Asia Pacific accounts for 30–34% share of the global Polyurethane Composites Market and is projected to grow at 4.8–5.4% CAGR. China dominates due to large-scale manufacturing, while Japan and South Korea focus on high-performance automotive and electronics applications. India is emerging as a key growth hub due to infrastructure expansion.

Australia contributes through mining and renewable energy investments. Strong government-backed industrial policies and rising foreign direct investments are accelerating composite adoption. Rapid urbanization and expanding construction activity across China and India are major structural drivers supporting regional dominance.

Middle East & Africa Polyurethane Composites Market

MEA holds 6–10% share in 2025 and is projected to grow at 3.8–4.3% CAGR. Saudi Arabia and the UAE lead demand through infrastructure diversification and renewable energy initiatives. South Africa contributes through industrial manufacturing and construction modernization.

Growth is supported by large-scale urban development projects and rising energy diversification strategies. Composite materials are increasingly used in construction and utility infrastructure due to durability advantages. The region’s long-term expansion is anchored in government-led economic transformation programs.

Segmentation Analysis

Fiber Type

Fiber Type segment is projected to grow at a CAGR of 4.3–4.9% during 2026–2034, driven by increasing integration of reinforcement materials in structural applications. Glass fiber dominates due to cost efficiency and balanced mechanical properties, while carbon fiber adoption is expanding in high-performance sectors. Demand is rising across automotive and aerospace industries where weight reduction and strength optimization are critical design priorities.

- Glass: Widely used due to cost-effectiveness and balanced strength-to-weight ratio, supporting large-scale adoption in construction panels and automotive components across industrial manufacturing environments.

- Carbon: Preferred for high-performance applications requiring superior tensile strength and lightweight characteristics, especially in aerospace, wind energy, and advanced automotive engineering systems.

End-user Industry

End-user Industry segment is projected to grow at a CAGR of 4.2–5.6% during 2026–2034, supported by diversification of polyurethane composite applications across multiple industrial verticals. Transportation remains the dominant consumer due to electrification trends and lightweighting requirements. Meanwhile, wind energy is emerging as a high-growth application area due to global renewable energy expansion and turbine modernization programs.

- Transportation: Strong demand from automotive and aerospace sectors focused on lightweight structures, fuel efficiency improvement, and emission reduction across global mobility systems.

- Building & Construction: Increasing use in durable panels, insulation systems, and corrosion-resistant structural materials supporting infrastructure modernization.

- Electrical & Electronics: Rising adoption in protective housings and insulating components for advanced electronic systems.

- Wind Energy: Expanding use in turbine blades and structural reinforcements driven by global renewable energy deployment initiatives.

Opportunity Snapshot

| Segment Name | Revenue Contribution | Trend Tag | Adoption Stage |

| Transportation | High | EV Lightweighting | Mature |

| Building & Construction | Medium | Smart Infrastructure | Scaling |

| Electrical & Electronics | Medium | Device Insulation | Scaling |

| Wind Energy | High | Turbine Expansion | Emerging |

Polyurethane Composites Market Growth Drivers and Impact Analysis

Rising Demand for Lightweight High-Strength Materials

There has been a rise in awareness of fuel efficiency and emissions reduction across the globe, leading to increased use of lightweight materials in the automotive, aerospace, and manufacturing industries. There is no better solution than polyurethane composites, which provide a perfect blend of strength, flexibility, and weight savings for future engineering designs. The automakers have started using composite materials instead of metal materials to comply with the tough regulations. The same trend has been observed in the aerospace industry, where composite materials have been incorporated into the structure.

Expansion of Renewable Energy Infrastructure

Rising global investments in renewable energy, particularly wind energy, have increased demand for high-end composite materials. Polyurethane composites are extensively used in turbine blades because of their strength and fatigue resistance features. The various government-led clean energy projects in Europe, China, and the U.S. have accelerated deployment capacity. Also, offshore wind projects have increased the need for higher material intensity. This fundamental shift in energy production has generated sustained demand for high-end composite materials.

Technological Advancements in Composite Manufacturing

Progress in resin chemistry, fiber reinforcement techniques, and manufacturing automation is revolutionizing the efficiency of composite production. Resin transfer molding and additive manufacturing have emerged as innovative techniques that allow precision in the fabrication of components with minimal wastage of raw materials. Significant investments in research and development are being made by companies for the improvement of thermal and mechanical properties of polyurethane systems. These developments are lowering production costs and broadening the range of applications across various industries, including aerospace, automotive, and construction sectors.

Polyurethane Composites Market Future Trends

Integration of Sustainable and Bio-Based Polyurethane Systems

Sustainability is prompting manufacturers to create bio-based polyurethane composites using renewable feedstocks. The manufacturing industry is becoming increasingly concerned with lowering its carbon footprint by adopting circularity in material design and composite recycling. Pressure from environmental regulatory bodies is prompting manufacturers to adopt manufacturing processes that emit fewer greenhouse gases. Early adopters of sustainable composite technology include the automotive and construction industries. Bio-polyols and green chemistry are continuously evolving and poised to transform manufacturers' product lineups.

Digitalization and Smart Manufacturing of Composite Materials

The adoption of digital technologies in composite manufacturing is emerging as a transformative trend. Smart factories equipped with IoT-enabled monitoring systems and AI-driven quality control are improving production efficiency and reducing defects. Predictive analytics is optimizing material usage and lifecycle performance. Manufacturers are integrating digital twin technologies to simulate composite behavior under real-world conditions. This digital transformation is enabling faster product development cycles and enhancing customization capabilities, particularly in aerospace and automotive sectors where precision engineering is critical for performance optimization.

Polyurethane Composites Market Opportunities

Rising Demand for Lightweight High-Strength Materials

There has been a rise in awareness of fuel efficiency and emissions reduction across the globe, leading to increased use of lightweight materials in the automotive, aerospace, and manufacturing industries. There is no better solution than polyurethane composites, which provide a perfect blend of strength, flexibility, and weight savings for future engineering designs. The automakers have started using composite materials instead of metal materials to comply with the tough regulations. The same trend has been observed in the aerospace industry, where composite materials have been incorporated into the structure.

Expansion of Renewable Energy Infrastructure

Rising global investments in renewable energy, particularly wind energy, have increased demand for high-end composite materials. Polyurethane composites are extensively used in turbine blades because of their strength and fatigue resistance features. The various government-led clean energy projects in Europe, China, and the U.S. have accelerated deployment capacity. Also, offshore wind projects have increased the need for higher material intensity. This fundamental shift in energy production has generated sustained demand for high-end composite materials.

Technological Advancements in Composite Manufacturing

Progress in resin chemistry, fiber reinforcement techniques, and manufacturing automation is revolutionizing the efficiency of composite production. Resin transfer molding and additive manufacturing have emerged as innovative techniques that allow precision in the fabrication of components with minimal wastage of raw materials. Significant investments in research and development are being made by companies for the improvement of thermal and mechanical properties of polyurethane systems. These developments are lowering production costs and broadening the range of applications across various industries, including aerospace, automotive, and construction sectors.

Recent Developments

- March 2026: Huntsman Corporation officially celebrated the grand opening of its expanded Performance Products manufacturing facility in Petfurdo, Hungary. This investment significantly increases global capacity for its JEFFCAT® amine catalysts. These specialized catalysts are crucial components used directly to initiate and control the reaction injection molding processes required to produce polyurethane composites, insulation, and lightweight automotive components.

- December 2025: Covestro AG formally announced the global scale-up and optimization support for its Direct Coating technology. This is an integrated, two-shot manufacturing method that merges plastic injection molding with polyurethane reaction injection molding (RIM) in a single system. It targets premium automotive structural components, enabling manufacturers to fuse lightweight plastic composite structures with protective polyurethane surface coatings simultaneously, cutting down process energy and production lines.

- September 2025: Dow Inc. officially announced a breakthrough partnership with recycling network operator Gruppo Fiori. The companies co-developed an industrial process capable of extracting polyurethane waste streams directly from end-of-life vehicle scrap metal processing matrices—negating the need for manual vehicle disassembly. The captured material exhibits high enough chemical purity to undergo depolymerization (chemical recycling), allowing the industry to re-feed scrap back into high-performance polyurethane mobility applications.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends