Ready-to-Eat Food Market Growth, Trends & Demand by 2034

Coverage: By Product Type (Breakfast Cereals, Instant Soups & Noodles, Ready Meals, Snacks, Baked Goods & Confectioneries, and Others) and Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, and Others)

- Status : Upcoming

- Report Code : TIPRE00029384

- Category : Food and Beverages

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 09, 2026

2025 Market Size

US$ 1,271.77 Bn

Base year value

2034 Forecast

US$ 2,112.42 Bn

Projected by 2034

CAGR 2026-2034

5.8 %

Growth rate

Addressable Market

US$ 15,334.55 Bn

(2026-2034)

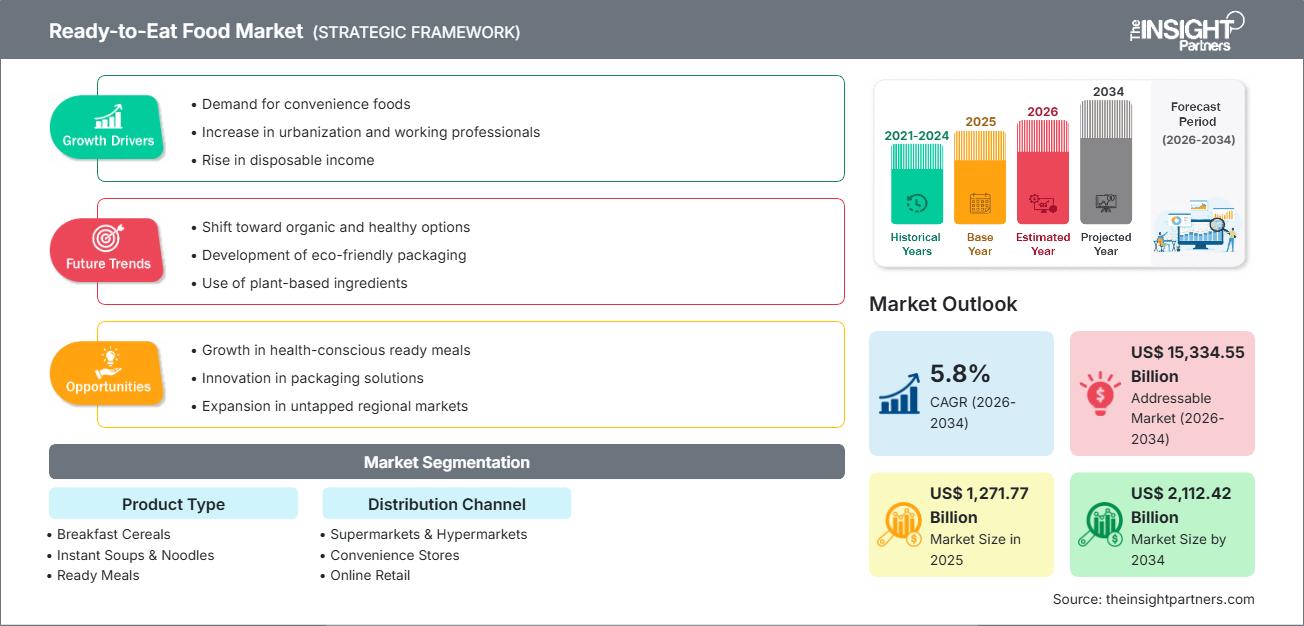

The global ready-to-eat food market size is projected to reach US$ 2,112.42 billion by 2034 from US$ 1,271.77 billion in 2025. The market is anticipated to register a CAGR of 5.8% during the forecast period 2026–2034.

Key market dynamics include a permanent structural shift toward high-speed convenience, the intensification of urbanization, and the growing time-poverty of dual-income households. Additionally, the market is expected to benefit from the rise of snackification, where traditional meals are replaced by small and frequent bites, alongside the integration of AI-driven demand forecasting and automated fulfillment centers that boost inventory turnover and reduce food waste.

Ready-to-Eat Food Market Analysis

The ready-to-eat food market analysis indicates a transition of ready-to-eat meals from low-quality compromises to mission-critical, nutrition-dense performance fuels for modern professionals. Recent data shows that the market is bifurcating into mass-market affordability and a rapidly expanding premium segment that emphasizes clean-label, gourmet-quality ingredients. Strategic opportunities are emerging in specialized nutrition, specifically the GLP-1 consumer segment, where leading brands are launching high-protein, fiber-rich portions for individuals on weight-loss medications. The analysis also identifies that market success is increasingly tied to technical logistics, as maintaining product integrity through last-mile delivery remains significantly more expensive than traditional dry goods. Competitive differentiation now stands out through smart packaging features, such as QR codes for farm-to-fork traceability and the use of biodegradable films, which appeal to the environmental and transparency demands of Gen Z and Millennial cohorts.

Ready-to-Eat Food Market Overview

Ready-to-eat food has evolved into a diverse convenience portfolio that caters to multi-track consumption patterns across all daily meal occasions. The market encompasses a wide variety of global and ethnic cuisines, with a notable surge in demand for authentic international flavors such as Thai, Indian, and Italian in shelf-stable and frozen formats. Both large-scale industrial players and quick-commerce platforms compete in this space, leveraging advanced freezing technologies and retort packaging to preserve flavor without excessive preservatives. Growing demand for portion-controlled and single-serve options among the rising number of single-person households in urban centers has solidified the role of ready-to-eat food as a staple dietary solution. Europe currently holds the largest value share due to established chilled-food infrastructure, while the Asia-Pacific region, particularly India and China, is emerging as the fastest-growing corridor driven by rapidly scaling food processing and high e-commerce penetration.

The US market represents a highly mature landscape where convenience intersects with a sophisticated fitness and wellness culture. Growth is primarily propelled by health-focused millennials and the widespread availability of functional snacks. Competition among brands continues to fuel diverse flavor profiles and the integration of superfoods into portable meal solutions.

Market Assessment and Insights

- Global market for Ready-to-Eat Food was valued at US$ 1,271.77 Billion in 2025

- Annual market size is expected to reach US$ 2,112.42 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 15,334.55 Billion

- Market is anticipated to register a CAGR of 5.8% during the forecast period

- The United States represents a key market, supported by Demand for convenience foods, Increase in urbanization and working professionals, Rise in disposable income, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Growth in health-conscious ready meals, Innovation in packaging solutions, Expansion in untapped regional markets are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Nestl? SA, Conagra Brands Inc., The Kraft Heinz Company, General Mills Inc., CAMPBELL SOUP COMPANY, MTR Foods Pvt Ltd., Hormel Foods Corporation, Tyson Foods, Inc., JBS S.A., The Kellogg Company, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Ready-to-Eat Food Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Ready-to-Eat Food Market Drivers and Opportunities

Market Drivers:

- Intensifying Time-Poverty and Urbanization: As global workweeks average over 40 hours, urban professionals—particularly those aged 25–44—are consuming an average of 4.2 ready-to-eat meals weekly to save preparation time.

- Technological Integration of AI and Robotics: The use of machine learning for demand forecasting and robotic assembly systems is enhancing production consistency and reducing operational waste, allowing for broader market access.

- Rise of Snackification and On-the-Go Consumption: A fundamental pivot in consumer behavior is replacing structured three-course meals with frequent, portable snacks and baked goods, which now account for a dominant volume of the market.

Market Opportunities:

- Targeting the GLP-1 and Health-Conscious Demographic: Developing nutrient-dense, portion-controlled meals tailored for the millions of consumers on weight-loss medications or seeking specific functional benefits like gut health.

- Expansion of Private-Label and Premium Offerings: Retailers are increasingly using their own brands to offer gourmet-quality ready meals at competitive prices, gaining significant traction in supermarkets and convenience stores.

- Sustainability and Packaging Innovation: Transitioning to rigid paperboard and biodegradable films presents a major opportunity to capture the growing segment of eco-conscious consumers who prioritize plastic-free solutions.

Ready-to-Eat Food Market Report Segmentation Analysis

The Ready-to-Eat Food Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Breakfast Cereals: A steady segment evolving with multi-grain and protein-enriched variants to cater to health-conscious morning routines.

- Instant Soups & Noodles: The fastest-growing volume driver, particularly in Asia-Pacific, fueled by innovation in premium flavors and the popularity of Asian cuisines.

- Ready Meals: The largest value segment, including chilled, frozen, and canned complete meals that serve as primary home-meal replacements.

- Snacks: A core industry workhorse driven by the shift toward frequent, small-portion consumption throughout the day.

- Baked Goods & Confectioneries: Dominates market volume due to high shelf stability, ease of portability, and consistent consumer demand for grab-and-go options.

By Distribution Channel:

- Supermarkets & Hypermarkets: The primary distribution segment, holding a dominant share (approx. 43.6%) by offering a wide variety of products and competitive pricing.

- Convenience Stores: Essential for impulse purchasing and urban accessibility, serving as a key channel for individual portions and immediate-use products.

- Online Retail: The fastest-rising gateway for sales, benefiting from the integration of e-commerce with sophisticated cold-chain logistics for direct-to-door delivery.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Ready-to-Eat Food Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1,271.77 Billion |

| Market Size by 2034 | US$ 2,112.42 Billion |

| Global CAGR (2026 - 2034) | 5.8% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Ready-to-Eat Food Market Players Density: Understanding Its Impact on Business Dynamics

The Ready-to-Eat Food Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Ready-to-Eat Food Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium food producers and convenience meal manufacturers to expand.

The ready-to-eat food market is undergoing a significant transformation, moving from basic canned staples to global high-value functional nutrition. Growth is driven by the rising prevalence of time-poverty, a surge in demand for international cuisines, and the expansion of the luxury chilled-meal. Below is a summary of market share and trends by region:

North America

- Market Share: A mature yet dominant segment driven by a deep-rooted convenience culture and a robust frozen food ecosystem.

- Key Drivers:

- Rising consumer preference for high-protein, clean-label profiles in frozen and chilled formats

- Mainstreaming of gourmet ready meals in high-end grocery chains.

- Increased consumption of functional snacks and organic frozen options among health-conscious professionals.

- Trends: Scaling of direct-to-consumer meal subscription models and the successful adoption of specialty certifications to appeal to health-focused demographics.

Europe

- Market Share: Holds the largest share globally, anchored by highly developed chilled-food chains and a strong preference for fresh-like ready meals.

- Key Drivers:

- High domestic consumption of chilled ready meals, bakery products, and traditional breakfast cereals

- Established processing infrastructure and strict regulatory frameworks for food safety and labeling

- Robust retail presence of private-label frozen foods offering high-quality, affordable alternatives.

- Trends: A strategic shift toward 100% compostable packaging and organic-certified ready meals to meet the demands of eco-conscious European consumers.

Asia-Pacific

- Market Share: The fastest-growing region, with a massive consumer base seeking convenient and westernized luxury food options.

- Key Drivers:

- Rapid urbanization and rising disposable incomes are leading to a preference for instant noodles and ready-to-heat traditional dishes

- Government-supported initiatives focused on scaling the food processing and cold-chain sectors.

- High e-commerce penetration is making niche global flavors accessible to the growing middle class.

- Trends: Heavy reliance on quick-commerce platforms for 10-minute delivery of café-style meals and a surge in demand for premium, nutrient-dense infant and toddler ready-to-eat nutrition.

South and Central America

- Market Share: Emerging market with a growing demand for artisanal and regional-style convenience foods.

- Key Drivers:

- Increasing awareness of the nutritional value of minimally processed ready meals.

- Modernization of retail chains in urban centers to provide better access to frozen entrees.

- Rising interest in international cuisines among middle-to-high income segments.

- Trends: Growth of boutique local brands and the introduction of regional-style ready meals that differentiate from global mass-market offerings.

Middle East and Africa

- Market Share: Developing market transitioning toward formalized commercial production and modern retail.

- Key Drivers:

- High demand for shelf-stable and Halal-certified ready meals in arid climates.

- Strategic investments in smart manufacturing to improve local food security and reduce import reliance.

- Traditional presence of ready-to-eat staples in regional cuisines adapting to modern packaging.

- Trends: Implementation of advanced refrigeration and retort packaging technologies to formalize the informal food market, coupled with a focus on high-nutrient ready meals.

High Market Density and Competition

Competition is intensifying as manufacturers shift from selling just food to selling time. Major players are increasingly managing convenience portfolios across multiple channels to capture diverse consumer touchpoints. This environment pushes vendors to differentiate through:

- Gourmet-Quality and Diet-Specific Options: Offering vegan, gluten-free, and high-protein ready meals that rival restaurant quality.

- AI-Driven Personalization: Using consumer data to create small-batch production of meals tailored to regional tastes and personalized nutrition demands.

- Supply Chain Transparency: Implementing blockchain and QR codes to ensure food safety and ethical sourcing, building consumer trust in processed categories.

Opportunities and Strategic Moves

- Partner with Quick-Commerce and Delivery Platforms: Tap into the surging demand for instant, café-style ready-to-eat meals and 10-minute delivery services in metropolitan hubs.

- Incorporate Sustainable Packaging and Traceability: Utilize biodegradable materials and QR codes for farm-to-fork transparency to appeal to environmentally conscious millennials and Gen Z consumers seeking ethical food choices.

Major Companies operating in the Ready-to-Eat Food Market are:

- Nestlé SA

- Conagra Brands Inc.

- The Kraft Heinz Company

- General Mills Inc.

- CAMPBELL SOUP COMPANY

- MTR Foods Pvt Ltd.

- Hormel Foods Corporation

- Tyson Foods, Inc.

- JBS S.A.

- The Kellogg Company

Disclaimer: The companies listed above are not ranked in any particular order.

Ready-to-Eat Food Market News and Recent Developments

- In July 2024, General Mills Foodservice announced the latest addition to its portfolio of individually wrapped products for school feeding programs with new Ready-to-Eat Muffins Trix™ and Cinnamon Toast Crunch ™ muffins. Convenient and mess-free for breakfast or snack time, the muffins offer 2 oz. equivalent grain and simply require foodservice staff to thaw and serve.

- In April 2024, VELVEETA announced its first-ever Ready-to-Eat Queso offering. Allowing fans to indulge in their favorite cheese on any occasion, VELVEETA Queso debuts in three delicious flavors – Queso Con Salsa, Queso Blanco, and Jalapeno – and marks the brand’s first venture into the ready-to-eat queso category.

Ready-to-Eat Food Market Report Coverage and Deliverables

The Ready-to-Eat Food Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Ready-to-Eat Food Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Ready-to-Eat Food Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Ready-to-Eat Food Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Ready-to-Eat Food Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends