Ultra-Low Alpha Metals Market Size, Share & Demand by 2034

Coverage: By Type (ULA Tin, ULA Tin Alloys, ULA Lead Alloys, ULA Lead-Free Alloys, and Others) and Application (Electronics, Automotive, Medical, Telecommunication, and Others)

- Status : Data Released

- Report Code : TIPRE00020178

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : February 24, 2026

2025 Market Size

US$ 4.48 Bn

Base year value

2034 Forecast

US$ 8.59 Bn

Projected by 2034

CAGR 2026-2034

7.5 %

Growth rate

Addressable Market

US$ 58.90 Bn

(2026-2034)

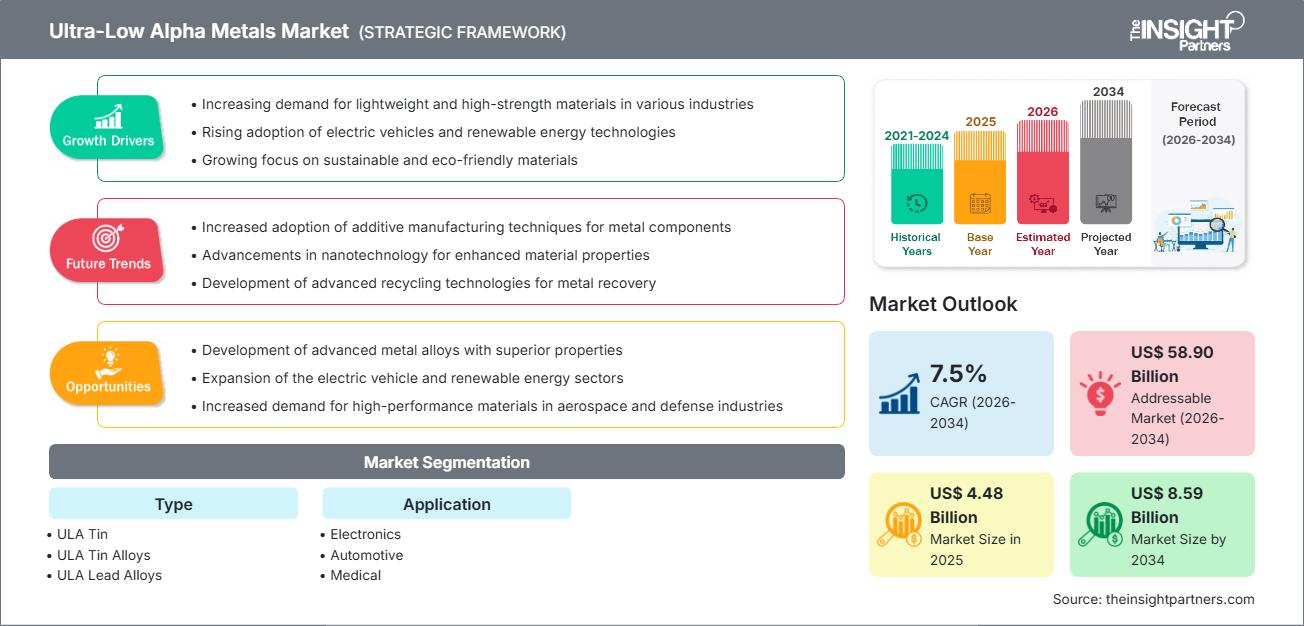

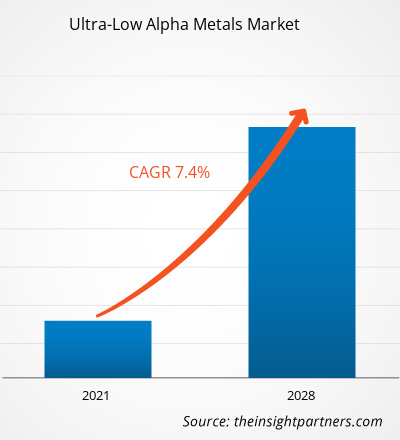

The global ultra-low alpha metals market size is projected to reach US$ 8.59 billion by 2034 from US$ 4.48 billion in 2025. The market is anticipated to register a CAGR of 7.5% during the forecast period 2026–2034. Key market dynamics include a heightening global focus on semiconductor reliability, rising consumer awareness regarding "soft errors" in high-density memory chips, and a significant shift toward ultra-high purity materials in advanced packaging. Additionally, the market is expected to benefit from the growing popularity of 5G infrastructure, expansion in automotive electrification across emerging economies, and the increasing inclusion of ultra-low alpha (ULA) metals in high-value segments like aerospace avionics and medical imaging.

Ultra-Low Alpha Metals Market Analysis

The ultra-low alpha metals market analysis shows that lead producers will increase their focus on value-added function materials as device longevity and data integrity are priorities for manufacturers. The procurement pattern indicates the market is transitioning from the traditional lead-based industries for defense applications to the rapidly-growing Asia Pacific lead-free export market. Specialty medical devices for pediatrics and geriatrics represent a growing strategic opportunity due to being radiation-quiet when compared with standard industrial-grade ultra-low alpha metals. The report also projects that the expansion of the ultra-low alpha metal market will require tight cleanroom integrity for handling of the raw materials and the best vacuum-distillation system to achieve their highest purity. Competitive differentiation now stands out depending on branding that tells a story and highlights certified emission levels, ethical sourcing of raw materials, and being able to track the purification batch. This approach helps premium suppliers charge higher prices in a market with sophisticated technical requirements.

Ultra-Low Alpha Metals Market Overview

Ultra-low alpha metals are shifting from a regional, specialized trade to a global high-tech commodity. While historically focused on basic soldering for industrial electronics, ultra-low alpha metals are expanding into value-added products like specialized alloys, plating anodes, and high-purity foils. Both major metallurgical refineries and niche high-purity specialists are part of this market, making use of the natural low-radioactivity profiles of specific ore bodies. More reliability-conscious manufacturers in North America and Asia-Pacific are looking for alternatives to standard metals, which has helped ULA metals gain popularity as a "gentle material" choice for sensitive circuits. Asia-Pacific is still the main producer and consumer, but North America has become a leader in innovation and mission-critical exports, especially through high-end B2B contracts for the aerospace sector.

For instance, in North America, the market is primarily propelled by the high-tech demands of the aerospace and defense industries, alongside a robust domestic semiconductor ecosystem. Strategic reshoring initiatives and federal funding for critical mineral supply chains have prioritized localized purification. High-purity metals are essential here for ensuring the reliability of advanced avionics, satellite communications, and high-performance computing systems.

Market Assessment and Insights

- Global market for Ultra-Low Alpha Metals was valued at US$ 4.48 Billion in 2025

- Annual market size is expected to reach US$ 8.59 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 58.90 Billion

- Market is anticipated to register a CAGR of 7.5% during the forecast period

- The United States represents a key market, supported by Increasing demand for lightweight and high-strength materials in various industries, Rising adoption of electric vehicles and renewable energy technologies, Growing focus on sustainable and eco-friendly materials, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Development of advanced metal alloys with superior properties, Expansion of the electric vehicle and renewable energy sectors, Increased demand for high-performance materials in aerospace and defense industries are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Mitsubishi Materials Corporation, Teck Resources Limited, Advanced Manufacturing Services (AMS) Ltd, Pure Technologies, Honeywell International Inc., DUKSAN Hi-Metal Co., Ltd, MacDermid Alpha Electronics Solutions, while analyzing competitive strategies and innovation developments

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Ultra-Low Alpha Metals Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Ultra-Low Alpha Metals Market Drivers and Opportunities

Market Drivers:

- Superior Reliability and Data Integrity: ULA metals minimize alpha particle emissions that cause soft errors in semiconductors. This technical benefit, along with growing interest in "zero-defect" manufacturing, is driving its popularity.

- Premiumization of the Semiconductor Packaging Category: The expansion of flip-chip and 3D packaging has sustained high demand for ULA inputs. As consumers trade up to faster and smaller devices, certified ULA materials continue to see stable volume gains.

- Rapid Expansion of Digital and AI Infrastructure: The rollout of 5G and AI data centers has removed traditional geographic barriers for high-purity metals. This is particularly evident in the rapid adoption of ULA tin-silver alloys in regions like Asia-Pacific and North America.

Market Opportunities:

- Expansion into Automotive and EV Power Electronics: Beyond traditional computing, ULA metals offer significant opportunities in high-reliability sensors and battery management systems for the automotive sector.

- Growth in Emerging APAC Tech Corridors: Forming strategic partnerships between Western material science firms and Asian foundries may facilitate access to high-margin market segments in Taiwan and South Korea, where demand for premium, high-purity materials is increasing.

- Diversification into Specialty Certifications: There is a growing opportunity for producers to target specific demographics through certifications such as RoHS compliance and "Zero-Emission" purity levels, as seen in recent successful retail expansions in the high-reliability market.

Ultra-Low Alpha Metals Market Report Segmentation Analysis

The Ultra-Low Alpha Metals Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Type:

- ULA Tin: The dominant volume driver, particularly within the traditional electronics soldering and plating sectors, due to established supply chains and cost-effectiveness.

- ULA Tin Alloys: A fast-growing niche that will grow much faster than those for ULA Tins due to the growing preference for advanced packaging methods (like flip-chip) among high-end semiconductor producers.

- ULA Lead Alloys: continue to have applications in specialty radiation shielding (due to its mass properties) and certain aerospace markets (due to its unique density and defect-preventing properties).

- ULA Lead-Free Alloys: The fastest-rising category, driven by environmental regulations and the global shift toward sustainable electronics manufacturing.

By Application:

- Electronics

- Automotive

- Medical

- Telecommunication

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Ultra-Low Alpha Metals Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 4.48 Billion |

| Market Size by 2034 | US$ 8.59 Billion |

| Global CAGR (2026 - 2034) | 7.5% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Ultra-Low Alpha Metals Market Players Density: Understanding Its Impact on Business Dynamics

The Ultra-Low Alpha Metals Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Ultra-Low Alpha Metals Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for industrial formalization and advanced tech manufacturing.

The ultra-low alpha metals market is undergoing a significant transformation, moving from a niche aerospace staple to a global high-value industrial food for the digital economy. Growth is driven by the rising sensitivity of chips, a surge in "high-reliability" electronic demand, and the expansion of the luxury automotive electronics sector. Below is a summary of market share and trends by region:

North America

- Market Share: A robust segment driven by aerospace, defense, and the growth of high-performance computing (HPC).

- Key Drivers:

- Rising manufacturer preference for certified "low-error" materials in military avionics.

- Mainstreaming of ULA metals in high-end medical device manufacturing.

- Increased focus on reshoring semiconductor supply chains within the US.

- Trends: Scaling of local purification facilities and the successful adoption of specialty certifications (e.g., RoHS, Conflict-Free) to appeal to ethical-tech demographics.

Europe

- Market Share: Holds a significant share globally, anchored by deep-seated automotive and industrial automation ecosystems in Germany and France.

- Key Drivers:

- High demand for ULA materials in safety-critical automotive electronics.

- Established processing infrastructure and strict RoHS regulatory frameworks.

- Robust government support for advanced materials research and "Green Electronics."

- Trends: A strategic shift toward prioritizing ULA lead-free alloys over traditional tin-lead versions. There is also an increasing focus on recycled ULA sources to meet eco-conscious European mandates.

Asia-Pacific

- Market Share: The largest and fastest-growing region, with China and Taiwan acting as the primary manufacturing engines for the global semiconductor industry.

- Key Drivers:

- Massive consumer electronics base seeking premium, reliable hardware.

- Government-supported initiatives focused on high-value "Smart Manufacturing."

- Rapid urbanization leading to a preference for high-bandwidth 5G infrastructure.

- Trends: Heavy reliance on B2B contracts for high-end ULA solder bumps used in the mobile and gaming industries.

South and Central America

- Market Share: Emerging market with a growing electronics assembly sector in countries like Chile and Brazil.

- Key Drivers:

- Increasing awareness of the impact of material purity on device lifespan.

- Modernization of local electronics manufacturing to supply regional automotive hubs.

- Rising interest in high-reliability industrial sensors.

- Trends: Growth of "clean-label" material suppliers and the introduction of ULA-grade plating for the regional telecommunications market.

Middle East and Africa

- Market Share: Developing market transitioning toward formalized high-tech industrial production.

- Key Drivers:

- Strategic investments in "Smart Cities" requiring reliable electronic infrastructure.

- High demand for durable, radiation-stable products in harsh desert climates.

- Government initiatives to improve local tech self-sufficiency.

- Trends: Implementation of modern smelting and refrigeration technologies for high-purity metal storage, coupled with a focus on ULA metals for the regional energy segment.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Honeywell International Inc., Mitsubishi Materials Corporation, and Indium Corporation. Regional experts and niche players like DUKSAN Hi-Metal Co., Ltd. (South Korea) and Pure Technologies, alongside North American innovators such as Alpha Assembly Solutions, also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Positioning ULA metals as a superior technical alternative to standard grades by emphasizing their role in preventing "Soft Error Rates" (SER) in mission-critical chips.

- Companies offer more than just raw metals; they provide ULA solder spheres, preforms, and high-purity chemicals for plating.

- Producers manage the entire chain, from high-purity ore selection to vacuum-distillation processing. This ensures quality and meets "Conflict-Free" clean-label standards.

- New testing technologies, like high-sensitivity alpha counting, help certify products for high-end nutraceutical and medical sensing applications.

Opportunities and Strategic Moves

- Partner with high-end semiconductor foundries and OSAT (Outsourced Semiconductor Assembly and Test) providers to tap into the surging demand for AI and 5G hardware.

- Incorporate sustainable smelting practices and circular economy certifications to appeal to environmentally conscious corporations and government procurement agencies.

Major Companies operating in the Ultra-Low Alpha Metals Market are:

- Mitsubishi Materials Corporation

- Teck Resources Limited

- Advanced Manufacturing Services (AMS) Ltd

- Pure Technologies

- Honeywell International Inc.

- DUKSAN Hi-Metal Co., Ltd

- MacDermid Alpha Electronics Solutions

Disclaimer: The companies listed above are not ranked in any particular order.

Ultra-Low Alpha Metals Market News and Recent Developments

- In July 2025, The Kurt J. Lesker Company announced the launch of the Pro Line Roll-to-Roll (R2R) Module, a transformative enhancement to the industry-leading Pro Line PVD 200 Thin Film Deposition System. This new, cost-effective, drop-in module brings true roll-to-roll coating capability to the PVD 200 platform, empowering researchers and product developers to bridge the gap between laboratory-scale experimentation and scalable pilot production of flexible electronic devices.

- In June 2025, Mitsubishi Corporation announced to invest and enter into a Business Partnership with DEScycle Ltd., a UK Company Developing Innovative Metal Recycling Technology.

Ultra-Low Alpha Metals Market Report Coverage and Deliverables

The "Ultra-Low Alpha Metals Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Ultra-Low Alpha Metals Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Ultra-Low Alpha Metals Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Ultra-Low Alpha Metals Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Ultra-Low Alpha Metals Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends