Alzheimers Disease Patients Market Trends, Size & Forecast by 2034

Coverage: By Onset Type (Late onset disease, Early Onset Disease); Drug Class (Cholinergic, Memantine, Combined Drug, AChE inhibitors, Immunoglobulins); Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Online Sales) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00019571

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 14, 2026

2025 Market Size

US$ 11.66 Bn

Base year value

2034 Forecast

US$ 17.07 Bn

Projected by 2034

CAGR 2026-2034

4.32 %

Growth rate

Addressable Market

US$ 130.43 Bn

(2026-2034)

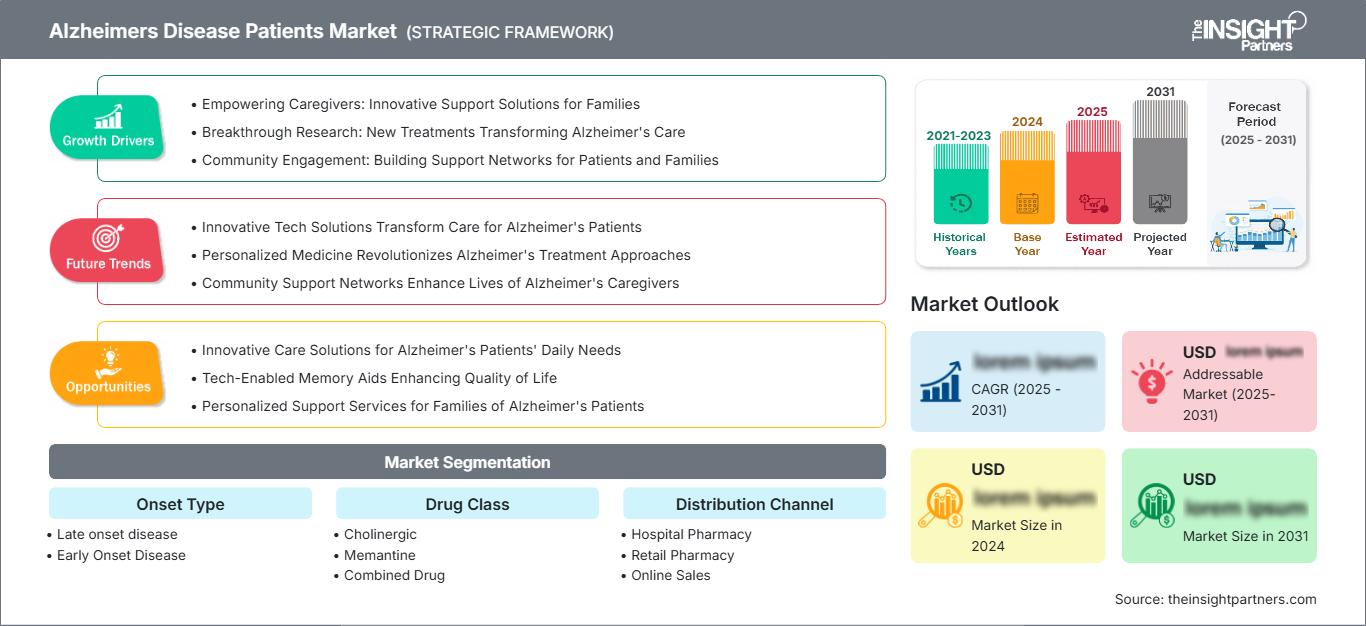

The Alzheimers Disease Patients market size is projected to grow from US$ 11.66 Billion in 2025 to US$ 17.07 Billion by 2034, recording a CAGR of 4.32% during 2026–2034. The market is an indication of the increased diagnosed prevalence rate, increasing number of patients eligible for treatment in the initial stages of the disease, and continued usage of therapies by those who need cognitive, behavioral, and functional assistance through pharmacy access channels.

North America is currently the most commercially advanced geographic region, where the Alzheimers Disease Patients market is propelled by diagnostic pathways of specialists, better affordability of treatments, and adoption of treatment protocols that modify the disease. The region is anticipated to experience a growth rate of CAGR 3.8-4.2% during the period 2026-2034.

Alzheimers Disease Patients Market Assessment and Insights

- North America accounted for 40–43% share in 2025 and is projected to grow at a CAGR between 2026–2034 of 3.8–4.2%, led by diagnosis infrastructure, specialist neurology access, and structured reimbursement for advanced therapies.

- US represented 84–87% of North America in 2025 and is expected to grow at a CAGR between 2026–2034 of 3.7–4.1%, supported by treatment registries and clinician uptake.

- Europe held 28–31% share in 2025 and is forecast to grow at a CAGR between 2026–2034 of 3.6–4.0%, with Germany, the UK, France, Italy, and Spain leading adoption.

- Asia Pacific captured 20–23% share in 2025 and is projected to grow at a CAGR between 2026–2034 of 5.0–5.6%, driven by Japan, China, South Korea, India, and Australia.

- Largest Segment Late onset disease held 82–86% Alzheimers Disease Patients market share in 2025 and is expected to grow at a CAGR between 2026–2034 of 4.0–4.4% due to aging-linked prevalence.

- High Growth Segment Online Sales held 6–9% market share in 2025 and is projected to grow at a CAGR between 2026–2034 of 6.8–7.4% as chronic refills digitize.

- Key companies analyzed in detail: AbbVie Inc., Eisai Co., Ltd., Novartis AG, Daiichi Sankyo Company, Limited, Merz Pharmaceuticals GmbH, Pfizer Inc., Johnson & Johnson Services, Inc., H. Lundbeck A/S, Biogen Inc., AstraZeneca PLC, F. Hoffmann-La Roche Ltd.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Clinical management strategies have evolved from merely symptomatic assistance to earlier diagnoses, validation by biomarkers, and increased length of coordinated care between neurologists, geriatricians, diagnostic laboratories, pharmacies, and caregivers. Alzheimers Disease Patients’ Care pathways are increasingly involving acetylcholinesterase inhibitors, NMDA Receptor Modulation, behavior management techniques, and disease modifying antibodies where applicable. Dynamics of production will also evolve given the need for logistics associated with infusion/injection of biologicals, MRI, pharmacovigilance, and different processes in pharmacies compared to previous oral drugs.

For the forecast period, new geographies are set to assume significance in terms of diagnosis as aging populations, campaigns against dementia, and increasing coverage of health insurance increase diagnosis rates. Favorable regulatory trends will occur more prominently in jurisdictions where health systems connect earlier diagnosis with covered care pathways for patients, including the US, Japan, China, and some European nations. Investments will focus on biomarker testing, specialty pharmacy coordination, and access channels that relieve caregiver burden without compromising patient safety.

Alzheimers Disease Patients Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 11.66 Billion |

| Market Size by 2034 | US$ 17.07 Billion |

| Global CAGR (2026 - 2034) | 4.32% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Alzheimers Disease Patients Market Analysis

Rising diagnosed prevalence, longer survival with neurodegenerative disease, and wider cognitive screening are shaping Alzheimers Disease Patients market forecast. According to WHO, there are tens of millions suffering from dementia in the world, out of which majority suffers from Alzheimer's Disease. Thus, the patient base is quite large and needs to be managed in stages. Increased demand will come about through early reporting by families, referrals from general practice and the knowledge that mild cognitive impairment may be clinically treatable.

This ecosystem consists of diagnostics, neurologists, geriatric specialists, pharmaceutical companies, hospital pharmacies, retail pharmacies, on-line refills, caregiver and payers. The supply situation is divided into generics and oral formulations on one side and biologics needing cold chain logistics and specialized administration on the other.

The Alzheimers Disease Patients market report shows competition shifting from conventional symptomatic treatment toward differentiated evidence, dosing convenience, and safety monitoring. For the initial anti-amyloid commercialization process, Eisai Co., Ltd. and Biogen Inc. will be key players, while F. Hoffmann-La Roche Ltd. will be driving the process of integrated diagnostic and research drugs. The organizations which will still be important include AbbVie Inc., Novartis AG, Pfizer Inc., H. Lundbeck A/S, and Merz Pharmaceuticals GmbH.

The investments will be focusing increasingly on patient journey management rather than just the product placement. These companies are forming relationships in biomarker tests, real-world databases, infusions, and educating the clinicians. Some organizations to watch in relation to neuroscience competencies and partnering potential, including in central nervous system products, are Daiichi Sankyo Company, Limited, Johnson & Johnson Services, Inc., and AstraZeneca PLC.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Alzheimers Disease Patients Market: Strategic Insights

Regional Insights

North America Alzheimers Disease Patients

North America held 40–43% share in 2025 and is projected to grow at a CAGR of 3.8–4.2% during 2026–2034. The Alzheimers Disease Patients market share is supported by high diagnosis intensity, broad Medicare-linked treatment access, neurologist concentration, and faster uptake of biomarker-based eligibility assessment. Memory clinics and large hospital systems are central to therapy initiation.

The growth will be restricted by infusion capabilities, needs for MRI evaluations, need for verification of benefits, and lack of specialists, but these restrictions are slowly being overcome. Involvement of pharmacists is increasing from dispensing to adherence, caregiver training, synchronization of refills, and safety communications. With the advancement of the subcutaneous or less burdensome treatments, the regional use of the therapy will increase into community-based neurological networks.

U.S. Alzheimers Disease Patients Market

The US represented 84–87% of North America in 2025 and is expected to grow at a CAGR of 3.7–4.1% during 2026–2034. The country benefits from early availability of disease-modifying therapies, large clinical trial infrastructure, and established Alzheimer’s advocacy organizations that encourage screening, diagnosis, and treatment readiness.

The companies’ presence is mainly centered on neurology centers, integrated delivery networks, and specialty pharmacy systems. The key players in this regard are Eisai Co., Ltd., Biogen Inc., F. Hoffmann-La Roche Ltd., AbbVie Inc., and Pfizer Inc. Application trends are associated with early identification of mild cognitive impairment, amyloid confirmation, and safety monitoring.

Europe Alzheimers Disease Patients Market

The region was responsible for 28–31% of the market share in 2025 and is estimated to expand at a CAGR of 3.6–4.0% between 2026 and 2034. The dominant country in the region is Germany owing to hospital neurology capability, specialist reimbursement model, and quicker adoption of newly approved innovative therapy. The UK is undergoing HTA, memory services reform, and earlier referral from primary care.

Germany and the UK together make most of the regional adoption signals but there is heavy reimbursement focus. France, Italy, and Spain are relevant because of their large aging population, health system procurement strength, and dementia plans development. They are dependent upon diagnostic capability, availability of MRI scans, and risk management strategy for biologic treatments which require genotyping and imaging screening.

APAC Alzheimers Disease Patients Market

APAC captured 20-23% market share in 2025 and is expected to register a growth rate of CAGR 5.0-5.6% between 2026-2034. APAC will be dominated by the Japanese market due to aging demographics and advancements in neurology treatments and availability of early-stage Alzheimer's treatment options.

China will increase the uptake of diagnostics and hospital neurology treatment facilities, whereas South Korea and Australia will provide quality specialized treatment facilities. In India, the treatment uptake will be relatively low but strategic due to increased awareness and presence of online pharmacies and hospitals.

Middle East & Africa Alzheimers Disease Patients Market

Middle East & Africa is expected to grow at a CAGR of 3.3–3.7% during 2026–2034. Saudi Arabia leads regional development through hospital infrastructure investment, specialist-care modernization, and national health transformation priorities that include chronic disease and aging-related services.

The UAE supports premium private care and medical tourism-linked neurology services, while South Africa anchors access in Sub-Saharan Africa through urban hospital networks. Rest of MEA remains constrained by underdiagnosis, affordability, and limited specialist availability. Energy-linked public investment in Gulf healthcare infrastructure supports incremental diagnostic and pharmacy market development.

Segmentation Analysis

Onset Type

The Onset Type segment in the Alzheimers Disease Patients Market is projected to grow at a CAGR of 4.1–4.5% during 2026–2034. The Alzheimers Disease Patients market scope across onset categories is shaped by age at symptom emergence, diagnostic urgency, genetic evaluation needs, and treatment planning. Late onset cases dominate volume, while early onset disease requires faster specialist referral, caregiver support, employment-related counseling, and closer family risk assessment.

- Late onset disease remains the dominant patient category because prevalence rises sharply after age 65, creating sustained demand for cognitive therapies, caregiver support, hospital pharmacy access, and retail refills.

- Early Onset Disease is smaller but strategically important because diagnosis is often delayed, disease burden affects working-age adults, and specialist-led treatment decisions may involve genetic counseling and family planning.

Drug Class

The Drug Class segment in the Alzheimers Disease Patients Market is expected to grow at a CAGR of 4.2–4.6% during 2026–2034. Treatment demand is split between established symptomatic therapies and newer protocols addressing disease biology in selected early-stage patients. Prescribers balance cognitive benefit, safety, tolerability, monitoring needs, comorbidity burden, affordability, and caregiver capacity when choosing oral, combination, or biologic-based approaches.

- Cholinergic therapies remain widely used for symptom management because clinicians understand their tolerability profile, dosing patterns, and role in maintaining daily function across mild-to-moderate disease stages.

- Memantine is important in moderate-to-severe disease management, particularly where NMDA receptor modulation is used to support cognition, behavior, and caregiver-reported functional stability.

- Combined Drug approaches address patients needing multi-mechanism support, especially when clinicians combine symptomatic agents to manage cognition, behavior, and functional decline over longer care periods.

- AChE inhibitors continue to represent a foundational prescribing class because donepezil, rivastigmine, and galantamine are embedded in guidelines, retail pharmacy flows, and generic access systems.

- Immunoglobulins occupy a niche position, with strategic relevance tied to immunology research, investigational mechanisms, and selected clinical contexts rather than broad routine use.

Distribution Channel

The Distribution Channel segment in the Alzheimers Disease Patients Market is forecast to grow at a CAGR of 4.4–4.8% during 2026–2034. Distribution is becoming more complex as the market combines chronic oral refills, hospital-administered therapies, specialty pharmacy coordination, caregiver-led medicine management, and digital adherence tools. Channel selection depends on product format, monitoring obligations, payer authorization, patient mobility, and proximity to specialist care.

- Hospital Pharmacy is critical for infusion therapies, treatment initiation, safety monitoring, and specialist coordination, particularly where biomarker confirmation and imaging surveillance are required before or during therapy.

- Retail Pharmacy remains the primary access point for chronic oral medicines, repeat refills, caregiver counseling, medication reconciliation, and adherence support in community-based dementia care.

- Online Sales is gaining relevance as caregivers seek convenient refill management, home delivery, reminders, and price transparency for long-term symptomatic therapy use.

Opportunity Snapshot

| Distribution Channel | Revenue Contribution | Trend Tag | Adoption Stage |

| Hospital Pharmacy | High | Infusion Access | Mature |

| Retail Pharmacy | High | Chronic Refills | Mature |

| Online Sales | Medium | Digital Refill | Scaling |

Alzheimers Disease Patients Market Growth Drivers and Impact Analysis

Earlier Diagnosis Through Biomarker-Enabled Care Pathways

Biomarker-enabled diagnosis is changing the addressable treated population by moving patients from uncertain cognitive complaints into clinically defined treatment pathways. Blood-based screening, cerebrospinal fluid testing, amyloid PET, and genotype-informed risk assessment improve patient stratification, especially in mild cognitive impairment and mild dementia stages. The commercial impact is significant because confirmed pathology supports therapy initiation, payer review, clinical trial recruitment, and caregiver decision-making. Hospitals that previously managed dementia mainly through clinical observation are now investing in diagnostic protocols that support advanced treatment eligibility. This driver also improves segmentation precision, allowing companies to align education, monitoring tools, and pharmacy services with patients most likely to receive long-term pharmacologic management.

Aging Populations and Rising Caregiver Burden

Population aging remains the most durable demand driver because Alzheimer’s prevalence rises steeply in older age groups. Longer life expectancy in North America, Europe, Japan, China, and parts of the Gulf is increasing the number of patients requiring diagnosis, treatment, behavioral support, and medicine management. Caregiver burden further strengthens healthcare engagement because families often seek therapies that preserve independence, reduce supervision intensity, or slow functional deterioration. Even where drug access is limited, demand for symptomatic therapies remains resilient due to established prescribing patterns. The market impact extends beyond pharmaceuticals into pharmacy counseling, adherence tools, home delivery, and care coordination services that help families manage complex, long-duration disease progression.

Expansion of Specialty Pharmacy and Monitoring Infrastructure

Advanced Alzheimer’s therapies require operational infrastructure that was less central to older oral treatment models. Specialty pharmacies, infusion centers, MRI networks, and hospital-based neurology teams are becoming access enablers because treatment safety depends on scheduling, monitoring, adverse event communication, and payer documentation. This infrastructure increases eligible patient throughput and reduces treatment abandonment. It also supports higher-value service models for manufacturers and healthcare providers. As maintenance dosing, subcutaneous formats, and digital adherence systems improve, therapy delivery may become less dependent on major academic centers. The market impact is broader geographic reach, stronger persistence, and better integration of pharmacy channels into dementia care pathways.

Alzheimers Disease Patients Market Future Trends

Shift Toward Lower-Burden Disease-Modifying Treatment Formats

Alzheimers Disease Patients market trends will increasingly favor treatment formats that reduce infusion center dependence and caregiver time commitment. Subcutaneous delivery, longer dosing intervals, and maintenance regimens can change how eligible patients remain on therapy after initiation. The trend is strategically important because current biologic adoption is constrained not only by cost and safety monitoring, but also by travel, infusion scheduling, and capacity limitations. Lower-burden formats may expand access beyond major academic centers into community neurology practices. They could also improve persistence by making treatment routines more compatible with frail patients, employed caregivers, and health systems facing specialist shortages.

Integration of Diagnostics, Registries, and Real-World Evidence

The next phase of market development will rely heavily on integrated evidence systems that connect diagnosis, therapy use, safety outcomes, and long-term functional measures. Registries and real-world data platforms will help payers assess value, clinicians refine eligibility, and companies demonstrate effectiveness outside controlled trials. This trend is especially relevant for biologic therapies, where safety monitoring and patient selection influence outcomes. Diagnostic companies and drug developers are expected to collaborate more closely as blood-based biomarkers become embedded in screening. Over time, evidence integration may support more precise reimbursement, earlier intervention, and stronger confidence among physicians managing complex elderly patients.

Alzheimers Disease Patients Market Opportunities

Building Scalable Early-Stage Patient Identification Networks

A major investment opportunity lies in connecting primary care, memory clinics, diagnostic labs, and pharmacies into scalable early-stage identification networks. Many patients enter care after functional decline becomes visible, reducing the potential benefit of therapies designed for earlier intervention. Companies can create value by supporting clinician education, cognitive screening workflows, referral protocols, and biomarker access. Alzheimers Disease Patients market Forecasts indicate that the largest commercial gains will come from converting undiagnosed or late-diagnosed individuals into monitored, treatable populations. Stakeholders that improve detection efficiency can influence therapy initiation, adherence, and caregiver engagement while strengthening market access arguments with measurable patient pathway data.

Expanding Caregiver-Centric Pharmacy Services

Caregiver-centric pharmacy services offer a practical opportunity because dementia treatment depends heavily on non-patient decision-makers. Retail and online pharmacies can differentiate through multi-month refill planning, medication synchronization, adherence reminders, interaction checks, home delivery, and counselling for behavioral or cognitive therapies. These services are especially valuable in late onset disease, where polypharmacy and mobility challenges complicate treatment persistence. Manufacturers and distributors can partner with pharmacy networks to improve refill continuity and safety communication without replacing physician oversight. The opportunity is strongest in markets with high retail pharmacy density, digital payment adoption, and growing caregiver willingness to use remote ordering tools.

Recent Developments

- July 2026: F. Hoffmann-La Roche Ltd. announced that it would present 18 Alzheimer’s disease portfolio presentations at AAIC 2026, including trontinemab Phase Ib/IIa extension data, Phase III PrevenTRON study design, neuroimmune target updates, and Elecsys pTau217 blood-test evidence for diagnosis across care settings.

- August 2025: Eisai Co., Ltd. and Biogen announced US FDA approval of LEQEMBI IQLIK, a once-weekly lecanemab subcutaneous autoinjector for maintenance dosing after 18 months of intravenous therapy in early Alzheimer’s disease, with US launch planned for October 2025.

- July 2025: Biogen Inc. announced Alzheimer’s disease presentations for AAIC 2025, including 48-month Clarity AD open-label extension findings for lecanemab, real-world treatment insights, subcutaneous maintenance dosing evidence, and baseline characteristics from the CELIA Phase 2 study of BIIB080 targeting tau.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends