Smart Card Material Market Size, Trends & Growth by 2034

Smart Card Material Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Material [Polyvinyl Chloride (PVC), Polycarbonate (PC), Acrylonitrile Butadiene Styrene (ABS), Polyethylene Terephthalate-Glycol (PETG), and Others]; Type (Contact Cards, Contactless Cards, and Multi-Component Cards); and Application (BFSI, Government, Telecommunication, Retail, Healthcare, Hospitality, and Others)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00026860

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

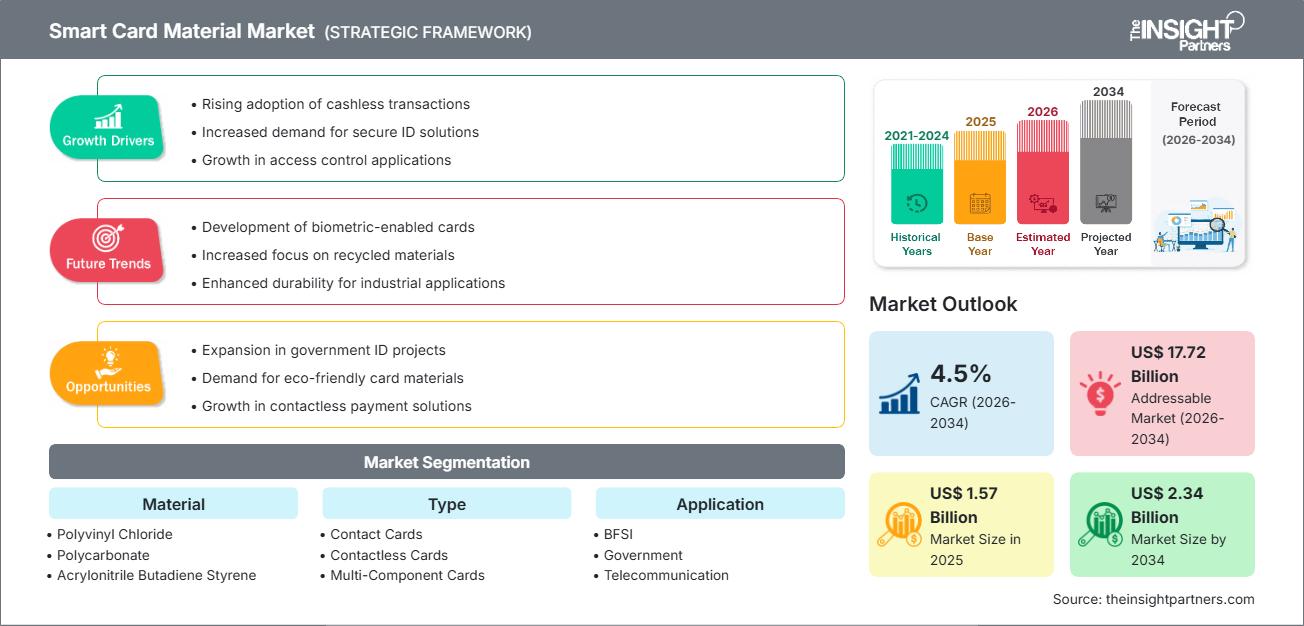

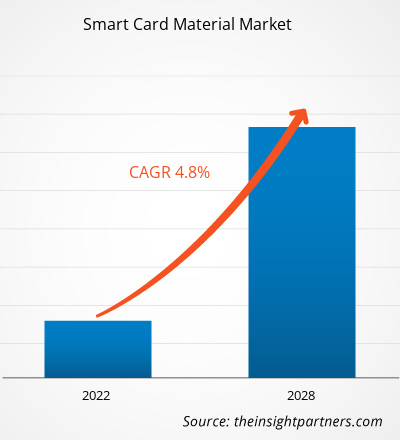

The global smart card material market size is projected to reach US$ 2.34 billion by 2034 from US$ 1.57 billion in 2025. The market is anticipated to register a CAGR of 4.5% during the forecast period 2026–2034. Key market dynamics include a heightening global focus on secure and durable digital identification, rising consumer awareness regarding the environmental impact of traditional plastic cards, and a significant shift toward high-performance polymers like polycarbonate. Additionally, the market is expected to benefit from the growing popularity of contactless payment systems, expansion in organized retail and banking channels across emerging economies, and the increasing inclusion of smart cards in high-value government sectors like national IDs and e-passports.

Smart Card Material Market Analysis

The smart card material market analysis shows a shift toward high-value functional substrates as issuers prioritize durability and tamper-resistance. Procurement trends indicate the market is splitting into traditional PVC-led commercial sectors and high-growth Polycarbonate-exclusive security markets in Europe and Asia. Strategic opportunities are emerging in specialty sustainable materials, where recycled PVC (rPVC) and bio-based alternatives offer a clear competitive advantage compared to virgin plastics. The analysis also notes that market expansion depends on lamination integrity for multi-component cards and the chemical resistance of materials used in diverse environmental conditions. Competitive differentiation now stands out depending on branding that tells a story and highlights eco-friendly sourcing, ethical manufacturing, and material traceability. This approach helps manufacturers charge higher prices in a market with many specialized suppliers.

Smart Card Material Market Overview

Smart card materials have evolved from simple plastic housing to advanced multi-layered substrates that protect sophisticated microchips. Both global chemical companies and specialized card manufacturers compete in this market, using polymer sources such as PVC, PC, ABS, and PETG. Growing demand for secure, long-lasting credentials among security-conscious governments and financial institutions in North America and Europe has increased the popularity of polycarbonate as a premium solution. Asia-Pacific leads in revenue due to its established manufacturing hub and rapid digital adoption, while emerging economies are advancing in material innovation and local card personalization. The US market is the most developed for payment card materials, driven by the broad availability of functional, high-end banking products. Competition among material providers is fueling greater variety and the inclusion of sustainable additives like ocean-bound plastics and wood-based composites.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONSmart Card Material Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Smart Card Material Market Drivers and Opportunities

Market Drivers:

- Superior Durability and Security Profile: Materials like Polycarbonate allow for laser engraving and high-impact resistance, making cards nearly impossible to forge or damage. This technical benefit, along with growing interest in high-security documents, is driving its popularity.

- Premiumization of the Financial Card Category: The expansion of metal-plastic hybrid cards and haptic card finishes has sustained high demand for specialty inputs. As consumers trade up to premium banking experiences, high-quality material finishes continue to see stable gains.

- Rapid Expansion of Digital and Contactless Infrastructure: Global shifts toward tap-and-pay have increased the demand for substrates that can house delicate antennas. This is particularly evident in the rapid adoption of dual-interface cards in regions like Asia-Pacific and Latin America.

Market Opportunities:

- Expansion into Sustainable and Bio-based Cards: Beyond traditional plastics, there are significant opportunities in developing cards made from recycled ocean plastic and biodegradable polymers for eco-conscious brands.

- Growth in Emerging APAC ID Corridors: Forming strategic partnerships between material suppliers and regional government contractors may facilitate access to high-margin market segments in China and India, where demand for national ID systems is increasing.

- Diversification into Biometric Multi-Component Cards: There is a growing opportunity for producers to target the high-security payment segment through materials optimized for embedding fingerprint sensors and flexible electronics.

Smart Card Material Market Report Segmentation Analysis

The Smart Card Material Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Material:

- Polyvinyl Chloride (PVC): The dominant volume driver, particularly within the telecommunications and retail sectors, due to established supply chains and cost efficiencies.

- Polycarbonate (PC): A fast-growing segment that aligns with global security trends. It is increasingly preferred for government-issued IDs that require high durability and laser-engraving features.

- Acrylonitrile Butadiene Styrene (ABS): Widely used in mobile telecommunications for SIM card manufacturing due to its high thermal and impact resistance.

- Polyethylene Terephthalate-Glycol (PETG): An eco-friendly alternative gaining traction in markets focusing on recyclability and high mechanical strength.

By Type:

- Contact Cards: Remains a primary segment for traditional banking and legacy SIM cards, benefiting from established infrastructure.

- Contactless Cards: The fastest-rising segment, especially in the BFSI and transit sectors, enabling quick and secure transactions.

- Multi-Component Cards: Offers a select but growing range of premium cards integrated with biometric sensors and high-end security elements.

By Application:

- BFSI: The primary driver for payment card materials, following the transition to dual-interface and EMV standards.

- Government: A high-value segment focusing on durable materials for long-term use in e-passports and national identity programs.

- Telecommunication: Dominated by SIM card production, currently evolving toward high-performance materials for 5G and M2M applications.

- Retail, Healthcare, and Hospitality: These sectors utilize smart cards for loyalty, patient identification, and secure access, requiring diverse material properties.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Smart Card Material Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1.57 Billion |

| Market Size by 2034 | US$ 2.34 Billion |

| Global CAGR (2026 - 2034) | 4.5% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Material

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Smart Card Material Market Players Density: Understanding Its Impact on Business Dynamics

The Smart Card Material Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Smart Card Material Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium material suppliers and secure document manufacturers to expand.

The smart card material market is undergoing a significant transformation, moving from basic commodity plastics to high-value functional substrates. Growth is driven by the rising prevalence of contactless payments, a surge in national ID programs, and the expansion of the luxury heavy-weight banking card sector. Below is a summary of market share and trends by region:

North America

- Market Share: A large segment driven by the transition to contactless EMV and the growth of premium metal-plastic hybrid cards.

- Key Drivers:

- Widespread adoption of contactless payment systems, with over 90% of consumers using tap-and-pay technologies.

- Strict federal requirements for high-security credentialing and identification for government employees.

- Strong presence of major regional card manufacturers prioritizing dual-interface lamination.

- Trends: Scaling of eco-friendly card initiatives and the successful adoption of recycled materials (rPVC) to appeal to environmentally conscious millennials.

Europe

- Market Share: Holds a significant share globally, anchored by a deep-seated focus on high-security standards and sustainability regulations.

- Key Drivers:

- Regulatory mandates for cross-border healthcare cards and digital-first administrative student IDs.

- Leading the global shift toward Polycarbonate (PC) for national e-passports and identity cards to ensure 10+ year durability.

- Aggressive environmental regulations (such as those from the European Commission) are pushing the phase-out of traditional virgin PVC.

- Trends: A strategic shift toward Green Cards and the prioritization of Polycarbonate for government documents to prevent identity fraud.

Asia-Pacific

- Market Share: The largest and fastest-growing region, with China acting as the primary manufacturing engine for the entire continent.

- Key Drivers:

- Enormous national ID infrastructures, such as India's Aadhaar and China's national ID programs, are creating high-volume demand for durable substrates.

- The world’s largest telecommunications subscriber base necessitates constant 4G/5G SIM card material replenishment.

- Rapid urbanization in Southeast Asia is driving the adoption of Namma Chennai-style smart transit and multi-utility prepaid cards.

- Trends: Heavy reliance on high-volume production of SIM and transit cards, coupled with a rising focus on locally sourced eco-friendly polymers.

South and Central America

- Market Share: Emerging market with a growing financial inclusion sector in countries like Brazil and Chile.

- Key Drivers:

- Growing digital transformation in the banking sector, particularly in Brazil and Chile, to combat high rates of financial fraud.

- Increasing modernization of small-scale government facilities into commercial-grade digital identity centers.

- Rising interest in Mediterranean-style smart retail and frictionless shopping among urban middle-to-high income segments.

- Trends: Growth of localized card personalization centers and the introduction of PETG as a durable alternative for regional banking.

Middle East and Africa

- Market Share: Developing market with deep government investment in digital governance and biometric ID systems.

- Key Drivers:

- High demand for shelf-stable and heat-resistant card materials (like ABS and PC) capable of withstanding arid climates.

- Strategic investments in Smart Agriculture and Smart Cities in the UAE and Saudi Arabia to improve local food security and logistics.

- The adoption of EMV chip technology to reduce card-present fraud in rapidly growing retail sectors like Egypt and Qatar.

- Trends: Implementation of high-end Polycarbonate solutions for national security programs and a focus on mobile-integrated smart card technologies.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Thales, IDEMIA, and Giesecke+Devrient. Regional specialists and material innovators like Eastman Chemical and LG Chem also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Premiumization and functional branding: Positioning materials like Polycarbonate as superior for high-security applications due to their longevity and laser-marking capabilities.

- Diversified Product Portfolios: Materials now include more than just flat plastic; providers offer specialized layers for biometric sensors, transparent windows, and haptic textures.

- Vertical Integration and Traceability: Producers manage the entire supply chain, ensuring ethical sourcing of recycled resins and meeting global ISO standards for card durability.

- New Material Technologies: Innovations like bio-sourced polymers and advanced multi-layer bonding help create high-quality cards used in secure financial and government ecosystems worldwide.

Opportunities and Strategic Moves

- Partner with high-end retail banks and fintechs to tap into the surging demand for metal and recycled plastic cards in the North American and European markets.

- Incorporate sustainable manufacturing practices and circular economy certifications to appeal to Gen Z consumers seeking ethical and low-carbon footprint products.

Major Companies operating in the Smart Card Material Market are:

- Eastman Chemical Company

- PetroChina Company Limited

- Solvay S.A.

- KEM ONE

- SABIC

- 3A Composites GmbH

- Teijin Limited

- LG Chem

- BASF SE

- Westlake Chemical Corporation

Disclaimer: The companies listed above are not ranked in any particular order.

Smart Card Material Market News and Recent Developments

- In December 2025, LG Innotek announced that the company had successfully developed a ‘Next-Generation Smart IC (integrated circuit) Substrate’ featuring enhanced performance and reducing carbon emissions generated in its production by half. The smart IC substrate is an essential component for mounting IC chips that store information on smart cards, such as those in credit cards, electronic passports, and USIMs. When users place a smart card in an ATM or on a passport reader, the IC chip's information is transmitted to the device via electronic signals.

- In November 2025, Teijin Limited announced the launch of proof-of-concept (PoC) demonstration using Digital Product Passports (DPPs) to ensure the traceability of recycled polycarbonate (PC) resin throughout the supply chain. Teijin will evaluate the effectiveness of the DPP as a means of complying with the European Union’s draft Directive on End-of-Life Vehicles (ELV).

Smart Card Material Market Report Coverage and Deliverables

The Smart Card Material Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Smart Card Material Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Smart Card Material Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Smart Card Material Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Smart Card Material Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For