تحليل سوق الزيوت والدهون الصالحة للأكل والتنبؤ بها حسب الحجم والحصة والنمو والاتجاهات 2030

البيانات التاريخية : 2020-2021 | سنة الأساس : 2022 | فترة التنبؤ : 2023-2030حجم سوق الزيوت والدهون الصالحة للأكل وتوقعاته (2020-2030)، والحصة العالمية والإقليمية، والاتجاهات، وتحليل فرص النمو. يغطي التقرير: حسب النوع [الزيت (زيت فول الصويا، زيت دوار الشمس، زيت النخيل، زيت الكانولا/زيت بذور اللفت، وغيرها) والدهون (الزبدة، السمن النباتي، السمن النباتي، السمن النباتي، وغيرها)] والاستخدام [الأغذية والمشروبات (المخبوزات والحلويات، منتجات الألبان والحلويات المجمدة، الوجبات الجاهزة والوجبات الجاهزة، وغيرها)، تغذية الحيوانات، والمستحضرات الصيدلانية والمكملات الغذائية].

- تاريخ التقرير : Nov 2023

- رمز التقرير : TIPRE00030249

- الفئة : المأكولات والمشروبات

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 150

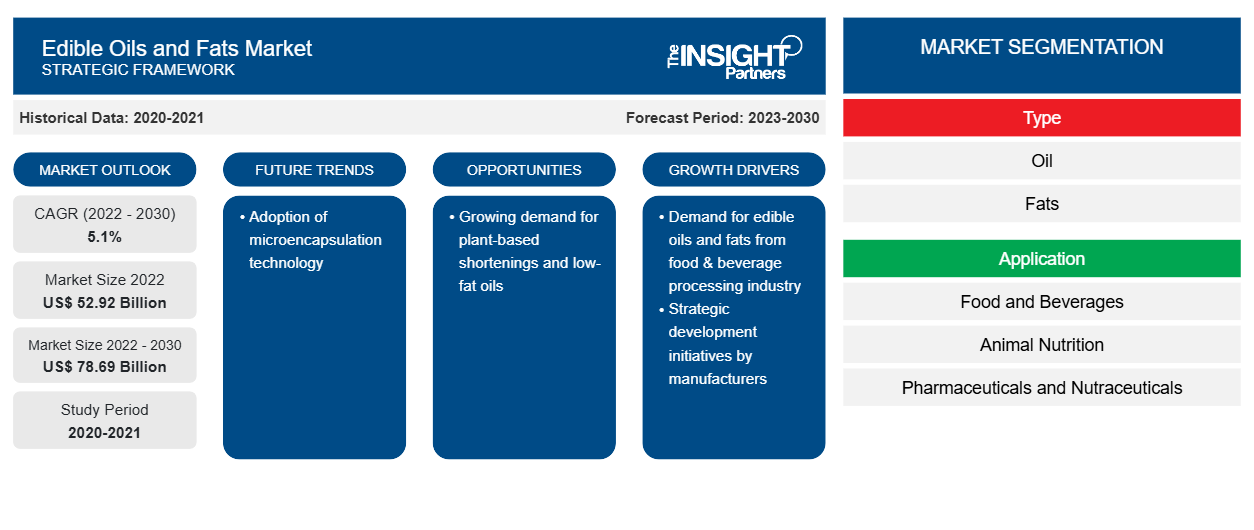

[تقرير بحثي] من المتوقع أن ينمو سوق الزيوت والدهون الصالحة للأكل من 52،920.00 مليون دولار أمريكي في عام 2022 إلى 78،686.61 مليون دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 5.1٪ من عام 2023 إلى عام 2030.

رؤى السوق ووجهة نظر المحلل:

يتم الحصول على الدهون الصالحة للأكل من خلال المواد الخام ذات الأصل الحيواني مثل دهن الخنزير (شحم الخنزير) والشحم البقري أو من أصل نباتي. تعد شركات معالجة اللحوم موردي المواد الخام لمصنعي الدهون الصالحة للأكل والمشتقة من الحيوانات. لدى الشركات المصنعة اتفاقيات طويلة الأجل مع صناعات معالجة اللحوم لتوريد المواد الخام دون انقطاع. يتم تقطيع الأنسجة الدهنية من لحم الخنزير أو لحم البقر إلى قطع صغيرة وغليها في أجهزة هضم بالبخار، حيث يتم إطلاق الدهون في الماء. تطفو الدهون فوق سطح الماء ويتم جمعها عن طريق الإزالة. يتم ضغط المادة الغشائية للأنسجة الحيوانية في مكبس هيدروليكي حيث يتم الحصول على دهون إضافية. يتم فصل الدهون عن الطور السائل في جهاز طرد مركزي لإزالة الحمأة.

يتم الحصول على الدهون النباتية مثل السمن النباتي عن طريق هدرجة زيت فول الصويا أو زيت الذرة أو زيت القرطم. يتم تبييض الزيت أولاً باستخدام تراب التبييض أو الفحم لإزالة الرائحة واللون غير المرغوب فيهما. ثم يتم تمريره عبر غاز الهيدروجين تحت ضغط عالٍ، مما يؤدي إلى تصلب الزيت للحصول على السمن النباتي. هناك عمليات مختلفة لتصنيع الزيوت والدهون النباتية.

يتم تعبئة الزيوت والدهون الصالحة للأكل المكررة في حاويات وإرسالها إلى المستخدمين النهائيين مثل صناعات الأغذية والمشروبات وتغذية الحيوانات والأدوية والمكملات الغذائية من خلال الموزعين والموردين. تعد شركة Cargill Incorporated وBunge Limited وADM وFuji Oil Co Ltd وKao Corporation من بين الشركات المصنعة الرئيسية للزيوت والدهون الصالحة للأكل في جميع أنحاء العالم.

محركات النمو والتحديات:

وفقًا لوزارة الزراعة الأمريكية (USDA)، فإن زيت الصويا هو ثاني أكبر زيت نباتي مستهلك. يتم استخدامه على نطاق واسع في القلي والطهي والتقصير والسمن. وفقًا لمنظمة التعاون الاقتصادي والتنمية (OECD)، في عام 2022، بلغ استهلاك الزيوت النباتية 249 مليون طن متري، حيث يمثل قطاع الأغذية الحصة الأكبر. علاوة على ذلك، تستخدم صناعة الحلويات الزبدة بشكل كبير كمكون أساسي، تليها السمن. تُستخدم الزيوت والدهون الصالحة للأكل عالية الجودة في المخابز والحلويات ومنتجات الألبان والحلويات المجمدة والوجبات الخفيفة والوجبات الجاهزة للأكل والجاهزة للطهي وغيرها من الأطعمة والمشروبات. الزيوت والدهون المكررة هي مصدر غني بالدهون. وبالتالي، يتزايد استخدامها بسبب زيادة استخدامها وتزايد عدد سكان العالم.

تشهد صناعة الأغذية والمشروبات في مناطق مختلفة مثل أمريكا الشمالية ومنطقة آسيا والمحيط الهادئ نموًا مستمرًا بسبب الميل المتزايد نحو الاستدامة وتفضيل الراحة والمنتجات الجاهزة للأكل والاعتماد المتزايد على المنتجات العضوية والنباتية. تشهد الصناعة حركة كبيرة مع الابتكار في العمليات والمنتجات والخدمات لتلبية تفضيلات المستهلكين المتغيرة بسرعة. وفقًا لمكتب الإحصاء الأمريكي، كان لدى الولايات المتحدة 39646 مصنعًا لتصنيع الأغذية والمشروبات في عام 2020. منها كاليفورنيا وتكساس ونيويورك 6116 و2625 و2600 على التوالي. وبالمثل، تعد صناعة الأغذية والمشروبات واحدة من المساهمين المهمين في الاقتصاد الأوروبي. وبالتالي، فإن صناعة الأغذية والمشروبات المتنامية في جميع أنحاء العالم تدفع الطلب على الزيوت والدهون الصالحة للأكل.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الزيوت والدهون الصالحة للأكل: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

"يُقسم " سوق الزيوت والدهون الصالحة للأكل العالمية " على أساس النوع والتطبيق والجغرافيا. بناءً على النوع، ينقسم السوق إلى زيوت ودهون. بناءً على التطبيق، تنقسم الزيوت والدهون الصالحة للأكل العالمية إلى أغذية ومشروبات، وتغذية حيوانية، ومستحضرات صيدلانية ومكملات غذائية. احتل قطاع الزيوت حصة أكبر من السوق العالمية.

سوق الزيوت والدهون الصالحة للأكل

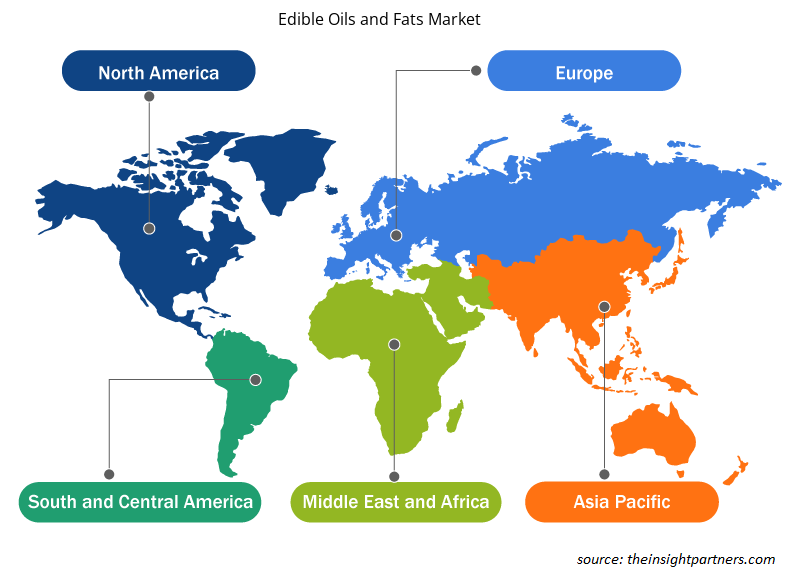

في عام 2022. بناءً على الجغرافيا، يتم تقسيم سوق الزيوت والدهون الصالحة للأكل إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك)، وأوروبا (ألمانيا وفرنسا وإيطاليا والمملكة المتحدة وروسيا وبقية أوروبا)، وآسيا والمحيط الهادئ (أستراليا والصين واليابان والهند وكوريا الجنوبية وبقية آسيا والمحيط الهادئ)، والشرق الأوسط وأفريقيا (جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وبقية الشرق الأوسط وأفريقيا)، وأمريكا الجنوبية والوسطى (البرازيل وتشيلي وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

بناءً على النوع، ينقسم سوق الزيوت والدهون الصالحة للأكل إلى زيت ودهون. احتل قطاع الزيوت حصة أكبر من سوق الزيوت والدهون الصالحة للأكل في عام 2022 ومن المتوقع أن يسجل معدل نمو سنوي مركب أعلى خلال فترة التوقعات. يمكن استخلاص الزيوت النباتية من البذور والحبوب والمكسرات والفواكه. تعد زيوت الزيتون وعباد الشمس والنخيل والكانولا وجوز الهند والقرطم والذرة والفول السوداني وبذور القطن ونواة النخيل وفول الصويا من بين أكثر الزيوت استهلاكًا. بشكل عام، تُستخدم الزيوت النباتية في تحضير الطعام، ويُضاف الزيت الخام للنكهة. كما يستخدم الزيت النباتي في إنتاج الأعلاف الحيوانية. يسهل تثبيت زيوت النخيل، وتحافظ على جودة النكهة والاتساق في الأطعمة المصنعة. لذلك، يفضلها مصنعو الأغذية بشكل متكرر. تعد إندونيسيا وماليزيا وتايلاند ونيجيريا من بين أكبر منتجي ومصدري زيت النخيل. يدفع الوعي المتزايد المتعلق بالمخاوف الصحية المرتبطة بالدهون المتحولة في الزيوت النباتية المهدرجة إلى استخدام زيت النخيل في صناعة الأغذية. إن صناعة الأغذية الزراعية تستهلك كميات كبيرة من زيت النخيل، حيث يستخدم بشكل رئيسي في المخبوزات الصناعية ومنتجات الشوكولاتة والحلويات والآيس كريم وحتى بدائل الوجبات الغذائية. يعتبر زيت النخيل مصدرًا غنيًا بالتوكوفيرول والكاروتينات، التي تمنحه ثباتًا طبيعيًا ضد التدهور التأكسدي. وبالتالي، فإن فوائد وتطبيقات زيت النخيل في مختلف الصناعات النهائية تدفع الطلب عليها في جميع أنحاء العالم.

التحليل الإقليمي:

تنقسم سوق الزيوت والدهون الصالحة للأكل إلى خمس مناطق رئيسية - أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا. كانت أمريكا الجنوبية والوسطى تهيمن على سوق الزيوت والدهون الصالحة للأكل العالمية وقُدِّرت بنحو 4500 مليار دولار أمريكي في عام 2022. تنقسم سوق الزيوت والدهون الصالحة للأكل في أمريكا الجنوبية والوسطى إلى البرازيل والأرجنتين وبقية أمريكا الجنوبية والوسطى. يتوسع قطاع الوجبات الخفيفة في المنطقة بسبب تفضيل المستهلك المتزايد لخيارات الوجبات الخفيفة المختلفة مثل الوجبات الخفيفة المجمدة والوجبات الخفيفة اللذيذة والوجبات الخفيفة من الفاكهة والوجبات الخفيفة من الحلويات والوجبات الخفيفة من المخبوزات. تلعب الزيوت والدهون الصالحة للأكل دورًا لا يتجزأ، حيث توفر نكهات مميزة للطعام وتوفر وظائف فريدة ومرغوبة في تصنيع الوجبات الخفيفة. على سبيل المثال، الزيوت هي وسائط القلي للأطعمة المقلية، وفي المعجنات، تُضاف الزيوت النباتية لمنع تكتل الدقيق والمكونات الأخرى. ومن ثم، فإن الطلب المتزايد على الوجبات الخفيفة المختلفة والفوائد المرتبطة بالزيوت والدهون الصالحة للأكل يدفع الطلب على الزيوت والدهون الصالحة للأكل في قطاع الوجبات الخفيفة في أمريكا الجنوبية والوسطى.

علاوة على ذلك، شهد الطلب على الزيوت والدهون الصالحة للأكل في الصناعات النهائية مثل تغذية الحيوانات ارتفاعًا في أمريكا الجنوبية والوسطى. ووفقًا لـ Oil World، في عام 2022، اشترت الصين حوالي 70٪ من زيت فول الصويا البرازيلي، وخاصة لاستهلاك البروتين الحيواني. علاوة على ذلك، فإن توسع صناعات التغذية الحيوانية والأدوية والمستحضرات الغذائية يدفع الطلب على الزيوت والدهون الصالحة للأكل المتخصصة. تتطلب هذه الصناعات أنواعًا معينة من الزيوت لتطبيقات مختلفة، مثل تركيبات الأعلاف الحيوانية والتركيبات الصيدلانية. ومع نمو هذه القطاعات وتنوعها، يزداد الطلب على متطلباتها الفريدة، مما يغذي نمو سوق الزيوت والدهون الصالحة للأكل في أمريكا الجنوبية والوسطى.

تطورات الصناعة والفرص المستقبلية:

فيما يلي قائمة بالمبادرات المختلفة التي اتخذها اللاعبون الرئيسيون العاملون في سوق الزيوت والدهون الصالحة للأكل العالمية:

- في أكتوبر 2021، أعلنت شركة ADM، إحدى أبرز شركات تصنيع الدهون والزيوت الصالحة للأكل في الولايات المتحدة، عن خططها لبناء أول مصنع ومصفاة لتكسير فول الصويا على الإطلاق في داكوتا الشمالية لتلبية الطلب المتزايد بسرعة على زيت فول الصويا من صناعات الأغذية والأعلاف الحيوانية.

- في ديسمبر 2021، أعلنت شركة ITOCHU Corporation، التي يقع مقرها الرئيسي في اليابان، عن اتفاقها من خلال شركة ITOCHU International Inc.، التي يقع مقرها الرئيسي في نيويورك، الولايات المتحدة، لتأسيس شركة Fuji Oil International Inc. في الولايات المتحدة. ومن خلال هذه الاتفاقية، تخطط الشركة لتعزيز أعمال الزيوت والدهون في أمريكا الشمالية.

رؤى إقليمية حول سوق الزيوت والدهون الصالحة للأكل

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الزيوت والدهون الصالحة للأكل طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الزيوت والدهون الصالحة للأكل والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الزيوت والدهون الصالحة للأكل

نطاق تقرير سوق الزيوت والدهون الصالحة للأكل

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 52.92 مليار دولار أمريكي |

| حجم السوق بحلول عام 2030 | 78.69 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 5.1% |

| البيانات التاريخية | 2020-2021 |

| فترة التنبؤ | 2023-2030 |

| القطاعات المغطاة |

حسب النوع

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

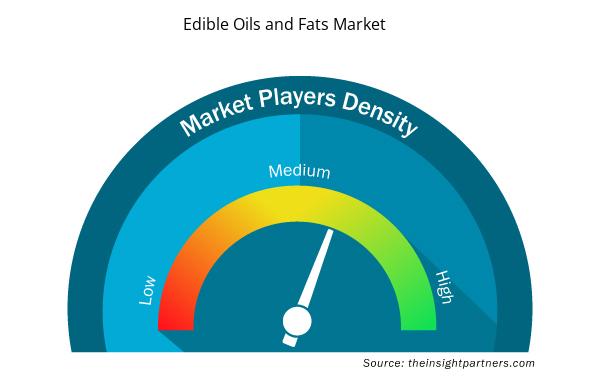

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الزيوت والدهون الصالحة للأكل نموًا سريعًا، مدفوعًا بالطلب المتزايد من جانب المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الزيوت والدهون الصالحة للأكل هي:

- شركة بونج المحدودة

- شركة آرتشر دانييلز ميدلاند

- شركة فوجي للزيوت المحدودة

- شركة كاو

- ايه ايه كيه ايه بي

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الزيوت والدهون الصالحة للأكل

تأثير جائحة كوفيد-19:

أثرت جائحة كوفيد-19 على الاقتصادات والصناعات في مختلف البلدان. أثرت عمليات الإغلاق وحظر السفر وإغلاق الشركات في الدول الرائدة في أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا سلبًا على نمو مختلف الصناعات، بما في ذلك صناعة الأغذية والمشروبات. أدى إغلاق وحدات التصنيع إلى اضطراب سلاسل التوريد العالمية وأنشطة التصنيع وجداول التسليم ومبيعات مختلف المنتجات الأساسية وغير الأساسية. أعلنت شركات مختلفة عن تأخيرات محتملة في تسليم المنتجات وانخفاض في مبيعات منتجاتها المستقبلية في عام 2020. بالإضافة إلى ذلك، أجبر الحظر الذي فرضته حكومات مختلفة في أوروبا وآسيا وأمريكا الشمالية على السفر الدولي الشركات على تعليق خطط التعاون والشراكة مؤقتًا. كل هذه العوامل أعاقت صناعة الأغذية والمشروبات في عام 2020 وأوائل عام 2021، وبالتالي كبح نمو سوق الزيوت والدهون الصالحة للأكل.

المنافسة والشركات الرئيسية:

تعد شركات Bunge Ltd وArcher-Daniels-Midland Co وFuji Oil Co Ltd وKao Corp وAAK AB وJ-Oil Mills Inc وCargill Inc وOlam Group Ltd وConnOils LLC وLouis Dreyfus Co BV من بين اللاعبين البارزين الذين يعملون في سوق الزيوت والدهون الصالحة للأكل على مستوى العالم. تقدم شركات تصنيع الزيوت والدهون الصالحة للأكل حلول مستخلصات متطورة بميزات مبتكرة لتقديم تجربة فائقة للمستهلكين.

حابي محلل أبحاث سوق متمرس، يتمتع بخبرة 8 سنوات في قطاع الكيماويات والمواد، بالإضافة إلى خبرته في قطاعي الأغذية والمشروبات والسلع الاستهلاكية. وهو مهندس كيميائي من معهد فيشواكارما للتكنولوجيا (VIT)، وقد اكتسب معرفةً عميقةً في مجالات الكيماويات الصناعية والتخصصية، والدهانات والطلاءات، والورق والتغليف، ومواد التشحيم، والمنتجات الاستهلاكية.

تشمل كفاءات حابي الأساسية تقدير حجم السوق والتنبؤ به، ووضع معايير تنافسية، وتحليل الاتجاهات، والتفاعل مع العملاء، وكتابة التقارير، وتنسيق الفريق، مما يجعله بارعًا في تقديم رؤى عملية ودعم اتخاذ القرارات الاستراتيجية.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

تقارير ذات صلة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق الزيوت والدهون الصالحة للأكل

احصل على عينة مجانية ل - سوق الزيوت والدهون الصالحة للأكل