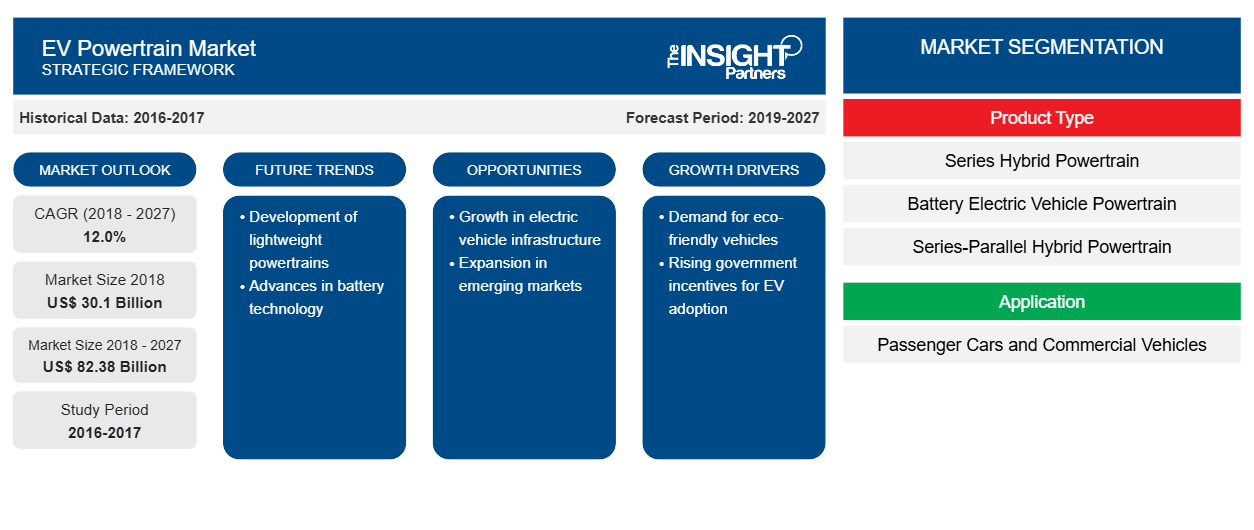

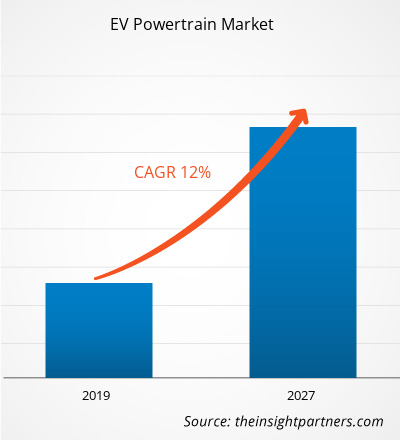

بلغت قيمة سوق توليد الطاقة للسيارات الكهربائية 30,095.5 مليون دولار أمريكي في عام 2018، ومن المتوقع أن تنمو بمعدل نمو سنوي مركب قدره 12.0٪ خلال الفترة المتوقعة 2019 - 2027، لتصل إلى 82,382.3 مليون دولار أمريكي بحلول عام 2027.

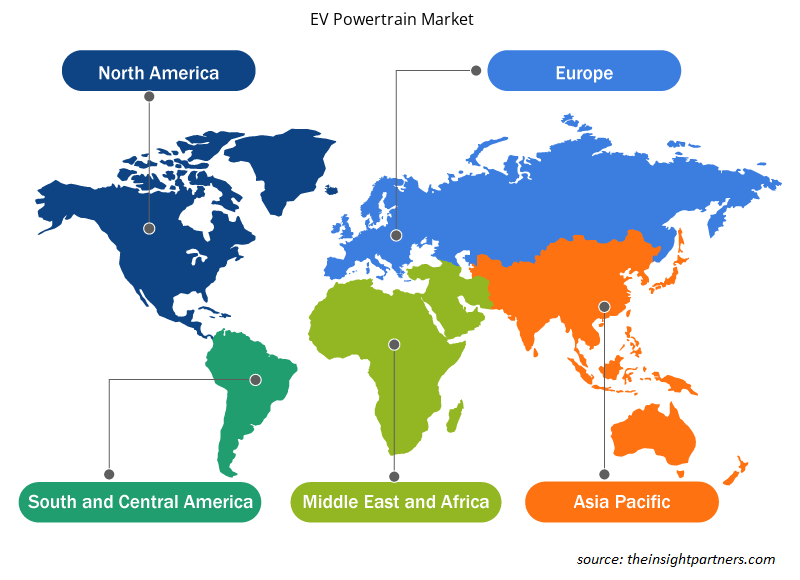

من الناحية الجغرافية، يتم تقسيم سوق توليد القوة الكهربائية للسيارات إلى أمريكا الشمالية، ومنطقة آسيا والمحيط الهادئ، وأوروبا، وبقية العالم. تصدرت منطقة آسيا والمحيط الهادئ سوق توليد القوة الكهربائية للسيارات في عام 2018 بحصة سوقية كبيرة، ومن المتوقع أيضًا أن تكون المنطقة الأسرع نموًا خلال الفترة المتوقعة من 2019 إلى 2027. تليها أوروبا التي تضم بعض البلدان المتقدمة، وتتمتع المنطقة بقطاع سيارات قوي من المتوقع أن يقود نمو سوق توليد القوة الكهربائية للسيارات في المنطقة. بينما في أمريكا الشمالية، يستثمر مصنعو المعدات الأصلية ومقدمو التكنولوجيا باستمرار مبالغ كبيرة في تطوير حلول قوية، وهو ما يجذب عملاء المركبات. تعد الصين أكبر دولة مصنعة للسيارات الكهربائية ، ومعدل تبني السيارات الكهربائية هو الأعلى في جميع أنحاء العالم، حيث تستثمر العديد من شركات تصنيع السيارات الكهربائية الدولية في البلاد وتوسع وحدات إنتاجها إلى البلاد. على سبيل المثال، تستثمر شركة تسلا 2.0 مليار دولار أمريكي في مصنع جديد في شنغهاي، الصين، لإنتاج سيارة سيدان موديل 3 والمركبات المستقبلية. كما تبنت شركة فولكس فاجن استراتيجية مماثلة لجمع أكثر من 10 مليارات دولار أمريكي في الصين لأكثر من ست سنوات. تعد أوروبا ثاني أكبر سوق في سوق توليد الطاقة للسيارات الكهربائية . تظل أمريكا الشمالية ثالث أكبر قطاع جغرافي في سوق توليد الطاقة للسيارات الكهربائية . في أمريكا الشمالية، تعد الشعبية المتزايدة للسيارات الكهربائية، وصناعة السيارات القوية في دول مثل الولايات المتحدة وكندا، ووجود عدد كبير من مزودي توليد الطاقة للسيارات الكهربائية من بين العوامل الرئيسية التي من المتوقع أن تدعم نمو سوق توليد الطاقة للسيارات الكهربائية في المنطقة.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق المحركات الكهربائية :

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

رؤى السوق

المبادرات الحكومية نحو اعتماد محركات السيارات الكهربائية

تشهد صناعة السيارات العالمية تحولًا كبيرًا من المركبات التقليدية إلى المركبات الكهربائية. تتخذ الحكومات في مختلف البلدان مبادرات لدفع تبني المركبات الكهربائية. على سبيل المثال، استثمرت حكومة كندا 182.5 مليون دولار أمريكي لتطوير شبكة شحن سريع للمركبات الكهربائية. أيضًا، في ديسمبر 2017، أصدرت الحكومة الفيدرالية الكندية استراتيجية الحكومة الخضراء، والتي تهدف إلى تقليل انبعاثات الغازات المسببة للانحباس الحراري بنسبة 80٪ بحلول عام 2050. أيضًا، وفقًا لشركة Clean Energy Canada، استثمرت الحكومة الكندية مليار دولار أمريكي في عام 2017 لإنتاج المركبات الكهربائية. في عام 2019، كان أكثر من 40 طرازًا من المركبات الكهربائية متاحًا في السوق الكندية بسبب زيادة الإنتاج والطلب. أيضًا، تمثل المركبات الكهربائية 2.5٪ من جميع المركبات المباعة في كندا. علاوة على ذلك، وفقًا لـ GOV.UK ، في يوليو 2019، استثمرت السلطات في المملكة المتحدة ما يصل إلى 100 مليون دولار أمريكي لتطوير الجيل القادم من المركبات الكهربائية. ومن ثم، تتعاون الحكومة أيضًا مع قادة الصناعة لتسريع تطوير المركبات الكهربائية والهجينة.

التطور التكنولوجي في المحركات التقليدية

على مدى السنوات الماضية، شهدت السيارات تطورات تكنولوجية كبيرة، وخاصة في تطوير التقنيات البديلة. ومن المرجح أن تحظى التقنيات مثل أنظمة القيادة الكهربائية بحصة كبيرة في قطاع السيارات. وتشهد المحركات تطورات، مع معايير جديدة لاقتصاد الوقود والانبعاثات. وعلاوة على ذلك، يُنظر إلى كهربة المركبات على أنها تقدم في تكنولوجيا السيارات.

رؤى حول نوع المنتج

تم تقسيم سوق توليد القوة الكهربائية العالمية حسب النوع إلى توليد القوة الهجينة المتسلسلة، وتوليد القوة الكهربائية للمركبات الكهربائية التي تعمل بالبطارية، وتوليد القوة الهجينة المتسلسلة المتوازية، وتوليد القوة الهجينة المعتدلة، وتوليد القوة الهجينة المتوازية. هيمنت شريحة توليد القوة الكهربائية للمركبات الكهربائية على سوق توليد القوة الكهربائية بشكل كبير ومن المتوقع أن تستمر في هيمنتها طوال فترة التنبؤ من 2019 إلى 2027. تعد مجموعة توليد القوة الكهربائية للمركبات الكهربائية التي تعمل بالبطارية هي مجموعة توليد القوة الكهربائية الأكثر شعبية في سيناريو صناعة توليد القوة الكهربائية الحالية.

رؤى التطبيق

ينقسم سوق نقل الحركة للسيارات الكهربائية حسب نوع المركبة إلى مركبات الركاب والمركبات التجارية. يهيمن قطاع مركبات الركاب في سوق نقل الحركة للسيارات الكهربائية على نوع المركبة ومن المتوقع أن يستمر هيمنته طوال الفترة المتوقعة من 2019 إلى 2027. ويعزى الطلب المتزايد على سيارات الركاب في جميع أنحاء العالم إلى زيادة الدخل المتاح بين السكان في البلدان المتقدمة والنامية.

يُلاحظ أن مبادرات السوق هي الاستراتيجية الأكثر استخدامًا في سوق توليد القوة للسيارات الكهربائية على مستوى العالم. وفيما يلي بعض مبادرات السوق الحديثة:

2019: أعلنت شركة Continental AG أنها ستبدأ الإنتاج الضخم لأول محرك محوري متكامل بالكامل في الصين. سيتم استخدام المحركات المنتجة في المركبات من الشركات المصنعة للمعدات الأصلية الصينية والأوروبية.

2019: أعلنت شركة Hydro-Québec أن الشركة استثمرت 85 مليون دولار لتأمين نمو TM4، والتي تسمى الآن Dana TM4، ولضمان مكانتها القيادية في قطاع توليد الطاقة الكهربائية. منذ يونيو 2018، احتفظت شركة Hydro-Québec بحصة 45٪ في شركة Dana TM4 التابعة كجزء من شراكة استراتيجية مع شركة Dana Incorporated.

2019: طورت شركة Mahle محركًا هجينًا معياريًا متكاملًا بالكامل يمكن استخدامه لمجموعة واسعة من التطبيقات. يعد محرك MAHLE Modular Hybrid Powertrain محركًا هجينًا مدمجًا بالكامل يتضمن محرك بنزين بشاحن توربيني مكون من أسطوانتين أو ثلاث أسطوانات.

رؤى إقليمية حول سوق أنظمة نقل الحركة في المركبات الكهربائية

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق توليد الطاقة للسيارات الكهربائية طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق توليد الطاقة للسيارات الكهربائية والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق مجموعة نقل الحركة للسيارات الكهربائية

نطاق تقرير سوق مجموعة نقل الحركة للسيارات الكهربائية

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2018 | 30.1 مليار دولار أمريكي |

| حجم السوق بحلول عام 2027 | 82.38 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2018 - 2027) | 12.0% |

| البيانات التاريخية | 2016-2017 |

| فترة التنبؤ | 2019-2027 |

| القطاعات المغطاة | حسب نوع المنتج

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق أنظمة نقل الحركة للسيارات الكهربائية نموًا سريعًا، مدفوعًا بالطلب المتزايد من جانب المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق توليد الطاقة للسيارات الكهربائية هي:

- شركة كونتيننتال ايه جي

- شركة روبرت بوش المحدودة

- شركة كومينز

- شركة مكسيم للمنتجات المتكاملة

- ماجنا الدولية المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق توليد القوة للسيارات الكهربائية

تجزئة سوق محركات السيارات الكهربائية العالمية

السوق العالمية لمحركات السيارات الكهربائية - حسب نوع المنتج

- سلسلة نقل الحركة الهجينة

- مجموعة نقل الحركة للسيارات الكهربائية التي تعمل بالبطارية

- مجموعة نقل الحركة الهجينة المتسلسلة المتوازية

- نظام نقل الحركة الهجين المعتدل

- نظام نقل الحركة الهجين المتوازي

السوق العالمية لمحركات السيارات الكهربائية - حسب التطبيق

- سيارات الركاب

- المركبات التجارية

السوق العالمية لمحركات السيارات الكهربائية - حسب المنطقة الجغرافية

أمريكا الشمالية

- نحن

- كندا

- المكسيك

أوروبا

- فرنسا

- ألمانيا

- المملكة المتحدة

- السويد

- هولندا

- سلوفاكيا

- بقية أوروبا

آسيا والمحيط الهادئ (APAC)

- الصين

- اليابان

- الهند

- كوريا الجنوبية

بقية العالم

سوق توليد الطاقة للسيارات الكهربائية العالمية - ملفات تعريف الشركات

- شركة كونتيننتال ايه جي

- شركة روبرت بوش المحدودة

- شركة كومينز

- شركة مكسيم للمنتجات المتكاملة

- ماجنا الدولية المحدودة

- تاتا إلكسي

- شركة دانا المحدودة

- شركة فاليو اس ايه

- شركة ماهله المحدودة

- شركة ZF فريدريشهافن ايه جي

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

- Data Annotation Tools Market

- Integrated Platform Management System Market

- Trade Promotion Management Software Market

- Ceiling Fans Market

- Industrial Inkjet Printers Market

- Rugged Servers Market

- Artificial Intelligence in Healthcare Diagnosis Market

- Rare Neurological Disease Treatment Market

- Wind Turbine Composites Market

- Radiopharmaceuticals Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

The passenger vehicle segment led the EV powertrain market, by application. The trend of procurement of passenger cars is increasing at a high rate over the years and the trend is anticipated to continue in the future. Passenger car segment undergo substantial technological advancements year on year, owing to the changes in consumer interests, emergence of new technologies. Also, the trend of procurement of passenger cars is increasing at a decent rate over the years. The increase in awareness among the vehicular customers related to the benefits of electric vehicles has resulted in downsizing of fossil fuel vehicles. Also, several governmental initiatives have propelled the growth of electric passenger cars over the years.

Key players in the automotive market are focusing on investing in the production of electric vehicles. There have been prominent collaborations in recent years between automakers and tech companies to develop technologically advanced electric vehicles. For instance, in December 2019, Fiat Chrysler planned a merger with French automaker PSA Group to focus on the development of electric vehicles. As the market is moving toward EV adaptation, due to changing business strategy in order to innovate, the ICE vehicle manufacturers are shifting their focus towards EVs. Further, with increasing awareness about the rising levels of greenhouse gas emission and negative impacts of the conventional vehicles in the form of increasing population are the major factors propelling key players to invest in electric vehicles

The growth of the EV powertrain market in the Asia-Pacific region is primarily driven by the growing automotive industry. Asia-Pacific EV powertrain market is progressing rapidly with China holding the leading position followed by Japan and South Korea. China dominates the entire Asia-Pacific region in terms of the number of electric vehicles. Pertaining to a growing middle class, high economic growth, and rapid technological advancement have created immense growth opportunities for the various industries especially automotive industry. China has been the largest automotive market globally over the years. The growth in the automotive sector in China has been achieved mainly through the establishment of various joint ventures with car manufacturers such as Volkswagen, General Motors, and others

The List of Companies - EV Powertrain Market

- Continental AG

- Robert Bosch GmbH

- Cummins, Inc.

- Maxim Integrated Products, Inc.

- Magna International Inc.

- Tata Elxsi

- Dana Limited

- Valeo SA

- Mahle GmbH

- ZF Friedrichshafen AG

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير