تقرير سوق معدات الهبوط بطائرات الهليكوبتر 2031 حسب القطاعات والجغرافيا والديناميكيات والتطورات الأخيرة والرؤى الاستراتيجية

البيانات التاريخية : 2021-2022 | سنة الأساس : 2023 | فترة التنبؤ : 2024-2031حجم سوق معدات هبوط المروحيات وتوقعاته (2021-2031)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: حسب النوع (الزلاجات والعجلات)، والمواد (مجموعة معدات هبوط من الألومنيوم، ومجموعة معدات هبوط من الفولاذ، ومجموعة معدات هبوط مركبة، والتيتانيوم)، والتطبيق (المروحيات المدنية والعسكرية)، والموقع الجغرافي.

- تاريخ التقرير : Mar 2026

- رمز التقرير : TIPRE00019420

- الفئة : الفضاء والدفاع

- الحالة : البيانات الصادرة

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 150

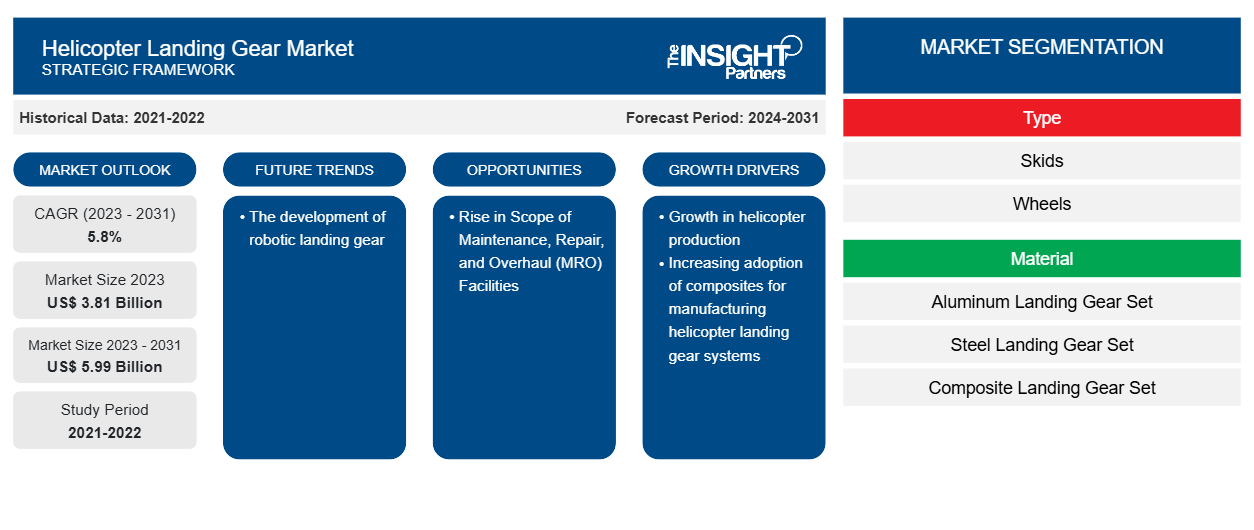

من المتوقع أن يصل حجم سوق معدات هبوط الطائرات المروحية إلى 5.99 مليار دولار أمريكي بحلول عام 2031 من 3.81 مليار دولار أمريكي في عام 2023. ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 5.8٪ خلال الفترة 2023-2031. ومن المرجح أن يظل تطوير معدات الهبوط الآلية اتجاهًا رئيسيًا في السوق.

تحليل سوق معدات هبوط المروحيات

تتميز صناعة تصنيع أو تحديث الطائرات المروحية العالمية بوجود شركات تصنيع طائرات مروحية معروفة وقوية مالياً مثل إيرباص وبيل هليكوبتر. ونتيجة لهذا، فإن القوة التفاوضية للمشترين في سوق معدات هبوط الطائرات المروحية عالية جدًا في الوقت الحاضر، ومع ذلك، من المتوقع أن تنخفض القوة التفاوضية للمشترين إلى مستوى معتدل في السنوات القادمة. تواجه شركات تصنيع الطائرات المروحية مثل إيرباص وبيل هليكوبتر وشركة سيكورسكي للطائرات وغيرها منافسة شرسة فيما بينها وتتطلب تحسينًا مستمرًا في طائراتها للحفاظ على قوتها في السوق. ونظرًا لهذه الحقيقة، فإن هذه الشركات لديها ميل كبير إلى تبديل مقاولي مكونات الطائرات المروحية على مدار فترة زمنية، من أجل تحسين أنظمة الطائرات المروحية بالكامل. وبالتالي، نظرًا للطبيعة الموحدة لصناعة تصنيع الطائرات المروحية مع وجود عدد قليل من مصنعي الطائرات المروحية الكبار، فمن المتوقع أن تظل القوة التفاوضية للمشترين عالية في السنوات القادمة.

نظرة عامة على سوق معدات هبوط المروحيات

يتألف سوق معدات هبوط المروحيات من عدد كبير من الشركات الراسخة والمعروفة مثل Safran SA وLiebherr Group وHéroux-Devtek Inc. وCircor International, Inc. وTriumph Group Inc. وغيرها الكثير. يتمتع هؤلاء اللاعبون في السوق بمكانة علامة تجارية راسخة وحضور طويل الأمد في سوق معدات الهبوط العالمية. يعتمد مصنعو المروحيات بشكل كبير على القيمة التجارية لمصنعي مكونات المروحيات، ونتيجة لهذا، يتم منح غالبية الاتصالات لمصنعي معدات هبوط المروحيات الراسخين والمعترف بهم في الصناعة، وبالتالي، يتم توفير مساحة ضئيلة للمصنعين الجدد لدخول السوق. بالإضافة إلى ذلك، فإن الاستثمارات الرأسمالية الأولية المطلوبة لدخول سوق معدات هبوط المروحيات مرتفعة للغاية، مما يعمل كحاجز دخول للوافدين الجدد.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق معدات هبوط المروحيات: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

محركات وفرص سوق معدات هبوط الطائرات المروحية

ارتفاع إنتاج الطائرات المروحية عالميا

إن ارتفاع عدد إنتاج وتسليم طائرات الهليكوبتر في جميع أنحاء العالم هو أحد العوامل الرئيسية التي تدعم اعتماد معدات هبوط طائرات الهليكوبتر للطائرات الهليكوبتر المدنية والعسكرية في مختلف المناطق حول العالم. على سبيل المثال، وفقًا لجمعية مصنعي الطيران العام (GAMA)، تم تسليم حوالي 1072 طائرة هليكوبتر مدنية في عام 2022 مقارنة بـ 1007 طائرات هليكوبتر في عام 2021. وعلاوة على ذلك، وفقًا لجمعية مصنعي الطيران العام، شهدت عمليات تسليم طائرات الهليكوبتر المكبسية نموًا بنحو 7.7٪ في عام 2023 مع تسليم 209 وحدات في جميع أنحاء العالم؛ في حين شهدت طائرات الهليكوبتر التوربينية المدنية التجارية ارتفاعًا بنحو 9.9٪ مع 811 وحدة في عام 2023. هذا النمو في عمليات التسليم وإنتاج طائرات الهليكوبتر يدفع نمو سوق معدات هبوط طائرات الهليكوبتر في جميع أنحاء العالم.

ارتفاع نطاق مرافق الصيانة والإصلاح والتجديد (MRO)

لقد استكمل النمو الهائل للطائرات المروحية إنشاء مرافق الصيانة والإصلاح والعمرة في العالم على مر السنين. ومن المتوقع أن يرتفع نطاق مرافق الصيانة والإصلاح والعمرة في أجزاء مختلفة من العالم، وخاصة في آسيا. ونظرًا للاعتماد المتزايد على المروحيات المدنية لأغراض تجارية مختلفة مثل مكافحة حرائق الغابات، وتسهيل تغطية الأخبار والمرور، وإجراء مهام البحث والإنقاذ، ودوريات خطوط أنابيب الغاز والنفط، فإن إنشاء مرافق الصيانة والإصلاح والعمرة يشهد أيضًا اتجاهًا إيجابيًا. إن الاستخدام المتزايد للطائرات المروحية يسرع بسرعة نطاق أعمال صيانة المروحيات. تشهد دول مثل سنغافورة والهند وجود شركات تقدم خدمات الصيانة والإصلاح والعمرة المرتبطة بمعدات هبوط المروحيات. وقد دخلت شركة Tentacle Aerologistix Pvt. Ltd. مجال الصيانة والإصلاح والعمرة بهدف إنشاء علامة فارقة في صيانة الطائرات. وعلاوة على ذلك، أعلنت العديد من الدول الناشئة أيضًا عن خططها لإنشاء مركز للصيانة والإصلاح والعمرة في مناطقها المعنية. على سبيل المثال، أعلنت الحكومة الهندية عن جعل البلاد مركزًا للصيانة والإصلاح والعمرة للطيران، ومن المتوقع أن يؤدي ذلك إلى زيادة الطلب على أنظمة معدات هبوط المروحيات في جميع أنحاء المنطقة.

تقرير تحليلي لتجزئة سوق معدات هبوط المروحيات

إن القطاعات الرئيسية التي ساهمت في اشتقاق تحليل سوق معدات هبوط المروحيات هي النوع والمادة والتطبيق.

- بناءً على النوع، ينقسم سوق معدات هبوط المروحيات إلى زلاجات وعجلات. احتلت شريحة الزلاجات حصة سوقية أكبر في عام 2023.

- بناءً على المواد، يتم تقسيم سوق معدات هبوط المروحيات إلى مجموعة معدات هبوط من الألومنيوم، ومجموعة معدات هبوط من الفولاذ، ومجموعة معدات هبوط مركبة، والتيتانيوم . احتلت شريحة المركبات حصة سوقية أكبر في عام 2023.

- بناءً على التطبيق، ينقسم سوق معدات هبوط المروحيات إلى مروحيات مدنية ومروحيات عسكرية. احتل قطاع المروحيات العسكرية حصة سوقية أكبر في عام 2023.

تحليل حصة سوق معدات هبوط الطائرات المروحية حسب المنطقة الجغرافية

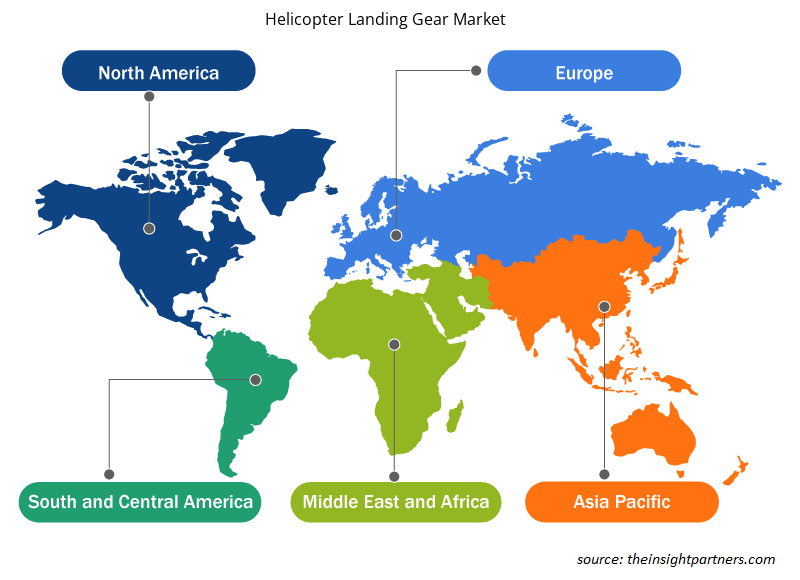

ينقسم النطاق الجغرافي لتقرير سوق معدات هبوط الطائرات المروحية بشكل أساسي إلى خمس مناطق: أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية.

سيطرت أمريكا الشمالية على السوق في عام 2023 تليها منطقتي أوروبا وآسيا والمحيط الهادئ. علاوة على ذلك، من المرجح أن تشهد منطقة آسيا والمحيط الهادئ أيضًا أعلى معدل نمو سنوي مركب في السنوات القادمة. سيطرت الولايات المتحدة على سوق معدات هبوط المروحيات في أمريكا الشمالية في عام 2023. تعد القوات الجوية الأمريكية واحدة من أقوى القوات المسلحة وأكثرها تقدمًا من الناحية التكنولوجية في العالم. تستثمر حكومة الولايات المتحدة باستمرار في تطوير قاعدة صناعية دفاعية في البلاد، وذلك بسبب التركيز الكبير على توسيع القدرات العسكرية كأولوية استراتيجية. في عام 2023، بلغ الإنفاق العسكري للولايات المتحدة 916 مليار دولار أمريكي، بزيادة قدرها 4.4 في المائة عن العام السابق. ومن المتوقع أن تكون الولايات المتحدة أكبر مساهم في الإيرادات في سوق معدات هبوط المروحيات في جميع أنحاء العالم بسبب الإنفاق المستمر على البحث والتطوير لتعزيز القطاع العسكري، فضلاً عن وجود بعض من أفضل مصنعي المروحيات القتالية ومعدات الهبوط. تعد CIRCOR Aerospace وSafran من بين الشركات المصنعة الرئيسية العاملة في سوق معدات الهبوط في الولايات المتحدة. ومن ثم، فمن المتوقع أن ينمو سوق معدات هبوط الطائرات المروحية طوال الفترة المتوقعة نتيجة للعوامل المذكورة أعلاه.

نطاق تقرير سوق معدات هبوط المروحيات

رؤى إقليمية حول سوق معدات هبوط المروحيات

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق معدات هبوط المروحيات طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق معدات هبوط المروحيات والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق معدات هبوط المروحيات

نطاق تقرير سوق معدات هبوط المروحيات

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2023 | 3.81 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 5.99 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2023 - 2031) | 5.8% |

| البيانات التاريخية | 2021-2022 |

| فترة التنبؤ | 2024-2031 |

| القطاعات المغطاة |

حسب النوع

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق معدات هبوط الطائرات المروحية: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق معدات هبوط المروحيات نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق معدات هبوط الطائرات المروحية هي:

- شركة سيركور للفضاء الجوي

- شركة سيكا إنتربلانت سيستمز المحدودة

- دارت للطيران والفضاء

- يوروكاربون بي في

- تريليبورج

- روستيك

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق معدات هبوط المروحيات

أخبار سوق معدات هبوط المروحيات والتطورات الأخيرة

يتم تقييم سوق معدات هبوط المروحيات من خلال جمع البيانات النوعية والكمية بعد البحث الأولي والثانوي، والتي تتضمن منشورات الشركات المهمة وبيانات الجمعيات وقواعد البيانات. فيما يلي بعض التطورات في سوق معدات هبوط المروحيات:

- تشارك شركة Safran Landing Systems في برنامج طائرات Tiltrotor التابع لشركة Bell، كجزء من مشروع الطائرات الهجومية بعيدة المدى المستقبلية (FLRAA) التابع للجيش الأمريكي. ووفقًا للعقد، ستقوم شركة Safran Landing Systems بتصميم وتطوير نظام الهبوط المتكامل بالكامل. وستؤدي هذه الجهود المشتركة إلى إرساء أسس متينة لتلبية جميع المتطلبات المستقبلية. (المصدر: Safran، بيان صحفي، سبتمبر 2023)

- أطلقت Trelleborg Sealing Solutions مادة Orkot® C620 المركبة، والتي تم تطويرها خصيصًا لتلبية احتياجات صناعة الطيران، وخاصة متطلبات وجود مادة قوية وخفيفة الوزن لتحمل الأحمال والضغوط العالية التي تتعرض لها معدات الهبوط. (المصدر: Trelleborg Sealing Solutions، بيان صحفي، فبراير 2022)

تقرير سوق معدات هبوط المروحيات والتغطية والنتائج المتوقعة

يقدم تقرير "حجم سوق معدات هبوط المروحيات والتوقعات (2021-2031)" تحليلاً مفصلاً للسوق يغطي المجالات التالية:

- حجم سوق معدات هبوط المروحيات وتوقعاتها على المستويات العالمية والإقليمية والوطنية لجميع قطاعات السوق الرئيسية المغطاة ضمن النطاق

- اتجاهات سوق معدات هبوط الطائرات المروحية بالإضافة إلى ديناميكيات السوق مثل العوامل المحركة والقيود والفرص الرئيسية

- تحليل مفصل لقوى بورتر الخمس

- تحليل سوق معدات هبوط المروحيات يغطي اتجاهات السوق الرئيسية والإطار العالمي والإقليمي واللاعبين الرئيسيين واللوائح والتطورات الأخيرة في السوق

- تحليل المشهد الصناعي والمنافسة الذي يغطي تركيز السوق، وتحليل خريطة الحرارة، واللاعبين البارزين، والتطورات الأخيرة لسوق معدات هبوط الطائرات المروحية

- ملفات تعريف الشركة التفصيلية

نافين خبيرٌ متمرسٌ في أبحاث السوق والاستشارات، يتمتع بخبرةٍ تزيد عن 9 سنوات في مشاريع مُخصصة ومُشتركة واستشارية. يشغل حاليًا منصب نائب الرئيس المساعد، وقد نجح في إدارة أصحاب المصلحة عبر سلسلة قيمة المشاريع، وألّف أكثر من 100 تقرير بحثي وأكثر من 30 مهمة استشارية. يمتد نطاق عمله ليشمل مشاريع صناعية وحكومية، مساهمًا بشكل كبير في نجاح العملاء واتخاذ القرارات القائمة على البيانات.

نافين حاصلٌ على شهادة في هندسة الإلكترونيات والاتصالات من جامعة فرجينيا التقنية، كارناتاكا، وشهادة ماجستير في إدارة الأعمال في التسويق والعمليات من جامعة مانيبال. وهو عضوٌ نشطٌ في معهد مهندسي الكهرباء والإلكترونيات (IEEE) لمدة 9 سنوات، حيث شارك في مؤتمراتٍ وندواتٍ تقنية، وتطوّع على مستوى الأقسام والمناطق. قبل منصبه الحالي، عمل مستشارًا استراتيجيًا مساعدًا في IndustryARC، ومستشارًا للخوادم الصناعية في شركة هيوليت باكارد (HP Global).

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق معدات هبوط المروحيات

احصل على عينة مجانية ل - سوق معدات هبوط المروحيات